Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the KSA Advanced Materials market is valued at approximately USD ~ billion according to industry analyses from the Saudi Ministry of Industry and Mineral Resources, SABIC industry disclosures, and international materials sector databases. Market growth is driven by expanding petrochemical downstream industries, large infrastructure construction programs, renewable energy manufacturing initiatives, and increasing use of high-performance composites, polymers, and specialty materials across aerospace, energy, and automotive manufacturing sectors.

Major industrial activity driving demand for advanced materials is concentrated across Riyadh, Jubail, Yanbu, and Dammam where petrochemical complexes, industrial clusters, and advanced manufacturing zones operate. Jubail Industrial City and Yanbu Industrial City host large petrochemical and specialty chemical production facilities supplying advanced polymers and composite materials. Riyadh leads in aerospace manufacturing, construction engineering, and defense industries that require high performance materials, while Dammam functions as a logistics and industrial hub supporting materials distribution and fabrication across eastern Saudi Arabia.

Market Segmentation

By Product Type

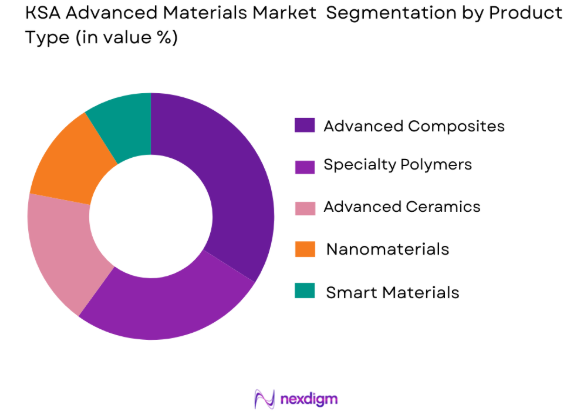

KSA Advanced Materials market is segmented by product type into advanced composites, specialty polymers, nanomaterials, advanced ceramics, and smart materials. Recently, advanced composites has a dominant market share due to factors such as strong demand from aerospace manufacturing, defense engineering, automotive components production, and energy infrastructure development. Composite materials provide superior strength to weight ratio, corrosion resistance, and durability compared with conventional materials. Saudi Arabia’s expanding aerospace sector and renewable energy projects rely heavily on composite structures used in aircraft components, wind turbine blades, and high performance engineering systems. Infrastructure megaprojects also utilize composite reinforcement materials for bridges, pipelines, and large construction projects. Industrial diversification initiatives encourage local manufacturing of composite materials to reduce reliance on imported high performance engineering materials. As industries prioritize lightweight materials capable of improving efficiency and reducing operational costs, advanced composites continue to dominate product type demand across the advanced materials ecosystem in Saudi Arabia.

By End User Industry

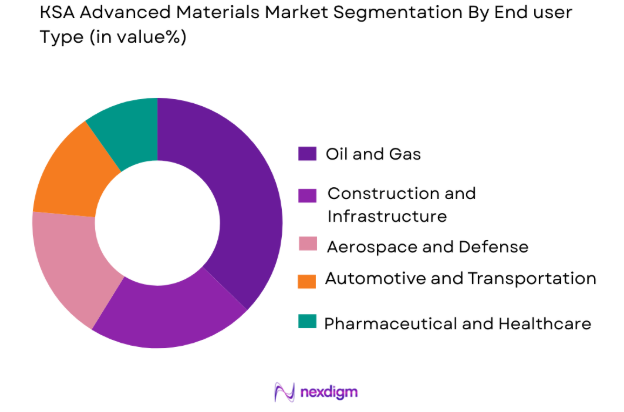

KSA Advanced Materials market is segmented by end user industry into oil and gas, aerospace and defense, construction and infrastructure, automotive and transportation, and electronics manufacturing. Recently, oil and gas has a dominant market share due to factors such as the extensive hydrocarbon production infrastructure operating across Saudi Arabia and the need for corrosion resistant and high temperature materials in energy facilities. Advanced alloys, composite materials, and specialized coatings are widely used in pipelines, drilling equipment, offshore platforms, and refining systems where extreme operating conditions require durable materials capable of maintaining performance over long operational cycles. Saudi Arabia’s large energy sector continues to upgrade infrastructure with advanced materials designed to improve operational efficiency and reduce maintenance requirements. Expansion of petrochemical processing facilities also increases demand for advanced polymers and specialty materials used in industrial equipment and processing systems.

Competitive Landscape

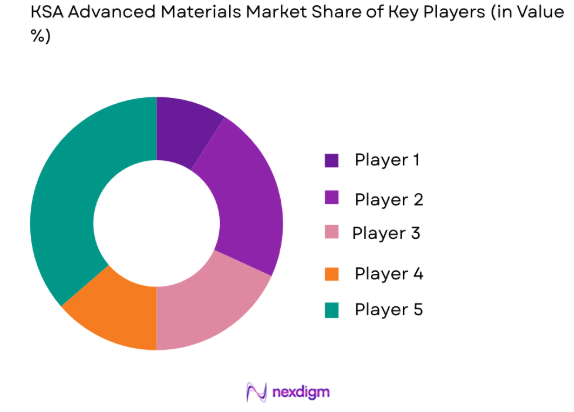

The KSA Advanced Materials market is moderately consolidated with several large global materials manufacturers operating alongside major regional petrochemical producers. Multinational companies provide advanced composites, nanomaterials, and specialty chemicals, while Saudi industrial companies focus on petrochemical derived advanced polymers and engineered materials. Strategic partnerships between international technology providers and domestic manufacturers are expanding local production capabilities and supporting industrial diversification initiatives.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Industrial Application Focus |

| Saudi Basic Industries Corporation | 1976 | Riyadh, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| BASF SE | 1865 | Ludwigshafen, Germany | ~ | ~ | ~ | ~ | ~ |

| Dow Inc | 1897 | Michigan, USA | ~ | ~ | ~ | ~ | ~ |

| Toray Industries | 1926 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ |

| Hexcel Corporation | 1948 | Connecticut, USA | ~ | ~ | ~ | ~ | ~ |

KSA Advanced Materials Market Analysis

Growth Drivers

Expansion of Industrial Diversification and Manufacturing Development Programs

Saudi Arabia’s long term economic transformation strategy encourages large scale industrial diversification initiatives designed to reduce reliance on hydrocarbon exports while developing advanced manufacturing capabilities across aerospace automotive defense and renewable energy sectors. Industrial policy initiatives encourage local manufacturing of high performance materials including composites polymers specialty chemicals and advanced alloys required for modern industrial production. Large scale manufacturing clusters located in Jubail Yanbu and Riyadh attract multinational materials manufacturers seeking regional production bases capable of supplying Middle Eastern and African markets. Government supported industrial zones provide infrastructure tax incentives and research funding designed to encourage advanced materials innovation and manufacturing development. Aerospace manufacturing programs operating in Riyadh require carbon fiber composites and specialized engineering materials used in aircraft structures propulsion components and high performance mechanical systems. Automotive assembly operations also increasingly incorporate lightweight materials designed to improve fuel efficiency and vehicle durability. Industrial modernization initiatives implemented across petrochemical and energy sectors also increase demand for corrosion resistant materials capable of withstanding extreme industrial conditions. Renewable energy projects including large solar and wind installations require specialized materials capable of maintaining structural stability under harsh environmental conditions. As Saudi Arabia continues expanding its industrial base the demand for advanced materials correspondingly increases across multiple manufacturing sectors.

Rapid Expansion of Energy Infrastructure and Petrochemical Processing Facilities

Saudi Arabia operates one of the largest energy production systems in the world including extensive oil extraction infrastructure refining facilities and petrochemical processing plants distributed across major industrial regions. These facilities operate under extremely demanding environmental conditions involving high temperatures chemical exposure and mechanical stress which require specialized materials capable of maintaining performance and structural integrity over extended operational cycles. Advanced materials including corrosion resistant alloys composite pipeline materials thermal barrier coatings and high performance polymers therefore become essential components of energy infrastructure systems. Petrochemical plants also rely heavily on specialty materials used in chemical processing equipment pressure vessels and high temperature reactors. Continuous modernization of energy infrastructure increases demand for materials capable of improving operational efficiency reducing equipment degradation and extending facility lifespan. Offshore drilling operations require composite materials and advanced alloys capable of resisting corrosion caused by seawater and chemical exposure. Large scale pipeline networks transporting hydrocarbons across long distances require durable materials capable of maintaining mechanical stability under high pressure conditions. Refining facilities also integrate advanced catalytic materials designed to improve chemical processing efficiency and product output. Expansion of downstream petrochemical manufacturing further increases demand for advanced polymers and specialty chemical materials used in industrial production systems.

Market Challenges

High Production Costs and Limited Domestic Processing Capabilities for Specialized Materials

Advanced materials production involves complex manufacturing processes including high temperature chemical synthesis precision polymer engineering nanotechnology fabrication and specialized composite manufacturing techniques that require sophisticated industrial infrastructure and significant capital investment. Many advanced material production processes rely on specialized equipment cleanroom environments and highly trained technical personnel capable of operating complex manufacturing systems. Saudi Arabia currently imports several high performance materials including carbon fiber nanomaterials and specialized ceramic materials because domestic processing capacity remains limited for certain advanced technologies. Establishing local manufacturing facilities capable of producing these materials requires large scale industrial investment and technology transfer partnerships with international material science companies. High energy consumption during advanced material manufacturing also increases operational costs particularly for processes involving high temperature furnaces chemical reactors and precision fabrication equipment. Small scale domestic manufacturers often face financial barriers when attempting to enter advanced materials production due to high research development and equipment costs. Certification requirements for aerospace automotive and defense materials also require extensive testing procedures that increase product development timelines and production expenses. These factors collectively create cost barriers that slow domestic expansion of advanced materials manufacturing capabilities.

Complex Certification Standards and Technology Transfer Limitations in Advanced Materials Manufacturing

Advanced materials used in aerospace defense automotive and energy infrastructure must comply with strict international certification standards designed to ensure reliability performance and safety during operation. Certification processes involve extensive laboratory testing performance validation and long term durability analysis which significantly increases the time required to introduce new materials into industrial supply chains. Companies seeking to manufacture advanced composite materials or nanotechnology based materials must often collaborate with international certification organizations capable of validating product performance against global industry standards. Technology transfer restrictions also limit access to certain advanced materials manufacturing technologies particularly those used in aerospace defense and semiconductor industries. International companies may hesitate to transfer proprietary production processes due to intellectual property protection concerns and strategic industrial considerations. Domestic manufacturers therefore face challenges when attempting to acquire advanced production technologies necessary for high performance materials manufacturing. Research and development investment required to independently develop similar technologies can require significant financial resources and long development timelines. These regulatory and technological barriers slow expansion of domestic advanced materials innovation within Saudi Arabia’s industrial ecosystem.

Opportunities

Development of Renewable Energy Infrastructure Requiring Advanced Structural Materials

Saudi Arabia continues investing heavily in renewable energy infrastructure including large scale solar power facilities wind energy projects and hydrogen production initiatives designed to diversify national energy sources. Renewable energy technologies require specialized advanced materials capable of maintaining durability under extreme environmental conditions including high temperature desert climates strong winds and prolonged ultraviolet radiation exposure. Solar panel mounting structures wind turbine blades and energy storage systems rely heavily on advanced composite materials lightweight alloys and specialized polymer coatings capable of protecting equipment from environmental degradation. Wind turbine blades in particular require high strength carbon fiber composite materials capable of supporting large structural loads while maintaining lightweight aerodynamic properties. Hydrogen production facilities also require specialized corrosion resistant materials capable of handling chemical processing environments involving hydrogen gas and electrolysis systems. Expansion of renewable energy manufacturing facilities within Saudi Arabia creates new industrial demand for locally produced advanced materials used in energy equipment manufacturing. Government renewable energy initiatives therefore create strong long term growth opportunities for advanced materials manufacturers capable of supplying structural materials used in next generation energy technologies.

Growth of Aerospace Manufacturing and Defense Industrial Development Programs

Saudi Arabia increasingly invests in domestic aerospace manufacturing and defense technology development programs designed to strengthen national security capabilities and expand high technology industrial sectors. Aerospace engineering requires specialized advanced materials including carbon fiber composites high temperature ceramic materials and lightweight metal alloys capable of supporting aircraft structures propulsion systems and defense equipment manufacturing. Aircraft components require materials capable of maintaining structural strength while minimizing weight in order to improve fuel efficiency and flight performance. Defense manufacturing programs also utilize advanced materials in missile systems armored vehicles communication equipment and radar infrastructure where material durability and performance reliability remain critical. Saudi aerospace manufacturing initiatives encourage partnerships with global aerospace companies capable of transferring advanced materials manufacturing technologies into domestic production facilities. Expansion of aerospace component manufacturing therefore increases demand for locally produced high performance materials. As defense technology development programs expand Saudi Arabia’s industrial ecosystem increasingly requires advanced materials capable of supporting sophisticated aerospace engineering systems and defense manufacturing technologies.

Future Outlook

The KSA Advanced Materials market is expected to experience steady expansion as industrial diversification programs continue supporting advanced manufacturing development across aerospace energy automotive and construction sectors. Renewable energy infrastructure projects and petrochemical processing expansion will increase demand for high performance materials capable of operating in demanding environments. Technological innovation in nanomaterials and smart materials will further enhance industrial applications. Government initiatives encouraging domestic production and research collaboration are expected to strengthen the national advanced materials manufacturing ecosystem.

Major Players

- Saudi Basic Industries Corporation

- BASF SE

- Dow Inc

- DuPont

- Toray Industries

- Hexcel Corporation

- Mitsubishi Chemical Group

- Huntsman Corporation

- Arkema SA

- Solvay SA

- LG Chem

- Covestro AG

- 3M Company

- Evonik Industries

- Teijin Limited

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aerospace and defense manufacturers

- Petrochemical and energy companies

- Automotive manufacturers

- Industrial manufacturing companies

- Construction and infrastructure developers

- Renewable energy equipment manufacturers

Research Methodology

Step 1: Identification of Key Variables

Primary industry variables including advanced material demand across aerospace petrochemical renewable energy and construction sectors were identified. Macroeconomic indicators industrial investment trends and manufacturing output data were also examined to determine market drivers influencing advanced materials consumption.

Step 2: Market Analysis and Construction

Market modeling involved analyzing production capacity trade flows industrial demand and manufacturing investments across Saudi Arabia. Data from industry associations government publications and corporate disclosures were integrated to estimate market structure and segmentation patterns.

Step 3: Hypothesis Validation and Expert Consultation

Industry specialists materials engineers and manufacturing executives were consulted to validate assumptions regarding technology adoption industrial demand and production capabilities. Expert insights ensured accuracy in understanding technological trends affecting advanced materials markets.

Step 4: Research Synthesis and Final Output

All research findings were synthesized through triangulation of industry databases government reports and company disclosures. Analytical frameworks were applied to generate comprehensive market insights covering competitive landscape demand drivers and long term industry outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Advanced Manufacturing and Industrial Diversification Initiatives

Growing Demand for High Performance Materials in Energy and Infrastructure Projects

Increasing Adoption of Lightweight and Durable Materials in Transportation Industries - Market Challenges

High Production Costs of Specialized Advanced Materials

Limited Domestic Raw Material Processing Capabilities

Complex Material Certification and Industrial Standardization Requirements - Market Opportunities

Development of Local Advanced Material Manufacturing Clusters

Growing Demand for High Performance Materials in Renewable Energy Projects

Strategic Partnerships with Global Material Technology Providers - Trends

Increasing Adoption of Nanotechnology Based Materials in Industrial Applications

Expansion of Smart Materials for Energy Efficient Infrastructure

Integration of Advanced Composite Materials in Aerospace and Automotive Manufacturing - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Advanced Composite Materials

High Performance Ceramics Specialty Polymers

Nanomaterials

Smart Materials - By Platform Type (In Value%)

Industrial Manufacturing Platforms

Construction and Infrastructure Platforms

Energy and Power Platforms

Automotive and Transportation Platforms

Aerospace and Defense Platforms - By Fitment Type (In Value%)

Structural Material Integration

Coating and Surface Engineering Solutions

Embedded Functional Materials

Thermal Management Material Integration

Protective Barrier Material Applications - By EndUser Segment (In Value%)

Oil and Gas Industry

Construction and Infrastructure Developers

Automotive and Transportation Manufacturers

Aerospace and Defense Organizations

Electronics and Semiconductor Industry - By Procurement Channel (In Value%)

Direct Industrial Procurement

Government Infrastructure

Industrial Distributors and Material Suppliers

Engineering Procurement Construction Firms

Strategic Technology Partnerships

- Market Share Analysis

- Cross Comparison Parameters (Material Technology Portfolio, Manufacturing Capability, Industry End User Coverage, Regional Supply Chain Presence, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Saudi Basic Industries Corporation

Advanced Petrochemical Company

Tasnee

3M Company

Dow Inc

DuPont

BASF SE

Toray Industries

Hexcel Corporation

Solvay SAMitsubishi

Chemical Group

Huntsman Corporation

Arkema SA

LG Chem

Covestro AG

- Energy sector companies increasing adoption of corrosion resistant and high temperature materials

- Construction sector demanding durable lightweight materials for mega infrastructure projects

- Automotive manufacturers integrating lightweight composites to improve fuel efficiency

- Electronics manufacturers adopting high performance materials for thermal and electrical applications

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035Price

- Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now