Download PDF

Download PDF Download PDF

Download PDFMarket Overview

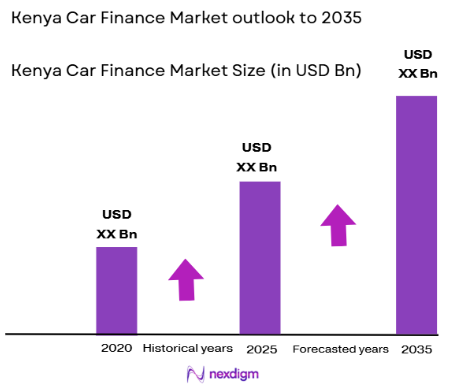

The Kenyan car finance market has seen considerable growth, driven by factors such as increased access to financing, rising vehicle demand, and a growing middle class. The market size is valued at approximately USD ~ billion in recent assessments, with steady growth observed due to expanding consumer credit and the ongoing shift towards private vehicle ownership. The role of financial institutions, mobile money platforms, and government incentives are pivotal in supporting this expansion, making car finance more accessible to various income groups across the nation. This dynamic market is expected to continue its expansion with increased competition and innovations in financing options.

The Kenyan car finance market is particularly dominant in major urban areas such as Nairobi, Mombasa, and Kisumu. Nairobi, as the capital, is the primary hub for vehicle purchases, supported by its high population density and the growing economy, which drives consumer demand for automobiles. Additionally, Mombasa, as the country’s port city, plays a significant role due to the influx of imported vehicles. These regions benefit from better access to financial services, a wider variety of car models, and stronger infrastructure for facilitating car purchases.

Market Segmentation

By Product Type:

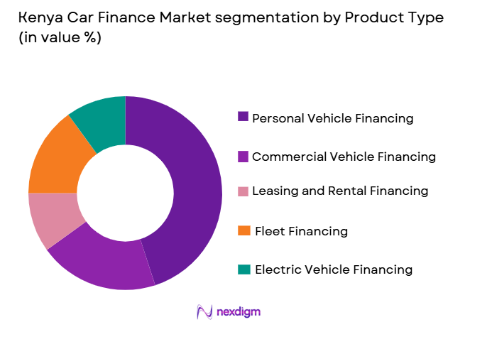

The Kenya car finance market is segmented by product type into personal vehicle financing, commercial vehicle financing, leasing and rental financing, fleet financing, and electric vehicle financing. Recently, personal vehicle financing has a dominant market share due to factors such as growing consumer demand, the expansion of mobile financing platforms like M-Pesa, and government incentives aimed at encouraging vehicle ownership. Consumer preference for personal vehicle ownership has been further boosted by easier access to affordable financing options and favorable repayment terms, making this sub-segment a key driver of market growth.

By Platform Type:

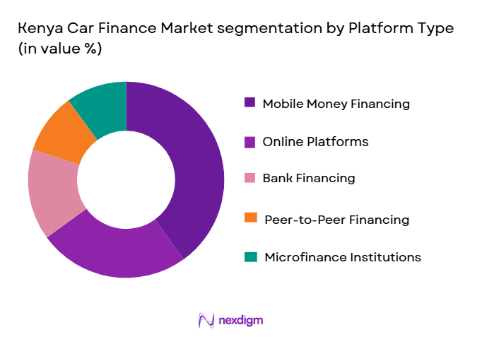

The Kenya car finance market is segmented by platform type into online platforms, bank financing, microfinance institutions, peer-to-peer financing, and mobile money financing. Recently, mobile money financing has emerged as a dominant sub-segment, largely driven by the widespread use of mobile money services like M-Pesa and Airtel Money. These platforms offer a convenient and fast way for consumers to access car financing, and their widespread adoption across rural and urban areas has made them a preferred method of financing for many individuals. The ease of use and accessibility of mobile platforms have contributed to this trend, making it a critical part of the overall market structure.

Competitive Landscape

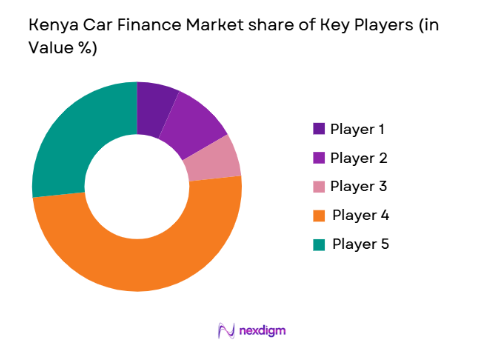

The competitive landscape in Kenya’s car finance market is driven by a combination of local banks, microfinance institutions, and mobile payment platforms. Major players in the market have been focusing on product diversification, such as offering tailored financing options for both low-income and middle-income groups. There is growing consolidation within the market, with financial institutions and mobile platforms seeking to integrate their services with car dealerships and automotive companies to capture more market share. The influence of mobile operators like Safaricom (through M-Pesa) and traditional banks is prominent, with a growing focus on digital and flexible financing solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| Safaricom | 1997 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| KCB Group | 1896 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| Equity Bank | 1984 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| M-Omnibus | 2014 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| Family Bank | 1984 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

Kenya Car Finance Market Analysis

Growth Drivers

Increasing Middle-Class Affluence:

The growing middle-class population in Kenya has been a significant driver of the car finance market. As disposable income increases, more consumers are able to afford private vehicles, and financing options have become more accessible, particularly through digital platforms like M-Pesa. The rise of middle-class families seeking reliable transportation solutions, combined with government subsidies and favorable loan conditions, has spurred demand for car loans. This demographic shift is expected to continue driving the market as urbanization and economic growth create more opportunities for financial products tailored to the growing consumer base.

Expanding Access to Financial Services:

The expansion of financial inclusion, especially through mobile banking and digital payment platforms, has played a vital role in expanding the reach of car financing. Mobile services like M-Pesa and Airtel Money allow consumers, especially those in rural areas, to access car loans without needing a traditional banking relationship. These platforms are highly effective at disbursing loans quickly and efficiently, allowing consumers to access financing for vehicle purchases that were once beyond their reach. The widespread availability of mobile-based financing solutions is a key factor in the accelerating growth of the Kenyan car finance market, contributing to greater accessibility for underserved populations.

Market Challenges

High Interest Rates and Loan Default Rates:

One of the primary challenges facing Kenya’s car finance market is the high interest rates associated with car loans. Financial institutions often impose high-interest rates, making it difficult for low-income individuals to afford vehicle financing. This issue is compounded by high default rates, which impact the ability of institutions to offer favorable terms. The risk of loan defaults leads to financial instability for lenders, and these elevated interest rates act as a barrier to entry for many consumers. The ongoing struggle for lenders to balance risk and profitability has been a persistent challenge in expanding the car finance market.

Limited Consumer Credit History:

Another significant barrier to the growth of car finance in Kenya is the limited credit history available for consumers, particularly in rural areas. In many cases, consumers lack sufficient credit history or the necessary documentation to qualify for car loans, which limits their access to financing. Additionally, the absence of comprehensive credit reporting systems in Kenya makes it difficult for lenders to assess the risk of potential borrowers accurately. This lack of credit visibility poses a challenge to financial institutions looking to expand their loan portfolios, further hindering market growth.

Opportunities

Growth of Electric Vehicle Financing:

As the global trend towards sustainable transport continues to gain momentum, there is a significant opportunity for the growth of electric vehicle financing in Kenya. While electric vehicle adoption is still in its early stages, government incentives and global environmental awareness are creating favorable conditions for this shift. Car finance companies can tap into the rising demand for electric vehicles by offering tailored financing solutions. The market potential for electric vehicle financing is considerable, and early movers in this space could capture significant market share as the trend toward clean energy and sustainability gains traction in the country.

Integration of Digital Financing and Dealership Partnerships:

The ongoing shift towards digital finance presents a tremendous opportunity for growth in the Kenyan car finance market. Partnerships between financial institutions and automotive dealerships can result in more streamlined and accessible financing solutions. By integrating loan applications and approvals directly into the purchasing process at dealerships, lenders can offer real-time financing options to consumers, making it easier for customers to secure car loans at the point of sale. This seamless integration could lead to higher loan uptake and faster processing times, benefitting both consumers and financial institutions.

Future Outlook

The future of Kenya’s car finance market appears robust, with substantial growth expected due to continued economic expansion, increasing consumer demand for vehicles, and further advancements in mobile and digital financing solutions. Technological developments in loan application processing and underwriting will help streamline operations, while ongoing regulatory support for car ownership and green vehicles will fuel future growth. The demand for private vehicles will continue to rise, especially among the growing middle class, with both traditional and electric vehicles gaining in popularity. Financial institutions are likely to explore new methods of expanding their loan portfolios to cater to this demand, particularly through digital platforms.

Major Players

- Safaricom

- KCB Group

- Equity Bank

- M-Omnibus

- Family Bank

- Commercial Bank of Africa

- Co-operative Bank of Kenya

- Stanbic Bank Kenya

- Standard Chartered Bank

- NCBA Group

- Absa Bank Kenya

- Fina Bank

- Postbank

- M-Shwari

- Sidian Bank

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive manufacturers and distributors

- Mobile money service providers

- Financial institutions offering loans

- Car dealerships

- Automotive leasing companies

- Insurance companies

Research Methodology

Step 1: Identification of Key Variables

Identify the key variables that influence the Kenya car finance market, such as consumer preferences, financing options, economic growth trends, and government regulations.

Step 2: Market Analysis and Construction

Perform an in-depth analysis of the Kenyan car finance market, focusing on factors such as market drivers, challenges, growth trends, and competitive dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Validate hypotheses with industry experts, financial analysts, and automotive experts to ensure accuracy in the data and insights.

Step 4: Research Synthesis and Final Output

Synthesize the research findings into a comprehensive report, providing actionable insights and market forecasts for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Consumer Demand for Vehicles

Increase in Disposable Income

Government Initiatives to Promote Vehicle Ownership

Growth in Microfinance Institutions

Adoption of Digital Financing Solutions - Market Challenges

High Interest Rates

Limited Access to Credit for Low-Income Individuals

Lack of Awareness of Financing Options

Inadequate Vehicle Financing Infrastructure

Regulatory Challenges in Financial Products - Market Opportunities

Expansion of Financing to the Rural Population

Growth in Electric Vehicle Financing

Integration of Mobile-Based Loan Platforms - Trends

Increase in Mobile and Digital Financing Solutions

Rising Adoption of Green and Sustainable Vehicles

Shift Towards Flexible Financing Options

Government Collaboration with Financial Institutions

Growth in Short-Term Vehicle Rentals - Government Regulations & Defense Policy

Regulation of Loan Interest Rates

Government Incentives for Vehicle Ownership

Regulatory Framework for Electric Vehicle Financing - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Personal Vehicle Financing

Commercial Vehicle Financing

Leasing and Rental Financing

Fleet Financing

Electric Vehicle Financing - By Platform Type (In Value%)

Online Platforms

Bank Financing

Microfinance Institutions

Peer-to-Peer Financing

Mobile Money Financing - By Fitment Type (In Value%)

Direct Financing

Indirect Financing

Lease Financing

Hire Purchase Financing

Consumer Financing - By EndUser Segment (In Value%)

Individual Consumers

Small and Medium Enterprises

Corporates

Government and Public Sector

Non-profit Organizations - By Procurement Channel (In Value%)

Direct Procurement

Third-party Distribution

Bank and Financial Institution Channels

Online Platforms

Retail Dealers - By Material / Technology (in Value%)

Digital Payment Technologies

Mobile Financing Solutions

Vehicle Tracking Technologies

Electronic Loan Platforms

Artificial Intelligence for Loan Assessment

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Interest Rates, Loan Terms, Loan Processing Time, Customer Service, Digital Platform Accessibility, Loan Amount, Repayment Options, Credit Score Flexibility, Loan Approval Rate, Loan Default Rates)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Standard Chartered Bank Kenya

Equity Bank

KCB Bank

M-Pesa

Cooperative Bank of Kenya

NCBA Group

Absa Bank Kenya

Commercial Bank of Africa

DTB Bank

Family Bank

Postbank

Micro Africa

Fina Bank

M-Omnibus

Kenya Vehicle Financing Ltd

- Individual Consumers’ Increasing Demand for Vehicles

- SMEs’ Growing Reliance on Vehicle Financing

- Corporate Fleet Financing Needs

- Government Programs for Public Sector Vehicle Acquisition

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now