Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Kenya EV Battery market is valued at approximately USD ~ billion based on a recent historical assessment. The market is primarily driven by factors such as the government’s increasing investment in clean energy, the growing adoption of electric vehicles (EVs), and the expansion of charging infrastructure across major cities. Furthermore, Kenya’s strategic focus on reducing carbon emissions and its favorable policies towards renewable energy sources are anticipated to push the market forward. The demand for EV batteries is expected to grow significantly as the adoption of electric mobility solutions increases, making it a key driver in the market’s expansion.

Kenya’s major cities, including Nairobi, Mombasa, and Kisumu, are playing a crucial role in the growth of the EV battery market due to their higher levels of urbanization and stronger infrastructure development. Nairobi, being the capital, stands as the primary hub for EV adoption, supported by policies such as tax exemptions and incentives on EVs and charging stations. Mombasa, being the main port city, has also witnessed significant interest in electric public transport. The government’s focus on developing sustainable energy solutions, alongside its initiatives to build a robust infrastructure, provides a solid foundation for continued growth in these cities.

Market Segmentation

By Product Type:

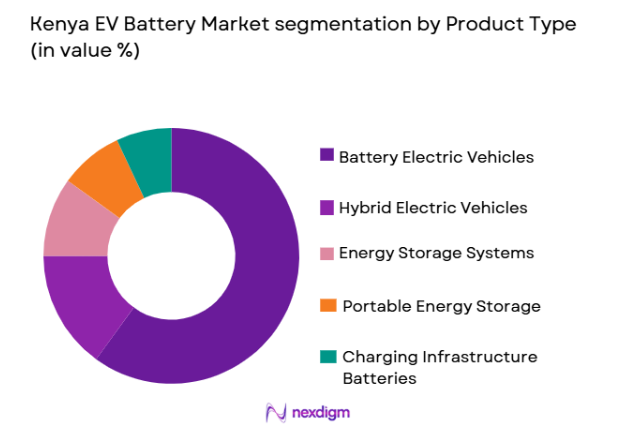

Kenya EV Battery market is segmented by product type into battery electric vehicles (BEVs), hybrid electric vehicles (HEVs), energy storage systems (ESS), portable energy storage, and charging infrastructure batteries. Recently, BEVs have dominated the market due to factors such as a growing shift toward zero-emission vehicles, advancements in battery technology, and government incentives that reduce the initial cost of electric vehicles. The demand for BEVs is further fueled by improvements in charging infrastructure, making them more accessible and practical for consumers.

By Platform Type:

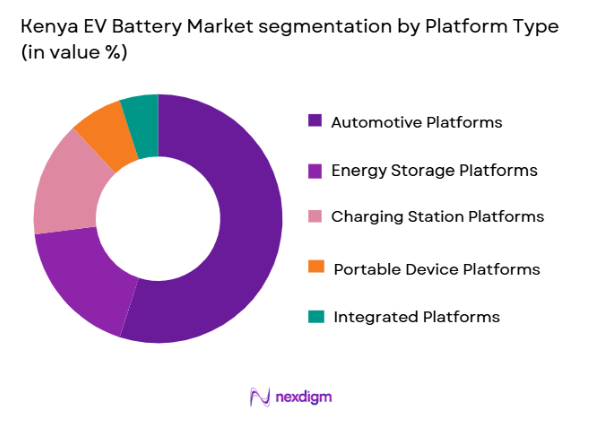

Kenya EV Battery market is segmented by platform type into automotive platforms, energy storage platforms, charging station platforms, portable device platforms, and integrated platforms. Recently, automotive platforms have taken the lead due to the rapid rise in electric vehicle adoption, supported by both consumer demand and the government’s push for sustainable transport. The presence of electric vehicle manufacturers and the growing installation of public charging stations have made automotive platforms the largest segment in the market.

Competitive Landscape

The competitive landscape of the Kenya EV Battery market shows a mixture of global and local players, with major companies influencing both product development and market strategy. These companies are involved in technological innovations, supply chain management, and expanding battery infrastructure. Consolidation in the market is occurring as players invest heavily in the development of battery technology and the establishment of a local manufacturing base. This market is highly competitive, with the top players focusing on efficiency, cost reduction, and sustainability.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD billion) | Battery Efficiency (%) |

| Tesla | 2003 | USA | ~ | ~ | ~ | ~ | ~ |

| BYD | 1995 | China | ~ | ~ | ~ | ~ | ~ |

| Panasonic | 1918 | Japan | ~ | ~ | ~ | ~ | ~ |

| LG Chem | 1947 | South Korea | ~ | ~ | ~ | ~ | ~ |

| CATL | 2011 | China | ~ | ~ | ~ | ~ | ~ |

Kenya EV Battery Market Analysis

Growth Drivers

Government Incentives:

The Kenyan government’s increased focus on promoting electric mobility is one of the key drivers of the EV battery market. Through subsidies, tax exemptions, and other incentives, the government has reduced the financial barrier to EV ownership. These incentives, combined with the national focus on reducing carbon emissions, make electric vehicles a more attractive option for consumers and businesses. As a result, EV adoption is growing rapidly, which in turn is stimulating the demand for EV batteries. These policies have paved the way for the establishment of a supportive ecosystem for EV adoption, which includes investments in charging infrastructure and manufacturing plants for battery components.

Technological Advancements:

Continuous improvements in EV battery technology have led to greater efficiency and lower costs, making electric vehicles more affordable for consumers. Innovations in battery life, energy density, and faster charging capabilities are key factors contributing to the growing demand for electric vehicles in Kenya. With global advancements in solid-state batteries, lithium-ion batteries, and charging infrastructure, Kenyan consumers benefit from improved performance, greater reliability, and better value for money. These technological developments are expected to further boost the adoption of EVs, contributing significantly to the overall growth of the EV battery market in Kenya.

Market Challenges

High Initial Cost:

One of the main challenges facing the Kenya EV battery market is the high upfront cost of electric vehicles, despite government incentives. The price of batteries, especially for electric vehicles, remains relatively high compared to traditional vehicles with internal combustion engines. Although prices have been steadily decreasing, they still constitute a significant portion of the overall vehicle cost. For many consumers in Kenya, especially in lower-income segments, this can be a barrier to entry. As the market matures and more cost-effective solutions are developed, this challenge is expected to ease.

Lack of Infrastructure:

Although Kenya’s government is actively promoting the adoption of electric vehicles, the lack of adequate charging infrastructure remains a significant hurdle. The limited number of charging stations and their distribution across the country poses challenges for potential EV buyers, especially in rural areas. This lack of infrastructure not only reduces the convenience of owning an electric vehicle but also creates uncertainty regarding the feasibility of long-distance travel. Therefore, further investment in charging infrastructure is crucial to accelerating the adoption of EVs and supporting the growth of the EV battery market.

Opportunities

Expansion of Charging Infrastructure:

The growth of EV infrastructure, particularly the installation of charging stations, presents a major opportunity for the Kenyan EV battery market. By improving the availability and accessibility of charging stations across urban and rural areas, Kenya can stimulate more widespread EV adoption. With better infrastructure, consumers will be more likely to consider electric vehicles, knowing they can charge their vehicles conveniently. Public and private sector collaboration in setting up these stations could also lead to lower operating costs and reduced barriers to EV ownership, which would ultimately boost the market for EV batteries.

Local Manufacturing of EV Batteries:

Another promising opportunity lies in the establishment of local manufacturing plants for electric vehicle batteries. Currently, a significant portion of Kenya’s battery supply is imported, which increases costs and creates dependency on foreign suppliers. However, by investing in domestic battery production, Kenya can reduce costs, create jobs, and improve its competitive advantage in the electric vehicle market. Local manufacturing of batteries would not only benefit EV manufacturers but also encourage the establishment of a local supply chain for components, further driving market growth.

Future Outlook

The future outlook for the Kenya EV battery market is positive, with a significant increase in demand expected over the next five years. Driven by advancements in technology, government policies promoting clean energy, and an increase in EV adoption, the market is poised for substantial growth. The expanding charging infrastructure and the move towards local manufacturing are expected to create a sustainable environment for the EV battery market, ensuring long-term success and profitability for both local and international players.

Major Players

- Tesla

- BYD

- Panasonic

- LG Chem

- CATL

- Samsung SDI

- Siemens

- Schneider Electric

- ABB

- Mitsubishi Electric

- ChargePoint

- Bosch

- Eaton

- General Electric

- Saft

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Electric vehicle manufacturers

- Energy storage companies

- Public and private transport operators

- Charging infrastructure developers

- Local battery manufacturers

- Clean energy and sustainability firms

Research Methodology

Step 1: Identification of Key Variables

In this step, the key variables affecting the market are identified and defined to focus the research efforts.

Step 2: Market Analysis and Construction

Data is collected and analyzed to construct an accurate market model that reflects current trends and market conditions.

Step 3: Hypothesis Validation and Expert Consultation

The initial market model is validated through discussions with industry experts, ensuring the assumptions are correct and feasible.

Step 4: Research Synthesis and Final Output

Final findings are synthesized into a comprehensive report that presents a clear view of the market, including trends, growth drivers, and challenges.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government subsidies for electric vehicle adoption

Technological advancements in battery efficiency

Increased urbanization and infrastructure development

International investment in renewable energy

Growing environmental awareness among consumers - Market Challenges

High initial cost of EV batteries

Lack of widespread charging infrastructure

Dependence on foreign imports for battery components

Limited local manufacturing capacity

Regulatory and compliance hurdles in the battery sector - Market Opportunities

Expansion of charging infrastructure networks

Integration of renewable energy with storage solutions

Local manufacturing of EV battery components - Trends

Rising demand for energy storage solutions

Technological innovation in battery recycling

Increased adoption of fast-charging technologies

Integration of AI and IoT in battery management systems

Government-backed sustainability initiatives - Government Regulations & Defense Policy

Battery disposal and recycling regulations

Government incentives for clean energy initiatives

Standards for electric vehicle emissions and safety - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Battery Electric Vehicles (BEVs)

Energy Storage Systems (ESS)

Portable Energy Storage

Charging Infrastructure Batteries

Hybrid Electric Vehicles (HEVs) - By Platform Type (In Value%)

Automotive Platforms

Energy Storage Platforms

Charging Station Platforms

Portable Device Platforms

Integrated Platforms - By Fitment Type (In Value%)

OEM Batteries

Aftermarket Batteries

Modular Batteries

Integrated Battery Systems

Refurbished Batteries - By EndUser Segment (In Value%)

Electric Vehicle Manufacturers

Energy Storage Providers

Commercial Fleets

Private EV Owners

Charging Infrastructure Developers - By Procurement Channel (In Value%)

Direct Sales

Government Tenders

Distribution Networks

Online Bidding Platforms

Third-Party Distributors - By Material / Technology (In Value%)

Lithium-ion Batteries

Nickel-Metal Hydride Batteries

Solid-State Batteries

Lead-Acid Batteries

Graphene-Based Batteries

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Material / Technology, Government Regulations, Charging Infrastructure, Battery Recycling, Cost Efficiency)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Tesla

BYD

Panasonic

LG Chem

CATL

Samsung SDI

SK Innovation

ABB

Schneider Electric

Siemens

Bosch

Eaton

Toshiba

Murata Manufacturing

ChargePoint

- Electric vehicle manufacturers seeking affordable, long-lasting batteries

- Energy storage providers investing in grid balancing technologies

- Commercial fleets transitioning to electric solutions

- Charging infrastructure developers expanding battery supply chains

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now