Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Kenya Semiconductor Manufacturing market is valued at approximately USD ~ million based on a recent historical assessment, driven by the increasing demand for semiconductors in sectors like telecommunications, electronics, automotive, and industrial applications. The growth is further supported by advancements in manufacturing processes, increased local demand for consumer electronics, and the expanding use of semiconductors in emerging technologies such as IoT, AI, and electric vehicles. This demand is also encouraged by local policies aimed at boosting the tech industry in Africa.

Key regions driving the semiconductor manufacturing market in Kenya include Nairobi, Mombasa, and Kisumu. Nairobi, being the capital, is a major hub for technology startups and multinational companies, driving demand for semiconductors in the electronics and telecommunications sectors. Mombasa’s growing industrial base, including its port operations, has positioned it as a key location for the import and distribution of semiconductor-related components. Kisumu is emerging as a growing center for innovation, with investments in manufacturing infrastructure contributing to the increasing production capacity for semiconductors.

Market Segmentation

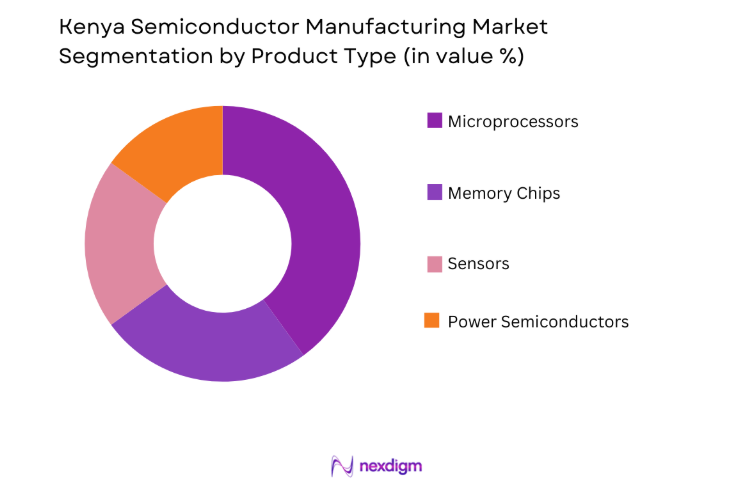

By Product Type

The Kenya Semiconductor Manufacturing market is segmented by product type into memory chips, sensors, microprocessors, and power semiconductors. Recently, microprocessors have dominated the market share due to their increasing use in a wide range of consumer electronics, automotive systems, and industrial applications. As Kenya experiences growth in sectors such as mobile technology, computing, and automotive manufacturing, the demand for microprocessors continues to rise. These components are essential for enabling complex functionalities in smartphones, laptops, and electric vehicles, driving their dominance in the market.

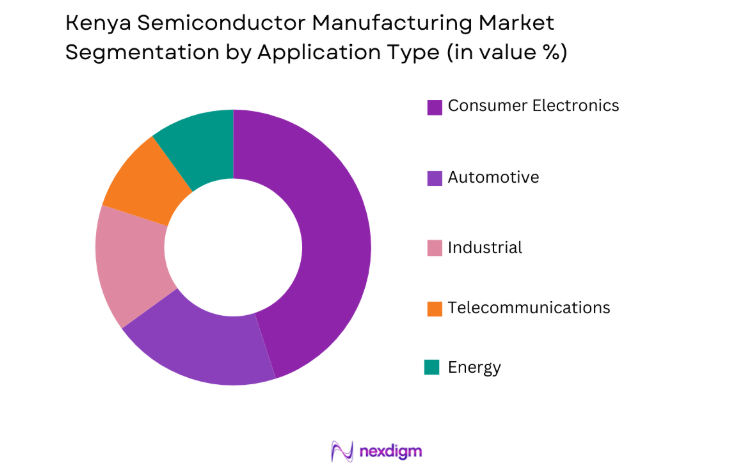

By Application Type

The Kenya Semiconductor Manufacturing market is also segmented by application type into consumer electronics, automotive, industrial, telecommunications, and energy. Consumer electronics applications hold the largest market share due to the high demand for smartphones, laptops, and other connected devices. As the adoption of technology in Kenya grows, so does the demand for semiconductor components, particularly microprocessors and memory chips, used in these devices. The growing middle class, rising disposable incomes, and expanding connectivity are significant factors driving the demand for consumer electronics in the region.

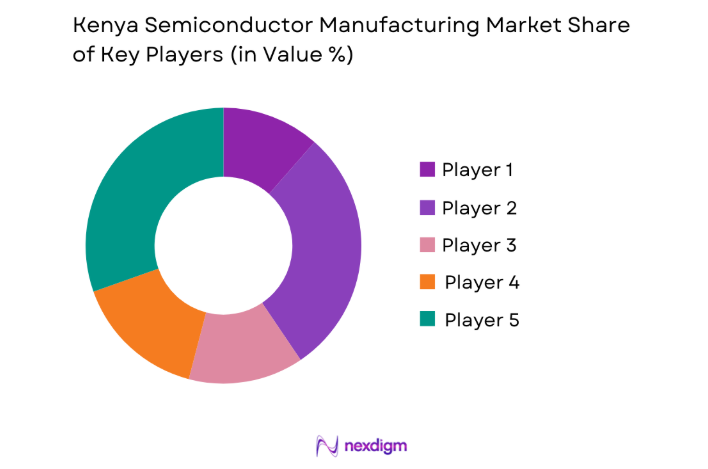

Competitive Landscape

The competitive landscape of the Kenya Semiconductor Manufacturing market is still in its early stages, with key global semiconductor manufacturers entering the market through partnerships and collaborations with local players. Market consolidation is expected as more multinational companies invest in local production capabilities. Local players are focusing on improving their manufacturing processes and technological capabilities to compete with international firms. With increasing demand for semiconductors across various industries, major players are investing in R&D and increasing production capacities to meet local market needs while expanding their reach across the African continent.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Industry-Specific Focus |

| Intel Corporation | 1968 | Santa Clara, USA | ~ | ~ | ~ | ~ | ~ |

| Samsung Electronics | 1938 | Seoul, South Korea | ~ | ~ | ~ | ~ | ~ |

| STMicroelectronics | 1987 | Geneva, Switzerland | ~ | ~ | ~ | ~ | ~ |

| NXP Semiconductors | 2006 | Eindhoven, Netherlands | ~ | ~ | ~ | ~ | ~ |

| Texas Instruments | 1930 | Dallas, USA | ~ | ~ | ~ | ~ | ~ |

Kenya Semiconductor Manufacturing Market Analysis

Growth Drivers

Technological Advancements in Consumer Electronics

The growth of the Kenya Semiconductor Manufacturing market is being fueled by advancements in consumer electronics, particularly smartphones, laptops, and wearables. The increasing penetration of mobile technology and the demand for smarter, more connected devices are driving the need for more advanced semiconductor components. As the adoption of 4G and 5G networks in Kenya accelerates, the demand for devices that support these technologies will continue to rise. Semiconductor manufacturers are responding by producing more efficient and powerful microprocessors, memory chips, and sensors, which are essential to the functionality of these devices. Additionally, the rise of the Internet of Things (IoT) is creating new opportunities for semiconductors, as the growing network of connected devices demands smaller, more efficient chips capable of handling complex tasks. This technology-driven demand is pushing the growth of the semiconductor manufacturing sector in Kenya, as local companies seek to capitalize on these emerging trends.

Government Investment in Infrastructure and Tech Development

The Kenyan government is playing a pivotal role in driving the growth of the semiconductor manufacturing market by investing in infrastructure development and encouraging technological innovation. Policies aimed at boosting the local manufacturing sector, such as tax incentives for tech companies and infrastructure improvements in key industrial hubs, are making it easier for companies to establish production facilities in Kenya. The government’s focus on building a digital economy, enhancing the country’s technological capacity, and positioning Kenya as a regional hub for tech innovation is further supporting the semiconductor market. Additionally, initiatives such as the “Kenya Vision 2030” plan, which aims to make Kenya a middle-income country through industrialization, are creating favorable conditions for the semiconductor industry. These investments are expected to attract both local and foreign companies to the sector, further driving market growth and establishing Kenya as a key player in the semiconductor supply chain.

Market Challenges

High Production Costs

A major challenge for the Kenya Semiconductor Manufacturing market is the high cost of production, which stems from the need for advanced manufacturing facilities, skilled labor, and high-quality materials. Semiconductor manufacturing is a capital-intensive process that requires substantial investment in infrastructure, technology, and skilled workforce development. Many local players face difficulty in securing the funding needed to build these sophisticated production facilities. Moreover, the price of raw materials such as silicon and metals used in semiconductor production remains high, which drives up the overall cost of manufacturing. As a result, this challenge limits the ability of smaller players to compete effectively in the global market. Additionally, the volatility of commodity prices can further strain production costs, making it harder for Kenyan manufacturers to offer competitive pricing.

Dependence on Imports

The semiconductor manufacturing industry in Kenya is heavily dependent on the importation of advanced equipment and raw materials. While the local demand for semiconductors continues to grow, Kenya lacks the necessary resources to produce high-end equipment and materials required for semiconductor fabrication. This reliance on imports creates vulnerabilities in the supply chain, especially in times of global economic disruptions or trade imbalances. Local manufacturers also face challenges in obtaining the latest technology and maintaining consistent access to raw materials, which hinders their ability to scale production and improve manufacturing efficiency. As a result, the dependency on international suppliers limits the competitiveness of the local market and increases operational risks, particularly for small and medium-sized enterprises (SMEs) in the sector.

Opportunities

Expansion of Automotive Industry

The growing automotive sector in Kenya presents significant opportunities for the semiconductor manufacturing market. As the demand for vehicles increases, there is a greater need for advanced automotive electronics, including sensors, microcontrollers, and power semiconductors, to support the development of smart vehicles and electric vehicles (EVs). The automotive industry is rapidly embracing new technologies such as autonomous driving, vehicle connectivity, and electrification, all of which rely heavily on semiconductors. With the rise of electric vehicle adoption in Kenya and the East African region, semiconductor manufacturers have a unique opportunity to cater to the automotive sector’s growing demand for advanced, high-performance chips. As Kenya’s automotive manufacturing capabilities expand, local semiconductor producers can establish themselves as key suppliers to the industry, tapping into both domestic and regional markets.

Growth of the Electronics and Telecommunications Sector

The expansion of the electronics and telecommunications sectors in Kenya presents a substantial growth opportunity for the semiconductor manufacturing market. The demand for semiconductors in mobile phones, consumer electronics, and telecommunications infrastructure is expected to increase as the country continues to experience high growth in mobile connectivity, digital services, and smart devices. The widespread adoption of 4G and 5G networks will further fuel the demand for advanced semiconductor components to support these technologies. Additionally, the increasing focus on IoT applications across sectors such as healthcare, agriculture, and smart cities will drive the need for smaller, more efficient semiconductors. By capitalizing on these trends, local semiconductor manufacturers in Kenya can establish a strong foothold in the fast-growing electronics and telecommunications industries.

Future Outlook

The Kenya Semiconductor Manufacturing market is expected to witness significant growth over the next five years, driven by technological advancements, increasing demand for consumer electronics, and expanding applications in automotive and telecommunications. As infrastructure development continues and government support for the tech industry strengthens, the market will see increased local manufacturing capabilities. Moreover, the growing adoption of electric vehicles, IoT, and 5G technology in Kenya will drive further demand for advanced semiconductors. However, challenges such as high production costs and dependence on imports must be addressed for Kenya to become a key player in the semiconductor industry.

Major Players

- Intel Corporation

- Samsung Electronics

- STMicroelectronics

- NXP Semiconductors

- Texas Instruments

- Micron Technology

- Qualcomm

- Broadcom

- ON Semiconductor

- Renesas Electronics

- Infineon Technologies

- Analog Devices

- MediaTek

- Applied Materials

- GlobalFoundries

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive manufacturers

- Electronics manufacturers

- Telecommunications companies

- Semiconductor equipment suppliers

- Energy providers

Research Methodology

Step 1: Identification of Key Variables

Identify key market variables, including demand drivers, technological trends, and economic factors influencing the semiconductor manufacturing sector in Kenya.

Step 2: Market Analysis and Construction

Analyze market size, trends, segmentation, and growth patterns to build a comprehensive market model, incorporating data from primary and secondary sources.

Step 3: Hypothesis Validation and Expert Consultation

Validate the hypotheses through consultations with industry experts and stakeholders to ensure the accuracy and relevance of the findings.

Step 4: Research Synthesis and Final Output

Synthesize the research findings into a final report that includes data analysis, insights, and expert opinions to provide actionable market intelligence for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Growth in consumer electronics demand

Technological advancements in semiconductor manufacturing

Increase in automotive electronics

Expanding telecommunications infrastructure - Market Challenges

High capital investment required for manufacturing

Supply chain and raw material challenges

Regulatory hurdles and compliance with global standards - Market Opportunities

Increasing demand for 5G semiconductors

Emerging opportunities in electric vehicle components

Growth in wearable devices and IoT applications - Trends

Advancements in chip miniaturization

Increased adoption of AI and machine learning in manufacturing - Government Regulations

Compliance with international semiconductor standards

Incentives for semiconductor R&D

Environmental regulations impacting manufacturing processes - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Integrated Circuits

Discrete Semiconductors

Optoelectronics

Sensors

Microelectromechanical Systems (MEMS) - By Platform Type (In Value%)

Manufacturing Equipment

Design Software

Testing Equipment

Packaging Materials - By Fitment Type (In Value%)

Standard Fitment

Custom Fitment

Integrated Fitment

Modular Fitment - By End User Segment (In Value%)

Consumer Electronics

Automotive

Telecommunications

Healthcare

- Market Share Analysis

- Cross Comparison Parameters (System Type, Fitment Type, Platform Type, End User Segment, Technology Integration, Price, Manufacturing Complexity)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Intel Corporation

Samsung Electronics

TSMC

GlobalFoundries

STMicroelectronics

NXP Semiconductors

Qualcomm

Micron Technology

Broadcom

Texas Instruments

MediaTek

Infineon Technologies

ON Semiconductor

Analog Devices

Renesas Electronics

- Consumer electronics manufacturers’ adoption of semiconductors

- Automotive industry’s growing reliance on semiconductors

- Telecom sector’s demand for high-performance chips

- Healthcare industry’s integration of medical semiconductors

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now