Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Kenya home finance market has reached approximately USD ~ billion in outstanding mortgage balances, as reported by the Central Bank of Kenya and the Kenya National Bureau of Statistics, expressed in USD equivalent terms. The market is primarily driven by urban housing demand, government housing programs, growing middle-income households, and digital payment integration for mortgage servicing. Commercial banks, savings and credit cooperatives (SACCOs), and non-bank financial institutions contribute significantly to the market’s expansion.

Nairobi remains the primary hub for home finance activity, driven by rapid urbanization, high population growth, and increased property transactions. Mombasa and Kisumu follow as secondary cities with significant demand for housing finance due to their economic activities, infrastructural growth, and regional connectivity. Kenya benefits from an expanding middle class, rising disposable incomes, and a growing demand for affordable housing across urban and peri-urban areas. The government’s initiatives, such as affordable housing programs, further stimulate lending activity.

Market Segmentation

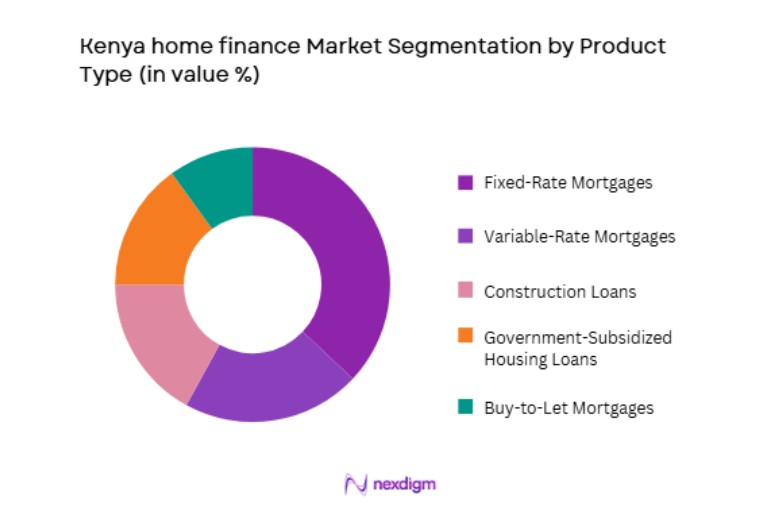

By Product Type

Kenya home finance market is segmented by product type into Fixed-Rate Mortgages, Variable-Rate Mortgages, Construction Loans, Government-Subsidized Housing Loans, and Buy-to-Let Mortgages. Recently, Fixed-Rate Mortgages has a dominant market share due to the increasing preference for repayment stability among borrowers in the face of inflation and rising interest rates. Lenders, particularly commercial banks, offer competitive fixed-rate products to attract long-term borrowers. Government-backed housing schemes also incentivize fixed-rate mortgage offerings, making them an attractive option for low- and middle-income buyers. The predictability of fixed repayments, alongside the rising cost of living, has encouraged a shift towards long-term, predictable borrowing solutions, which has reinforced fixed-rate mortgages as the leading product in the market.

By Lender Type

Kenya home finance market is segmented by lender type into Commercial Banks, SACCOs (Savings and Credit Cooperative Organizations), Microfinance Banks, Non-Bank Financial Institutions, and Insurance Companies. Recently, Commercial Banks has a dominant market share due to their strong capital base, wide-reaching branch networks, and access to liquidity from deposits and institutional funding. These banks offer a variety of mortgage products and have the capacity to serve both high-net-worth individuals and middle-income homebuyers. SACCOs also hold a significant share, especially for providing affordable housing finance solutions to their members. The competitive advantage of SACCOs lies in their local community focus and favorable loan terms. However, commercial banks remain the primary players due to their ability to offer comprehensive mortgage solutions and larger loan sizes.

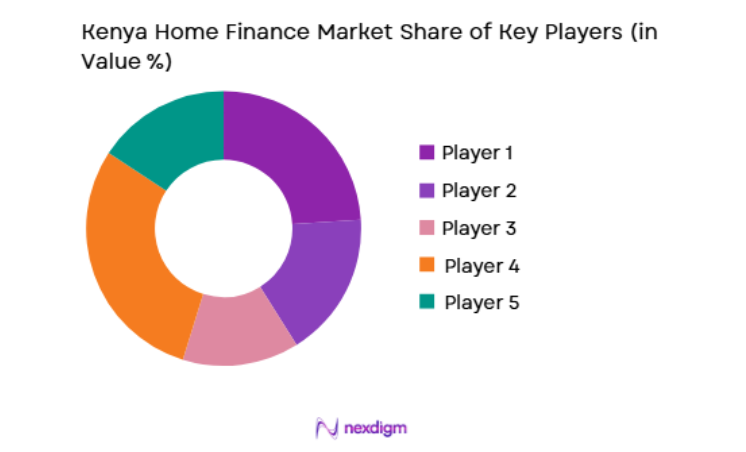

Competitive Landscape

The Kenya home finance market is moderately competitive, with a mix of established commercial banks, SACCOs, and emerging microfinance institutions competing for market share. Banks dominate the market with their broad product offerings and extensive distribution networks, while SACCOs continue to provide affordable solutions, particularly for low-income buyers. Non-bank financial institutions are gradually increasing their influence by offering more flexible and innovative products. The market sees consolidation through partnerships between banks and insurance companies, and the growing use of digital platforms is pushing both traditional and new players to innovate.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Loan Book (USD) |

| Housing Finance Company Kenya | 1965 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| Kenya Commercial Bank | 1896 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| Cooperative Bank of Kenya | 1965 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| NIC Bank | 1959 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| SACCOs Kenya | 1980 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

Kenya Home Finance Market Analysis

Growth Drivers

Urbanization and Growing Middle-Class Housing Demand

One of the primary growth drivers in the Kenya home finance market is the rapid urbanization and expanding middle class, which has led to an increased demand for housing. Nairobi, Mombasa, and Kisumu have seen significant growth in the demand for residential housing, driven by an increase in disposable income and a shift toward homeownership as a wealth-building tool. This urbanization trend is further supported by government initiatives, such as affordable housing projects, which have created opportunities for financial institutions to expand their mortgage portfolios. As more individuals transition from renting to owning property, commercial banks, SACCOs, and other lenders have experienced heightened demand for long-term financing options. This has fueled the growth of both affordable and high-end housing markets, strengthening the home finance sector across the country.

Government Housing Initiatives and Public-Private Partnerships

Government initiatives such as the Affordable Housing Programme are a significant driver of the home finance market in Kenya. These initiatives are designed to provide low-cost housing solutions to the growing middle class, supported by public-private partnerships that aim to reduce the cost of homeownership. The government’s subsidy programs, which offer affordable mortgage rates and favorable terms, have created a supportive environment for homebuyers. These efforts are also creating a more favorable market for lenders by ensuring a larger pool of potential homebuyers with the ability to make payments. Additionally, the government’s efforts to encourage private sector participation through land development incentives have driven increased construction activity, further boosting demand for home loans.

Market Challenges

High-Interest Rates and Affordability Constraints

One of the major challenges facing the Kenya home finance market is the high-interest rates that lenders impose on home loans. Despite a growing demand for mortgages, many potential buyers are unable to afford the high monthly repayments associated with these loans. As a result, banks and financial institutions must balance profitability with the need to offer competitive, affordable loan terms. Although interest rates have fluctuated in response to changing economic conditions, they remain relatively high compared to other markets, which creates barriers for many prospective homebuyers, especially those in the low-income and informal sectors.

Limited Access to Affordable Housing and Land Constraints

Another significant challenge is the limited availability of affordable housing in urban areas, especially for the low- to middle-income population. Rising construction costs, coupled with land scarcity, have made it difficult for developers to provide affordable housing options. Additionally, land ownership issues and the complexity of land titling have created legal barriers for developers and financial institutions looking to expand housing supply. These challenges make it difficult to meet the housing needs of a rapidly urbanizing population, which further exacerbates the affordability constraints for prospective homeowners.

Opportunities

Expansion of Digital Mortgage Platforms and Mobile Loan Applications

One of the key opportunities for growth in the Kenya home finance market lies in the expansion of digital mortgage platforms and mobile loan applications. With the high penetration of mobile phones and mobile money services in Kenya, digital platforms offer a convenient, accessible, and efficient way to access mortgage products. Financial institutions are increasingly offering loan applications and approvals through mobile apps, enabling a larger number of consumers to access financing for homeownership. This shift to digital platforms is expected to continue driving market growth, as it allows lenders to expand their customer base, particularly in underserved areas. Additionally, mobile loan servicing and payments will enhance the overall customer experience, making it easier for homeowners to manage their mortgages.

Opportunities in Affordable Housing Development and Public-Private Partnerships

There is significant potential for growth in the affordable housing segment through public-private partnerships. The government’s initiatives, such as the Affordable Housing Programme, aim to provide millions of Kenyans with access to low-cost homes. Developers and financial institutions can capitalize on these efforts by offering tailored financing solutions for these projects. By collaborating with the government, financial institutions can help ensure the successful implementation of affordable housing initiatives while also expanding their mortgage portfolios. Furthermore, the government’s commitment to reducing construction costs and simplifying land acquisition processes presents a lucrative opportunity for developers to build affordable homes.

Future Outlook

The Kenya home finance market is expected to experience moderate growth over the next five years, driven by increased demand for homeownership and ongoing government support for affordable housing. Digital transformation within the banking sector will continue to play a pivotal role in expanding access to home loans, especially through mobile banking and digital platforms. While challenges such as high-interest rates and land constraints persist, strategic partnerships and innovative lending products will provide new growth opportunities for the market.

Major Players

- Housing Finance Company Kenya

- Kenya Commercial Bank

- Cooperative Bank of Kenya

- NIC Bank

- Commercial Bank of Africa

- Standard Chartered Bank Kenya

- Barclays Kenya

- Family Bank

- Standard Bank Kenya

- ABC Bank

- Diamond Trust Bank

- Bank of Africa Kenya

- Equity Bank

- CFC Stanbic Bank

- National Bank of Kenya

Key Target Audience

- Commercial banks

- Savings and Credit Cooperative Organizations

- Microfinance banks

- Real estate developers

- Government agencies

- Property investors

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables such as mortgage loan volumes, interest rates, government housing initiatives, and real estate development trends were identified using data from official financial institutions and regulatory bodies.

Step 2: Market Analysis and Construction

A top-down approach was used to estimate the total market size by aggregating data from commercial banks, SACCOs, and microfinance institutions regarding home loans and mortgages.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through interviews with mortgage brokers, developers, and financial advisors to ensure alignment with current market trends and projections.

Step 4: Research Synthesis and Final Output

Quantitative data was integrated with qualitative insights to create a comprehensive report, addressing key drivers, challenges, and opportunities within the Kenya home finance market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Urbanization and Housing Demand Expansion

Government Affordable Housing Initiatives

Growth in Mortgage Penetration and Financial Inclusion - Market Challenges

High Interest Rate Environment

Limited Long-Term Funding Sources

Stringent Credit Assessment Norms - Market Opportunities

Expansion of Sharia-Compliant Home Finance

Digital Mortgage Processing Platforms

Public-Private Partnerships in Housing Development - Trends

Rising Adoption of Green Building Financing

Integration of Digital Credit Scoring Models - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Mortgage Loans

Home Construction Loans

Home Improvement Loans

Islamic Home Finance

Refinancing Solutions - By Platform Type (In Value%)

Commercial Banks

Mortgage Finance Companies

SACCOs

Digital Lending Platforms

Microfinance Institutions - By Fitment Type (In Value%)

New Property Financing

Resale Property Financing

Off-Plan Property Financing

Self-Construction Financing - By End User Segment (In Value%)

Salaried Individuals

Self-Employed Professionals

Diaspora Investors

- Market Share Analysis

- Cross Comparison Parameters (Interest Rate Structure, Loan Tenure, Loan-to-Value Ratio, Processing Time, Digital Application Capability, Prepayment Options, Collateral Requirements, Eligibility Criteria, Customer Support, Repayment Flexibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Kenya Mortgage Refinance Company

HF Group

KCB Bank Kenya

Equity Bank Kenya

Co-operative Bank of Kenya

NCBA Bank Kenya

Stanbic Bank Kenya

Absa Bank Kenya

I&M Bank Kenya

Family Bank Kenya

Housing Finance Company of Kenya

Gulf African Bank

First Community Bank Kenya

Standard Chartered Bank Kenya

DTB Bank Kenya

- Increasing Demand from First-Time Homebuyers

- Growing Diaspora Participation in Property Investment

- Rising Preference for Structured Mortgage Products

- Shift Toward Digitally Enabled Loan Processing

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now