Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Saudi Arabia AI infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by sovereign cloud programs, hyperscale data center deployments, and national artificial intelligence initiatives led by public sector entities and digital transformation mandates. Large scale investments in GPU clusters, advanced cooling systems, and AI optimized networking by telecom operators and government backed digital companies continue to expand compute capacity and enterprise adoption across strategic sectors including energy, finance, and smart city ecosystems.

Riyadh dominates deployment due to concentration of national data authorities, hyperscale facilities, and sovereign cloud programs, while NEOM and Eastern Province emerge as secondary hubs supported by giga project digital infrastructure and energy sector AI demand. Jeddah strengthens regional connectivity through subsea cable landings and edge infrastructure serving logistics and trade applications. These locations benefit from policy driven localization, large energy availability, and proximity to government and industrial demand centers enabling infrastructure scale and investment continuity.

Market Segmentation

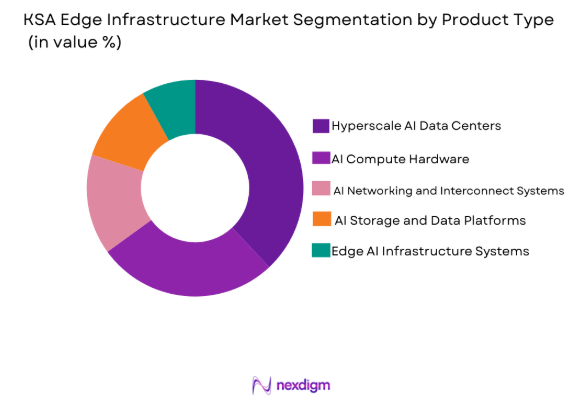

By Product Type

KSA AI Infrastructure market is segmented by product type into AI Edge compute hardware, hyperscale AI data centers, AI networking and interconnect systems, AI storage and data platforms, and edge AI infrastructure systems. Recently, hyperscale AI data centers has a dominant market share due to sovereign cloud mandates, centralized national data platforms, hyperscaler partnerships, and concentration of large scale GPU clusters required for government and giga project artificial intelligence workloads across sectors including energy, finance, and smart cities.

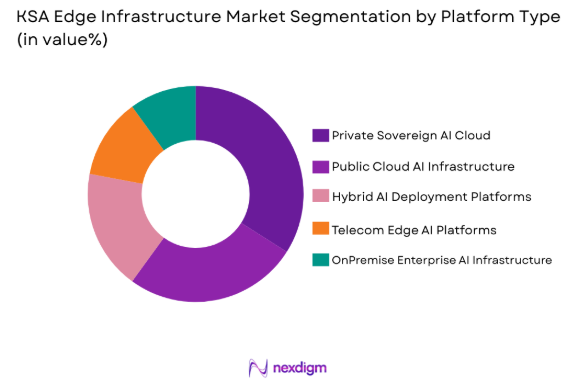

By Platform Type

KSA AI Infrastructure market is segmented by platform type into public cloud AI infrastructure, private sovereign AI cloud, hybrid AI deployment platforms, telecom edge AI platforms, and onpremise enterprise AI infrastructure. Recently, private sovereign AI cloud has a dominant market share due to national data localization regulations, government AI programs, and domestic hosting requirements for critical sector workloads across public agencies, finance, and energy industries.

Competitive Landscape

KSA AI infrastructure market shows moderate concentration driven by sovereign digital entities, telecom operators, and global hyperscale technology providers collaborating on national cloud and compute programs. Government backed companies control large scale infrastructure ownership while international hardware and cloud vendors supply advanced AI accelerators, platforms, and software ecosystems. Strategic partnerships between domestic digital authorities and global hyperscalers shape deployment standards, procurement frameworks, and technology adoption patterns across national artificial intelligence initiatives.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Sovereign AI Capability |

| Saudi Company for Artificial Intelligence | 2021 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| STC Group | 1998 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Aramco Digital | 2023 | Dhahran | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | Redmond | ~ | ~ | ~ | ~ | ~ |

| NVIDIA | 1993 | Santa Clara | ~ | ~ | ~ | ~ | ~ |

KSA AI Infrastructure Market Analysis

Growth Drivers

National Sovereign AI and Data Localization Programs

Saudi Arabia’s sovereign artificial intelligence and data localization initiatives are driving large scale AI infrastructure investments because national policies mandate domestic hosting of critical data, analytics workloads, and government digital platforms across ministries, public agencies, and strategic sectors. These programs require deployment of hyperscale AI data centers, GPU clusters, and sovereign cloud platforms designed to meet national security, privacy, and regulatory compliance requirements, which significantly increases demand for advanced compute, storage, and networking infrastructure across the country. Public sector procurement budgets allocated for national digital transformation and artificial intelligence adoption are enabling continuous expansion of domestic AI infrastructure capacity, particularly in centralized government data centers and sovereign cloud environments. Localization mandates also restrict cross border data transfer for sensitive workloads, forcing enterprises in finance, energy, and healthcare to adopt domestically hosted AI infrastructure solutions rather than offshore cloud services. The government’s strategy to build national artificial intelligence capability across defense, urban planning, public services, and industrial automation further accelerates infrastructure deployment across sovereign facilities. Strategic partnerships between national digital authorities and global hyperscalers provide technology transfer and hardware access while maintaining domestic control of data and compute environments. These policy driven requirements ensure sustained capital investment cycles in AI infrastructure including high density compute clusters, advanced cooling systems, and energy optimized data centers. As sovereign AI capability becomes a national competitiveness priority, infrastructure scale and performance requirements continue expanding across public and strategic private sectors.

Hyperscale Cloud and Giga Project Digital Infrastructure Expansion

Rapid expansion of hyperscale cloud platforms and digital infrastructure within mega urban and industrial projects is accelerating demand for AI infrastructure because giga developments require advanced analytics, automation, digital twin simulation, and real time data processing capabilities embedded across transportation, energy, security, and urban services systems. These large scale developments integrate AI across surveillance, predictive maintenance, mobility optimization, and environmental management, requiring centralized and edge AI infrastructure deployments across project ecosystems. Hyperscale cloud providers are establishing domestic availability zones and AI compute regions to support enterprise migration and public sector cloud adoption, which increases investment in GPU clusters, high bandwidth networking, and AI optimized storage architectures. Telecom operators deploying 5G and edge computing platforms across smart cities and industrial zones also require localized AI processing infrastructure to enable low latency analytics and automation services. Giga project operators procure dedicated AI infrastructure for simulation, robotics control, and real time analytics across construction, logistics, and urban management phases, creating sustained infrastructure demand cycles. Integration of AI platforms across energy grids, water systems, and transportation networks within mega developments requires scalable compute environments capable of processing large sensor and operational datasets. These infrastructure deployments extend beyond project boundaries to serve surrounding economic zones and digital services ecosystems, further expanding national AI capacity. Continuous digital expansion within these developments ensures long term demand for AI infrastructure upgrades and capacity scaling.

Market Challenges

Dependence on Imported Advanced AI Hardware and Semiconductor Supply Chains

Saudi Arabia’s AI infrastructure development faces structural constraints due to reliance on imported advanced semiconductor technologies, GPUs, high speed interconnect components, and specialized data center hardware, which exposes national deployment timelines and costs to global supply chain disruptions and export control restrictions. Advanced AI accelerators and networking technologies are produced by a limited number of global manufacturers, creating procurement bottlenecks and price volatility that directly affect domestic infrastructure project budgets and schedules. Export regulations and geopolitical technology controls can limit access to high performance AI chips and associated software stacks required for hyperscale compute clusters, constraining national AI capability scaling. Domestic absence of semiconductor fabrication and advanced packaging ecosystems prevents local production of critical AI hardware components, reinforcing import dependency. Supply chain delays in cooling systems, photonic interconnects, and high density power equipment further complicate large scale AI data center construction and deployment. Fluctuations in global semiconductor demand driven by hyperscale cloud and artificial intelligence growth worldwide intensify competition for hardware allocation, impacting national procurement timelines. Infrastructure operators must maintain higher capital buffers and long procurement lead times to secure hardware availability, reducing deployment flexibility. These constraints collectively slow domestic AI infrastructure expansion and increase cost per compute unit relative to markets with local semiconductor ecosystems.

Power Density, Cooling, and Energy Infrastructure Constraints in High Performance AI Data Centers

High performance AI workloads require extremely dense compute clusters that generate significant thermal loads and power consumption, creating engineering and operational challenges in designing and scaling AI data centers within regional climate conditions and energy distribution frameworks. GPU dense servers consume substantially higher power per rack than traditional data center equipment, necessitating specialized electrical distribution, high capacity substations, and redundant energy supply systems for stable operation. Cooling requirements for such environments exceed conventional air cooling capabilities, requiring adoption of liquid cooling or immersion systems that increase capital expenditure and operational complexity. Desert climate conditions and ambient temperatures in major deployment regions increase cooling load and water management requirements for thermal control systems. Energy availability and grid connection capacity must scale proportionally with AI data center growth, requiring coordination with national utilities and infrastructure providers. Integration of renewable energy sources into data center power supply introduces variability management challenges that require advanced energy storage and distribution technologies. High density facilities also demand advanced fire safety, structural design, and environmental control engineering, increasing construction timelines and costs. These technical and energy constraints collectively complicate rapid expansion of hyperscale AI infrastructure across the Kingdom.

Opportunities

Development of Regional Sovereign AI Cloud Hub Serving Middle East and North Africa

Saudi Arabia has opportunity to position itself as a regional sovereign artificial intelligence cloud hub because its national data localization policies, sovereign infrastructure investments, and hyperscale deployments create trusted domestic hosting environments capable of serving neighboring countries with similar regulatory and data sovereignty requirements. Many regional governments and enterprises require AI processing environments compliant with domestic or regional data residency frameworks, which can be supported through Saudi based sovereign cloud platforms and AI compute infrastructure. The Kingdom’s investments in subsea connectivity, terrestrial fiber networks, and international digital corridors enhance cross border data flow capability and latency performance, supporting regional service delivery. Hyperscale AI facilities located within national territory can provide compute resources to regional clients lacking domestic infrastructure scale, expanding utilization rates and revenue streams. Strategic alignment with regional digital economy initiatives and cross border technology cooperation agreements can further strengthen hub positioning. Availability of large scale energy resources supports competitive operating costs for compute intensive workloads relative to smaller regional markets. Government backed digital companies can export sovereign cloud and AI infrastructure services to neighboring economies seeking trusted hosting environments. This regionalization strategy can diversify infrastructure demand beyond domestic consumption and increase economic return on national AI investments.

Localization of AI Hardware Integration, Assembly, and Data Center Manufacturing Ecosystems

Establishing domestic capability in AI hardware integration, data center module manufacturing, and advanced cooling system assembly presents opportunity to reduce import dependence and build a localized AI infrastructure supply chain ecosystem. While advanced semiconductor fabrication may remain external, significant value exists in assembling AI servers, integrating GPU clusters, producing racks and enclosures, and manufacturing cooling and power distribution systems domestically. Localization programs can encourage global hardware vendors to establish assembly and integration facilities within the Kingdom to serve national and regional markets. Domestic manufacturing of modular data center units and prefabricated AI infrastructure components can reduce construction time and logistics cost for deployments. Development of specialized workforce skills in AI hardware engineering, thermal management, and data center operations supports ecosystem sustainability. Government incentives and industrial zones dedicated to digital infrastructure manufacturing can attract investment from global technology suppliers. Localization also enhances supply chain resilience and maintenance capability for critical infrastructure. Over time, domestic integration capability can support export of AI infrastructure modules to regional markets, strengthening industrial diversification objectives. These ecosystem developments align with national economic transformation strategies while accelerating AI infrastructure deployment capacity.

Future Outlook

The KSA AI infrastructure market is expected to expand rapidly over the next five years driven by sovereign AI programs, hyperscale cloud expansion, and giga project digitalization. Deployment of high density GPU clusters and advanced cooling technologies will accelerate hyperscale facility construction. Government localization policies and regional cloud hub ambitions will sustain investment cycles. Telecom edge AI and industrial automation adoption will broaden infrastructure demand across sectors.

Major Players

- Saudi Company for Artificial Intelligence

- STC Group

- Aramco Digital

- Mobily

- Zain Saudi Arabia

- Elm Company

- SITE Saudi Information Technology Company

- Advanced Electronics Company

- NEOM Tech and Digital Company

- King Abdulaziz City for Science and Technology

- NVIDIA • Microsoft

- Google Cloud

- Amazon Web Services

- Oracle

Key Target Audience

- Government and regulatory bodies

- Investments and venture capitalist firms

- Telecom operators

- Energy and industrial enterprises

- Cloud service providers

- Data center developers

- Defense and security agencies

- Financial institutions

Research Methodology

Step 1: Identification of Key Variables

Core variables such as AI compute capacity, data center deployments, sovereign cloud investments, and end user adoption across sectors were identified through secondary data sources and policy analysis. Supply chain factors, technology trends, and procurement frameworks were mapped to define market boundaries.

Step 2: Market Analysis and Construction

Market sizing was constructed using infrastructure investment data, hyperscale deployment metrics, hardware procurement trends, and sector level AI adoption indicators. Segmentation frameworks were built across system types and end users to reflect infrastructure demand distribution.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding deployment scale, technology adoption, and demand drivers were validated through expert interviews with infrastructure engineers, cloud architects, and regional digital ecosystem specialists. Cross verification ensured consistency with national digital strategy direction.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative findings were synthesized into market estimates, segmentation shares, and strategic insights. Final outputs were reviewed for logical consistency, policy alignment, and infrastructure deployment realism before publication.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National AI strategy and sovereign compute investments

Rapid hyperscale cloud expansion in the Kingdom

Energy sector digitalization and AI adoption

Smart city and giga project AI requirements

Public sector data localization mandates - Market Challenges

High capital intensity of AI data center builds

Limited domestic semiconductor ecosystem

Power density and cooling infrastructure constraints

Specialized AI talent and operational skills gaps

Dependence on imported advanced hardware - Market Opportunities

Localization of AI hardware assembly and integration

AI infrastructure for industrial automation and robotics

Regional AI cloud hub serving Middle East markets

- Trends

Shift toward GPU dense high performance clusters

Adoption of liquid and immersion cooling systems

Emergence of sovereign AI cloud platforms

Integration of AI with 5G and edge networks

Growth of modular prefabricated AI data centers

- Government Regulations & Defense Policy

Data sovereignty and localization compliance frameworks

National supercomputing and AI research funding programs

Cybersecurity and critical infrastructure standards

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Compute Servers and Accelerated Hardware

Hyperscale AI Data Centers

Edge AI Infrastructure Systems

AI Networking and Interconnect Systems

AI Storage and Data Management Systems - By Platform Type (In Value%)

Cloud AI Infrastructure Platforms

OnPremise Enterprise AI Infrastructure

Hybrid AI Deployment Platforms

Telecom Edge AI Platforms

Government Sovereign AI Platforms - By Fitment Type (In Value%)

Greenfield AI Data Center Deployments

Brownfield Data Center AI Retrofits

Modular Prefabricated AI Infrastructure

Containerized Edge AI Units

Integrated AI Supercomputing Facilities - By End User Segment (In Value%)

Government and Public Sector Entities

Telecom and Digital Service Providers

Energy and Industrial Enterprises

Financial Services Institutions

Healthcare and Life Sciences Organizations

- By Procurement Channel (In Value%)

Direct Government Procurement Programs

Hyperscaler Strategic Partnerships

System Integrator and EPC Contracts

Technology Vendor Direct Sales

Public/Private Partnership Models - By Material / Technology (in Value %)

GPU and AI Accelerator Chipsets

HighPerformance Cooling Technologies

Silicon Photonics Interconnects

Advanced Semiconductor Packaging

AIOptimized Power and Energy Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Compute Performance Density, Energy Efficiency, Cooling Technology, Deployment Scalability, Data Sovereignty Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Saudi Company for Artificial Intelligence

Aramco Digital

STC Group

Mobily

Zain Saudi Arabia

Elm Company

SITE Saudi Information Technology Company

Advanced Electronics Company

Saudi Data and Artificial Intelligence Authority

King Abdulaziz City for Science and Technology

NEOM Tech and Digital Company

NVIDIA

Microsoft

Google Cloud

Amazon Web Services

- Government entities drive sovereign compute demand and national AI capability building

- Telecom operators deploy edge AI infrastructure to support 5G and smart services

- Energy and industrial firms invest in AI for automation and predictive operations

- Financial and healthcare sectors adopt AI infrastructure for analytics and secure data processing

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now