Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Kenya semiconductor infrastructure market forms part of the national electronics, ICT hardware, and data center equipment ecosystem valued above USD ~ million in annual technology hardware expenditure, with semiconductor-related infrastructure such as chip-enabled servers, networking silicon systems, and embedded electronics platforms accounting for a measurable subset of capital deployment across telecom, cloud, industrial, and consumer electronics value chains. Demand is driven by telecom network upgrades, data center expansion, device assembly, and electronics manufacturing activities requiring semiconductor-dependent infrastructure procurement.

Dominance in the Kenya semiconductor infrastructure market is concentrated in Nairobi and emerging technology corridors such as Konza due to proximity to electronics distribution networks, telecom core infrastructure, data centers, and assembly facilities. Nairobi hosts the majority of ICT hardware distributors, telecom switching facilities, and electronics integration firms dependent on semiconductor supply chains, while Konza Technopolis is structured as a national electronics and technology manufacturing zone attracting device assembly, embedded systems development, and digital infrastructure projects linked to semiconductor-enabled platforms.

Market Segmentation

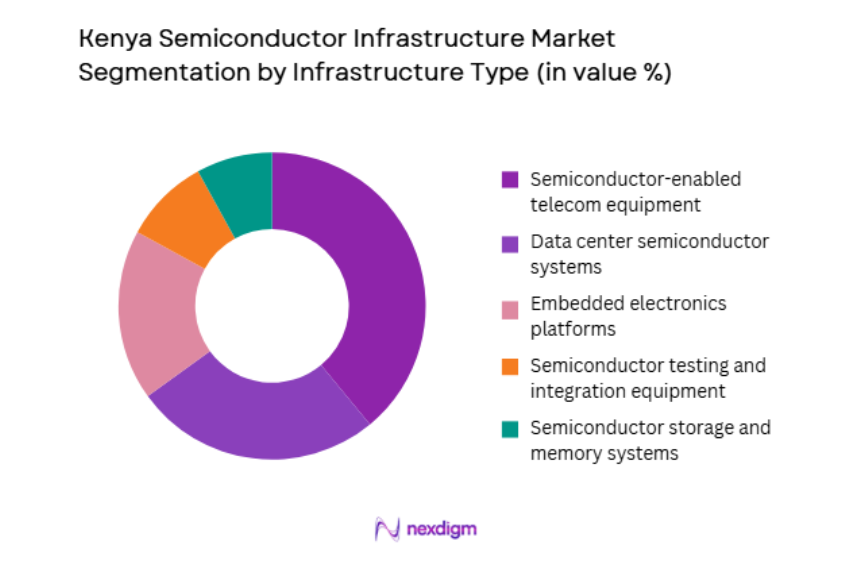

By Infrastructure Type

Kenya Semiconductor Infrastructure market is segmented by product type into semiconductor-enabled telecom equipment, data center semiconductor systems, embedded electronics platforms, semiconductor testing and integration equipment, and semiconductor storage and memory systems. Recently, semiconductor-enabled telecom equipment has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Kenya’s telecom-centric digital economy requires routers, base stations, optical transmission systems, and switching hardware dependent on advanced semiconductor chipsets, leading telecom infrastructure upgrades and 5G-ready deployments to drive the largest semiconductor-related hardware procurement volumes across national ICT infrastructure investment programs.

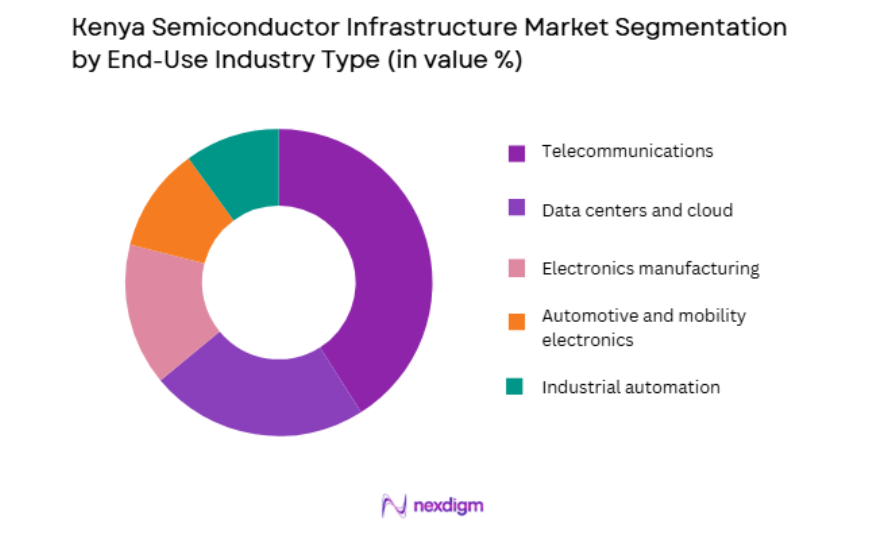

By End-Use Industry

Kenya Semiconductor Infrastructure market is segmented by product type into telecommunications, data centers and cloud, electronics manufacturing, automotive and mobility electronics, and industrial automation. Recently, telecommunications has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Telecom operators and network vendors deploy semiconductor-intensive switching, transmission, and radio systems across nationwide connectivity infrastructure, making telecommunications the largest consumer of semiconductor-dependent infrastructure hardware compared to emerging electronics manufacturing or industrial automation segments.

Competitive Landscape

The Kenya semiconductor infrastructure market is shaped by global semiconductor manufacturers, telecom equipment vendors, and electronics hardware suppliers providing chip-enabled infrastructure to telecom operators, data centers, and industrial sectors, resulting in a supply-driven competitive structure dominated by international firms with established semiconductor design and manufacturing capabilities. Local market activity is concentrated in distribution, integration, and deployment partnerships, while global vendors control core semiconductor technologies embedded in telecom, computing, and electronics systems deployed across Kenya.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Semiconductor Domain |

| Intel | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| Qualcomm | 1985 | USA | ~ | ~ | ~ | ~ | ~ |

| Broadcom | 1961 | USA | ~ | ~ | ~ | ~ | ~ |

| Texas Instruments | 1930 | USA | ~ | ~ | ~ | ~ | ~ |

| Samsung Electronics | 1969 | South Korea | ~ | ~ | ~ | ~ | ~ |

Kenya Semiconductor Infrastructure Market Analysis

Growth Drivers

Expansion of Telecom and Digital Connectivity Infrastructure Requiring Semiconductor-Intensive Network Hardware

Kenya’s semiconductor infrastructure market is fundamentally driven by sustained investment in nationwide telecom connectivity systems including mobile broadband networks, fiber transmission infrastructure, switching platforms, and data routing systems that depend heavily on advanced semiconductor chipsets for processing, signal transmission, and network control functions across digital communication ecosystems. Telecom operators expanding 4G capacity, preparing for 5G deployment, and upgrading optical backbones require semiconductor-enabled baseband processors, radio frequency chips, network processors, and switching ASICs embedded within telecom equipment procured from global vendors, making network infrastructure modernization the largest semiconductor hardware demand driver in the country. Rising mobile data consumption, smartphone penetration, and digital service usage across Kenya necessitate continuous upgrades to network capacity and efficiency, leading operators to deploy higher-performance semiconductor-based routers, optical transport systems, and radio units capable of handling increased traffic loads and latency requirements.

Growth of Data Centers, Cloud Computing, and Enterprise Digitalization Requiring High-Performance Semiconductor Systems

Kenya’s accelerating adoption of cloud computing, enterprise digital platforms, and data center infrastructure is driving substantial demand for semiconductor-based computing systems including processors, memory, networking chips, and storage controllers embedded in servers, storage arrays, and networking equipment deployed across carrier-neutral and enterprise data centers nationwide. The expansion of cloud regions and colocation facilities in Nairobi and technology zones requires large-scale procurement of semiconductor-dependent server and networking hardware to support enterprise workloads, analytics platforms, and digital services hosted within domestic data infrastructure rather than external locations. Enterprises migrating applications to cloud environments and adopting digital transformation strategies deploy semiconductor-intensive computing infrastructure including CPUs, GPUs, network interface chips, and memory modules integrated within server platforms, increasing domestic semiconductor hardware demand. Telecommunications operators integrating edge computing and cloud services into network architecture also deploy semiconductor-based compute and switching systems within core and edge data centers, further expanding infrastructure procurement volumes. Growth in digital commerce, fintech, and online service platforms generates continuous computing workloads requiring high-performance semiconductor processors and memory systems for transaction processing and analytics, reinforcing demand for advanced data center hardware.

Market Challenges

Absence of Domestic Semiconductor Manufacturing and Dependence on Imported Chip Supply Chains

Kenya’s semiconductor infrastructure market faces structural constraints due to the complete absence of domestic semiconductor fabrication, assembly, or advanced packaging capabilities, resulting in total dependence on imported chips and semiconductor-enabled hardware systems sourced from global manufacturers, which exposes the market to supply chain disruptions, pricing volatility, and geopolitical trade dynamics affecting semiconductor availability. Telecom equipment, computing hardware, embedded electronics, and industrial systems deployed in Kenya rely on semiconductor components produced in international fabrication facilities, making infrastructure deployment timelines and costs sensitive to global semiconductor shortages or logistics bottlenecks that delay equipment delivery. Import dependence also increases capital costs due to currency fluctuations, import duties, and transportation expenses associated with semiconductor-embedded hardware procurement, raising total infrastructure investment requirements for telecom operators, data center providers, and enterprises. The absence of local semiconductor assembly or integration industries prevents cost optimization through domestic value addition or customization of chip-based systems tailored to Kenyan deployment conditions. Limited domestic technical expertise in semiconductor design, fabrication, and advanced electronics engineering further constrains development of local supply chains or innovation ecosystems capable of producing or adapting semiconductor technologies.

Limited Electronics Manufacturing Ecosystem and Testing Infrastructure for Semiconductor-Based Systems

The development of semiconductor infrastructure deployment and maintenance capabilities in Kenya is constrained by the relatively small scale of domestic electronics manufacturing, testing, and system integration ecosystems, which remain concentrated in assembly and distribution rather than advanced semiconductor-based hardware design or validation, limiting local capacity to support large-scale semiconductor infrastructure deployment. Telecom and computing equipment installed in Kenya is typically imported as finished systems rather than locally assembled from semiconductor components, reducing opportunities for domestic integration expertise and value chain participation in semiconductor-based infrastructure development. The absence of advanced electronics testing laboratories, semiconductor validation facilities, and component reliability engineering capabilities restricts local ability to certify, customize, or optimize semiconductor-enabled hardware for environmental and operational conditions specific to Kenyan deployments. Industrial sectors adopting automation or embedded electronics solutions depend on imported equipment and external technical support due to limited domestic engineering ecosystems, slowing diffusion of semiconductor-dependent technologies across manufacturing and industrial sectors.

Opportunities

Development of Electronics Manufacturing Clusters and Assembly Ecosystems Supporting Semiconductor-Based Infrastructure

Kenya’s strategic efforts to establish electronics manufacturing zones and technology parks create opportunity for developing localized assembly, integration, and value-addition capabilities for semiconductor-enabled infrastructure systems such as telecom equipment, computing hardware, and embedded electronics platforms, reducing dependence on fully imported hardware and expanding domestic participation in semiconductor value chains. Industrial zones and innovation corridors such as Konza Technopolis provide infrastructure, policy incentives, and logistics connectivity suitable for electronics assembly operations that integrate imported semiconductor components into finished infrastructure products deployed domestically and regionally. Local assembly of telecom network equipment, servers, and embedded systems can reduce import costs, shorten deployment timelines, and support customization for regional environmental conditions, increasing adoption of semiconductor-dependent infrastructure across industries. Collaboration between global semiconductor vendors and local electronics manufacturers can enable technology transfer, workforce training, and gradual development of integration capabilities within Kenya’s industrial ecosystem. Expanding electronics assembly clusters also supports maintenance and lifecycle management services for semiconductor-based infrastructure deployed nationwide, improving reliability and reducing operational costs. Regional demand from East African markets creates export potential for locally assembled semiconductor-enabled infrastructure equipment, strengthening economic viability of manufacturing clusters.

Adoption of Semiconductor-Driven Automation, IoT, and Smart Infrastructure Across Industrial and Urban Systems

The increasing deployment of automation, Internet of Things platforms, and smart infrastructure systems across Kenya’s industrial sectors, transportation networks, energy systems, and urban services presents substantial opportunity for semiconductor-enabled hardware such as sensors, microcontrollers, communication chips, and embedded processors integrated within connected devices and control platforms supporting digital transformation initiatives nationwide. Industrial modernization in manufacturing, agriculture processing, and logistics requires semiconductor-based automation equipment including programmable controllers, robotics interfaces, and sensor networks capable of improving efficiency and monitoring operations in real time, expanding demand for embedded semiconductor systems. Smart city initiatives incorporating traffic management, surveillance, environmental monitoring, and utility control systems rely on semiconductor-driven electronics and connectivity hardware deployed across urban infrastructure networks. Energy sector modernization including smart grids, renewable energy management systems, and distributed monitoring platforms also depends on semiconductor-enabled control and communication devices embedded in generation and distribution systems. Transportation digitization and mobility management solutions such as intelligent transport systems and vehicle electronics further expand semiconductor hardware adoption across national infrastructure.

Future Outlook

Kenya’s semiconductor infrastructure market is expected to expand steadily as telecom modernization, data center growth, and electronics manufacturing initiatives increase demand for semiconductor-enabled hardware systems. Industrial automation and smart infrastructure adoption will broaden semiconductor deployment across sectors. Government digitalization and connectivity programs will sustain infrastructure investment.

Major Players

- Intel

- Qualcomm

- Broadcom

- Texas Instruments

- Samsung Electronics

- NVIDIA

- AMD

- STMicroelectronics

- NXP Semiconductors

- MediaTek

- Huawei Technologies

- Cisco Systems

- Ericsson

- Nokia

- Juniper Networks

Key Target Audience

- Telecom network operators

- Data center operators

- Electronics manufacturing firms

- Investments and venture capitalist firms

- Government and regulatory bodies

- Industrial automation companies

- Automotive and mobility technology firms

- Smart infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

Key variables including telecom infrastructure investment, data center capacity expansion, electronics manufacturing activity, and industrial automation adoption were identified. Semiconductor hardware demand drivers were mapped across connectivity, computing, and embedded system domains. Technology deployment intensity across sectors was analyzed.

Step 2: Market Analysis and Construction

Market sizing integrated ICT hardware expenditure, telecom equipment procurement, and electronics infrastructure deployment patterns across industries. Segment shares were derived from infrastructure investment distribution across telecom, computing, and embedded systems. Geographic clustering informed infrastructure concentration.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on semiconductor infrastructure demand were validated through vendor hardware deployment data, telecom modernization trends, and digital economy indicators. Cross-verification ensured consistency with ICT and electronics hardware spending patterns. Technology adoption trajectories were assessed.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into segmentation, competitive, and market dynamic frameworks. Infrastructure demand drivers and constraints were integrated into analysis. Final outputs combined quantitative estimates with structural semiconductor ecosystem assessment for Kenya.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of electronics manufacturing and assembly in Kenya

Government push for local value addition in electronics supply chains

Rising demand for semiconductor-enabled telecom and automotive devices - Market Challenges

Absence of full-scale wafer fabrication ecosystem in Kenya

High capital and technology barriers for semiconductor infrastructure

Limited specialized workforce in semiconductor engineering - Market Opportunities

Development of assembly and test hubs for regional electronics markets

Semiconductor prototyping and design labs for academia and startups

Integration of semiconductor packaging in electronics clusters - Trends

Shift toward advanced semiconductor packaging capabilities

Adoption of modular cleanroom and microfab facilities - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Semiconductor assembly and packaging equipment

Wafer fabrication support systems

Semiconductor testing and inspection equipment

Cleanroom and contamination control systems

Semiconductor materials handling and automation - By Platform Type (In Value%)

Outsourced assembly and test facilities

Electronics manufacturing clusters

Research and prototyping labs

University semiconductor centers

Industrial automation parks - By Fitment Type (In Value%)

Greenfield semiconductor facilities

Brownfield electronics plant upgrades

Modular cleanroom installations

Pilot and prototyping lines - By End User Segment (In Value%)

Electronics manufacturers

Telecom equipment producers

Automotive electronics firms

- Market Share Analysis

- Cross Comparison Parameters (Process capability, Facility scalability, Cleanroom class compliance, Automation level, Technology support ecosystem, Yield optimization capability, Equipment integration compatibility, Throughput efficiency, Local service availability, Total lifecycle cost)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Applied Materials

Lam Research

KLA Corporation

ASML

Tokyo Electron

SCREEN Semiconductor Solutions

ASM International

Advantest

Teradyne

Kulicke and Soffa

Besi

Veeco Instruments

Edwards Vacuum

MKS Instruments

Foxconn Technology Group

- Electronics manufacturers investing in local assembly and packaging capacity

- Telecom device producers seeking regional semiconductor sourcing

- Automotive electronics firms exploring localized component assembly

- Research institutions building semiconductor prototyping facilities

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now