Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Kenya cloud infrastructure market operates within a national ICT sector valued at approximately USD ~ billion, with cloud data center, storage, and compute infrastructure forming a rapidly expanding subset supported by enterprise digitalization, telecom virtualization, and public sector platform migration. Investments in carrier-neutral data centers, hyperscale cloud nodes, and enterprise colocation facilities amount to several hundred million USD in infrastructure assets deployed across the country, reflecting strong demand for scalable computing and storage capacity supporting digital services and analytics workloads.

Dominance in the Kenya cloud infrastructure market is concentrated in Nairobi and the Konza technology corridor due to dense fiber backbones, submarine cable connectivity, carrier-neutral data centers, and enterprise headquarters clusters requiring cloud hosting capacity. Nairobi hosts most cloud regions, interconnection hubs, and colocation facilities linked to telecom networks and financial platforms, while Konza Technopolis is designed as a national digital infrastructure zone attracting hyperscale cloud providers, data center operators, and enterprise technology deployments aligned with smart city and innovation initiatives.

Market Segmentation

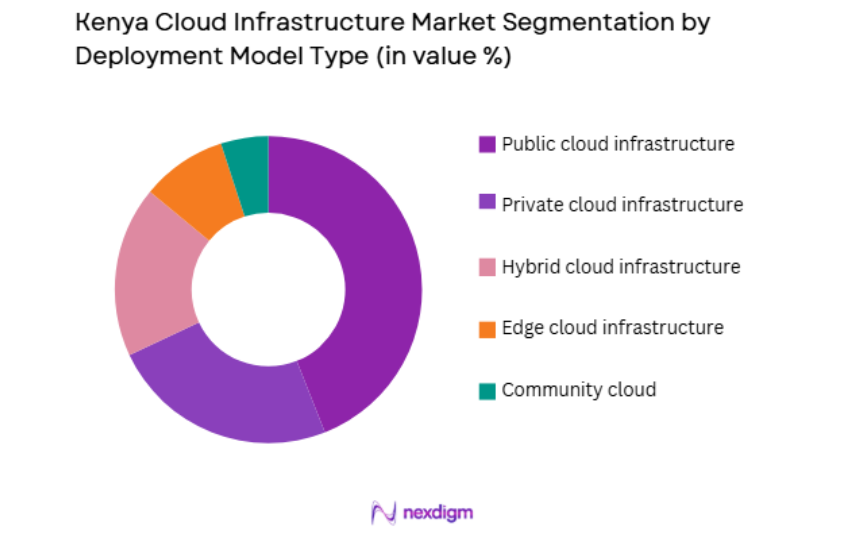

By Deployment Model

Kenya Cloud Infrastructure market is segmented by product type into public cloud infrastructure, private cloud infrastructure, hybrid cloud infrastructure, community cloud, and edge cloud infrastructure. Recently, public cloud infrastructure has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Enterprises and telecom operators increasingly migrate workloads to hyperscale and regional public cloud platforms offering scalable compute, storage, and analytics services hosted in domestic data centers, making public cloud the primary infrastructure consumption model across Kenya’s digital economy.

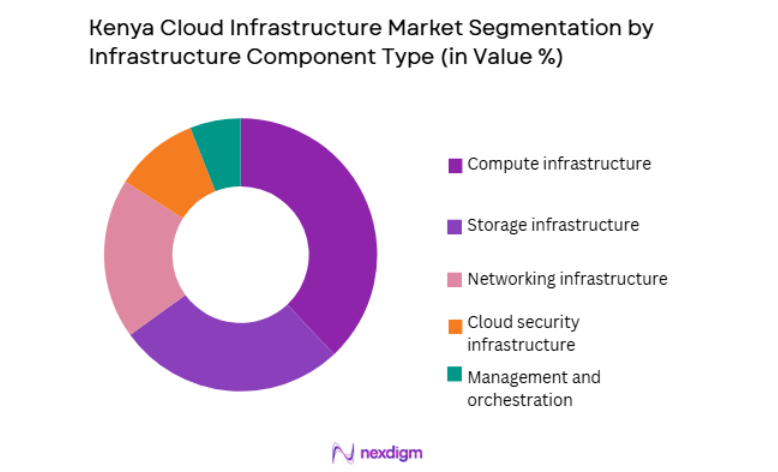

By Infrastructure Component

Kenya Cloud Infrastructure market is segmented by product type into compute infrastructure, storage infrastructure, networking infrastructure, cloud security infrastructure, and management and orchestration platforms. Recently, compute infrastructure has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Cloud adoption in Kenya centers on virtual machines, container platforms, and AI-ready processing capacity hosted in data centers, leading enterprises and providers to prioritize server and processor infrastructure investments over ancillary components such as orchestration or security tools.

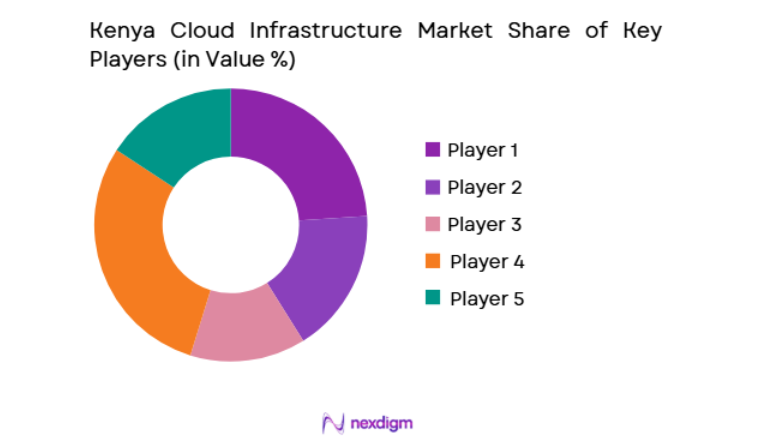

Competitive Landscape

The Kenya cloud infrastructure market is moderately consolidated around global hyperscale cloud providers and regional data center operators collaborating with telecom carriers to deliver compute, storage, and networking capacity to enterprises and public institutions. Market influence is concentrated among providers with regional cloud regions, carrier-neutral facilities, and fiber interconnection assets, while global cloud vendors dominate platform layers and regional infrastructure investment through partnerships with local operators.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Regional Cloud Presence |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | USA | ~ | ~ | ~ | ~ | ~ |

| Oracle Cloud | 2016 | USA | ~ | ~ | ~ | ~ | ~ |

| Africa Data Centres | 2018 | South Africa | ~ | ~ | ~ | ~ | ~ |

Kenya Cloud Infrastructure Market Analysis

Growth Drivers

Expansion of Hyperscale Cloud Regions and Carrier-Neutral Data Center Capacity in East Africa

Kenya’s cloud infrastructure market growth is strongly driven by the establishment of hyperscale cloud regions and carrier-neutral colocation facilities designed to provide scalable compute, storage, and networking capacity to enterprises and digital platforms across East Africa from centralized infrastructure nodes located in Nairobi and emerging technology zones. Global cloud providers and regional data center operators are investing in high-density server halls, fiber interconnection fabrics, and redundant power systems to host public cloud platforms and enterprise workloads domestically, enabling organizations to migrate applications from on-premise environments to scalable cloud infrastructure with improved performance and regulatory compliance. Enterprises across finance, telecommunications, media, logistics, and public administration sectors increasingly adopt cloud computing for digital transformation initiatives including analytics, e-commerce platforms, AI services, and enterprise software deployment, requiring reliable local infrastructure capable of handling latency-sensitive workloads and data sovereignty requirements. Telecom operators integrating virtualization and software-defined networking into core and edge architectures also deploy cloud infrastructure within network data centers, further expanding compute and storage capacity deployment nationwide.

Enterprise Digital Transformation and Adoption of Data-Intensive Applications Across Industries

The accelerating digital transformation of Kenyan enterprises across financial services, telecommunications, retail, logistics, healthcare, and public administration is driving substantial demand for scalable cloud infrastructure capable of supporting data-intensive applications, analytics platforms, and AI-enabled services deployed across digital business operations. Organizations migrating enterprise resource planning systems, customer platforms, analytics tools, and online service architectures to cloud environments require elastic compute and storage capacity to handle fluctuating workloads, increasing reliance on domestic cloud infrastructure hosted in local data centers rather than legacy on-premise hardware. Financial institutions deploy cloud-based transaction processing, fraud detection analytics, and digital banking platforms requiring high-availability infrastructure and secure storage environments, while telecom providers adopt cloud-native network functions and service delivery platforms requiring distributed computing capacity across core and edge facilities.

Market Challenges

High Energy and Infrastructure Costs Affecting Data Center and Cloud Deployment Economics

The Kenya cloud infrastructure market faces significant constraints due to high energy costs, power reliability challenges, and infrastructure expenses associated with constructing and operating large-scale data centers required to host cloud compute and storage platforms, increasing capital and operational expenditure for infrastructure providers and influencing pricing for cloud services. Cloud data centers require continuous high-density power supply, cooling systems, and redundant energy infrastructure to maintain uptime and performance standards, yet electricity costs and grid reliability variability in certain regions increase operational risk and total cost of ownership for providers deploying hyperscale facilities. Backup generation, battery storage, and cooling infrastructure further raise deployment expenses, making infrastructure investment more capital-intensive compared to regions with lower energy costs and established utility reliability. Land acquisition, fiber connectivity build-out, and regulatory compliance requirements add additional costs to data center construction and expansion projects. Smaller cloud providers and local enterprises face barriers in establishing private or regional cloud infrastructure due to these high capital requirements, reinforcing market concentration among large hyperscale and colocation firms.

Cybersecurity, Data Sovereignty, and Skills Gaps in Cloud Infrastructure Management

The expansion of cloud infrastructure in Kenya introduces complex cybersecurity, data governance, and operational management challenges that affect enterprise adoption and infrastructure provider operations, particularly in a regulatory environment emphasizing data protection and digital sovereignty. Cloud environments host sensitive financial, government, and enterprise data requiring advanced security architecture, encryption, and monitoring capabilities, yet organizations often lack specialized expertise in cloud security configuration and compliance management, increasing risk exposure and slowing migration from on-premise systems. Data sovereignty expectations require domestic hosting and strict governance of cross-border data flows, adding compliance complexity for providers operating multi-region infrastructure architectures. Skilled cloud architects, DevOps engineers, and cybersecurity professionals capable of designing and managing large-scale cloud environments remain limited in local labor markets, increasing reliance on external vendors and raising operational costs for enterprises and providers deploying infrastructure. Misconfiguration and operational errors in cloud environments can lead to service disruptions or security vulnerabilities, discouraging risk-averse organizations from full cloud adoption.

Opportunities

Development of Regional Cloud Hubs Serving East African Digital Economies

Kenya’s strategic geographic and connectivity position enables the country to serve as a regional cloud infrastructure hub for East Africa, creating opportunity for deploying hyperscale and colocation facilities capable of delivering compute and storage services to neighboring markets lacking large-scale domestic cloud infrastructure. Nairobi’s submarine cable connectivity, fiber backbones, and carrier-neutral data centers provide the foundation for regional cloud hosting environments serving enterprises and digital platforms across East African economies seeking low-latency access to cloud resources without building local infrastructure in each country. Multinational enterprises operating regional digital services and cross-border e-commerce platforms require centralized cloud hosting nodes within East Africa, driving demand for Kenyan data center expansion. Content delivery networks, streaming platforms, and fintech services targeting regional users benefit from hosting infrastructure within Kenyan cloud facilities to improve performance and reduce latency across borders.

Expansion of Edge and Hybrid Cloud Architectures Supporting Industry and Smart Infrastructure

The evolution of Kenya’s digital economy toward distributed computing models incorporating edge and hybrid cloud architectures creates opportunity for deploying cloud infrastructure beyond centralized data centers into telecom facilities, industrial sites, and smart infrastructure environments requiring localized processing and storage capacity integrated with central cloud platforms. Telecom operators deploying edge computing nodes for low-latency services and network optimization require localized cloud infrastructure integrated with core data centers, expanding infrastructure footprints nationwide. Industrial automation systems, IoT platforms, and smart city applications generate data streams that benefit from hybrid cloud architectures combining local processing with centralized analytics and storage, increasing demand for modular cloud infrastructure deployments across sectors. Enterprises adopting hybrid cloud strategies require infrastructure capable of integrating on-premise systems with public cloud platforms, stimulating deployment of private cloud clusters and edge nodes within enterprise facilities.

Future Outlook

Kenya’s cloud infrastructure market is expected to expand steadily as hyperscale investments, enterprise digitalization, and regional cloud hub positioning increase demand for compute and storage capacity. Edge and hybrid cloud architectures will broaden deployment beyond centralized data centers. Government digitalization and regulatory support for domestic hosting will sustain infrastructure investment.

Major Players

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Oracle Cloud

- Africa Data Centers

- Liquid Intelligent Technologies

- Huawei Cloud

- Equinix

- Cisco Systems

- Dell Technologies

- HPE

- IBM Cloud

- Oracle

- Safaricom

- Rack Centre

Key Target Audience

- Telecom network operators

- Cloud service providers

- Data center operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Financial institutions

- Large enterprises adopting cloud

- Digital platform companies

Research Methodology

Step 1: Identification of Key Variables

Key variables including data center capacity, cloud adoption rates, enterprise digitalization levels, telecom virtualization, and infrastructure investment were identified. These variables determine demand for compute, storage, and networking infrastructure. Deployment intensity across sectors was mapped.

Step 2: Market Analysis and Construction

Market sizing integrated ICT sector value, data center infrastructure assets, and enterprise cloud adoption patterns across industries. Segment shares were derived from infrastructure component spending distribution and deployment models. Geographic clustering informed infrastructure concentration.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on cloud infrastructure demand were validated through provider deployment data, enterprise IT trends, and regional digital economy indicators. Cross-verification ensured consistency with ICT and data center investment levels. Adoption trajectories were assessed.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into segmentation, competitive, and market dynamic frameworks. Infrastructure drivers and constraints were integrated into analysis. Final outputs combined quantitative estimates with structural cloud ecosystem assessment for Kenya.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid digitization of enterprises and public services in Kenya

Expansion of hyperscale and regional cloud availability zones

Growth of data-intensive applications in fintech and media - Market Challenges

Power reliability and energy costs for data center operations

Data sovereignty and compliance complexities

Shortage of advanced cloud engineering skills - Market Opportunities

Localized cloud regions for financial and government workloads

Hybrid cloud adoption across enterprises and telecom

Cloud infrastructure for AI and analytics workloads - Trends

Shift toward hybrid and multi-cloud architectures

Integration of cloud with edge computing infrastructure - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Compute infrastructure

Cloud storage systems

Cloud networking infrastructure

Cloud security infrastructure

Cloud management and orchestration platforms - By Platform Type (In Value%)

Public cloud regions

Private cloud data centers

Hybrid cloud environments

Telecom cloud infrastructure

Edge-integrated cloud platforms - By Fitment Type (In Value%)

Hyperscale data centers

Enterprise on-premise cloud

Colocation cloud deployments

Modular cloud facilities - By End User Segment (In Value%)

Cloud service providers

Telecom operators

Financial services institutions

- Market Share Analysis

- Cross Comparison Parameters (Compute scalability, Storage performance, Network latency, Security and compliance, Deployment flexibility, Data sovereignty controls, Hybrid cloud integration, Service availability SLAs, Automation and orchestration maturity, Total cost of ownership)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services

Microsoft

Google

Oracle

IBM

Huawei Cloud

Alibaba Cloud

Liquid Intelligent Technologies

Safaricom

Africa Data Centres

IXAfrica Data Centre

Teraco Data Environments

Schneider Electric

Vertiv

Cisco Systems

- Cloud providers expanding regional infrastructure presence

- Telecom operators building cloud-native network platforms

- Financial institutions migrating core systems to cloud

- Government agencies adopting sovereign cloud environments

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now