Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Kenya Diagnostic Labs Market generated approximately USD ~ million in revenue according to healthcare service expenditure data reported by the Kenya Ministry of Health and global health organizations including the World Health Organization. Market growth is supported by increasing demand for diagnostic testing associated with infectious diseases, chronic disease monitoring, and preventive healthcare screening. Expansion of hospital laboratories, private diagnostic centers, and public health testing facilities continues to drive demand for clinical pathology, molecular diagnostics, and laboratory automation systems.

Nairobi dominates the Kenya Diagnostic Labs Market due to the concentration of tertiary hospitals, national referral laboratories, and advanced diagnostic infrastructure capable of handling high testing volumes. Cities such as Mombasa, Kisumu, and Eldoret also contribute significantly to diagnostic activity because of expanding hospital networks and rising healthcare utilization among urban populations. These healthcare hubs host major diagnostic chains and hospital laboratories that invest in automated analyzers and specialized testing technologies to deliver efficient diagnostic services.

Market Segmentation

By Product Type

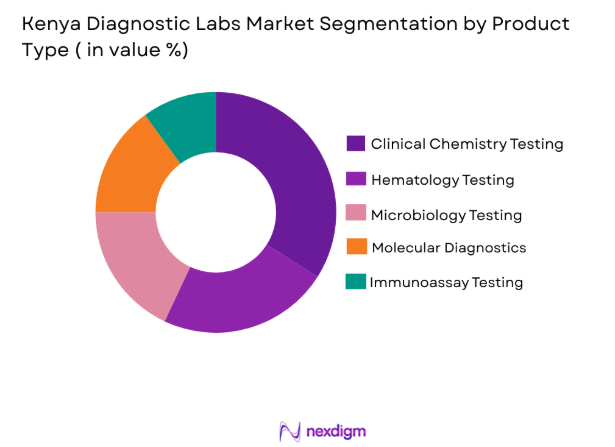

Kenya Diagnostic Labs Market market is segmented by product type into Clinical Chemistry Testing, Hematology Testing, Microbiology Testing, Molecular Diagnostics, and Immunoassay Testing. Recently, Clinical Chemistry Testing has a dominant market share due to factors such as high testing volumes for metabolic disorders, diabetes monitoring, and routine hospital diagnostics. Hospitals and diagnostic centers frequently rely on clinical chemistry analyzers for routine blood testing because these systems provide rapid and cost-efficient diagnostic results. The widespread availability of automated analyzers in hospital laboratories further strengthens adoption, enabling laboratories to process large volumes of patient samples efficiently.

By Platform Type

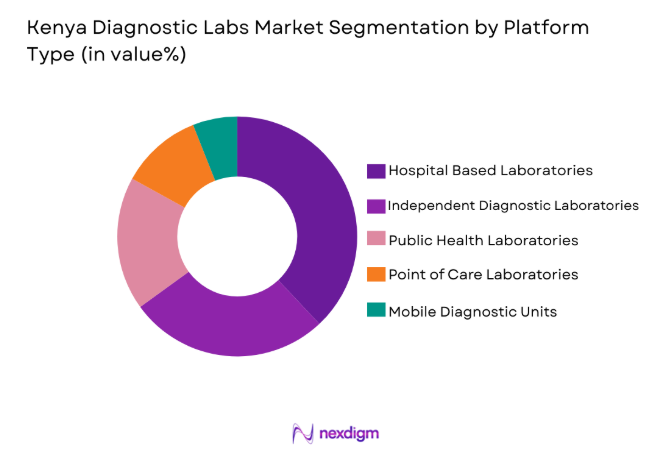

Kenya Diagnostic Labs Market market is segmented by platform type into Hospital-Based Laboratories, Independent Diagnostic Laboratories, Public Health Laboratories, Point-of-Care Laboratories, and Mobile Diagnostic Units. Recently, Hospital-Based Laboratories has a dominant market share due to factors such as patient flow concentration, infrastructure availability, and integrated healthcare service delivery. Major hospitals across Kenya operate advanced laboratory units that handle large diagnostic volumes associated with inpatient treatment, emergency services, and specialized medical procedures. These laboratories benefit from access to clinical specialists, high-capacity automated testing systems, and strong referral networks that drive continuous testing demand.

Competitive Landscape

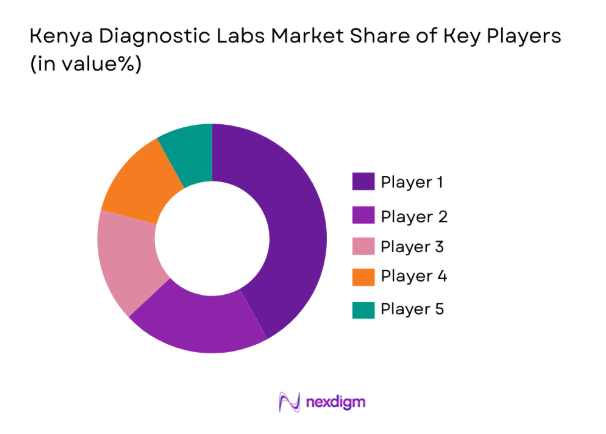

The Kenya Diagnostic Labs Market demonstrates moderate consolidation with several large diagnostic chains and hospital laboratory networks dominating advanced testing services. International diagnostic groups collaborate with domestic healthcare providers to introduce automated testing technologies and molecular diagnostics platforms. Major players compete through test portfolio expansion, laboratory automation, geographic expansion, and partnerships with hospitals and clinics. Large laboratory networks benefit from economies of scale, strong procurement systems, and referral networks that enable high sample processing volumes and improved diagnostic turnaround times.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Diagnostic Network Coverage |

| Lancet Kenya | 2009 | Nairobi | ~ | ~ | ~ | ~ | ~ |

| PathCare Kenya | 2006 | Nairobi | ~ | ~ | ~ | ~ | ~ |

| Aga Khan Hospital Laboratories | 1958 | Nairobi | ~ | ~ | ~ | ~ | ~ |

| Metropolis Healthcare Kenya | 2016 | Nairobi | ~ | ~ | ~ | ~ | ~ |

| Ampath Kenya Laboratories | 2001 | Eldoret | ~ | ~ | ~ | ~ |

Kenya Diagnostic Labs Market Analysis

Growth Drivers

Expansion of National Healthcare Infrastructure and Universal Health Coverage Programs

The Kenya Diagnostic Labs Market is significantly influenced by the continued expansion of healthcare infrastructure supported by national universal health coverage initiatives designed to improve healthcare accessibility across the population. Government programs aimed at strengthening hospital infrastructure have increased investments in diagnostic laboratories within public hospitals and regional healthcare facilities. These investments support the procurement of automated laboratory analyzers, diagnostic reagents, and laboratory information systems. Hospitals and clinics increasingly require diagnostic capabilities to support treatment decisions for infectious diseases, chronic illnesses, and preventive healthcare screening. Public health programs also rely on diagnostic laboratories for disease surveillance, vaccination monitoring, and early outbreak detection. The expansion of county level healthcare facilities has created additional demand for laboratory equipment and trained laboratory personnel. International healthcare organizations collaborate with government agencies to strengthen laboratory capacity through funding, training programs, and technology transfer initiatives. Improved healthcare access and increased patient awareness of disease diagnosis continue to drive higher diagnostic testing volumes nationwide.

Rising Burden of Infectious and Chronic Diseases Driving Diagnostic Demand

The growing burden of infectious diseases and chronic medical conditions across Kenya significantly increases the demand for laboratory diagnostics that support early detection, monitoring, and treatment of diseases. Diagnostic laboratories perform large volumes of tests related to HIV, tuberculosis, malaria, and emerging infectious diseases that require laboratory confirmation for accurate treatment decisions. Chronic diseases such as diabetes, cardiovascular disorders, and kidney disease also require routine laboratory testing to monitor disease progression and treatment effectiveness. Healthcare providers rely heavily on diagnostic laboratory services to guide medical decisions and reduce treatment complications. Increased public health screening programs further expand diagnostic testing volumes across hospitals and community healthcare facilities. Population growth and urbanization contribute to higher healthcare utilization rates, increasing the number of patients requiring laboratory diagnostics. Healthcare awareness campaigns encourage patients to seek early diagnosis for various health conditions. The continued need for accurate laboratory testing across multiple disease categories strengthens the demand for diagnostic laboratories.

Market Challenges

Limited Skilled Laboratory Workforce and Technical Expertise

The Kenya Diagnostic Labs Market faces significant operational challenges due to the limited availability of highly trained laboratory technologists and specialists capable of operating advanced diagnostic equipment and interpreting complex test results. Many healthcare facilities struggle to recruit experienced laboratory professionals, particularly in rural and underserved regions where healthcare infrastructure is less developed. Training programs for laboratory professionals remain limited compared with the rapidly growing demand for diagnostic services across hospitals and clinics. Advanced molecular diagnostic technologies require specialized technical expertise that many laboratories currently lack. Healthcare institutions must invest in training programs and partnerships with international organizations to strengthen laboratory workforce capabilities. Staffing shortages also increase workload pressure on existing laboratory technicians, potentially affecting operational efficiency and diagnostic turnaround times. The lack of specialized training programs in certain diagnostic fields further restricts the adoption of advanced diagnostic platforms. Workforce development remains a critical challenge for sustaining diagnostic laboratory growth.

High Cost of Advanced Diagnostic Equipment and Laboratory Infrastructure

The adoption of advanced diagnostic technologies in Kenya remains constrained by the high cost associated with laboratory equipment procurement, maintenance, and reagent supply chains required for complex diagnostic testing procedures. Modern automated analyzers, molecular diagnostic platforms, and laboratory information systems require significant capital investment that many smaller hospitals and independent laboratories cannot easily afford. Healthcare institutions must also invest in facility upgrades, power supply systems, and quality control mechanisms necessary to maintain laboratory accreditation standards. Imported diagnostic equipment and reagents further increase operational costs due to logistics expenses and currency fluctuations affecting procurement budgets. Smaller diagnostic laboratories often rely on manual testing systems that limit testing capacity and diagnostic accuracy. Financial constraints also restrict the expansion of laboratory networks into rural regions where diagnostic access remains limited. High operational costs therefore remain a barrier to widespread adoption of advanced laboratory technologies across the country.

Opportunities

Expansion of Private Diagnostic Laboratory Chains and Franchise Networks

The Kenya Diagnostic Labs Market presents significant opportunities for private diagnostic laboratory chains to expand their networks through franchise partnerships, regional laboratory hubs, and integrated diagnostic service platforms across major urban and semi urban regions. Private laboratory operators increasingly establish satellite collection centers that connect to centralized laboratories equipped with high capacity automated analyzers. This hub and spoke model enables laboratories to process large testing volumes while maintaining operational efficiency and quality control standards. Expanding private healthcare demand encourages investment in advanced diagnostic technologies including molecular diagnostics, genetic testing, and specialized pathology services. Partnerships with hospitals and clinics allow diagnostic providers to secure steady referral flows for laboratory testing services. International diagnostic companies also explore opportunities to enter the Kenyan market through joint ventures and technology partnerships with local healthcare providers. These expansion strategies enable private laboratory networks to improve geographic coverage and increase diagnostic accessibility.

Growing Adoption of Digital Laboratory Systems and Automation Technologies

The increasing adoption of laboratory automation technologies and digital laboratory information systems creates strong opportunities for improving diagnostic efficiency, accuracy, and sample processing capacity within the Kenya Diagnostic Labs Market. Modern laboratory information management systems allow healthcare providers to digitally manage patient test requests, sample tracking, and diagnostic reporting across multiple healthcare facilities. Automated diagnostic analyzers significantly reduce manual processing errors while enabling laboratories to handle higher testing volumes within shorter timeframes. Integration of digital reporting platforms allows physicians to access laboratory results quickly and securely through hospital information systems. Healthcare organizations increasingly invest in digital infrastructure to streamline laboratory operations and improve patient care coordination. Automation technologies also enable laboratories to perform complex diagnostic testing procedures that require high precision and standardized workflows. The continued digital transformation of healthcare systems therefore provides significant opportunities for diagnostic laboratories to expand their capabilities.

Future Outlook

The Kenya Diagnostic Labs Market is expected to experience steady expansion as healthcare infrastructure development and diagnostic technology adoption continue to accelerate nationwide. Increasing investments in automated laboratory systems, molecular diagnostics, and digital laboratory information platforms will enhance testing capacity and operational efficiency. Government healthcare reforms aimed at expanding universal health coverage are expected to strengthen demand for diagnostic services across hospitals and community healthcare centers. Growing awareness of preventive healthcare and early disease detection will further increase diagnostic testing volumes in the coming years.

Major Players

- Lancet Kenya

- PathCare Kenya

- Aga Khan University Hospital Laboratories

- Metropolis Healthcare Kenya

- Ampath Kenya

- Cerba Lancet Africa

- AAR Healthcare Laboratories

- Nairobqi West Hospital Laboratory

- Mediheal Diagnostic Laboratories

- Mater Hospital Laboratory

- Premier Hospital Diagnostic Laboratory

- Gertrude’s Children’s Hospital Laboratory

- KEMRI Diagnostic Laboratories

- Equity Afia Laboratory Services

- Avenue Healthcare Laboratories

Key Target Audience

- Diagnostic laboratory equipment manufacturers

- Healthcare service providers and hospital groups

- Pharmaceutical and biotechnology companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Medical device distributors

- Healthcare infrastructure investors

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the Kenya Diagnostic Labs Market were identified through healthcare infrastructure data, diagnostic service demand trends, and public health program analysis. Market drivers such as disease prevalence, laboratory capacity, and healthcare spending were examined.

Step 2: Market Analysis and Construction

The market model was constructed by analyzing diagnostic service volumes, laboratory infrastructure distribution, and diagnostic equipment adoption across hospitals and laboratories. Multiple secondary sources were evaluated to establish market size and industry dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions and market estimates were validated through consultations with healthcare professionals, diagnostic equipment suppliers, and laboratory management experts. Expert feedback helped refine market dynamics and confirm demand trends.

Step 4: Research Synthesis and Final Output

All collected insights were synthesized through analytical frameworks to construct the final market outlook. Market segmentation, competitive positioning, and industry dynamics were consolidated into a structured research report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Public Healthcare Infrastructure and National Laboratory Networks

Increasing Demand for Chronic Disease and Infectious Disease Testing

Growing Adoption of Advanced Molecular and Automated Diagnostic Technologies - Market Challenges

Limited Skilled Laboratory Workforce and Technical Expertise

High Cost of Advanced Diagnostic Equipment and Reagents

Uneven Access to Laboratory Infrastructure in Rural Regions - Market Opportunities

Expansion of Private Diagnostic Laboratory Chains in Urban Centers

Rising Investment in Infectious Disease Surveillance and Public Health Testing

Growing Partnerships Between International Diagnostic Firms and Local Healthcare Providers - Trends

Integration of Digital Laboratory Information Management Systems

Increasing Adoption of Point of Care Diagnostic Testing Technologies - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry Testing Systems

Hematology Diagnostic Systems

Microbiology Diagnostic Systems

Molecular Diagnostic Systems

Immunoassay Diagnostic Systems - By Platform Type (In Value%)

Hospital Based Diagnostic Laboratories

Independent Reference Laboratories

Point of Care Testing Laboratories

Mobile Diagnostic Laboratories

Public Health Diagnostic Laboratories - By Fitment Type (In Value%)

Standalone Laboratory Facilities

Hospital Integrated Laboratories

Mobile Diagnostic Units

Clinic Based Laboratory Installations - By End User Segment (In Value%)

Public Hospitals and Government Health Facilities

Private Hospitals and Diagnostic Centers

Research Institutes and Public Health Programs

- Market Share Analysis

- Cross Comparison Parameters (Test Portfolio Breadth, Automation Level, Geographic Presence, Laboratory Accreditation Standards, Technology Integration, Pricing Strategy, Partnership Ecosystem)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Lancet Kenya

PathCare Kenya

Aga Khan University Hospital Laboratory Services

KEMRI Wellcome Trust Diagnostic Laboratories

Metropolis Healthcare Kenya

Cerba Lancet Africa

Equity Afia Medical Centres Laboratory Services

Gertrude’s Children’s Hospital Laboratory

Ampath Kenya Diagnostic Services

Premier Hospital Nyali Diagnostic Laboratory

Mediheal Group of Hospitals Laboratory Services

Platinum Medical Centre Laboratory

Nairobi West Hospital Diagnostic Laboratory

Mater Hospital Diagnostic Laboratory

AAR Healthcare Diagnostic Laboratories

- Public hospitals expanding laboratory capacity to support universal healthcare initiatives

- Private diagnostic centers increasing adoption of automated testing platforms

- Research institutes strengthening infectious disease surveillance and laboratory research

- Public health laboratories supporting nationwide disease monitoring programs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now