Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Kenya Electric Vehicle market has been witnessing a steady growth trend, with the market size reaching an estimated USD ~ billion based on a recent historical assessment. This growth is primarily driven by government incentives, the increasing adoption of electric vehicles in urban areas, and advancements in EV infrastructure. With the government’s focus on environmental sustainability and renewable energy, more consumers and businesses are turning to electric vehicles, encouraged by subsidies, tax exemptions, and a growing network of charging stations. These factors have contributed to the steady rise of electric vehicle adoption across Kenya, fueling the market’s expansion in recent years.

Dominant cities in the Kenya Electric Vehicle market include Nairobi and Mombasa, where EV adoption is most prominent due to better infrastructure and government incentives. Nairobi, as the capital, has seen a rise in both government and private sector investments in electric vehicle infrastructure, including charging stations and vehicle fleets. Mombasa follows as a key location for both public transport and fleet vehicles, leveraging the availability of electric vehicle options. These cities have led the push towards electric mobility, driven by urbanization, rising fuel prices, and the government’s focus on reducing carbon emissions.

Market Segmentation

By Product Type:

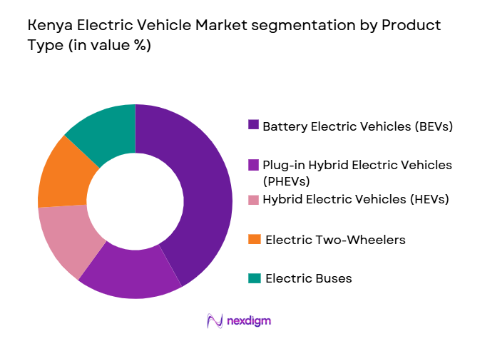

The Kenya Electric Vehicle market is segmented by product type into Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Hybrid Electric Vehicles (HEVs), Electric Two-Wheelers, and Electric Buses. Recently, Battery Electric Vehicles (BEVs) have a dominant market share due to factors such as the increasing demand for fully electric mobility solutions, improved battery technologies, and growing environmental consciousness among consumers. BEVs are favored as they provide a cleaner and more sustainable alternative to conventional vehicles. Furthermore, the expanding availability of charging infrastructure and the government’s strong push for zero-emission transportation have further solidified BEVs as the primary choice for many consumers and businesses.

By Platform Type:

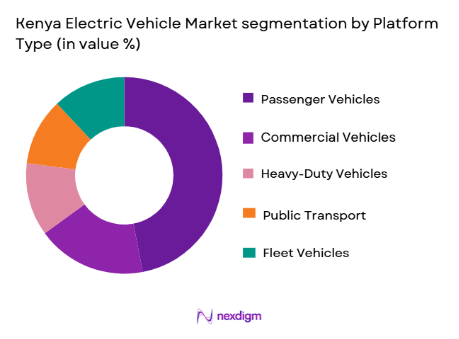

The Kenya Electric Vehicle market is segmented by platform type into Passenger Vehicles, Commercial Vehicles, Heavy-Duty Vehicles, Public Transport, and Fleet Vehicles. Passenger vehicles dominate the market share, driven by the increasing demand for personal electric mobility, supported by consumer incentives and growing awareness of environmental issues. The government’s focus on transitioning private transportation to sustainable modes, alongside advancements in battery technology and charging infrastructure, has further bolstered the rise in electric passenger vehicle adoption. Public transport systems, including electric buses, are also gaining momentum, but passenger vehicles remain the largest contributor to market growth.

Competitive Landscape

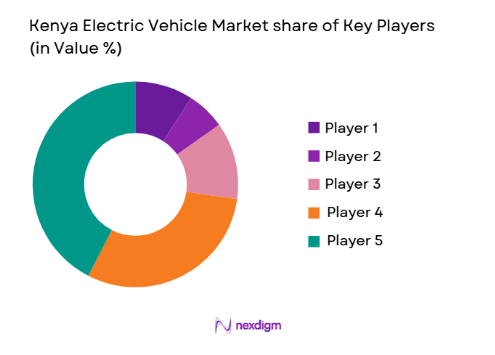

The Kenya Electric Vehicle market is characterized by increasing competition, with both local and international companies entering the market. Key players are focusing on the expansion of electric vehicle infrastructure, strategic partnerships, and technological innovation to meet the rising demand for electric mobility. The market is seeing consolidation as major automotive manufacturers and energy companies collaborate to provide sustainable solutions for electric vehicles. Established companies are strengthening their presence through local production and charging station infrastructure.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue |

| Opibus | 2017 | Nairobi | ~ | ~ | ~ | ~ |

| BasiGo | 2020 | Nairobi | ~ | ~ | ~ | ~ |

| KenGen | 1997 | Nairobi | ~ | ~ | ~ | ~ |

| BYD Auto | 1995 | Shenzhen | ~ | ~ | ~ | ~ |

| Tesla | 2003 | Palo Alto | ~ | ~ | ~ | ~ |

Kenya Electric Vehicle Market Analysis

Growth Drivers

Government Incentives for EV Adoption:

Government policies are a key driver in the adoption of electric vehicles in Kenya. With initiatives such as tax exemptions, subsidies, and financial incentives for both consumers and businesses, the Kenyan government is actively promoting the shift toward electric mobility. These incentives have significantly reduced the financial barriers to EV adoption, making electric vehicles more accessible to a wider segment of the population. Furthermore, the government’s long-term commitment to achieving carbon neutrality by 2030 aligns with the growing demand for clean energy solutions, creating a favorable environment for EV market growth. The establishment of an EV-friendly regulatory framework, coupled with infrastructure investments in charging stations, has reinforced the government’s dedication to sustainable transportation solutions, driving the rapid uptake of electric vehicles.

Technological Advancements in Battery Technology:

Another major growth driver for the Kenya Electric Vehicle market is the continuous advancements in battery technology. With improved energy density, faster charging times, and reduced costs, battery technology has significantly enhanced the performance and affordability of electric vehicles. As battery prices continue to decline, electric vehicles are becoming more competitive with traditional vehicles in terms of initial cost, making them an attractive option for both consumers and businesses. Additionally, innovations such as solid-state batteries, which offer even higher energy density and faster charging, are expected to further revolutionize the electric vehicle market. These advancements in battery technology are directly addressing one of the major challenges faced by the industry – limited driving range – thereby expanding the adoption of electric vehicles across Kenya and beyond.

Market Challenges

High Initial Purchase Cost of Electric Vehicles:

Despite the growing interest in electric vehicles, one of the main challenges faced by consumers is the high initial cost of purchasing an electric vehicle. While the total cost of ownership over the lifetime of an EV is generally lower due to savings on fuel and maintenance, the upfront cost remains a significant barrier, especially for consumers in Kenya, where average income levels are relatively low. While government incentives and subsidies have helped alleviate some of this burden, the initial price remains a hurdle for many consumers, particularly in rural areas. As a result, the adoption of electric vehicles in Kenya remains concentrated in urban centers where the purchasing power is higher, limiting the market’s overall reach.

Limited Charging Infrastructure in Rural Areas:

Another key challenge to the growth of the Kenya Electric Vehicle market is the lack of comprehensive charging infrastructure, particularly in rural areas. While major cities like Nairobi and Mombasa have seen improvements in charging stations, much of the country still lacks the necessary infrastructure to support widespread EV adoption. The absence of reliable and accessible charging stations creates range anxiety among potential electric vehicle owners, making them hesitant to make the switch from conventional vehicles. Additionally, the high costs of establishing charging stations in remote areas pose a significant financial challenge for private companies and the government. Until the infrastructure issue is addressed, the adoption of electric vehicles will remain limited, especially in regions outside the major urban hubs.

Opportunities

Expansion of Electric Vehicle Charging Infrastructure:

One of the key opportunities for growth in the Kenya Electric Vehicle market is the expansion of the electric vehicle charging infrastructure. As the demand for electric vehicles continues to rise, there is a growing need for a robust and widespread network of charging stations. The government, along with private sector investments, can play a pivotal role in developing this infrastructure. By expanding charging stations across the country, including rural areas, Kenya can remove one of the major barriers to EV adoption, ensuring that consumers feel more confident in making the switch to electric mobility. This infrastructure expansion will not only benefit electric vehicle owners but also create new business opportunities for companies involved in the charging station supply chain.

Public Transport Electrification:

Another significant opportunity lies in the electrification of public transport systems, particularly buses and taxis. As urban populations continue to grow, the demand for sustainable public transport solutions is also on the rise. The adoption of electric buses offers a cleaner and more cost-effective alternative to conventional diesel-powered buses, with the potential to significantly reduce urban air pollution and greenhouse gas emissions. In Kenya, where public transportation is widely used, the government has the opportunity to lead the transition to electric public transport, reducing the country’s carbon footprint. This initiative would also help create jobs and stimulate the local economy, making it a valuable opportunity for both the government and the private sector to pursue.

Future Outlook

The Kenya Electric Vehicle market is expected to experience substantial growth in the coming years, driven by continued advancements in technology, increasing government support, and the growing demand for sustainable transportation solutions. As the adoption of electric vehicles becomes more widespread, advancements in battery technology will make electric vehicles more affordable and accessible. With supportive government policies, improved infrastructure, and increasing consumer awareness, the future of the Kenya Electric Vehicle market looks promising. The market is poised to benefit from regulatory incentives, technological breakthroughs, and the global push towards carbon neutrality, positioning Kenya as a key player in the African EV market.

Major Players

- Opibus

- BasiGo

- KenGen

- BYD Auto

- Tesla

- Nissan

- General Motors

- BMW

- Toyota

- Volkswagen

- Mercedes-Benz

- Ford Motor Company

- Audi

- Rivian Automotive

- Hyundai

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Electric vehicle manufacturers

- Charging station infrastructure developers

- Commercial fleet operators

- Automotive component suppliers

- Public transportation agencies

- Environmental organizations

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the most critical factors driving and hindering the electric vehicle market in Kenya. These include government policies, consumer preferences, technological trends, and infrastructure development.

Step 2: Market Analysis and Construction

Data is collected from a range of credible sources, including industry reports, market surveys, and government publications, to construct an accurate market model that includes key trends and insights.

Step 3: Hypothesis Validation and Expert Consultation

In this step, the findings from the market analysis are validated by consulting with industry experts, EV manufacturers, and infrastructure developers to ensure the data is accurate and relevant.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing all gathered data, expert feedback, and market analysis into a comprehensive report, providing actionable insights and forecasts for stakeholders in the Kenya Electric Vehicle market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government incentives for EV adoption

Technological advancements in battery technology

Growing interest in sustainable transport solutions

Expansion of charging infrastructure

Increase in urban mobility needs - Market Challenges

High initial purchase cost of EVs

Limited charging infrastructure in rural areas

Lack of local manufacturing capabilities

Dependence on imported components

Low consumer awareness about EV benefits - Market Opportunities

Government partnerships for infrastructure development

Expansion of public EV charging networks

Increased private sector investment in EV technology - Trends

Shift toward environmentally friendly transportation

Growing adoption of shared mobility solutions

Development of EV-friendly policies and incentives

Focus on energy-efficient transportation solutions

Integration of renewable energy in EV infrastructure - Government Regulations & Defense Policy

EV adoption incentives

Environmental regulations promoting zero-emission vehicles

Import policies on electric vehicle components - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Battery Electric Vehicles (BEVs)

Plug-in Hybrid Electric Vehicles (PHEVs)

Hybrid Electric Vehicles (HEVs)

Electric Two-Wheelers

Electric Buses - By Platform Type (In Value%)

Passenger Vehicles

Commercial Vehicles

Heavy-Duty Vehicles

Public Transport

Fleet Vehicles - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By EndUser Segment (In Value%)

Government Agencies

Private Sector / Technology Firms

Transportation Companies

Fleet Owners

Consumers - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors - By Material / Technology (in Value%)

Lithium-Ion Batteries

Solid-State Batteries

Battery Management Systems

Charging Stations

Electric Drivetrains

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Material / Technology, Geographic Reach, Product Range, Pricing Strategy, Innovation Capabilities)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Kenya Power and Lighting Company

Electric Vehicle Solutions Ltd.

Opibus

BasiGo

Rivian Automotive

Tesla Inc.

BYD Auto

Ford Motor Company

Nissan Motor Corporation

BMW Group

Toyota Motor Corporation

Volkswagen Group

Mercedes-Benz

General Motors

Audi AG

- Government’s role in EV adoption

- Private sector investment in fleet electrification

- Rising demand from transportation companies

- Consumer interest in sustainable mobility options

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now