Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Kenya Cold Chain Logistics market is experiencing robust growth, driven by the increasing demand for temperature-sensitive goods across various sectors. Based on a recent historical assessment, the market size for Kenya Cold Chain Logistics is valued at USD ~ billion, with the growth being fueled by rising demand in the food and pharmaceuticals industries. The government’s investment in infrastructure improvements and the expansion of e-commerce also contribute significantly to this development, creating favorable conditions for cold chain logistics. These factors, combined with the growing awareness of food safety and quality standards, position the market for further expansion in the coming years.

The market dominance is concentrated in key urban centers such as Nairobi and Mombasa. These cities hold the logistical advantage due to their strategic positioning as commercial and transportation hubs. Nairobi, being the capital, serves as the main focal point for trade and distribution, while Mombasa’s port plays a crucial role in supporting cold chain logistics. These regions benefit from the government’s infrastructure initiatives and proximity to international trade routes, enabling efficient handling and distribution of perishable goods, particularly in food and pharmaceuticals.

Market Segmentation

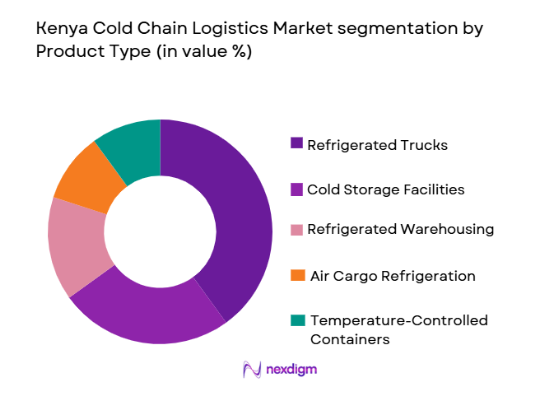

By Product Type

Kenya Cold Chain Logistics market is segmented by product type into refrigerated trucks, cold storage facilities, refrigerated warehousing, air cargo refrigeration, and temperature-controlled containers. Recently, refrigerated trucks have a dominant market share due to factors such as increased demand for fresh food products and pharmaceuticals requiring time-sensitive delivery. The growing demand for refrigerated transport is attributed to its flexibility in reaching rural and remote areas, coupled with rising e-commerce and retail sector activities that require prompt and reliable delivery solutions.

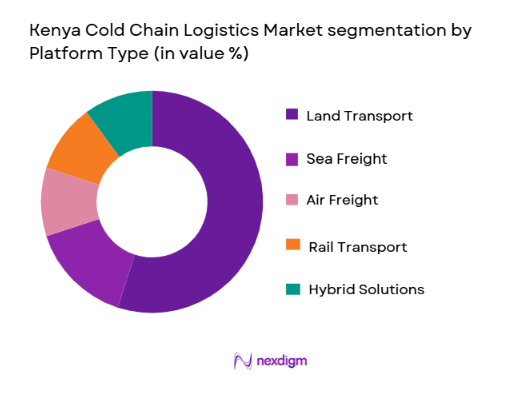

By Platform Type

Kenya Cold Chain Logistics market is segmented by platform type into land transport, sea freight, air freight, rail transport, and hybrid solutions. Recently, land transport has a dominant market share due to its widespread accessibility and cost-effectiveness compared to air and sea freight. The growth of land transport in cold chain logistics is driven by Kenya’s road network improvements and increased demand for efficient delivery systems within the country. The availability of refrigerated trucks and growing consumer demand for perishables further boost land transport’s market presence.

Competitive Landscape

The competitive landscape of the Kenya Cold Chain Logistics market is characterized by both local and international players consolidating their presence to capture the growing demand. Leading players are focusing on expanding their service offerings, including temperature-controlled transport and warehousing solutions, to cater to a broad range of industries. Major logistics companies are also investing in advanced technologies, such as IoT-based tracking systems and automated storage solutions, to enhance efficiency and transparency in cold chain operations.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Temperature-Controlled Logistics |

| Safmarine | 1900 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Mombasa, Kenya | ~ | ~ | ~ | ~ | ~ |

| Maersk Line | 1904 | Mombasa, Kenya | ~ | ~ | ~ | ~ | ~ |

| Jumia | 2012 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| Transworld Group | 1994 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

Kenya Cold Chain Logistics Market Analysis

Growth Drivers

Increased Demand for Perishable Goods:

The demand for perishable goods, especially fresh food, pharmaceuticals, and medical supplies, is a key driver in the Kenya Cold Chain Logistics market. The growing middle-class population in Kenya, along with urbanization, has led to higher consumption of fresh produce, dairy products, and meat. As consumer preferences shift towards higher-quality perishable goods, the need for effective cold chain logistics has increased, facilitating smoother transportation and storage. Moreover, the expanding e-commerce sector, particularly in grocery deliveries, has further intensified the demand for temperature-sensitive logistics solutions. In the pharmaceutical industry, there is also an increasing need for transporting medicines that require precise temperature control to maintain their efficacy. This rise in demand for fresh and temperature-sensitive goods drives the growth of cold chain logistics infrastructure and services, further bolstered by government initiatives and investments in supply chain infrastructure, thus ensuring the smooth flow of goods from farm to table or manufacturer to consumer.

Government Investment in Infrastructure Development:

Government investments in transportation and cold storage infrastructure have significantly boosted the cold chain logistics sector. The Kenyan government has recognized the importance of a robust logistics network to support the growing demand for perishable goods. Investments in road networks, such as the improvement of highways linking rural and urban areas, have facilitated more efficient land transport solutions, allowing refrigerated trucks to deliver goods faster and with reduced risk of spoilage. In addition, the establishment of modern cold storage facilities has further strengthened the supply chain for perishable goods. The development of air cargo refrigeration services at key airports, such as Nairobi’s Jomo Kenyatta International Airport, also supports the logistics of high-value perishables, including pharmaceuticals and food products, ensuring that they reach international markets quickly. With continued government support for infrastructure, the cold chain logistics market is poised for further growth, ensuring a more efficient supply chain for industries relying on perishable goods.

Market Challenges

High Operational Costs:

One of the significant challenges facing the Kenya Cold Chain Logistics market is the high operational costs associated with maintaining temperature-controlled transportation and storage. The initial investment in refrigerated trucks, temperature-controlled warehouses, and specialized equipment is substantial, and this increases the overall cost of logistics services. In addition to capital investment, maintaining these systems involves high operational costs related to energy consumption, particularly for refrigeration units, and labor costs associated with the handling of perishable goods. These factors often lead to increased costs for businesses, which can be passed onto consumers, affecting the overall affordability of cold chain services. Furthermore, many companies struggle to find skilled workers to manage these specialized logistics services, which can further increase operational costs and reduce efficiency. The lack of economies of scale in the cold chain logistics sector in Kenya also exacerbates these issues, making it harder for smaller players to compete with established companies.

Infrastructure Gaps in Rural Areas:

Another key challenge faced by the Kenya Cold Chain Logistics market is the insufficient cold chain infrastructure in rural areas. While urban centers like Nairobi and Mombasa benefit from modern logistics facilities, rural areas often lack the necessary infrastructure to support temperature-controlled transportation and storage. This results in delays and inefficiencies in delivering fresh produce from farms to processing facilities and retail outlets. Many farmers are forced to rely on basic refrigeration methods, which are often inadequate for preserving the quality of perishable goods. Moreover, the absence of adequate cold storage facilities in rural areas leads to significant post-harvest losses, reducing the overall supply of fresh produce available in urban markets. This infrastructure gap poses a challenge to the efficient distribution of perishable goods and limits the potential for growth in the cold chain logistics market.

Opportunities

Expansion in Pharmaceutical Cold Chain Logistics:

The pharmaceutical sector in Kenya presents a significant growth opportunity for cold chain logistics. The increasing demand for vaccines, biologics, and temperature-sensitive medicines creates a need for efficient and reliable cold chain solutions. With the rise in healthcare awareness and the expansion of public and private healthcare facilities, there is a growing demand for cold chain logistics to ensure the safe transportation and storage of pharmaceutical products. Moreover, with the expansion of medical tourism and increased foreign investments in the Kenyan healthcare sector, the demand for temperature-controlled logistics is expected to rise. Cold chain logistics providers who can offer advanced temperature monitoring and tracking solutions are in a strong position to tap into this growing segment. This sector offers substantial potential for businesses looking to diversify and expand their service offerings in Kenya.

Growth of E-Commerce in Grocery Deliveries:

The rise of e-commerce, particularly in grocery deliveries, offers another significant opportunity for the Kenya Cold Chain Logistics market. As more consumers opt for online shopping, particularly in urban areas, the demand for fresh food delivery services has surged. Companies like Jumia and local grocery delivery services are expanding their offerings to include fresh produce, dairy products, and frozen foods, all of which require temperature-controlled logistics. This presents an opportunity for cold chain logistics providers to integrate their services with e-commerce platforms and offer last-mile delivery solutions for perishable goods. By leveraging technology to ensure real-time temperature monitoring and integrating automated cold storage solutions, logistics providers can meet the growing demand for fast, efficient, and safe delivery of temperature-sensitive goods. This trend is expected to continue, especially as internet penetration increases and consumer preferences shift towards online grocery shopping.

Future Outlook

Over the next five years, the Kenya Cold Chain Logistics market is expected to experience steady growth, driven by continued infrastructure development and increasing consumer demand for perishable goods. Technological advancements in refrigerated transport and storage solutions will further enhance market efficiency. Additionally, regulatory support for the food and pharmaceutical industries will provide a conducive environment for market expansion. The growing e-commerce sector will also drive demand for cold chain services, particularly in the grocery delivery space, ensuring that the market remains dynamic and responsive to shifting consumer preferences.

Major Players

- Safmarine

- Kuehne + Nagel

- Maersk Line

- Jumia

- Transworld Group

- DHL

- FedEx

- Panalpina

- DB Schenker

- CEVA Logistics

- Agility Logistics

- Cargill

- Rhenus Logistics

- Bolloré Logistics

- U-Freight

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Food and beverage manufacturers

- Pharmaceutical companies

- E-commerce platforms

- Retail chains

- Cold storage and logistics service providers

- Distribution companies

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the key drivers, challenges, and trends affecting the Kenya Cold Chain Logistics market. We define market boundaries and focus on the core factors influencing the industry.

Step 2: Market Analysis and Construction

This step includes the collection of historical data and market trends to establish a baseline for the current state of the market. The focus is on segmenting the market and identifying its structure.

Step 3: Hypothesis Validation and Expert Consultation

The research methodology is validated by consulting industry experts to refine assumptions and validate the findings, ensuring that the research is grounded in real-world insights.

Step 4: Research Synthesis and Final Output

Finally, the gathered data is synthesized into a coherent report, providing an actionable analysis of the market, its challenges, growth drivers, and future opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in Consumer Demand for Perishable Goods

Government Investments in Infrastructure Development

Expansion of E-commerce and Online Grocery Delivery

Technological Advancements in Cold Chain Logistics

Rising Awareness of Food Safety and Quality Standards - Market Challenges

High Capital Investment and Operating Costs

Lack of Skilled Workforce in Cold Chain Operations

Inefficiency in Rural Cold Chain Infrastructure

Regulatory Barriers and Lack of Standardization

Energy Consumption and Sustainability Issues - Market Opportunities

Expanding the Pharmaceutical Cold Chain Market

Developing Eco-friendly and Sustainable Refrigeration Solutions

Growth of E-commerce and Online Grocery Delivery - Trends

Adoption of IoT and AI for Real-time Monitoring

Growth of Temperature-controlled E-commerce Solutions

Increased Focus on Cold Chain Sustainability

Expansion of Last-Mile Delivery Networks

Use of Blockchain for Supply Chain Transparency - Government Regulations & Defense Policy

Strict Food Safety Regulations

Government Initiatives to Support Cold Chain Infrastructure

Energy Efficiency Standards in Cold Chain Logistics - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Trucks

Cold Storage Facilities

Refrigerated Warehousing

Air Cargo Refrigeration

Temperature-Controlled Containers - By Platform Type (In Value%)

Land Transport

Sea Freight

Air Freight

Rail Transport

Hybrid Solutions - By Fitment Type (In Value%)

Standalone Solutions

Integrated Solutions

Modular Systems

Multi-Temperature Systems

Centralized Solutions - By EndUser Segment (In Value%)

Food & Beverages

Pharmaceuticals

Agriculture

Retail

Healthcare - By Procurement Channel (In Value%)

Direct Procurement

Third-Party Logistics Providers

Online Marketplaces

Government Procurement

Private Sector Procurement - By Material / Technology (in Value%)

Refrigeration Technology

Cold Storage Material

Insulation Material

Energy-efficient Technology

Automation Technology

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Material/Technology, Geographic Reach, Supply Chain Integration, Regulatory Compliance, Sustainability Practices)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Safmarine

Mombasa Container Terminal

Kuehne + Nagel

Maersk Line

Oasis Cold Chain Logistics

Jumia

SPEED Logistics

Transworld Group

DHL Supply Chain

DHL Global Forwarding

Cool Chain Solutions

Schenker Logistics

CMA CGM

TATA Logistics

Gulfstream Cold Storage

- Food & Beverage Industry’s Demand for Efficient Cold Chains

- Pharmaceutical Industry’s Need for Temperature-sensitive Delivery

- Agriculture Sector’s Growing Need for Perishable Goods Transportation

- Retail Sector’s Shift Towards Online Grocery Delivery

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now