Download PDF

Download PDF Download PDF

Download PDFMarket Overview:

Adaptive Cruise Control (ACC) is an Advanced Driver Assistance System (ADAS) feature that automatically adjusts a vehicle’s speed to maintain a safe following distance from the car ahead. It combines radar, camera, and sensor technologies to monitor traffic and adjust acceleration and braking without driver intervention, enhancing safety and comfort during highway and urban driving. ACC is seen as an important stepping stone toward semi‑autonomous driving.The ACC and related safety systems market (including ACC & BSD) in Saudi Arabia is projected to grow significantly — with combined segments expected to reach around USD ~billion by 2030, at a robust annual growth rate driven by safety feature adoption.

While specific KSA‑only ACC figures vary across sources, the global ACC market is expected to grow strongly (e.g., from around USD ~B in 2024 to USD ~by 2030), indicating parallel regional growth within Saudi Arabia driven by global trends.

Market Segmentation

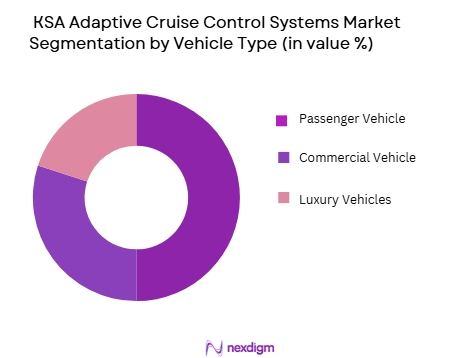

By Vehicle Type

The KSA ACC market is segmented into passenger vehicles, commercial vehicles, and luxury vehicles. Passenger vehicles dominate the market due to the growing awareness of road safety and the increasing availability of ACC systems in mainstream models. Within the passenger vehicle segment, the rising popularity of SUVs and sedans equipped with advanced safety features is a key trend. The commercial vehicle segment, though smaller, is showing growth driven by fleet management requirements and regulatory mandates for safer road transportation. Luxury vehicles, while representing a smaller share, lead in ACC system adoption due to consumer demand for high-end features.

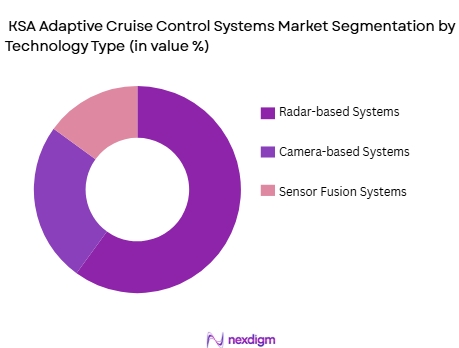

By Technology Type

The ACC system market in Saudi Arabia is primarily segmented by technology type into radar-based systems, camera-based systems, and sensor fusion-based systems. Radar-based systems currently lead the market as they are more reliable and cost-effective compared to other technologies. These systems use electromagnetic waves to detect objects and adjust the speed of vehicles accordingly. Camera-based systems are gaining traction due to their ability to detect lane markings and traffic signals, which complement the radar-based systems in more advanced implementations. Sensor fusion technology, which integrates radar and camera data, is emerging but still in the developmental stage, contributing to a smaller segment of the market.

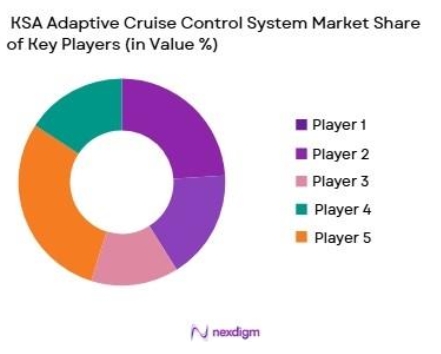

Competitive Landscape

The market in KSA is highly competitive, with major international automotive brands such as Toyota, BMW, and Mercedes-Benz leading the way in terms of implementing ACC systems in their vehicles. These companies are complemented by emerging regional players and local distributors that integrate aftermarket solutions into vehicles. Companies in the KSA market are striving to differentiate themselves through the inclusion of additional safety features, better integration with existing car systems, and enhanced user experiences via smart technologies like IoT.

| Company Name | Establishment Year | Headquarters | Product Portfolio | Key Markets | Distribution Channels | Technology Used |

| Toyota | 1937 | Japan | ~ | ~ | ~ | ~ |

| BMW | 1916 | Germany | ~ | ~ | ~ | ~ |

| Mercedes-Benz | 1926 | Germany | ~ | ~ | ~ | ~ |

| Hyundai | 1967 | South Korea | ~ | ~ | ~ | ~ |

| General Motors | 1908 | USA | ~ | ~ | ~ | ~ |

KSA Adaptive Cruise Control Systems Market Analysis

Growth Drivers

Urbanization

Urbanization is a major driver for the air quality monitoring system market in Indonesia. With urban population growth reaching ~in 2022, as reported by the World Bank, the increase in urban areas, especially in cities like Jakarta and Surabaya, has led to a rise in vehicular emissions and industrial activities, which in turn increases air pollution levels. The expansion of these urban areas necessitates effective monitoring systems to manage air quality and protect public health. Urban growth fuels demand for real-time air quality data to mitigate health risks, thus driving market demand.

Industrialization

Industrialization has significantly impacted air quality in Indonesia, contributing to the demand for air quality monitoring systems. The manufacturing sector accounted for ~ of the country’s GDP in 2022, according to the World Bank. This industrial growth has led to emissions of particulate matter, nitrogen dioxide, and sulfur dioxide, primarily from sectors like construction, mining, and manufacturing. The Indonesian government is taking steps to reduce these emissions, creating a need for advanced monitoring technologies to ensure compliance with stricter regulations and control pollution.

Restraints

High Initial Costs

The high initial costs associated with the installation of air quality monitoring systems represent a significant barrier to their widespread adoption in Indonesia. According to the Ministry of Finance, setting up a basic air quality station in an urban area can cost up to IDR ~million. The cost of purchasing advanced sensors, along with infrastructure for data management and regular maintenance, poses financial challenges, particularly for smaller municipalities and businesses. Despite the long-term benefits of monitoring, the high upfront costs limit the ability of lower-income regions to invest in these systems. Source: Ministry of Finance, Indonesia .

Technical Challenges

Technical challenges associated with maintaining and calibrating air quality monitoring systems are a major constraint in Indonesia. Environmental factors, such as high humidity, temperature fluctuations, and particulate buildup, can affect the accuracy and lifespan of sensors. In 2022, the Ministry of Environment and Forestry reported that around ~of monitoring stations experienced malfunctions due to these environmental conditions. The complexity of maintaining the accuracy of these systems, along with the need for frequent recalibrations, reduces the effectiveness of monitoring efforts, hindering market growth. Source: Ministry of Environment and Forestry, Indonesia

Opportunities

Technological Advancements

Technological advancements in air quality monitoring systems present major growth opportunities in Indonesia. The development of low-cost, IoT-enabled sensors and advanced data analytics has made air quality monitoring more accessible and affordable. Innovations such as AI-powered real-time air quality data analysis are improving the accuracy and efficiency of monitoring systems. In 2022, the Indonesian government collaborated with tech companies to deploy IoT-based air quality monitoring systems, making it easier to track pollution levels remotely. These advancements have the potential to expand the market by making monitoring systems more cost-effective for a wider range of users. Source: Ministry of Environment and Forestry, Indonesia

International Collaborations

International collaborations between Indonesia and global environmental organizations offer significant opportunities to enhance the country’s air quality monitoring capabilities. In 2022, Indonesia entered into partnerships with the United Nations Environment Programmed (UNEP) to improve air quality management. These collaborations enable the transfer of advanced technology, expertise, and funding to support the development of Indonesia’s monitoring infrastructure. Additionally, international environmental funds are contributing to projects aimed at enhancing air quality monitoring in urban and industrial regions, which will help accelerate market growth. Source: United Nations Environment Programmed

Future Outlook

The KSA Adaptive Cruise Control Systems market is expected to experience steady growth over the next several years, driven by advancements in vehicle automation and continued government support for the integration of intelligent transportation systems (ITS) as part of the Vision 2030 initiative. Increased demand for safety features, regulatory mandates for ADAS in new vehicles, and the growing popularity of semi-autonomous driving technologies are all expected to fuel market expansion. Additionally, advancements in radar, sensor fusion technologies, and AI-driven features will likely shape the future of the market, making ACC systems a standard feature in Saudi vehicles.

Major Players

- Toyota

- BMW

- Mercedes-Benz

- Hyundai

- General Motors

- Audi

- Nissan

- Ford

- Volkswagen

- Honda

- Tesla

- Volvo

- Kia

- Mazda

- Porsche

Key Target Audience

- Automotive Manufacturers

- Vehicle OEMs and Tier 1 Suppliers

- Regulatory Bodies

- Government Agencies

- Automotive Technology Innovators

- Fleet Management Companies

- Vehicle Dealerships and Aftermarket Installers

- Investment and Venture Capital Firms

Research Methodology

step 1: Identification of Key Variables

The initial phase focuses on identifying key market variables influencing the adoption of Adaptive Cruise Control Systems in KSA. This involves gathering data from secondary sources such as government reports, industry publications, and market databases.

Step 2: Market Analysis and Constructions

We analyze historical data on the adoption of automotive safety technologies in KSA, focusing on trends in vehicle type, technology preferences, and demand for ADAS features. This helps construct accurate market projects.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses on growth drivers, challenges, and opportunities are validated through interviews with industry experts, OEM representatives, and suppliers of ADAS technologies. This phase ensures that market insights align with real-world developments.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Consolidated Research Approach, Understanding Market Potential Through In-Depth Industry Interviews, Primary Research Approach, Limitations and Future Conclusions)

- Definition and Scope

- Market Genesis in KSA

- Timeline of Key Milestones

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers

Rising Adoption of Autonomous Driving Technologies

Government Push for Automotive Safety

Increasing Demand for Luxury Vehicles - Market Challenges

High Initial Implementation Costs

Integration Challenges with Existing Systems

Regulatory and Compliance Hurdles - Opportunities

Government Support for Smart City Initiatives

Emerging Demand for Autonomous Vehicle Features

Increased Focus on Road Safety and Traffic Efficiency - Trends

Adoption of Semi-autonomous Vehicle Technologies

Integration with IoT and 5G Networks

Innovations in Sensor Technology - Government Regulation

Road Safety Standards

Environmental Regulations and Impact on Vehicle Features - SWOT Analysis

Stakeholder Ecosystem

Porter’s Five Forces Analysis

Competition Ecosystem

- By Value, 2026-2030

- By Volume, 2026-2030

- By Average Price, 2026-2025

- By Vehicle Type, (In Value %)

Luxury Vehicles

Economy Vehicles

Commercial Vehicles - By Technology Type,(In Value %)

Radar-Based Systems

Camera-Based Systems

LIDAR-Based Systems - By Distribution Channel, (In Value %)

OEM Integration

Aftermarket Installations - By Region, (In Value %)

Central Region

Western Region

Eastern Region - By Vehicle Manufacturer, (In Value %)

Toyota

BMW

Mercedes-Benz

- Cross Comparison Parameters:(Company Overview, Business Strategies, Recent Developments, Strengths, Weaknesses, Organizational Structure, Revenues, Revenues by Segment, Number of Touchpoints, Distribution Channels, Margins, Production Plant, Capacity, Unique Value Offering, and Others)

- SWOT Analysis of Major Players

- Pricing Analysis

- Detailed Profiles of Major Companies

Toyota

BMW

Mercedes-Benz

Ford

Audi

Hyundai

Nissan

Honda

Tesla

General Motors

Volkswagen Group

Mazda

Kia

Porsche

Fiat Chrysler Automobiles

- Market Demand and Utilization

- Purchasing Power and Budget Allocations

- Regulatory and Compliance Requirements

- Needs, Desires, and Pain Point Analysis

- Decision-Making Process

- Forecast Market Value 2026-2035

- Forecast Installed Units 2026-2035

- Price Forecast by System Tier 2026-2035

- Future Demand by Platform 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now