Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Japan medical devices market is valued at approximately USD ~ billion, driven by the increasing healthcare needs of an aging population, technological advancements, and government initiatives promoting healthcare innovation. This growth is further supported by high demand for advanced diagnostic and therapeutic devices, especially in hospitals and outpatient care centers. Continuous innovations in medical technologies, such as minimally invasive surgeries and robotics, also play a crucial role in the market’s expansion. The rise of preventive healthcare is also a key factor contributing to the adoption of various medical devices.

Japan’s dominance in the medical devices sector is attributed to its robust healthcare infrastructure, significant investments in medical technology, and high standards of medical care. Major urban centers like Tokyo, Osaka, and Yokohama are at the forefront of driving market growth due to the concentration of hospitals, research institutions, and advanced healthcare facilities. Japan’s strong regulatory environment and government support for healthcare innovation also contribute to its position as a leader in the Asia-Pacific medical devices market. Technological advancements, along with increased consumer awareness and demand for health monitoring, are expected to further enhance Japan’s market leadership.

Market Segmentation

By Product Type

The Japan medical devices market is segmented by product type into diagnostic imaging devices, surgical instruments, orthopedic devices, in-vitro diagnostic devices, and patient monitoring devices. Among these, diagnostic imaging devices have a dominant market share due to the increasing prevalence of chronic diseases such as cancer and cardiovascular conditions, which require early detection and accurate diagnosis. The high adoption rate of advanced imaging technologies, such as MRI and CT scans, combined with the growing healthcare infrastructure, fuels the demand for these devices. Furthermore, technological advancements like 3D imaging and AI-driven diagnostics are enhancing the capabilities of these devices, further driving their dominance.

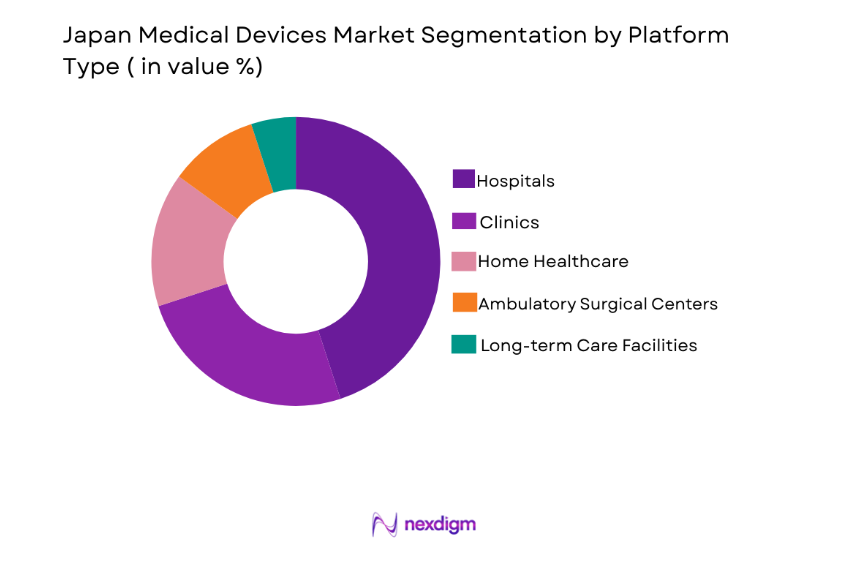

By Platform Type

The Japan medical devices market is segmented by platform type into hospitals, clinics, home healthcare, ambulatory surgical centers, and long-term care facilities. Among these, hospitals have a dominant market share due to their comprehensive healthcare services, advanced medical technologies, and high patient volume. Hospitals are the primary location for most medical procedures, including surgeries, diagnostic imaging, and intensive care, leading to a higher demand for various medical devices. The presence of highly specialized departments, such as cardiology and neurology, further drives the demand for specialized medical equipment in hospitals. Additionally, the continuous advancements in hospital infrastructure contribute to the growing adoption of innovative devices.

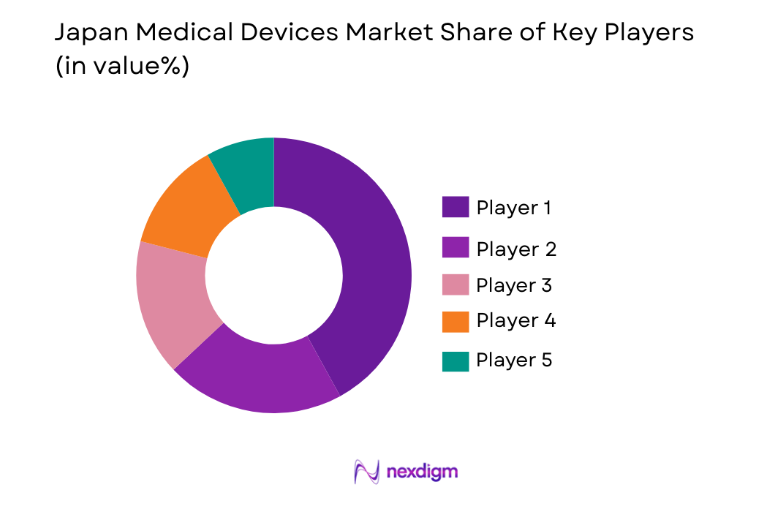

Competitive Landscape

The competitive landscape of Japan’s medical devices market is characterized by both international and domestic companies. Major players in the market continuously innovate and adopt advanced technologies to maintain their market share. There is also a trend of consolidation, with large companies acquiring smaller players to expand their product portfolios and market reach. The presence of well-established brands with a strong distribution network further intensifies competition. These companies focus on offering comprehensive solutions that cater to a wide range of healthcare needs, from diagnostics to therapeutics, positioning themselves for long-term growth in a highly competitive market.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Market Parameter |

| Terumo Corporation | 1921 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ |

| Olympus Corporation | 1919 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ |

| Hitachi, Ltd. | 1910 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ |

| Fujifilm Holdings Corporation | 1934 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ |

| Nipro Corporation | 1954 | Osaka, Japan | ~ | ~ | ~ | ~ | ~ |

Japan Medical Devices Market Analysis

Growth Drivers

Aging Population

Japan’s rapidly aging population is a major driver of the medical devices market, as the number of elderly individuals continues to increase, creating a significant demand for medical devices tailored to age-related health issues. Common conditions such as cardiovascular diseases, diabetes, and arthritis are rising among the elderly, requiring advanced diagnostic and therapeutic devices. As chronic diseases become more prevalent, the healthcare system faces increasing pressure to provide long-term care and efficient management. This has led to greater investment in medical technologies, including devices for remote monitoring, mobility aids, and advanced treatment solutions to help manage these conditions effectively. Furthermore, the aging population results in a higher need for rehabilitation and home care devices, contributing to the growth of the market. With the elderly population growing rapidly, the demand for specialized medical devices to manage these conditions will continue to rise, propelling the market forward.

Technological Advancements

Continuous advancements in medical technologies are significantly driving the growth of Japan’s medical devices market. Innovations in imaging technologies, robotics, and minimally invasive surgeries have improved patient outcomes while reducing the invasiveness and recovery times associated with procedures. The emergence of AI-driven diagnostic tools, particularly in imaging and disease detection, is improving the precision of diagnostics, enabling earlier and more accurate detection of various diseases, which is essential for effective treatment. Additionally, developments in personalized medicine, where devices are tailored to an individual’s specific medical needs, are expected to further drive market growth. Telemedicine, remote monitoring systems, and wearable health devices are also becoming more integrated into Japan’s healthcare ecosystem, enabling patients to manage their health and receive care outside of traditional hospital settings. As these technologies evolve, the ability to offer more efficient and cost-effective healthcare will contribute to the continued expansion of the medical device market.

Market Challenges

Regulatory Hurdles

Japan has one of the most stringent regulatory environments for medical devices in the world. The rigorous approval processes, including extensive clinical trials and documentation, can significantly delay the market entry of new products, hindering market growth. The long approval timelines, often taking several years, and the high costs involved in meeting regulatory requirements create a barrier for smaller companies looking to enter the market. Moreover, medical devices must meet Japan’s high-quality standards for safety and efficacy, which requires substantial investment in quality control and compliance. These regulatory challenges can create delays in the introduction of innovative products, limiting the speed at which new technologies can reach the market. While this regulatory structure ensures patient safety, it also makes it difficult for companies to keep up with the fast pace of technological advancements and market demands.

High Costs of Advanced Medical Devices

Despite Japan’s leadership in the medical technology sector, the high cost of advanced medical devices presents a significant challenge for both healthcare providers and patients. The importation of specialized medical equipment and the expenses associated with maintenance, training, and integration into existing healthcare systems contribute to the financial burden. Public healthcare systems in Japan, although comprehensive, face budget constraints that make it difficult to adopt and implement the latest medical technologies across all levels of care. This high cost also limits access to certain devices, particularly in rural areas where healthcare facilities may lack the funds for new investments. Additionally, the ongoing need for updates and specialized training for medical professionals further elevates the costs. As medical devices become more complex, their price tags continue to rise, limiting their widespread adoption and making it more difficult for healthcare systems to keep pace with technological advancements.

Opportunities

Home Healthcare Solutions

The growing demand for home healthcare presents a significant opportunity for the medical devices market in Japan. With the elderly population increasing and more individuals seeking personalized and convenient care, there is a rising need for home-based healthcare solutions. Devices such as remote monitoring systems, wearable health trackers, and home dialysis units are gaining traction among consumers and healthcare providers. These devices enable patients to receive care in the comfort of their homes, reducing the burden on healthcare facilities and improving overall patient satisfaction. Furthermore, home healthcare is being supported by technological advancements such as telemedicine, which allows healthcare providers to remotely monitor patients and offer consultations without requiring in-person visits. This shift toward at-home care, combined with Japan’s well-established healthcare infrastructure, positions the country to benefit from the increasing demand for home healthcare devices. As more elderly individuals prefer to manage their health from home, this sector is expected to experience significant growth, providing a fertile ground for the development and expansion of medical devices designed for home use.

AI and Robotics in Healthcare

The integration of artificial intelligence (AI) and robotics into medical devices offers a wealth of opportunities for market expansion in Japan. AI-powered diagnostic systems and robotic surgeries are gaining momentum due to their ability to reduce human error, improve precision, and enhance patient outcomes. AI-driven algorithms enable faster and more accurate interpretation of medical imaging, while robotic systems allow for minimally invasive procedures that improve recovery times and reduce complications. The growing demand for personalized treatment plans also opens up opportunities for AI to assist in customizing therapies based on individual patient data. Additionally, robotic surgeries and automation in medical procedures are helping healthcare providers achieve higher efficiency levels, reduce costs, and improve operational workflows. As Japan continues to embrace technological advancements in healthcare, the integration of AI and robotics into medical devices is expected to significantly transform the market. The increasing adoption of these technologies will drive demand for next-generation medical devices, making them essential tools in the future of healthcare in Japan.

Future Outlook

The Japan medical devices market is expected to continue its growth trajectory over the next five years, driven by the ongoing advancements in medical technology, an aging population, and increasing healthcare demand. The government’s continued investment in healthcare infrastructure, particularly in high-tech medical devices, will further bolster market expansion. With technological innovations such as AI and robotics becoming integral to Japan’s healthcare sector, the market is poised to experience significant developments, particularly in the areas of diagnostics, surgery, and patient monitoring.

Major Players

- Terumo Corporation

- Olympus Corporation

- Hitachi, Ltd.

- Fujifilm Holdings Corporation

- Nipro Corporation

- Medtronic Plc

- Stryker Corporation

- GE Healthcare

- Siemens Healthineers

- Canon Medical Systems Corporation

- Johnson & Johnson Medical Devices

- Abbott Laboratories

- Boston Scientific Corporation

- Philips Healthcare

- Baxter International

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers and hospital groups

- Medical device distributors

- Pharmaceutical companies

- Technology providers in healthcare

- Insurance companies

Research Methodology

Step 1: Identification of Key Variables

The key variables impacting the market, such as regulatory standards, technological advancements, and demographic factors, are identified for analysis.

Step 2: Market Analysis and Construction

A thorough market analysis is conducted using both primary and secondary data sources to build a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations and market feedback are used to validate initial hypotheses and refine the research framework.

Step 4: Research Synthesis and Final Output

The synthesized data is used to create actionable insights and deliver the final report to stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Aging Population and Increasing Chronic Diseases

Technological Advancements in Medical Devices

Government Initiatives and Healthcare Investment - Market Challenges

High Regulatory and Certification Barriers

Cost of Advanced Medical Devices

Limited Reimbursement for Certain Devices - Market Opportunities

Expansion in Home Healthcare Solutions

Growth in Diagnostic and Monitoring Devices

Rising Demand for Minimally Invasive Procedures - Trends

Integration of AI in Medical Devices

Increase in Remote Patient Monitoring - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Diagnostic Imaging Devices

Surgical Instruments

Patient Monitoring Devices

Orthopedic Devices

In Vitro Diagnostic Devices - By Platform Type (In Value%)

Hospitals

Clinics

Home Healthcare

Ambulatory Surgical Centers

Long-Term Care Facilities - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions - By End User Segment (In Value%)

Hospitals

Clinics

Home Care Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, System Complexity Tier, Region)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Terumo Corporation

Olympus Corporation

Hitachi, Ltd.

Fujifilm Holdings Corporation

Nipro Corporation

Mitsubishi Electric Corporation

Panasonic Corporation

SHIMADZU CORPORATION

Canon Medical Systems Corporation

Johnson & Johnson Medical Devices

Medtronic Plc

Stryker Corporation

GE Healthcare

Siemens Healthineers

Abbott Laboratories

- Increasing Demand for Diagnostic Devices

- Hospitals Increasingly Investing in High-End Technologies

- Rising Demand for Home Healthcare Devices

- Expanding Ambulatory Surgical Centers Market

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now