Download PDF

Download PDF Download PDF

Download PDFJapan Business Jet Market Overview

The Japan Business Jet market is valued at approximately USD ~ billion in 2025, driven by a combination of factors, including a significant increase in high-net-worth individuals (HNWIs), growing demand for corporate air travel, and Japan’s robust economy. The aviation sector in Japan is poised for expansion, with a rising preference for personalized and private travel experiences, particularly for business executives. This growth is further fueled by technological advancements in aircraft manufacturing, the rise of on-demand charter services, and the growing trend towards cost-effective fractional ownership models.

Japan’s business jet market is primarily dominated by key metropolitan areas such as Tokyo, Osaka, and Fukuoka. Tokyo, as a financial hub, houses the highest concentration of HNWIs and corporate headquarters, making it the epicenter of demand for business aviation services. Osaka, with its proximity to major industrial sectors, also sees significant demand, particularly for corporate air travel. Fukuoka, while smaller, has been emerging due to its growing business infrastructure and increasing international connectivity. These cities dominate due to their economic significance, infrastructure development, and higher disposable income levels.

Market Segmentation

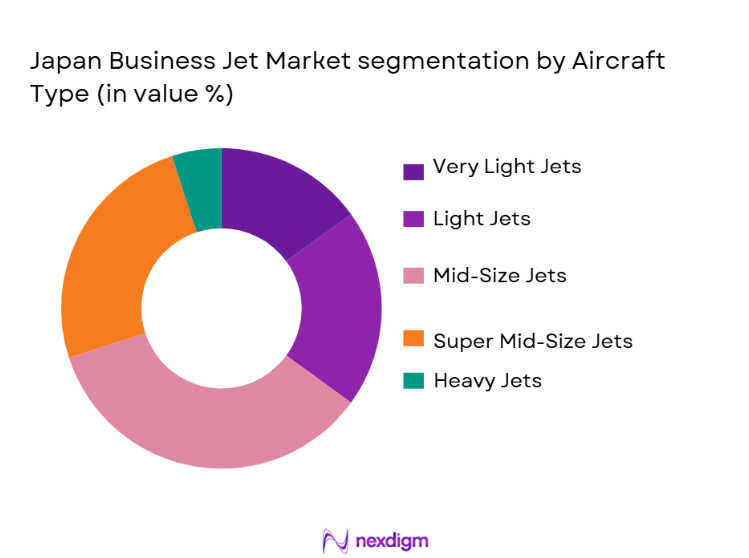

By Aircraft Type

The Japan Business Jet market is segmented by aircraft type into Very Light Jets (VLJ), Light Jets, MidSize Jets, Super MidSize Jets, and Heavy Jets. In recent years, MidSize Jets have witnessed significant market dominance. These aircraft offer a balanced combination of range, comfort, and operating cost efficiency, making them ideal for both business executives and companies looking for flexible solutions. Companies such as Gulfstream and Bombardier have established strong presences in this segment, providing advanced models with significant range capabilities to meet both domestic and international demand.

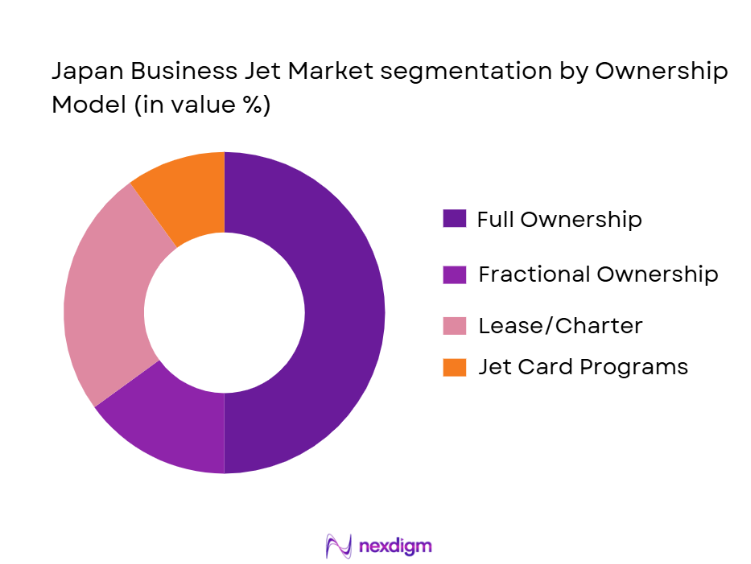

By Ownership Model

Japan’s business jet market is also segmented by ownership model, including Full Ownership, Fractional Ownership, Lease / Charter, and Jet Card Programs. The dominant segment in Japan is Full Ownership, driven by the high number of corporate clients and affluent individuals preferring control and flexibility. Full ownership provides businesses with complete autonomy over aircraft schedules and maintenance, which is particularly beneficial for large corporations and government agencies with frequent travel needs. The ease of access to private airfields and the growing availability of support services have contributed to the increased popularity of this model.

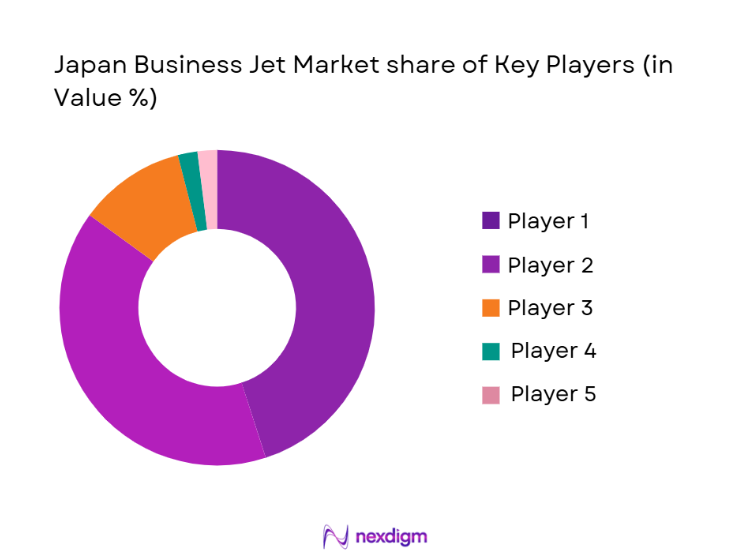

Competitive Landscape

The Japan Business Jet market is characterized by the dominance of several key international and local players. Major global aircraft manufacturers such as Gulfstream, Bombardier, and Dassault Aviation play a pivotal role in shaping the market landscape. Additionally, charter operators like ANA Business Jet and Japan Airlines’ corporate fleet offer business jet services catering to both corporate clients and affluent individuals. The market is consolidating around these players, given their strong brand recognition, after-sales support networks, and strategic positioning in the major metropolitan areas.

| Company | Establishment Year | Headquarters | Fleet Size | Annual Revenue (USD) | Product Range | Service Offering |

| Gulfstream Aerospace | 1958 | Savannah, Georgia | ~ | ~ | ~ | ~ |

| Bombardier Aerospace | 1942 | Montreal, Canada | ~ | ~ | ~ | ~ |

| Dassault Aviation | 1929 | Paris, France | ~ | ~ | ~ | ~ |

| ANA Business Jet | 1952 | Tokyo, Japan | ~ | ~ | ~ | ~ |

| Japan Airlines (JAL) | 1951 | Tokyo, Japan | ~ | ~ | ~ | ~ |

Japan Business Jet Market Analysis

Growth Drivers

Increasing Demand for Corporate Air Travel

Japan’s robust economy, alongside a rising number of high-net-worth individuals (HNWIs), continues to fuel the demand for business jets. With an increasing number of business executives and corporations seeking flexible and time-efficient travel options, corporate air travel is becoming a critical mode of transportation for high-level professionals and international business dealings.

Technological Advancements in Aircraft

Continuous innovations in aircraft technology, such as improved fuel efficiency, enhanced comfort, and longer ranges, are driving growth in the market. New models offer greater flexibility and reduced operational costs, making them increasingly attractive to both large corporations and private owners.

Market Challenges

High Operational and Maintenance Costs

The cost of maintaining a business jet is significant, including fuel, personnel, and regular maintenance. These high operating costs can deter new entrants, especially in a competitive market like Japan, where cost efficiency remains a concern for many businesses and owners.

Regulatory Barriers and Airspace Congestion

Stringent regulatory requirements, along with airspace congestion in busy regions like Tokyo, can limit the operational flexibility of business jets. Navigating complex air traffic regulations and securing landing rights can be time-consuming and costly for operators, thus slowing down market expansion.

Opportunities

Expansion of On-Demand Charter Services

The growth of on-demand business jet services, such as fractional ownership and jet card programs, presents a major opportunity for market expansion. With businesses increasingly opting for flexible travel solutions that do not require full ownership, the charter segment has the potential to cater to a broader clientele.

Sustainability and Green Aviation Technologies

There is a rising demand for environmentally friendly travel solutions. The Japan business jet market presents an opportunity for growth through the integration of sustainable aviation fuels (SAF) and electric aircraft technologies. As global pressure to reduce carbon emissions increases, adopting green technologies will not only attract environmentally conscious customers but also help comply with tightening regulations on emissions.

Future Outlook

Over the next six years, the Japan Business Jet market is expected to show sustained growth, driven by the increasing number of high-net-worth individuals and businesses seeking greater flexibility in their travel options. The adoption of fractional ownership and on-demand charter services will further bolster market growth. Additionally, advancements in sustainable aviation technologies, such as the integration of SAF (sustainable aviation fuel) and electric aircraft, will likely become more prominent in the industry. The regulatory landscape will also evolve to support green aviation initiatives and enhance the ease of operations for private jet owners.

Major Players

- Gulfstream Aerospace

- Bombardier Aerospace

- Dassault Aviation

- ANA Business Jet

- Japan Airlines (JAL)

- Textron Aviation (Cessna)

- Embraer

- Airbus Corporate Jets

- Boeing Business Jets

- Mitsubishi Aircraft Corporation

- Honda Aircraft Company

- NetJets

- Wheels Up

- Flexjet

- Global Jet Services

Key Target Audience

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Corporate Executives and High Net-Worth Individuals (HNWI)

- Private Jet Charter Companies

- Aircraft Leasing Companies

- Aviation Manufacturers

- Aviation Maintenance and MRO Providers

- Tourism and Luxury Service Providers

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves identifying the major stakeholders in the Japan Business Jet market, such as OEMs, operators, and regulatory bodies. This step combines secondary data from databases like ICAO and local civil aviation reports with proprietary market insights, aiming to recognize variables that influence demand and competition.

Step 2: Market Analysis and Construction

We will compile and analyze historical data from Japan’s business aviation sector, assessing the number of business jets registered, fleet utilization rates, and regional demand patterns. This phase also includes evaluating market penetration and analyzing the geographical distribution of business jet services within Japan.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be tested through interviews with industry experts, including executives from leading OEMs and operators, as well as government regulators. These consultations will verify the assumptions underlying our forecasts and provide additional insights into the future trajectory of the business jet market in Japan.

Step 4: Research Synthesis and Final Output

The final stage synthesizes data obtained through both top-down and bottom-up methodologies, offering a complete view of the market. Insights will be drawn from interviews with key decision-makers in the aviation industry, OEMs, and operators to ensure the robustness of the analysis and to provide a comprehensive, validated market outlook.

- Executive Summary

- Research Methodology (Definition and Scope of Business Jet Market, Data Sources and Validation, Market Sizing Approach, Model Assumptions, Fleet Registry Data Normalization, Primary Research and Expert Horizon Scanning, Forecasting Model)

- Industry Definition and Scope

- Historical Genesis of Business Aviation in Japan

- Lifecycle and Business Jet Utilization Patterns

- Regulatory and Certification Landscape

- Operator and FBO Infrastructure Configuration

- Growth Drivers

Affluence Expansion and Corporate Travel Demand

Domestic and Regional Intercity Connectivity Gaps

HNWI Penetration and TimeEfficiency Premium

Infrastructure Development (FBOs & Business Jet Terminals) - Market Challenges

High Operating Cost (Fuel + Maintenance)

Pilot and Crew Availability Constraints

Airport Slot and Airspace Congestion

Regulatory Barriers for International Charter - Opportunities

Emerging OnDemand Business Jet Services (Air Taxi / Jet Card)

Fractional Ownership & Secondary Market Liquidity

Sustainability (SAF Integration, Emissions Metrics) - Industry Trends

Shift Toward Light and Very Light Jets for Cost Efficiency

Growth of Charter and Subscription Models

Digitalization of Flight Operations and CRM - Regulatory & Compliance Structure

JCAB Certification Requirements

Noise and Emission Standards

Safety and Crew Licensing Framework

- Market Value 2020-2025

- Fleet Registry Count 2020-2025

- Delivery Volume 2020-2025

- Average Pricing Trends 2020-2025

- By Aircraft Type (In Value %)

Very Light Jets

Light Jets

MidSize Jets

Super MidSize Jets

Heavy Jets - By Ownership Model (In Value%)

Full Ownership

Fractional Ownership

Lease / Charter Operators

Jet Card Programs - By Range Classification (In Value%)

< 3000 NM (Domestic / ShortHaul Premium Travel)

3000–5000 NM (Regional APAC Connectivity)

> 5000 NM (Intercontinental Corporate Travel) - By EndUse (In Value%)

Corporate / Enterprise Travel

Charter and OnDemand Operators

VIP / Government / Diplomatic Usage

High NetWorth Individuals (HNWI) Personal Travel

Training / Support Fleet Utilization - By Sales Channel (In Value%)

OEM Direct Sourcing

Preowned Aircraft Exchange

Aviation Brokers and Dealers

Fractional Network Providers

- Market Share

- Cross Comparison Parameters (Company Profile, Business Strategy, Fleet Focus, Range Portfolio, Engine Type Metrics, Sales & Service Network, AfterSale Support, MRO Capability, Pricing & Residual Value, Distribution Network, Fractional / Charter Footprint, Tech Adoption Level, Safety Ratings)

- SWOT Analysis — Key OEMs & Operators

- Major Competitors

Honda Aircraft Company

Bombardier Aerospace

Gulfstream Aerospace

Textron Aviation

Dassault Aviation

Embraer Executive Jets

Boeing Business Jets

Airbus Corporate Jets

Japan Civil Aviation Leasing & Charter Providers

PanPacific Jet Charter Operators

Fractional Network Operators

PreOwned Aircraft Dealers

FBO Network Operators in Japan

Aircraft Management & Charter Firms

Maintenance & MRO Specialists

- Utilization Patterns

- Purchasing Decision Drivers

- Budget Allocation Trends

- Pain Points: Turnaround Time, Slot Access, Maintenance Windows

- Decision Hierarchy and Flight Planner Roles

- Value Projection Modeling 2026-2035

- Fleet & Deliveries Outlook 2026-2035

- Utilization Forecast by Segment 2026-2035

- Price Trend Prediction 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now