Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Kenya edge computing market is anchored within a national ICT economy valued at USD ~ billion, with edge deployments expanding alongside rising data localization and low-latency processing demand across telecom, fintech, and public digital infrastructure. The Kenya edge data center segment alone shows measurable scale, with localized processing infrastructure tied to tens of millions in USD investments, reflecting enterprise and operator adoption of distributed computing architectures for real-time analytics and IoT enablement.

Dominance within the Kenya edge computing market is concentrated in Nairobi and the emerging Konza technology corridor due to dense fiber connectivity, hyperscale data interconnection nodes, financial technology ecosystems, and national digital service platforms. Nairobi hosts most carrier-neutral data centers and telecom switching infrastructure, while Konza Technopolis is structured as a national technology special economic zone designed for cloud and edge workloads, attracting telecom operators, data center providers, and smart-city infrastructure deployments.

Market Segmentation

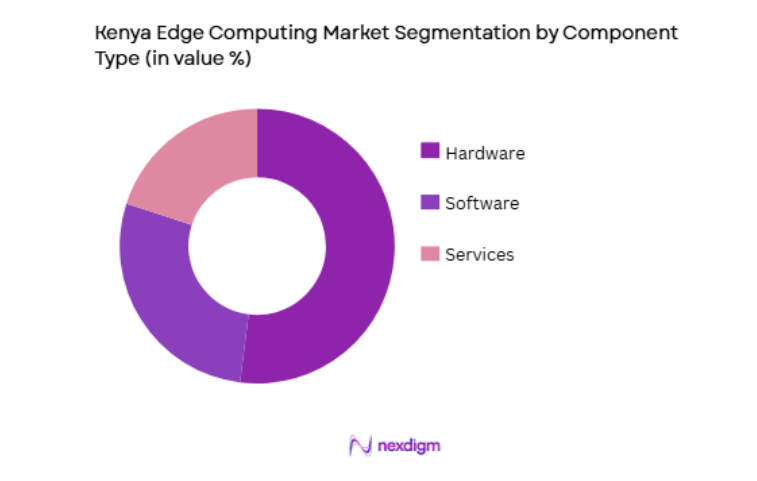

By Component

Kenya Edge Computing market is segmented by product type into hardware, software, and services. Recently, hardware has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Edge deployments in Kenya require localized compute nodes, ruggedized micro-data centers, and telecom-integrated edge servers to support mobile money platforms, video analytics, and network optimization, making hardware procurement the largest expenditure layer.

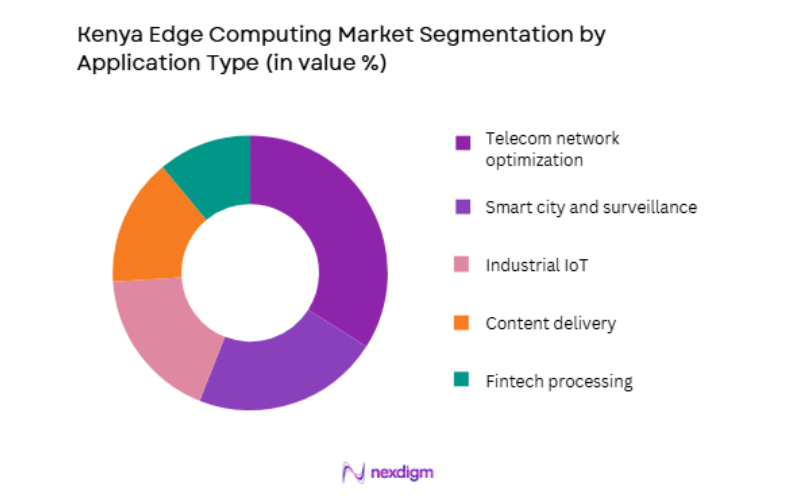

By Application

Kenya Edge Computing market is segmented by product type into telecom network optimization, smart city and surveillance, industrial IoT, content delivery, and fintech processing. Recently, telecom network optimization has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

Competitive Landscape

The Kenya edge computing market exhibits moderate consolidation driven by telecom operators, global cloud providers, and regional data center firms forming infrastructure partnerships. Telecom-cloud alliances shape deployment models, with operators providing network edge locations and global vendors supplying platforms and orchestration layers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Edge Deployment Model |

| Safaricom | 1997 | Kenya | ~ | ~ | ~ | ~ | ~ |

| Liquid Intelligent Technologies | 2004 | UK / Africa | ~ | ~ | ~ | ~ | ~ |

| Huawei Technologies | 1987 | China | ~ | ~ | ~ | ~ | ~ |

| Nokia | 1865 | Finland | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

Kenya Edge Computing Market Analysis

Growth Drivers

5G-Ready Telecom Infrastructure Expansion and Mobile Data Localization Requirements

Kenya’s edge computing market growth is strongly driven by the structural shift of telecom networks toward distributed architectures capable of processing data closer to users and devices, particularly in dense urban clusters where mobile broadband traffic and mobile money transactions create sustained latency-sensitive workloads. Telecom operators are deploying multi-access edge computing nodes within base station aggregation sites and regional switching facilities to support real-time analytics, video compression, and network optimization, enabling faster response times for digital services and reducing backbone congestion across national fiber corridors. This transformation is reinforced by regulatory emphasis on data localization and cybersecurity resilience, encouraging enterprises and financial platforms to host processing workloads within national borders rather than relying solely on distant hyperscale cloud regions, thereby stimulating localized edge infrastructure investment across telecom and financial ecosystems. The widespread adoption of smartphones, mobile payment platforms, and digital public services generates massive transactional data streams that require near-instant processing to maintain user experience quality, fraud detection efficiency, and service continuity, pushing operators and cloud partners to establish distributed compute nodes at the network edge rather than centralized data centers. Enterprise sectors such as banking, logistics, and media are increasingly integrating latency-sensitive analytics and streaming applications into customer-facing platforms, creating additional demand for edge hosting environments that combine telecom connectivity with compute acceleration and local caching capabilities. Government digital transformation programs and smart infrastructure initiatives also require localized data processing for surveillance analytics, traffic systems, and public service delivery, further expanding edge node deployment footprints across urban regions. Partnerships between telecom operators and hyperscale cloud providers are accelerating deployment through shared infrastructure models in which operators supply physical edge locations and connectivity while cloud vendors deliver orchestration software and platform services, lowering entry barriers and scaling adoption.

Rapid Growth of IoT-Enabled Industries and Real-Time Analytics Applications Across Urban and Industrial Sectors

The proliferation of connected devices and sensor-driven systems across Kenya’s industrial, urban, and commercial sectors is generating continuous streams of operational data that require immediate processing near the point of generation, making edge computing essential for efficiency, automation, and predictive analytics use cases. Industrial facilities in manufacturing, energy distribution, and logistics are deploying IoT sensors for equipment monitoring, asset tracking, and environmental control, creating latency-sensitive workloads that benefit from localized compute nodes capable of processing data without dependence on distant cloud infrastructure. Smart city deployments in Nairobi and emerging technology zones incorporate surveillance cameras, traffic sensors, and public safety systems that demand instant video analytics and anomaly detection at edge locations to ensure operational responsiveness and bandwidth efficiency, further reinforcing distributed processing demand. The financial technology sector, which processes high volumes of mobile transactions and digital payments, relies on near-real-time fraud detection and transaction validation systems that operate more effectively when hosted at localized edge environments integrated with telecom networks. Retail and content distribution platforms also require localized caching and analytics to deliver personalized experiences and streaming content with minimal latency to mobile users, expanding edge deployment footprints in commercial districts. As enterprises adopt artificial intelligence and machine learning models for operational optimization, deploying inference engines at edge nodes reduces latency and bandwidth costs compared to centralized cloud processing, accelerating adoption across sectors.

Market Challenges

Limited Distributed Infrastructure Density and Power Reliability Constraints Across Secondary Regions

Kenya’s edge computing expansion faces structural challenges due to uneven infrastructure distribution beyond major urban centers, where fiber connectivity density, reliable power supply, and secure data hosting environments remain less developed, constraining deployment of distributed compute nodes across the national territory. Edge architectures require numerous localized micro-data centers integrated with telecom aggregation points and stable energy systems to maintain continuous low-latency processing, yet secondary cities and rural corridors often experience intermittent power availability and limited carrier-neutral facilities, increasing operational risk and capital costs for infrastructure providers. Telecom operators prioritize metropolitan deployment zones where connectivity demand and revenue potential justify investment, leaving peripheral regions underserved and reducing nationwide edge coverage that would enable industrial and public sector digitalization at scale. The need for redundant power systems, cooling infrastructure, and physical security further increases deployment costs in areas lacking established data center ecosystems, discouraging expansion into lower-density markets despite growing digital service demand. Enterprises operating in agriculture, mining, and logistics sectors across remote regions cannot fully leverage edge computing capabilities due to connectivity gaps and infrastructure limitations, slowing adoption outside urban clusters. Infrastructure financing constraints and long payback periods for distributed facilities also deter private investors from building micro-data centers in smaller markets where utilization rates may initially be low.

Data Security, Sovereignty, and Skills Gaps in Edge Platform Deployment and Management

The implementation of edge computing environments introduces complex cybersecurity, data governance, and operational management requirements that present challenges for enterprises and infrastructure providers in Kenya, particularly in a context of evolving regulatory frameworks and limited specialized workforce capacity. Edge architectures distribute data processing across numerous localized nodes, increasing the attack surface and necessitating advanced security orchestration, encryption, and monitoring capabilities that many organizations lack experience deploying at scale. Compliance with data protection regulations and sovereignty expectations requires careful management of where data is processed and stored, especially for financial, government, and telecommunications workloads, adding complexity to multi-node edge environments compared to centralized cloud models. Organizations adopting edge computing must integrate heterogeneous hardware platforms, orchestration software, and telecom connectivity layers, demanding specialized engineering and cybersecurity expertise that remains scarce in local labor markets, increasing reliance on external vendors and raising operational costs. Skills shortages in edge platform management, AI inference deployment, and distributed network optimization slow enterprise adoption and limit local innovation capacity in developing customized edge applications tailored to Kenyan industry needs. Smaller enterprises face barriers in understanding deployment models and return-on-investment metrics, reducing uptake beyond large telecom and financial institutions.

Opportunities

Expansion of Smart City Infrastructure and National Digital Public Service Platforms Requiring Edge Processing

Kenya’s ongoing urbanization and digital government transformation create substantial opportunity for edge computing deployment across smart city infrastructure, public safety systems, and digital service delivery platforms that require localized processing of sensor and video data for real-time decision-making and citizen service responsiveness. Municipal surveillance networks, intelligent traffic management systems, environmental monitoring sensors, and emergency response platforms generate high-volume data streams that must be processed at edge nodes to minimize latency and reduce bandwidth consumption across national networks, driving demand for distributed compute infrastructure in urban centers. Government digital service platforms delivering identity, health, taxation, and public administration functions increasingly rely on real-time analytics and secure localized data handling, further expanding the need for sovereign edge hosting environments integrated with telecom and government networks. National smart city initiatives and technology zones such as Konza Technopolis are designed around digital infrastructure ecosystems that incorporate edge computing as a foundational layer supporting urban services, innovation hubs, and connected industry clusters. Public-private partnerships between municipalities, telecom operators, and technology vendors provide a pathway for financing and deploying edge infrastructure aligned with urban modernization goals, enabling scalable rollouts of distributed compute nodes across metropolitan regions.

Emergence of Regional Edge Hubs Supporting East African Digital Trade and Cross-Border Data Services

Kenya’s position as a regional technology and connectivity hub in East Africa creates opportunity for the country to host edge computing infrastructure serving neighboring markets, enabling low-latency digital services, content delivery, and enterprise applications across cross-border economic corridors. Nairobi’s concentration of fiber backbones, submarine cable landing stations, and carrier-neutral data centers positions it as a logical regional edge aggregation point capable of serving enterprises and telecom operators across East Africa seeking localized processing without building infrastructure in each country. Regional digital trade, fintech expansion, and cloud adoption among East African enterprises increase demand for distributed computing resources accessible within the region, encouraging global cloud and telecom providers to establish edge nodes in Kenya that deliver services to multiple national markets. Content distribution networks, streaming platforms, and gaming services targeting East African audiences benefit from hosting caches and compute nodes in Kenyan facilities to reduce latency and improve user experience across neighboring countries. Multinational enterprises operating regional logistics, retail, and financial platforms require real-time analytics across cross-border operations, creating demand for edge environments integrated with regional connectivity infrastructure.

Future Outlook

Kenya’s edge computing market is expected to expand steadily as telecom-cloud convergence, 5G deployment, and smart infrastructure programs accelerate distributed computing adoption. Increasing IoT integration across industry and urban systems will deepen demand for localized processing. Government digitalization and regional connectivity projects will support infrastructure investment, while enterprise AI and analytics adoption will expand application diversity.

Major Players

- Safaricom

- Liquid Intelligent Technologies

- Huawei Technologies

- Nokia

- Microsoft Azure

- Amazon Web Services

- Cisco Systems

- Intel Corporation

- Equinix

- Africa Data Centres

- Schneider Electric

- Dell Technologies

- HPE

- Ericsson

- Vertiv

Key Target Audience

- Telecom network operators

- Cloud service providers

- Data center operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Smart city infrastructure developers

- Large enterprises with IoT deployments

- Content delivery and streaming platforms

Research Methodology

Step 1: Identification of Key Variables

Key variables including telecom infrastructure density, data center capacity, IoT device penetration, enterprise digitalization level, and regulatory data localization requirements were identified. These variables define demand for distributed computing and edge deployments. Data points were mapped across telecom, ICT, and digital economy indicators.

Step 2: Market Analysis and Construction

Market sizing combined ICT sector value, edge data infrastructure investment, and telecom-driven distributed computing adoption patterns. Segment shares were constructed using application demand intensity and component expenditure patterns across deployments. Regional infrastructure concentration analysis informed geographic dominance.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on edge deployment drivers, telecom-cloud partnerships, and application demand were validated through technology vendor publications, infrastructure investment trends, and regional digital economy data. Cross-verification ensured consistency with ICT market scale and distributed computing adoption trajectories.

Step 4: Research Synthesis and Final Output

Validated data and qualitative drivers were synthesized into segmentation, competitive, and outlook frameworks. Market dynamics were articulated through infrastructure, regulatory, and application trends shaping adoption. Final outputs integrated quantitative estimates with structural technology ecosystem analysis.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising mobile data traffic and 5G readiness in Kenya

Demand for low-latency services in fintech and media applications

Expansion of smart city and surveillance infrastructure - Market Challenges

Limited local data center power and cooling infrastructure

High capital costs for distributed edge deployments

Skills gaps in edge and AI infrastructure management - Market Opportunities

Edge enablement for mobile money and real-time fintech platforms

Industrial IoT adoption in logistics corridors and ports

Localized content caching for video and gaming growth - Trends

Integration of edge with telecom 5G core networks

Adoption of modular micro data center architectures - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Edge servers

Micro data centers

Edge AI accelerators

Edge gateways

Edge orchestration software - By Platform Type (In Value%)

Telecom network edge

Enterprise on-premise edge

Industrial edge computing

Smart city edge infrastructure

Cloud provider edge zones - By Fitment Type (In Value%)

On-premises deployment

Co-located edge sites

Tower-mounted edge nodes

Modular containerized edge - By End User Segment (In Value%)

Telecom operators

Manufacturing and logistics firms

Government and smart city agencies

- Market Share Analysis

- Cross Comparison Parameters (Latency performance, Deployment model, Power efficiency, Scalability, Connectivity integration, Edge AI capability, Security architecture, Manageability platform, Local support presence, Total cost of ownership)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Safaricom

Liquid Intelligent Technologies

SEACOM

Telkom Kenya

Huawei Technologies

Nokia

Ericsson

IBM

Microsoft

Amazon Web Services

Google

Oracle

Cisco Systems

Schneider Electric

Vertiv

- Telecom operators deploying edge to support 5G and traffic localization

- Manufacturing and logistics adopting edge for automation and tracking

- Public sector using edge for surveillance and smart city services

- Media and CDN providers leveraging edge caching for latency reduction

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now