Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA aeroderivative gas turbine market is valued at approximately USD ~ billion in 2025, driven by increasing energy demand, strategic industrial growth, and the country’s Vision 2030 initiatives. The demand for efficient and flexible power generation solutions, such as gas turbines, is rising due to the country’s ambitious projects in oil, gas, and energy infrastructure. Saudi Arabia’s rapid development in sectors like petrochemicals, desalination, and power generation, combined with a shift towards cleaner energy sources, propels the adoption of advanced gas turbine technologies. The market’s growth is also attributed to increased investments in energy projects and government incentives aimed at reducing emissions and improving energy efficiency.

Saudi Arabia dominates the aeroderivative gas turbine market, with key cities like Riyadh, Jeddah, and Dhahran being central to the energy and industrial sectors. Riyadh is the heart of the country’s power generation projects, while Dhahran hosts major oil and gas infrastructure. Jeddah, located on the Red Sea coast, is pivotal for desalination projects and regional energy distribution. The dominance of these cities is rooted in Saudi Arabia’s strategic location, high demand for power, and large-scale industrial investments, positioning the Kingdom as the leader in the regional gas turbine market.

Market Segmentation

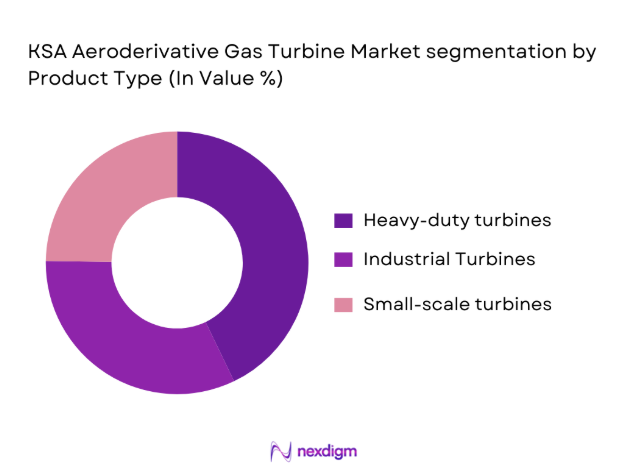

By Product Type

The Saudi aeroderivative gas turbine market is segmented by product type into heavy-duty turbines, industrial turbines, and small-scale turbines. Heavy-duty turbines dominate the market due to their widespread use in large-scale power generation plants and oil & gas operations. These turbines offer high reliability, flexibility, and efficiency, which is critical for KSA’s power generation sector that experiences fluctuations in energy demand. The need for reliability in extreme operating conditions, such as those found in oil and gas extraction, ensures that heavy-duty turbines will continue to command a significant share of the market.

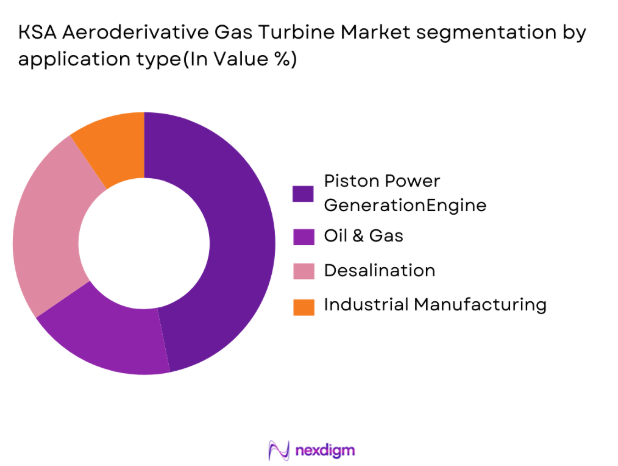

By Application

The application segmentation in the KSA aeroderivative gas turbine market includes power generation, oil & gas, desalination, and industrial manufacturing. Power generation is the dominant application for gas turbines in Saudi Arabia, driven by the country’s need for continuous, reliable electricity supply to support rapid urbanization and industrial expansion. Gas turbines are favored for their ability to offer high efficiency and flexibility, essential for both base-load and peak-load generation. The rising population and increased industrial activity further enhance the demand for turbines in the power generation sector.

Competitive Landscape

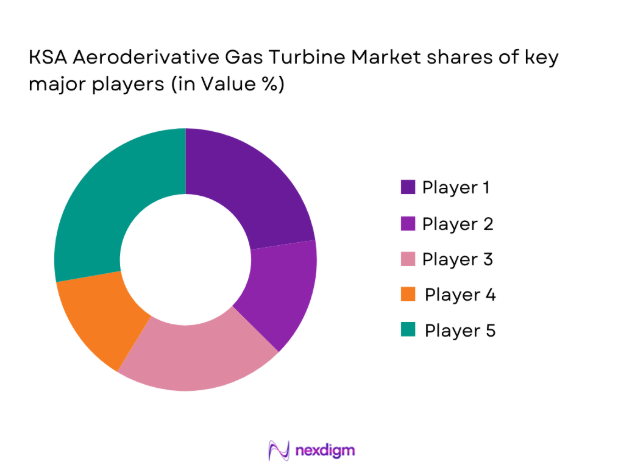

The KSA aeroderivative gas turbine market is dominated by a few major players, both international and local, who provide advanced turbine solutions tailored to the country’s growing energy sector. The market includes large global manufacturers such as General Electric, Siemens Energy, and Mitsubishi Heavy Industries, along with regional players like Doosan Heavy Industries & Construction. These companies leverage their expertise in turbine technology, local partnerships, and service agreements to maintain a strong competitive position. The Saudi Arabian market is competitive, with a few global leaders providing high-efficiency turbines designed for the country’s harsh operating conditions. Companies like General Electric and Siemens Energy lead the market with their proven, reliable, and efficient turbine solutions that meet the demands of Saudi Arabia’s expanding power generation and industrial sectors. Additionally, local players such as Saeed R. Al-Shaikh & Sons Company and Zamil Industrial have a growing presence, particularly in servicing the gas turbines and offering localized support for customers.

| Company | Establishment Year | Headquarters | Turbine Type | Market Focus | Key Differentiator |

| General Electric | 1892 | USA | ~ | ~ | ~ |

| Siemens Energy | 1847 | Germany | ~ | ~ | ~ |

| Mitsubishi Heavy Industries | 1884 | Japan | ~ | ~ | ~ |

| Doosan Heavy Industries & Construction | 1962 | South Korea | ~ | ~ | ~ |

| Zamil Industrial | 1998 | Saudi Arabia | ~ | ~ | ~ |

KSA aeroderivative gas turbine Market

Growth Drivers

Oil & Gas Expansion

KSA continues to expand its oil and gas industry, with a focus on increasing oil production capacity. In 2024, the Kingdom is expected to produce 10.5 million barrels per day (bpd) of oil, further solidifying its position as the world’s largest exporter of crude oil. This expansion includes the construction of new refineries, petrochemical plants, and other infrastructure, which require a substantial and reliable power generation capacity. Aeroderivative gas turbines are vital for these high-demand sectors due to their flexibility and reliability, especially in off-grid locations or remote areas. The continuous growth of KSA’s oil and gas industry underpins the demand for power solutions like aeroderivative turbines.

Technological Advancements

Technological advancements in aeroderivative gas turbine efficiency and fuel flexibility have been key drivers of growth. In 2024, companies are introducing turbines capable of integrating hydrogen as a fuel source alongside natural gas, making them suitable for both traditional and renewable power generation setups. Innovations in turbine designs are improving both performance and fuel efficiency, reducing operational costs. KSA’s growing focus on achieving sustainability through energy-efficient technologies supports the adoption of these advancements in turbines, as they offer reduced emissions and better operational flexibility for power generation.

Market Challenges

Maintenance Complexity

The complexity of maintaining aeroderivative gas turbines, including routine maintenance and part replacements, increases operational costs for turbine owners. In Saudi Arabia, turbines require specialized parts and expertise for regular servicing, with costs for scheduled maintenance rising by 10-15% annually. The lack of sufficient local service providers with the required technical expertise in Saudi Arabia adds to these challenges, leading many companies to rely on foreign service providers for turbine maintenance. This reliance on external resources can lead to delays and increased downtime, affecting the efficiency of power generation plants.

Dependence on Foreign Manufacturers

Saudi Arabia remains heavily dependent on international manufacturers for aeroderivative gas turbines, as local manufacturing capacity is limited. Key global players like General Electric and Siemens Energy dominate the turbine supply chain. This dependence on foreign suppliers results in longer lead times for turbine procurement and increases vulnerability to international trade disruptions. Additionally, the country’s limited ability to produce critical turbine components domestically increases the cost of sourcing and servicing turbines. However, ongoing efforts under Vision 2030 to localize production and reduce dependency on imports are expected to alleviate some of these challenges. Source: Saudi Arabian General Investment Authority

Opportunities

Energy Diversification

Saudi Arabia’s emphasis on energy diversification, as outlined in Vision 2030, is an ongoing opportunity for aeroderivative gas turbines. The Kingdom is diversifying its energy mix, planning to source 50% of its energy from renewable sources by 2030, and gas turbines will play a pivotal role in supporting this transition. Gas turbines are ideal for providing reliable backup power when renewable energy sources like solar or wind are not available, thus ensuring grid stability. As the Kingdom moves forward with renewable energy projects, there will be a growing demand for turbines that can work in hybrid systems alongside solar and wind energy.

Local Manufacturing Growth

Saudi Arabia’s push for local manufacturing in line with its Vision 2030 economic goals presents a significant opportunity for the aeroderivative gas turbine market. In 2024, the government is focusing on incentivizing local manufacturing through investment subsidies and tax breaks for companies that set up production facilities within the country. Local manufacturing growth would reduce the reliance on imports, decrease operational costs for turbine operators, and create a more competitive domestic market. By fostering partnerships between local industries and global turbine manufacturers, the Kingdom can establish a strong domestic supply chain for gas turbine production and maintenance. Source: Saudi Arabian General Investment Authority

Future Outlook

Over the next few years, the KSA aeroderivative gas turbine market is expected to show steady growth driven by continuous infrastructure developments, energy efficiency goals, and technological advancements in turbine design. The Kingdom’s increasing focus on sustainability, as outlined in Vision 2030, will likely spur the demand for more efficient, eco-friendly turbines. Technological improvements in hybrid turbine systems and green energy initiatives will further shape the future landscape of the gas turbine market. Moreover, the government’s commitment to diversifying its energy mix with renewable energy sources will increase the reliance on flexible and efficient aeroderivative gas turbines in hybrid energy systems.

Major Players in the KSA Aeroderivative Gas Turbine Market

- General Electric

- Siemens Energy

- Mitsubishi Heavy Industries

- Doosan Heavy Industries & Construction

- Zamil Industrial

- Caterpillar Energy Solutions

- Alstom Power (GE Power)

- Ansaldo Energia

- BHEL (Bharat Heavy Electricals Limited)

- MAN Energy Solutions

- Suzlon Energy

- Turbomachinery Systems

- Solar Turbines

- Rolls-Royce

- Harbin Electric International

Key Target Audience

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (Ministry of Energy, Saudi Arabian General Investment Authority)

- Private Power Generation Companies

- Industrial Manufacturing Firms

- Oil and Gas Companies

- Energy Service Providers

- Desalination Plant Operators

- Engineering & Procurement Contractors

Research Methodology

Step 1: Identification of Key Variables

This phase involves identifying all critical market variables related to turbine technology, applications, and regional influences in KSA. The research combines both primary and secondary data sources to define the key drivers and challenges shaping the aeroderivative gas turbine market.

Step 2: Market Analysis and Construction

This step involves analyzing past market trends, technological developments, and energy consumption patterns in KSA. Data from industry reports, government publications, and energy sector statistics are used to develop a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Expert opinions are gathered through interviews with key stakeholders, including turbine manufacturers, energy consultants, and government officials. This helps validate market hypotheses and provides insights into operational realities.

Step 4: Research Synthesis and Final Output

The final research phase synthesizes all findings from both quantitative and qualitative data sources. The goal is to provide a clear, accurate, and actionable analysis of the KSA aeroderivative gas turbine market, outlining the opportunities, challenges, and future trends.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Consolidated Research Approach, Understanding Market Potential Through In-Depth Industry Interviews, Primary Research Approach, Limitations and Future Conclusions)

- Definition of Aeroderivative Gas

- Market Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers

Increased Energy Demand

Vision 2030 Initiatives

Oil & Gas Expansion

Technological Advancements - Market Challenges

High Initial Capital Investment

Maintenance Complexity

Dependence on Foreign Manufacturer - Opportunities

Energy Diversification

Local Manufacturing Growth - Trends

Adoption of Hybrid Systems

Energy Efficiency Demand - Government Regulation

Local Content Requirement

Environmental Compliance - KSA Aeroderivative Gas Turbine

- SWOT Analysis

- Stakeholder Ecosystem

- Porter’s Five Forces

Competitive rivalry

Supplier power

Buyer power

Threat of new entrants

Threat of substitutes in KSA’s turbine market - Competition Ecosystem

- By Value, 2020-2025

- By Volume, 2020-2025

- By Average Price, 2025

- By Product Type (In Value %)

Heavy-Duty Gas Turbines

Industrial Gas Turbines

Miniaturized Gas Turbines - By Application (In Value %)

Power Generation

Oil & Gas

Desalination Plants

Industrial Manufacturing - By Fuel Type (In Value %)

Natural Gas

Diesel

Hybrid Fuels - By End User (In Value %)

Government and State-owned Entities

Private Sector (Energy Companies)

Industrial & Commercial Users - By Region (In Value %)

Eastern Region

Western Region

Central Region

Southern Region

- Market Share & Competitive Positioning

- Cross Comparison Parameters (Company Overview, Business Strategies, Recent Developments, Strengths, Weaknesses, Organizational Structure, Revenues, Revenues by Turbine Type, Number of Touchpoints, Distribution Channels, Number of Dealers and Distributors, Margins, Production Plant Capacity, Unique Value Offering)

- SWOT Analysis of Major Players

- Detailed Profiles of 15 Major Companies

General Electric

Siemens Energy

Mitsubishi Power

Rolls-Royce Holdings

Ansaldo Energia

Solar Turbines

Kawasaki Heavy Industries

MAN Energy Solutions

Baker Hughes

Bharat Heavy Electricals Limited (BHEL)

Harbin Electric International

Capstone Turbine Corporation

OPRA Turbines

Vericor Power Systems

Capstone Green Energy

- Power Generation Companies

- Oil & Gas

- Desalination Plants

- Industrial Manufacturers

- Government Utilities

- By Value, 2025-2030

- By Volume, 2025-2030

- By Average Price, 2025-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now