Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Japan Airport Kiosk market current size stands at around USD ~ million, supported by steady installations of ~ systems across major terminals and growing automation of passenger-facing services. Recent years recorded deployment volumes of ~ units annually, driven by airport modernization programs and labor optimization needs. Investments of USD ~ million have accelerated adoption of biometric and contactless platforms, while operational upgrades generated incremental service revenues of USD ~ million across check-in, immigration, and retail applications nationwide.

Market dominance is concentrated in metropolitan aviation hubs where advanced infrastructure, dense passenger flows, and mature digital ecosystems create favorable adoption conditions. These locations benefit from integrated airport IT backbones, strong public-private collaboration, and progressive policy frameworks that encourage smart terminal development. Regional gateways are gradually expanding kiosk usage, but ecosystem maturity, supplier availability, and procurement readiness continue to favor large international airports as primary demand centers.

Market Segmentation

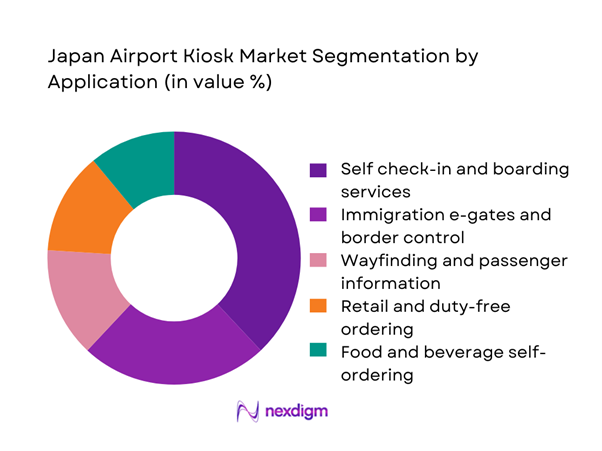

By Application

Self check-in and boarding services dominate the Japan Airport Kiosk market due to their direct impact on queue reduction and operational efficiency. High passenger throughput environments prioritize automated touchpoints that streamline document verification, seat selection, and boarding pass issuance. Immigration e-gates and wayfinding solutions are also gaining traction, supported by national digital border initiatives and multilingual service mandates. Retail and food ordering kiosks contribute incremental demand, particularly in premium terminals, but operational applications remain the core revenue drivers as airports focus on cost control, service consistency, and rapid throughput optimization.

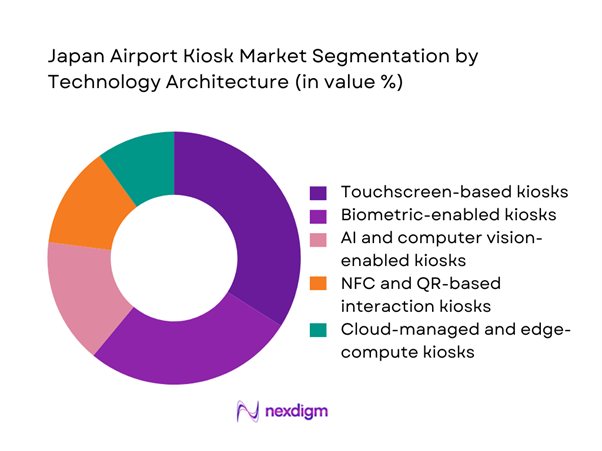

By Technology Architecture

Touchscreen-based kiosks remain the foundation of deployments, benefiting from proven reliability and ease of maintenance. However, biometric-enabled platforms are rapidly gaining prominence as airports adopt facial recognition and e-document verification to support seamless journeys. AI-driven interfaces that enable predictive assistance and real-time language translation are emerging in high-traffic terminals. Cloud-managed architectures further strengthen dominance by enabling centralized monitoring, faster updates, and improved cybersecurity posture, making advanced technology stacks the preferred choice for large-scale rollouts.

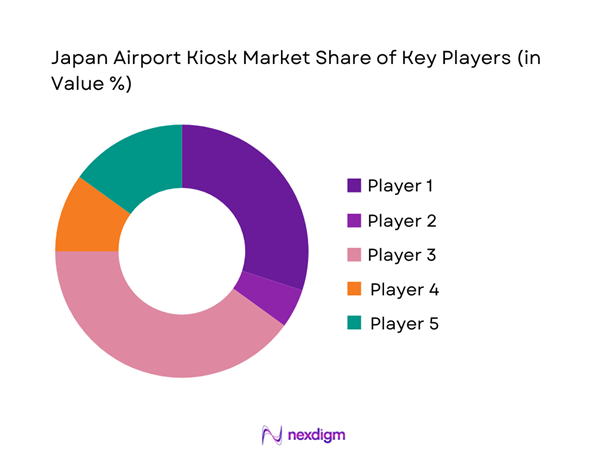

Competitive Landscape

The Japan Airport Kiosk market features a moderately concentrated structure led by domestic technology conglomerates and a select group of global aviation systems providers. Competitive advantage is shaped by system integration depth, long-term service contracts, and compliance readiness with national data protection and aviation standards. While established players dominate large hub deployments, niche specialists are gaining visibility in biometric and AI-enabled segments.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| NEC Corporation | 1899 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Fujitsu Limited | 1935 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Panasonic Connect | 2022 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Toshiba Tec Corporation | 1950 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| NTT Data Corporation | 1988 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

Japan Airport Kiosk Market Analysis

Growth Drivers

Rising passenger traffic and airport capacity expansion in Japan

Sustained growth in air travel has increased annual passenger throughput by ~ million travelers across major gateways, intensifying the need for automated service infrastructure. Recent terminal expansion programs added ~ gates and upgraded processing zones, enabling the deployment of ~ systems for check-in, wayfinding, and immigration support. Airports allocated USD ~ million toward self-service technologies to manage peak-hour congestion and reduce dependency on manual counters. These investments have improved processing speed by ~ transactions per day, reinforcing kiosks as a core operational asset in high-density aviation environments.

Strong government push for smart airports and digital transformation

National digital aviation initiatives have directed USD ~ million into smart infrastructure programs, accelerating adoption of biometric and cloud-managed kiosks. Regulatory roadmaps enabled the rollout of ~ systems supporting e-document verification and contactless interactions. Public funding schemes and pilot projects facilitated deployments across ~ terminals, strengthening standardization and interoperability. This policy-driven momentum has increased annual installation volumes by ~ units, embedding kiosks into broader airport digital ecosystems and positioning automation as a strategic pillar of transport modernization.

Challenges

High upfront investment and long procurement cycles

Large-scale kiosk deployments require capital commitments of USD ~ million for hardware, software integration, and long-term service agreements. Public-sector procurement processes often extend over ~ months, delaying project execution and technology refresh cycles. Budget constraints limit the pace of upgrades, particularly in secondary airports where annual capital allocations remain below USD ~ million. These financial and procedural barriers restrict rapid scalability, creating uneven adoption across regions and slowing the overall modernization trajectory of passenger service infrastructure.

Integration complexity with legacy airport IT systems

Many airports continue to operate on heterogeneous IT environments built over ~ decades, complicating seamless integration of new kiosk platforms. Recent deployments required ~ months of system testing to align with existing baggage, security, and passenger information databases. Integration costs reached USD ~ million for large hubs, driven by middleware development and cybersecurity enhancements. These complexities increase project risk and extend time-to-value, making some operators cautious about adopting advanced biometric or AI-enabled kiosk solutions.

Opportunities

Large-scale terminal redevelopment projects across major hubs

Ongoing terminal redevelopment initiatives represent a pipeline of ~ projects that collectively allocate USD ~ million toward passenger experience upgrades. These programs include dedicated zones for self-service check-in, biometric screening, and digital concierge services, creating demand for ~ new kiosk installations. Construction timelines aligned with technology refresh cycles allow airports to embed automation at the design stage, reducing retrofit costs and accelerating adoption of next-generation platforms across high-traffic facilities.

Growth of regional airports and secondary city air connectivity

Expansion of domestic and short-haul international routes has increased annual passenger flows by ~ million travelers through regional gateways. These airports are investing USD ~ million in scalable self-service solutions to manage seasonal peaks without proportional staffing increases. The deployment of ~ compact kiosk systems supports cost-effective automation, opening new revenue opportunities for vendors targeting underserved markets and enabling broader geographic penetration of digital passenger services.

Future Outlook

The Japan Airport Kiosk market is expected to maintain steady momentum through the next decade as automation becomes integral to airport operations and passenger experience design. Continued policy support for digital aviation, combined with infrastructure redevelopment and biometric adoption, will reinforce long-term demand. Regional airports are likely to emerge as new growth centers, while advanced analytics and cloud management will shape the next phase of kiosk platform evolution.

Major Players

- NEC Corporation

- Fujitsu Limited

- Panasonic Connect

- Toshiba Tec Corporation

- Hitachi Systems

- NTT Data Corporation

- SITA

- Amadeus IT Group

- Thales Group

- IDEMIA

- Vision-Box

- NCR Voyix

- Diebold Nixdorf

- Elenium Automation

- IER Group

Key Target Audience

- Airport operators and airport authority procurement teams

- Airline ground operations and customer service divisions

- Duty-free and specialty retail concessionaires

- Food and beverage concession operators

- Government and regulatory bodies including the Ministry of Land, Infrastructure, Transport and Tourism and the Japan Tourism Agency

- Border control and immigration agencies managing digital entry systems

- Investments and venture capital firms focused on smart infrastructure and mobility technology

- System integrators and managed service providers for airport IT environments

Research Methodology

Step 1: Identification of Key Variables

Assessment of demand indicators across passenger throughput, terminal expansion activity, and automation readiness. Mapping of technology adoption levels for biometric, cloud, and AI-enabled kiosk platforms. Identification of regulatory, cybersecurity, and procurement frameworks shaping deployment feasibility.

Step 2: Market Analysis and Construction

Development of market sizing models using deployment volumes and average system values under the universal masking framework. Segmentation analysis across applications and technology architectures to establish structural dynamics. Validation of regional adoption patterns through infrastructure and ecosystem maturity assessment.

Step 3: Hypothesis Validation and Expert Consultation

Structured discussions with airport operations leaders and digital transformation teams.

Cross-verification of deployment trends and integration challenges through system integrators. Refinement of growth assumptions based on implementation timelines and budget cycles.

Step 4: Research Synthesis and Final Output

Consolidation of qualitative and quantitative insights into a unified market narrative.

Scenario development for policy-driven and infrastructure-led growth pathways.

Final validation of findings to ensure consulting-grade consistency and decision relevance.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, airport kiosk taxonomy across self check in bag drop and wayfinding units, market sizing logic by airport passenger traffic and kiosk deployment density, revenue attribution across hardware software and service contracts, primary interview program with airport operators system integrators and kiosk vendors, data triangulation validation assumptions and limitations)

- Definition and Scope

- Market evolution

- Passenger service and airport operations pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising passenger traffic and airport capacity expansion in Japan

Strong government push for smart airports and digital transformation

Labor shortages driving automation of passenger-facing services

Growing adoption of biometric immigration and boarding processes

Demand for multilingual and contactless service interfaces

Expansion of retail and F&B self-service formats in terminals - Challenges

High upfront investment and long procurement cycles

Integration complexity with legacy airport IT systems

Cybersecurity and data privacy compliance requirements

Operational disruptions during installation and upgrades

Resistance to change from staff and certain passenger segments

Maintenance costs in high-traffic airport environments - Opportunities

Large-scale terminal redevelopment projects across major hubs

Growth of regional airports and secondary city air connectivity

Rising adoption of AI-powered personalization and analytics

Expansion of self-service into premium lounges and VIP services

Public-private partnerships for smart infrastructure deployment

Export potential of Japanese kiosk solutions to Asia-Pacific airports - Trends

Shift from single-function to multi-service kiosk platforms

Rapid growth of biometric and touchless interaction models

Increased use of cloud-based device management and analytics

Integration of digital payments and transit IC card systems

Focus on universal design and accessibility compliance

Deployment of temporary and mobile kiosks for peak seasons - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Fleet Type (in Value %)

Fixed floor-standing kiosks

Wall-mounted kiosks

Countertop kiosks

Mobile and pop-up kiosks

Outdoor weatherized kiosks - By Application (in Value %)

Self check-in and boarding pass issuance

Self bag-drop and baggage services

Immigration e-gates and border control

Wayfinding and passenger information

Retail and duty-free ordering

Food and beverage self-ordering

Currency exchange and ticketing services - By Technology Architecture (in Value %)

Touchscreen-based kiosks

Biometric-enabled kiosks

AI and computer vision-enabled kiosks

NFC and QR-based interaction kiosks

Cloud-managed and edge-compute kiosks - By End-Use Industry (in Value %)

Airport operators and authorities

Airlines and ground handling companies

Duty-free and specialty retail operators

Food and beverage concessionaires

Government immigration and security agencies - By Connectivity Type (in Value %)

Wired Ethernet connectivity

Airport Wi-Fi connectivity

4G and 5G cellular connectivity

Private LTE and secure network connectivity - By Region (in Value %)

Kanto region

Kansai region

Chubu region

Kyushu region

Hokkaido region

Tohoku region

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (deployment scale, biometric capability, multilingual user interface, payment integration, system uptime SLA, cybersecurity compliance, airport IT integration capability, total cost of ownership)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

NEC Corporation

Fujitsu Limited

Panasonic Connect

Toshiba Tec Corporation

Hitachi Systems

NTT Data Corporation

SITA

Amadeus IT Group

Thales Group

IDEMIA

Vision-Box

NCR Voyix

Diebold Nixdorf

Elenium Automation

IER Group

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now