Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA agrochemical market is a vital sector in the region, valued at approximately USD ~ billion. The market’s growth is driven by an increasing demand for high-yield agricultural products due to the nation’s growing agricultural needs, supported by government initiatives aimed at boosting food security. The adoption of advanced farming techniques and technologies also contributes to the expanding demand for various agrochemicals, including pesticides, herbicides, and fertilizers. The market is also bolstered by rising investments in agricultural infrastructure, enhancing production capabilities and driving the growth of the agrochemical market.

Saudi Arabia, being one of the largest agricultural markets in the region, dominates the agrochemical industry in the Gulf Cooperation Council (GCC) due to its vast agricultural initiatives and investment in irrigation systems. Key cities like Riyadh and Jeddah are major hubs for agrochemical distribution and usage, supported by government policies that encourage domestic production and reliance on advanced farming methods. The country’s strategic geographic location and favorable weather conditions for certain crops further cement its position as a regional leader in agrochemicals.

Market Segmentation

By Product Type:

The KSA agrochemical market is segmented by product type into pesticides, herbicides, fungicides, fertilizers, and insecticides. Recently, fertilizers have had a dominant market share due to their essential role in increasing crop yields and improving soil quality. This dominance is largely driven by the growing need for food security and the expansion of irrigated agriculture. The government’s support for sustainable farming and soil health initiatives has further boosted the demand for fertilizers, making them a central focus of the market.

By End-User:

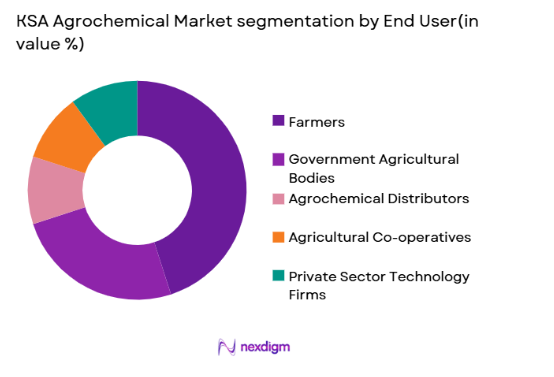

The KSA agrochemical market is segmented by end-user into farmers, government agricultural bodies, agrochemical distributors, agricultural co-operatives, and private sector technology firms. Farmers have a dominant share in the market due to their reliance on agrochemicals for high crop productivity. The government’s ongoing initiatives to improve agricultural yields, especially in arid regions, have further contributed to the farmer segment’s expansion. Additionally, the government’s subsidy programs for agrochemicals play a significant role in enabling farmers to access these products more affordably, reinforcing their dominant position in the market.

Competitive Landscape

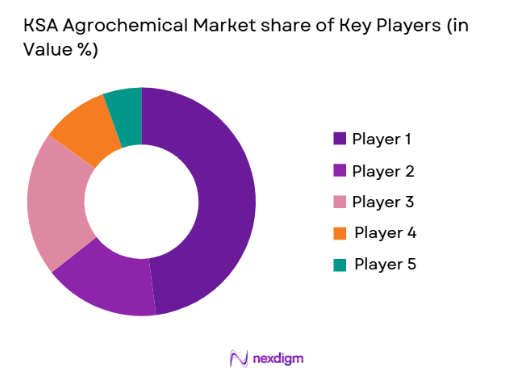

The KSA agrochemical market is highly competitive, characterized by the presence of numerous global and local players. Major multinational companies dominate the market, bringing advanced technologies and innovative products to the region. These companies are involved in strategic mergers and acquisitions, expanding their market footprint and increasing their distribution networks. While global players lead in technological innovation, local companies benefit from government partnerships and a deep understanding of regional agricultural needs. This competitive dynamic fosters a diverse market with intense competition among established and emerging companies.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD billion) | Additional Parameter |

| BASF SE | 1865 | Germany | ~ | ~ | ~ | ~ | ~ |

| Syngenta AG | 2000 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Dow AgroSciences | 1897 | USA | ~ | ~ | ~ | ~ | ~ |

| UPL Limited | 1970 | India | ~ | ~ | ~ | ~ | ~ |

| Adama Agricultural Solutions | 1946 | Israel | ~ | ~ | ~ | ~ | ~ |

KSA Agrochemical Market Analysis

Growth Drivers

Increasing demand for food security:

The growing population and the need for increased agricultural production have driven the demand for agrochemicals in Saudi Arabia. The government’s focus on food security is evident through programs aimed at boosting agricultural productivity, especially in regions with challenging climates. These initiatives include increasing the use of advanced fertilizers and pesticides to improve yields and reduce crop loss due to pests. Additionally, Saudi Arabia’s reliance on imports for much of its food supply has made self-sufficiency a key priority. With such strategic policies in place, agrochemicals have become critical to ensuring food production meets the country’s needs. As a result, there has been a steady increase in the adoption of agrochemicals by farmers and other agricultural stakeholders, fueling market growth.

Government initiatives and subsidies:

Saudi Arabia’s government has consistently supported the agrochemical industry by providing subsidies and incentives for farmers to adopt agrochemicals that enhance crop productivity. The government’s focus on sustainable agriculture and increasing efficiency through advanced technologies has spurred the development and adoption of agrochemical solutions. Subsidies on fertilizers and pesticides make these products more affordable, particularly for small-scale farmers. This support, combined with investments in irrigation infrastructure, has enabled farmers to better manage their crops, improving yields and reducing environmental impact. Consequently, government policies have proven to be a key growth driver for the agrochemical market in the country.

Market Challenges

Environmental impact and sustainability concerns:

One of the significant challenges facing the KSA agrochemical market is the growing environmental impact of chemical-based products. Pesticides and fertilizers, when used excessively, can lead to soil degradation, water pollution, and loss of biodiversity. As the demand for more sustainable agricultural practices increases, there is rising pressure on agrochemical companies to develop eco-friendly products. The need for regulatory compliance regarding the environmental impact of chemicals adds to the challenge for businesses operating in this market. Moreover, local authorities and international bodies are increasingly emphasizing sustainability, urging the industry to invest in environmentally safe alternatives. This shift towards sustainability could disrupt the current market structure and lead to higher costs for agrochemical producers.

Regulatory restrictions and market compliance:

The KSA agrochemical market faces several regulatory challenges as the government introduces stricter standards for the use of agrochemicals. These regulations are intended to reduce the negative environmental effects of agrochemical products and ensure that their use is safe for consumers and the ecosystem. However, the complex regulatory environment can result in delays in product approval and higher compliance costs for manufacturers. The market must continuously adapt to these regulatory changes, which can be a significant barrier for new entrants. Furthermore, non-compliance can lead to fines and the loss of market access, putting pressure on companies to stay up-to-date with the latest regulations and invest in compliance systems.

Opportunities

Expansion in organic farming:

The growing trend toward organic farming presents a significant opportunity for the agrochemical market in Saudi Arabia. Organic farming requires different types of agrochemicals, such as bio-based pesticides and natural fertilizers, to replace traditional chemical products. This shift towards organic farming is being driven by consumer demand for healthier food options and a desire for more sustainable agricultural practices. The government’s support for organic agriculture, alongside the increasing availability of organic agrochemicals, creates a favorable market environment. Companies that can innovate and offer eco-friendly solutions have a clear opportunity to capture the growing share of the organic segment in the Saudi agrochemical market.

Integration of digital technologies in farming:

The increasing adoption of precision agriculture technologies presents a significant opportunity for agrochemical companies in Saudi Arabia. Digital technologies, such as drones, sensors, and data analytics, are being used to optimize crop production and improve the efficiency of agrochemical applications. Precision farming allows for targeted use of fertilizers and pesticides, reducing waste and minimizing environmental impact. Agrochemical companies that integrate these technologies into their product offerings can provide more tailored solutions to farmers, creating a competitive edge. The rise of smart agriculture provides a lucrative opportunity for companies to innovate and expand their presence in the market.

Future Outlook

The future outlook for the KSA agrochemical market is promising, with continued growth expected over the next five years. The market is anticipated to benefit from the government’s ongoing support for agricultural development and food security initiatives. Technological advancements, particularly in digital farming and the development of sustainable agrochemicals, will drive market growth. The increasing demand for organic and eco-friendly products will also play a crucial role in shaping the future of the agrochemical sector. Regulatory policies will likely become more stringent, pushing companies to innovate and adopt greener solutions. With a combination of government policies, technological progress, and evolving consumer preferences, the KSA agrochemical market is poised for steady growth.

Major Players

- BASF SE

- Syngenta AG

- Dow AgroSciences

- UPL Limited

- Adama Agricultural Solutions

- Bayer CropScience

- FMC Corporation

- Nufarm Limited

- Sumitomo Chemical Co.

- Mitsui Chemicals Agro

- ICL Group

- Corteva Agriscience

- Monsanto Company

- Helm AG

- Arysta LifeScience

Key Target Audience

- Government agricultural bodies

- Farmers and agricultural producers

- Agrochemical distributors

- Agribusiness companies

- Agricultural technology firms

- Environmental regulatory agencies

- Agricultural cooperatives

- Private sector agricultural investors

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying the critical market variables, including key trends, consumer behaviors, technological advancements, and regulatory factors that influence the agrochemical market.

Step 2: Market Analysis and Construction

This stage focuses on constructing the market model based on historical data, current trends, and projected growth factors, considering the dynamics and structure of the KSA agrochemical industry.

Step 3: Hypothesis Validation and Expert Consultation

Experts from both local and international agrochemical markets are consulted to validate hypotheses and refine the market construction, ensuring the analysis is accurate and relevant.

Step 4: Research Synthesis and Final Output

After comprehensive research and expert consultation, the data is synthesized to create the final market report, ensuring it aligns with the defined scope and accurately represents the KSA agrochemical market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing demand for high-yield crops

Government subsidies for agricultural innovations

Rise in organic farming practices

Technological advancements in agrochemical formulations

Expanding agricultural export potential - Market Challenges

Environmental impact concerns

Regulatory compliance for chemical use

High cost of advanced agrochemicals

Adoption barriers for sustainable farming practices

Limited access to modern agricultural technologies - Market Opportunities

Expansion in organic agrochemical demand

Government investment in smart agriculture

Growing interest in sustainable pest control solutions - Trends

Rise in precision farming technologies

Adoption of bio-based agrochemicals

Increase in agrochemical usage in arid regions

Shift towards automated application techniques

Advancements in crop protection innovations - Government Regulations & Defense Policy

Regulations on pesticide usage

Support for agrochemical research and development

Environmental compliance and sustainability initiatives - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Pesticides

Fertilizers

Herbicides

Insecticides

Fungicides - By Platform Type (In Value%)

Liquid Agrochemicals

Granular Agrochemicals

Soluble Agrochemicals

Suspended Agrochemicals

Powder Agrochemicals - By Fitment Type (In Value%)

Field Application

Greenhouse Application

Seed Treatment

Fertigation Application

Aerial Application - By EndUser Segment (In Value%)

Farmers

Agrochemical Distributors

Agricultural Co-operatives

Agricultural Product Retailers

Governmental Agricultural Bodies - By Procurement Channel (In Value%)

Direct Procurement

Retailers

E-commerce Platforms

Agrochemical Distributors

Third-party Wholesale - By Material / Technology (in Value%)

Biological Agrochemicals

Chemical-based Agrochemicals

Nano-based Agrochemicals

Organic Agrochemicals

Synthetic Agrochemicals

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Market Share, Product Offering, Pricing, Distribution Channels, Technological Innovation, Customer Reach, Regulatory Compliance, Brand Reputation, Supply Chain Efficiency, Financial Strength)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

BASF SE

Syngenta AG

Dow AgroSciences

Bayer CropScience

Monsanto Company

Adama Agricultural Solutions

UPL Limited

Nufarm Limited

Sumitomo Chemical Co.

FMC Corporation

Kubota Corporation

Mitsui Chemicals Agro

Oerlikon Balzers

Ishihara Sangyo Kaisha Ltd

Hanfeng Evergreen Inc.

- Farmers focusing on high productivity

- Retailers increasing accessibility to agrochemical products

- Government entities ensuring regulatory standards

- Agrochemical distributors expanding service reach

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now