Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Kenya online insurance market generated approximately USD ~ million in gross written premiums through digital and mobile channels, according to data from the Insurance Regulatory Authority of Kenya and the Central Bank of Kenya, expressed in USD equivalent terms. The market is driven by widespread mobile money penetration, digital payment infrastructure, increasing smartphone adoption, and insurer partnerships with telecom operators offering microinsurance and health coverage products through online platforms.

Nairobi dominates online insurance activity due to its concentration of insurers, fintech firms, and telecommunications infrastructure, supported by high digital literacy and urban income levels. Mombasa and Kisumu follow as regional commercial hubs with expanding mobile banking adoption. Kenya benefits from a robust mobile money ecosystem led by telecom operators, enabling seamless premium payments and policy issuance through digital applications and USSD-based insurance platforms across urban and peri-urban populations.

Market Segmentation

By Product Type

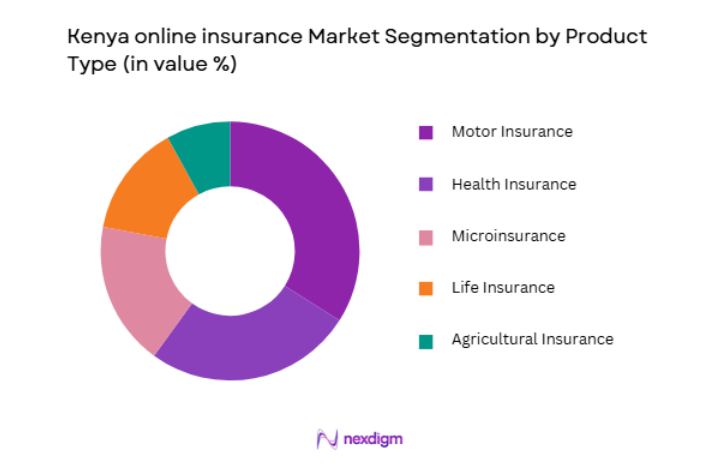

Kenya Online Insurance market is segmented by product type into Motor Insurance, Health Insurance, Microinsurance, Life Insurance, and Agricultural Insurance. Recently, Motor Insurance has a dominant market share due to mandatory third-party coverage requirements and growing digital policy issuance through insurer portals and mobile applications. Regulatory enforcement encourages compliance, leading to significant online purchase volumes. Insurers collaborate with digital marketplaces and vehicle registration systems to streamline policy verification and renewals. Mobile money payment integration simplifies premium collection for motor coverage. High vehicle ownership in urban centers reinforces recurring demand for motor insurance renewals via digital channels, consolidating its leadership within the Kenya Online Insurance market.

By Distribution Channel

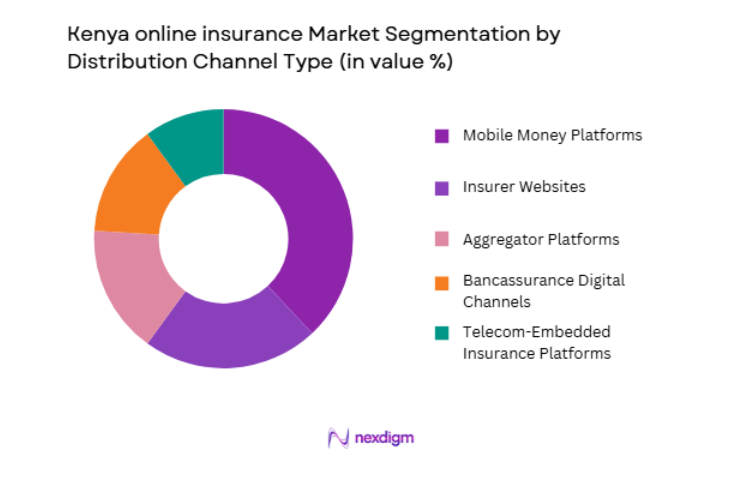

Kenya Online Insurance market is segmented by distribution channel into Insurer Websites, Mobile Money Platforms, Aggregator Platforms, Bancassurance Digital Channels, and Telecom-Embedded Insurance Platforms. Recently, Mobile Money Platforms has a dominant market share due to high penetration of mobile wallets and seamless micro-premium payments across diverse income groups. Insurers leverage telecom partnerships to distribute affordable health and microinsurance policies via USSD codes and smartphone applications. Instant payment confirmation and policy issuance enhance customer convenience. The accessibility of mobile wallets in rural and urban areas strengthens inclusivity. Recurring premium collection through automated deductions further reinforces mobile money’s leadership in the Kenya Online Insurance ecosystem.

Competitive Landscape

The Kenya online insurance market is moderately competitive, with established insurers integrating digital platforms alongside emerging insurtech firms. Major players leverage telecom partnerships and bancassurance networks to expand online reach. Consolidation is influenced by regulatory compliance costs and technology investments. Insurers increasingly invest in mobile applications, data analytics, and digital underwriting systems to enhance operational efficiency and customer acquisition across Kenya’s expanding digital financial ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Digital Premium Share (USD) |

| Jubilee Insurance | 1937 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| Britam Holdings | 1965 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| CIC Insurance Group | 1968 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| APA Insurance | 2003 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

| Old Mutual Kenya | 1845 | Nairobi, Kenya | ~ | ~ | ~ | ~ | ~ |

Kenya Online Insurance Market Analysis

Growth Drivers

Mobile Money Penetration and Digital Payment Infrastructure Expansion

The extensive penetration of mobile money services across Kenya serves as a fundamental growth driver for the Kenya Online Insurance market by enabling seamless premium collection and policy management. Integration between insurers and telecom operators facilitates micro-premium payments accessible to low-income and rural populations. Mobile wallet interoperability allows recurring premium deductions and instant policy activation. Digital payment convenience reduces administrative overhead for insurers and increases affordability for customers. The widespread availability of USSD-based insurance enrollment broadens reach beyond smartphone users. Financial inclusion initiatives encourage adoption of microinsurance products linked to mobile platforms. Automated claims notifications and digital documentation enhance operational efficiency. Strong consumer trust in mobile money systems strengthens transaction reliability. These interconnected digital finance capabilities collectively accelerate expansion of online insurance distribution across Kenya.

Regulatory Support and Financial Inclusion Initiatives

Regulatory backing from the Insurance Regulatory Authority promotes digital innovation and microinsurance development within the Kenya Online Insurance market. Structured guidelines for electronic policy issuance and digital signatures enhance compliance clarity. Government-driven financial inclusion strategies encourage insurers to design affordable, technology-enabled coverage solutions. Partnerships between insurers and development agencies expand agricultural and health microinsurance schemes. Consumer education campaigns raise awareness of online insurance benefits. Regulatory sandboxes allow insurtech experimentation within controlled frameworks. Public support for universal health initiatives strengthens demand for digital health coverage. Simplified licensing requirements for digital intermediaries encourage market entry. These supportive policy measures create a conducive environment for sustained online insurance growth.

Market Challenges

Low Insurance Penetration and Consumer Awareness Constraints

Despite digital advancements, the Kenya Online Insurance market faces structural challenges arising from relatively low insurance penetration across the broader population. Limited awareness of policy benefits reduces voluntary uptake outside mandatory segments such as motor insurance. Informal employment patterns constrain long-term premium commitments. Cultural perceptions regarding insurance claims reliability may affect trust. Digital literacy gaps in rural regions limit online adoption. Premium affordability concerns influence product design complexity. Insurers must invest in targeted education campaigns to expand understanding. Weak historical claims experiences may discourage renewals. These constraints moderate the pace of expansion in voluntary online insurance segments.

Cybersecurity Risks and Digital Fraud Exposure

The Kenya Online Insurance market increasingly faces cybersecurity threats associated with digital payment systems and online data processing. Unauthorized access to customer information can undermine consumer confidence. Fraudulent claims submitted through digital platforms require robust verification mechanisms. Insurers must invest in encryption and multi-factor authentication systems. Collaboration with telecom operators necessitates secure data-sharing protocols. Rapid technological innovation may outpace regulatory adaptation. System outages or transaction failures could disrupt premium collection. Data privacy compliance requirements add operational complexity. These digital risk exposures require continuous technological upgrades and risk mitigation strategies to sustain trust in online insurance platforms.

Opportunities

Expansion of Microinsurance and Usage-Based Insurance Products

Growing demand for affordable and flexible insurance coverage presents substantial opportunities within the Kenya Online Insurance market. Usage-based motor insurance leveraging telematics can align premiums with driving behavior. Agricultural microinsurance linked to weather index data supports rural resilience. Health microinsurance delivered via mobile platforms expands access to primary healthcare coverage. Data analytics enable tailored pricing for low-income households. Partnerships with mobile network operators expand distribution reach. Instant claims settlement via mobile wallets enhances customer experience. Subscription-based coverage models attract younger demographics. These innovations support inclusive growth across underserved segments of the insurance market.

Integration of Insurtech and Artificial Intelligence-Based Underwriting

Technological advancements create significant opportunities to enhance efficiency within the Kenya Online Insurance market. Artificial intelligence-driven underwriting models improve risk assessment accuracy. Automated chatbots provide real-time customer service and claims assistance. Predictive analytics detect fraudulent patterns and optimize pricing structures. Cloud-based platforms reduce infrastructure costs for insurers. API integration enables collaboration between insurers, banks, and fintech companies. Real-time policy customization enhances consumer engagement. Digital dashboards provide transparent policy tracking. These insurtech-driven capabilities position Kenya’s online insurance providers to scale operations and strengthen profitability while improving service delivery.

Future Outlook

The Kenya online insurance market is expected to expand steadily over the next five years, supported by mobile money innovation and increasing smartphone penetration. Regulatory encouragement for digital microinsurance will enhance product diversity. Technological upgrades in underwriting and claims automation are likely to improve efficiency. Growing financial inclusion and expanding digital ecosystems will continue driving online policy adoption across urban and rural populations.

Major Players

- Jubilee Insurance

- Britam Holdings

- CIC Insurance Group

- APA Insurance

- Old Mutual Kenya

- Sanlam Kenya

- Madison Insurance

- ICEA Lion Group

- GA Insurance

- Directline Assurance

- Heritage Insurance

- Resolution Insurance

- Invesco Assurance

- Monarch Insurance

- AAR Insurance Kenya

Key Target Audience

- Insurance companies

- Telecom operators

- Digital payment platforms

- Bancassurance divisions

- Healthcare provider networks

- Agricultural cooperatives

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key indicators including digital premium volumes, product segmentation, mobile payment integration, and regulatory frameworks were identified through official insurance authority publications and financial disclosures.

Step 2: Market Analysis and Construction

A bottom-up aggregation of digital premium data across insurers and distribution platforms was conducted to structure the overall Kenya Online Insurance market framework.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with insurance executives, fintech specialists, and regulatory professionals to ensure alignment with prevailing digital insurance practices.

Step 4: Research Synthesis and Final Output

Quantitative metrics and qualitative insights were consolidated into a structured analytical report integrating segmentation, competitive positioning, and forward-looking evaluation.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

High Mobile Money Penetration and Digital Payment Adoption

Government Push for Financial Inclusion and Insurance Penetration

Growth of Insurtech Innovation and Mobile Based Distribution - Market Challenges

Low Insurance Awareness and Trust Deficit

Regulatory Compliance and Licensing Requirements

Cybersecurity and Data Privacy Risks - Market Opportunities

Expansion of Microinsurance and Pay As You Go Models

Integration with Mobile Network Operators and Fintech Platforms

AI Driven Claims Processing and Fraud Detection - Trends

Increasing Adoption of Mobile First Insurance Solutions

Growth of Index Based and Parametric Insurance Products - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Online Motor Insurance

Online Health Insurance

Online Life Insurance

Microinsurance Products

Agricultural and Index Based Insurance - By Platform Type (In Value%)

Insurer Direct Websites

Mobile Insurance Applications

USSD Based Insurance Platforms

Aggregator and Comparison Portals

Embedded Insurance via Mobile Money Platforms - By Fitment Type (In Value%)

Direct to Consumer Online Policies

Agent Assisted Digital Sales

API Integrated Insurance Distribution

White Label Digital Insurance Solutions - By End User Segment (In Value%)

Individual Policyholders

Small and Medium Enterprises

Agricultural Cooperatives

- Market Share Analysis

- Cross Comparison Parameters (Premium Pricing Model, Mobile Integration Capability, Claims Settlement Time, Coverage Customization Options, Regulatory Compliance Standards)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Britam Holdings

Jubilee Insurance

APA Insurance

CIC Insurance Group

Old Mutual Kenya

Sanlam Kenya

UAP Old Mutual

Madison Insurance

ICEA Lion Group

Heritage Insurance

GA Insurance

Directline Assurance

Kenya Orient Insurance

AAR Insurance Kenya

MUA Kenya

- Rising Demand for Affordable and Flexible Premium Structures

- Preference for Mobile Based Policy Purchase and Renewal

- SME Uptake of Digital Commercial Insurance Solutions

- Growing Interest in Agricultural Risk Coverage

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now