Download PDF

Download PDF Download PDF

Download PDFMarket Overview

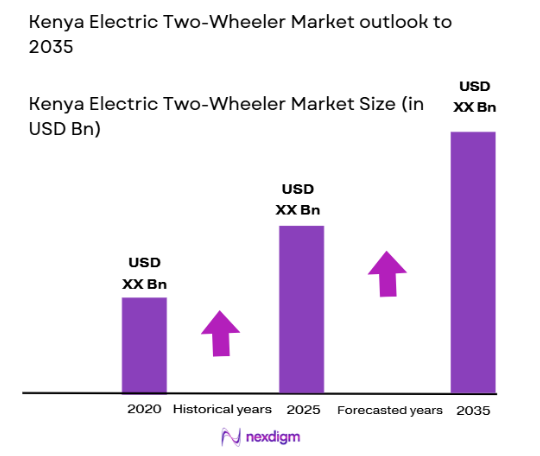

The Kenya Electric Two-Wheeler Market is projected to reach a size of USD ~ billion by the end of a recent historical assessment, driven by the increasing demand for affordable and sustainable urban mobility solutions. Factors such as government initiatives, rising fuel prices, and the adoption of electric vehicle technologies are contributing to this growth. The market is supported by investments in infrastructure development, including charging stations and battery-swapping services. Additionally, improvements in battery technology and affordability of electric two-wheelers are fueling further market expansion.

Kenya’s dominance in the electric two-wheeler market is mainly attributed to the country’s favorable regulatory environment, urbanization, and rapid growth of the middle class. Nairobi, as the largest city, plays a key role in driving the adoption of electric two-wheelers due to traffic congestion, pollution concerns, and the need for affordable commuting. Other cities, such as Mombasa and Kisumu, are also witnessing a rise in demand as the national infrastructure expands. Increased governmental focus on clean energy and electric mobility is further accelerating this trend.

Market Segmentation

By Product Type:

Kenya Electric Two-Wheeler market is segmented by product type into Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Electric Scooters, Electric Motorcycles, and Electric Bicycles. Recently, electric scooters have dominated the market share due to their affordability, compact size, and suitability for urban commuting in traffic-congested cities. These vehicles are increasingly being adopted by both consumers and commercial fleets, with scooters offering the advantage of low maintenance costs and easy maneuverability. The growing demand for affordable last-mile transportation solutions, coupled with supportive government incentives, has helped electric scooters dominate the market in Kenya.

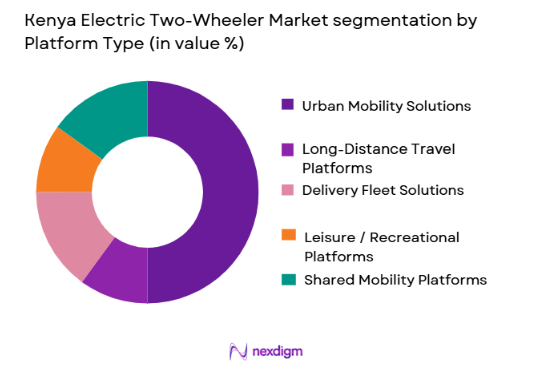

By Platform Type:

Kenya Electric Two-Wheeler market is segmented by platform type into Urban Mobility Solutions, Long-Distance Travel Platforms, Delivery Fleet Solutions, Leisure / Recreational Platforms, and Shared Mobility Platforms. Urban Mobility Solutions have dominated the market due to the increasing preference for eco-friendly transportation modes in urban centers. The high level of traffic congestion, coupled with the affordability and flexibility of electric two-wheelers, makes urban mobility solutions a popular choice among commuters. This demand is further driven by government subsidies for electric vehicle purchases and the growing concern over pollution in cities.

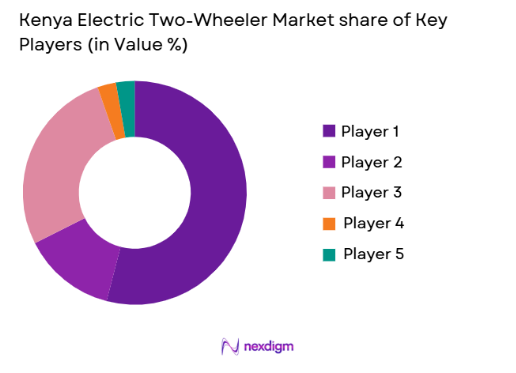

Competitive Landscape

The competitive landscape in Kenya’s electric two-wheeler market is characterized by a mix of local and international players. There is consolidation within the market as major players expand their market reach through partnerships and technology advancements. The market is also seeing an increasing number of startups focused on offering innovative solutions to cater to urban mobility. Established players such as Yamaha, Hero Electric, and Yadea have a significant influence, with a strong presence in both the consumer and commercial segments. The key focus areas for competition include battery technology, pricing strategies, and fleet management solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD billion) | Local Distribution Network |

| Yamaha | 1953 | Japan | ~ | ~ | ~ | ~ | ~ |

| Hero Electric | 1956 | India | ~ | ~ | ~ | ~ | ~ |

| Yadea | 2001 | China | ~ | ~ | ~ | ~ | ~ |

| Ampere Vehicles | 2008 | India | ~ | ~ | ~ | ~ | ~ |

| Okinawa | 2015 | India | ~ | ~ | ~ | ~ | ~ |

Kenya Electric Two-Wheeler Market Analysis

Growth Drivers

Government Incentives for Electric Two-Wheeler Adoption:

Government policies supporting electric vehicle adoption have been a significant driver of the market in Kenya. Financial incentives such as tax exemptions, subsidies, and rebates have reduced the initial cost of electric two-wheelers, making them more accessible to both consumers and businesses. Furthermore, the Kenyan government has prioritized environmental sustainability in its long-term plans, encouraging the adoption of electric vehicles across the country. The introduction of low-emission zones in major cities has also created a favorable environment for the market’s growth. As more consumers seek cost-effective and eco-friendly transportation options, electric two-wheelers are increasingly seen as a practical solution, aided by favorable government policies.

Advancements in Battery Technology:

The continued improvement of battery technology is driving the growth of the electric two-wheeler market. Lithium-ion and other advanced battery technologies are now more affordable, with improved energy efficiency, charging times, and lifespan. This has made electric two-wheelers more competitive in comparison to conventional gasoline-powered vehicles, especially for urban commuting. Battery innovations have also enhanced the range of electric two-wheelers, addressing concerns related to battery depletion and the need for frequent recharging. As battery technology becomes more efficient, electric two-wheelers are expected to offer a more attractive and reliable alternative, boosting consumer confidence in electric vehicles.

Market Challenges

High Initial Cost of Electric Two-Wheelers:

One of the most significant challenges facing the electric two-wheeler market in Kenya is the high initial cost. Despite government incentives, electric two-wheelers remain relatively expensive compared to conventional gasoline-powered models. This cost barrier limits the accessibility of electric two-wheelers, especially in rural areas where purchasing power is lower. Additionally, the relatively high cost of batteries and their replacement costs further deter consumers from adopting electric two-wheelers. While the total cost of ownership may be lower over time due to savings on fuel and maintenance, the upfront expense remains a challenge that limits widespread adoption.

Limited Charging Infrastructure:

Another challenge hindering the growth of the electric two-wheeler market in Kenya is the limited charging infrastructure, particularly in rural and suburban areas. While urban centers like Nairobi have seen significant investments in charging stations, many remote areas still lack the infrastructure needed to support widespread electric vehicle adoption. The absence of a robust network of charging stations makes long-distance travel on electric two-wheelers challenging, and consumers are often hesitant to invest in electric vehicles without the assurance of adequate charging facilities. Expanding the charging infrastructure is crucial for the sustained growth of the electric two-wheeler market in Kenya.

Opportunities

Expansion of Battery Swapping Networks:

The growing demand for electric two-wheelers presents an opportunity for the expansion of battery swapping networks. Battery swapping offers an efficient solution to the issue of charging time, which is a major concern for electric vehicle owners. In regions where charging stations are sparse, battery swapping provides an alternative that enables users to exchange depleted batteries for fully charged ones within minutes. This model has already gained traction in markets like China and is gaining attention in Kenya due to its ability to reduce downtime for users and increase the convenience of owning electric two-wheelers. The establishment of more battery swapping stations in urban and rural areas could help accelerate the adoption of electric two-wheelers across Kenya.

Partnerships with International Manufacturers:

Another key opportunity lies in forming partnerships with international electric vehicle manufacturers to improve market penetration. Collaborations between local distributors and global players can provide the Kenyan market with access to advanced electric vehicle technology, including better battery systems, charging solutions, and vehicle design. These partnerships could also help lower the cost of electric two-wheelers by leveraging economies of scale and facilitating the import of affordable models. Moreover, global players can benefit from entering the emerging African market, where the demand for sustainable transport solutions is on the rise.

Future Outlook

Over the next five years, the Kenya Electric Two-Wheeler Market is expected to experience significant growth. Technological advancements, such as improvements in battery life, efficiency, and charging infrastructure, will further drive adoption. The Kenyan government’s continued focus on sustainable mobility, coupled with supportive policies, will encourage more consumers to shift towards electric vehicles. As more cities invest in clean energy transportation solutions and electric vehicle infrastructure, the demand for electric two-wheelers is projected to expand, with commercial fleets, delivery services, and individual consumers increasingly embracing these eco-friendly alternatives.

Major Players

- Yamaha

- Hero Electric

- Yadea

- Ampere Vehicles

- Okinawa

- NIU Technologies

- Super Soco

- Triumph Motorcycles

- Electric Motion

- Zero Motorcycles

- Evoke Electric Motorcycles

- Vespa

- KTM

- Piaggio

- Honda

Key Target Audience

- Government and regulatory bodies

- Electric vehicle manufacturers

- Urban planners and municipalities

- Commercial fleet operators

- Delivery service providers

- Ride-hailing companies

- Environmental NGOs

- Investors and venture capitalist firms

Research Methodology

Step 1: Identification of Key Variables

Identification of key market drivers, challenges, trends, and relevant sub-segments affecting the electric two-wheeler market in Kenya.

Step 2: Market Analysis and Construction

Data collection through primary and secondary sources, including industry reports, market surveys, and expert consultations, to build the market structure.

Step 3: Hypothesis Validation and Expert Consultation

Consultation with industry experts to validate findings and adjust hypotheses related to growth patterns, technology developments, and competitive factors.

Step 4: Research Synthesis and Final Output

Synthesis of research findings into a comprehensive report, focusing on actionable insights and key strategic recommendations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government incentives for electric vehicle adoption

Improved charging infrastructure

Rising fuel costs driving demand for electric solutions

Urbanization and traffic congestion fostering demand for two-wheelers

Technological advancements in battery efficiency - Market Challenges

High initial cost of electric two-wheelers

Limited charging infrastructure in remote areas

Battery disposal and recycling concerns

Lack of public awareness about electric mobility

Regulatory and policy uncertainties - Market Opportunities

Partnerships with international electric vehicle manufacturers

Expansion of battery swapping networks

Growth in last-mile delivery services - Trends

Increase in adoption of electric two-wheelers in urban centers

Development of integrated transport systems combining electric mobility

Rise in environmentally conscious consumer preferences

Advances in battery technology enhancing vehicle range and efficiency

Government-backed programs for sustainable mobility - Government Regulations & Defense Policy

Subsidies for electric vehicle purchases

Carbon emissions reduction targets

Charging infrastructure development incentives - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Battery Electric Vehicles (BEVs)

Plug-in Hybrid Electric Vehicles (PHEVs)

Electric Scooters

Electric Motorcycles

Electric Bicycles - By Platform Type (In Value%)

Urban Mobility Solutions

Long-Distance Travel Platforms

Delivery Fleet Solutions

Leisure / Recreational Platforms

Shared Mobility Platforms - By Fitment Type (In Value%)

Standalone Electric Two-Wheelers

Integrated Mobility Solutions

Fleet Solutions

Retrofit Solutions

Leasing Solutions - By EndUser Segment (In Value%)

Individual Consumers

Commercial Fleets

Ride-Hailing and Shared Mobility Providers

Delivery Service Providers

Tourism and Leisure Providers - By Procurement Channel (In Value%)

Direct Purchase

Leasing Options

Government and Private Sector Tenders

Online Sales Channels

Dealership Networks - By Material / Technology (in Value%)

Lithium-Ion Battery Technology

Solid-State Batteries

Electric Motors

Charging Infrastructure Technology

Energy Management Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Vehicle Range, Battery Life, Charging Time, Price Point, Customer Service, After-Sales Support, Battery Technology, Charging Infrastructure Availability, Fleet Management Solutions, Sustainability Practices)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Hero Electric

Yadea

Liuji

Ampere Vehicles

Okinawa Autotech

Haojue

NIU Technologies

Super Soco

Triton Electric

Zero Motorcycles

Evoke Electric Motorcycles

Vespa

BMW Motorrad

Honda

KYMCO

- Urban commuters seeking cost-effective mobility solutions

- Commercial fleets transitioning to electric vehicles

- Delivery companies embracing electric two-wheelers for sustainability

- Consumers in rural areas looking for affordable mobility options

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now