Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, Saudi Arabia’s AI servers and GPU hardware market reached approximately USD ~ billion, driven by hyperscale data center investments, sovereign AI cloud programs, and enterprise adoption of accelerated computing across energy, finance, and public sector domains. National digital infrastructure initiatives and localization mandates are stimulating procurement of GPU-dense servers and high-performance AI clusters, while regional cloud providers and telecom operators expand AI-ready compute capacity to support generative AI, analytics, and automation workloads across industries.

Riyadh dominates the KSA AI servers and GPU hardware market due to concentration of sovereign data centers, government AI programs, and hyperscale cloud regions aligned with national digital strategies. Neom and Eastern Province are emerging hubs as large-scale smart city and industrial digitalization projects require AI compute infrastructure for energy optimization, robotics, and predictive analytics. Strategic placement near subsea connectivity, power infrastructure, and technology parks enables these locations to attract hyperscale and enterprise AI server deployments across the Kingdom.

Market Segmentation

By Product Type

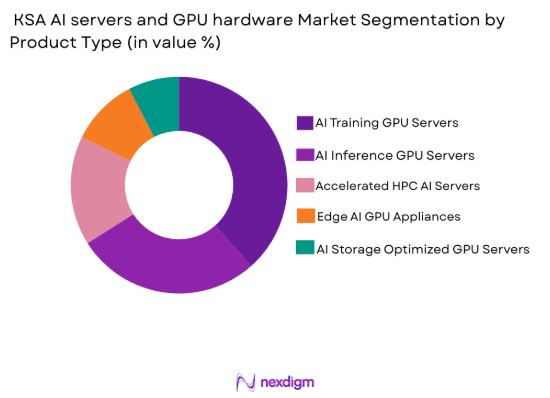

KSA AI servers and GPU hardware market is segmented by product type into AI training GPU servers, AI inference GPU servers, accelerated HPC AI servers, edge AI GPU appliances, and AI storage optimized GPU servers. Recently, AI training GPU servers has a dominant market share due to factors such as hyperscale model development demand, sovereign AI initiatives, and concentration of large GPU clusters within national data centers. Training workloads require multi-GPU nodes, high-bandwidth interconnects, and liquid-cooled racks, significantly increasing hardware intensity compared to inference or edge deployments. Government AI programs and cloud providers prioritize training capacity to build national language models, industrial digital twins, and defense analytics platforms, reinforcing procurement of high-performance GPU training systems across centralized facilities.

By Platform Type

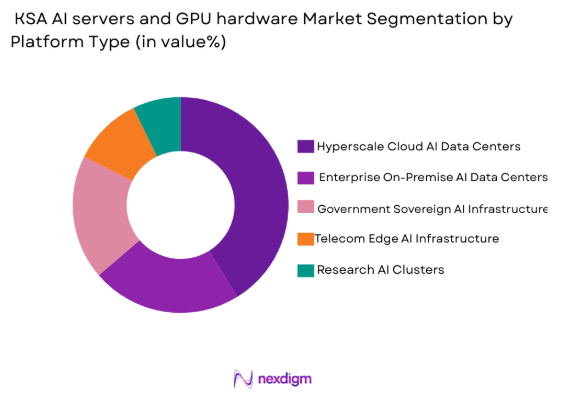

KSA AI servers and GPU hardware market is segmented by platform type into hyperscale cloud AI data centers, enterprise on-premise AI data centers, government sovereign AI infrastructure, telecom edge AI infrastructure, and research AI clusters. Recently, hyperscale cloud AI data centers has a dominant market share due to factors such as cloud region expansion, multi-tenant AI services, and concentration of GPU superclusters in centralized hyperscale facilities. Cloud providers deploy large GPU fleets to deliver AI training, inference, and platform services to enterprises and public agencies, achieving higher utilization and economies of scale. Localization policies and regional service demand further encourage hyperscale GPU deployments within national data center campuses.

Competitive Landscape

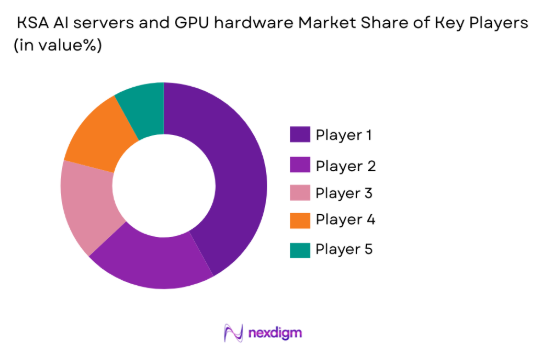

The KSA AI servers and GPU hardware market shows moderate consolidation, with global GPU and server vendors partnering with regional integrators and sovereign cloud initiatives to secure large national deployments. Hyperscale infrastructure contracts and government AI programs strongly influence vendor positioning, favoring suppliers with advanced GPU architectures, liquid-cooled server designs, and local deployment capability. Competition centers on performance density, energy efficiency, AI software ecosystems, and ability to support sovereign data center localization strategies across Saudi Arabia.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Local Integration Capability |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| Advanced Micro Devices | 1969 | USA | ~ | ~ | ~ | ~ | ~ |

| Intel | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 2015 | USA | ~ | ~ | ~ | ~ | ~ |

KSA AI Servers and GPU Hardware Market Analysis

Growth Drivers

National Sovereign AI Infrastructure and Hyperscale Data Center Expansion

Saudi Arabia’s strategy to establish sovereign artificial intelligence capabilities and regional hyperscale cloud leadership is creating sustained structural demand for AI servers and GPU hardware across centralized data center campuses and national computing facilities. Government backed AI initiatives and digital transformation programs are funding large scale GPU clusters to support language models, defense analytics, smart city platforms, and industrial optimization systems across priority sectors. Hyperscale cloud providers are simultaneously deploying GPU dense infrastructure to offer AI services regionally, positioning the Kingdom as a Middle East compute hub serving domestic and cross border workloads. Sovereign data localization mandates further require AI compute resources to be hosted within national territory, accelerating procurement of onshore GPU superclusters and high performance AI servers by public agencies and regulated industries. Large national projects such as smart city developments, energy digitalization platforms, and autonomous mobility ecosystems require centralized AI training capacity, reinforcing adoption of multi GPU server racks and exascale computing systems. Expansion of subsea connectivity, renewable power availability, and large scale data center zones enables hyperscale operators to deploy GPU fleets at scale with improved cost efficiency and latency performance. Local partnerships between global hardware vendors and regional system integrators are improving deployment capability and lifecycle support for complex AI infrastructure within Saudi Arabia. Rising enterprise demand for generative AI, predictive analytics, and automation platforms across finance, healthcare, logistics, and government services further increases utilization of GPU based servers hosted in sovereign and cloud environments. These combined public and private sector investments create a durable growth foundation for the national AI server hardware ecosystem, reinforcing long term market expansion.

Enterprise and Industrial Adoption of Accelerated AI Computing Across Key Sectors

Rapid adoption of artificial intelligence applications across Saudi Arabia’s energy, manufacturing, finance, telecommunications, and public administration sectors is significantly increasing demand for GPU accelerated servers and high performance AI computing infrastructure within enterprise and hybrid environments. Energy companies are deploying AI HPC clusters for seismic imaging, reservoir modeling, predictive maintenance, and grid optimization, requiring dense GPU nodes with high bandwidth memory and interconnect technologies. Industrial and manufacturing enterprises are implementing digital twins, robotics optimization, computer vision quality systems, and autonomous operations platforms that rely on centralized AI training and inference servers integrated with operational technology networks. Financial institutions and government agencies are expanding use of generative AI, fraud detection, cybersecurity analytics, and citizen service automation, necessitating secure sovereign AI compute capacity and on premise GPU clusters. Telecom operators are embedding AI inference platforms across 5G networks for traffic optimization, edge analytics, and service automation, driving distributed GPU hardware deployment across network infrastructure sites. Growing enterprise AI maturity and data availability are increasing complexity of models and workloads, shifting organizations from CPU based analytics toward GPU accelerated compute environments for performance and scalability. Adoption of hybrid cloud architectures is enabling enterprises to combine hyperscale GPU capacity with on premise AI servers for sensitive workloads, increasing total hardware demand. National digital transformation programs and sector specific AI mandates are incentivizing enterprises to invest in accelerated computing infrastructure to remain competitive and compliant. Workforce upskilling initiatives and AI ecosystem development are further supporting enterprise AI adoption and associated GPU server procurement across industries. These cross sector deployment patterns are expanding the addressable market for AI servers and GPU hardware beyond hyperscale environments into widespread enterprise and industrial infrastructure.

Market Challenges

High Power Density, Cooling Requirements, and Data Center Infrastructure Constraints

AI servers and GPU hardware deployments in Saudi Arabia face significant infrastructure challenges due to extreme power density, thermal management demands, and environmental conditions associated with large scale accelerated computing systems. Modern GPU clusters consume substantially higher electricity per rack compared to conventional servers, requiring advanced power distribution units, redundant supply architecture, and high capacity substations within data center facilities. Desert climate conditions increase cooling loads and reduce efficiency of traditional air cooled systems, necessitating adoption of liquid cooling, immersion technologies, and specialized thermal management infrastructure that increases capital and operational complexity. Many existing enterprise and telecom data centers lack sufficient power and cooling capacity to host high density GPU racks, requiring costly retrofits or migration to new purpose built AI data center campuses. Energy availability and sustainability considerations also affect GPU infrastructure expansion, as hyperscale and sovereign AI facilities seek renewable energy integration and grid reliability to support continuous high load operation. Construction timelines for new high capacity data centers can delay AI hardware deployment cycles, constraining near term market growth despite strong demand. Integration of advanced cooling systems requires specialized engineering expertise and maintenance capabilities that remain limited in the regional workforce. Supply chain dependencies for cooling fluids, heat exchangers, and high power electrical components further complicate deployment logistics. These infrastructure constraints raise total cost of ownership for AI servers and GPU hardware and may slow adoption among enterprises lacking hyperscale level facilities. Addressing power and cooling challenges remains a critical barrier influencing the pace and scale of GPU infrastructure rollout across the Kingdom.

Dependence on Imported Semiconductors and Geopolitical Export Controls

The KSA AI servers and GPU hardware market is structurally dependent on imported advanced semiconductors and accelerator technologies, exposing supply continuity and procurement cycles to global geopolitical dynamics and export control regimes affecting high performance computing hardware. Leading edge AI GPUs and accelerators are manufactured by a limited number of international vendors subject to export restrictions and licensing requirements, which can affect availability timelines, configuration options, and performance tiers accessible to regional buyers. Global demand for AI chips has created supply shortages and extended lead times, complicating planning for large sovereign and hyperscale deployments within Saudi Arabia. Restrictions on advanced node semiconductor technologies may limit access to top tier GPU architectures required for frontier model training and exascale AI computing initiatives. Reliance on foreign manufacturing ecosystems also constrains localization of the AI hardware value chain within the Kingdom, reducing strategic autonomy in critical digital infrastructure components. Currency fluctuations and import logistics add cost variability and procurement risk for enterprises and government agencies acquiring GPU servers. Limited domestic fabrication or advanced packaging capability means the national AI hardware ecosystem cannot independently scale production to meet demand. Vendor concentration further reduces bargaining leverage and diversification options for buyers. These geopolitical and supply chain dependencies create uncertainty in long term AI infrastructure planning and represent a structural challenge for sustained GPU hardware market development in Saudi Arabia.

Opportunities

Localization of Sovereign AI Cloud and National Compute Infrastructure

Saudi Arabia’s ambition to build sovereign artificial intelligence capabilities and regionally competitive cloud infrastructure presents a major opportunity for domestic deployment of AI servers and GPU hardware across national data center ecosystems and government computing platforms. Public investment in sovereign cloud environments is enabling establishment of large GPU superclusters dedicated to national language models, defense analytics, smart city platforms, and public sector AI services hosted within national jurisdiction. Localization policies requiring sensitive data and AI workloads to remain onshore further drive procurement of domestic GPU infrastructure by regulated industries and public agencies. Development of large scale data center zones with renewable energy integration and high capacity connectivity is creating favorable conditions for hyperscale GPU deployments within the Kingdom. Partnerships between global hardware vendors and local integrators are supporting technology transfer, workforce development, and lifecycle support capabilities necessary for sustaining national AI infrastructure. Sovereign AI cloud platforms can also serve regional markets across the Middle East and North Africa, expanding utilization of installed GPU capacity beyond domestic demand. Establishment of national supercomputing centers and research AI facilities strengthens innovation ecosystems and demand for advanced GPU hardware. Government funding mechanisms and procurement frameworks provide long term revenue visibility for suppliers participating in localization programs. These structural initiatives position the Kingdom as a regional AI compute hub and create sustained growth opportunities for AI server and GPU hardware deployment within sovereign infrastructure projects.

Expansion of AI Compute for Energy, Industrial, and Smart City Digitalization

Large scale digital transformation across Saudi Arabia’s energy sector, industrial base, and smart city developments offers substantial opportunity for distributed and centralized AI computing infrastructure deployment utilizing GPU accelerated servers and specialized AI hardware platforms. Energy enterprises are scaling AI driven exploration, production optimization, grid management, and carbon management systems requiring high performance computing clusters with GPU acceleration. Industrial digitalization programs across manufacturing, mining, and logistics are adopting AI robotics, predictive maintenance, computer vision inspection, and autonomous operations that depend on AI training and inference infrastructure. Smart city initiatives incorporating intelligent mobility, surveillance analytics, urban digital twins, and citizen services generate continuous demand for centralized GPU training clusters and edge inference servers. Integration of AI into national infrastructure systems such as transportation networks, utilities, and public safety platforms further expands the addressable GPU hardware market. These sectoral deployments require both hyperscale training environments and localized enterprise AI servers integrated with operational technology environments. Growth of industrial data generation and IoT connectivity increases model complexity and compute intensity, reinforcing GPU adoption. Government incentives and sector specific AI programs are encouraging enterprises to invest in accelerated computing capacity. Localization of AI solutions within national projects ensures sustained domestic hardware demand. This convergence of industrial, energy, and urban AI applications represents a long term structural opportunity for AI server and GPU hardware expansion across Saudi Arabia.

Future Outlook

Saudi Arabia’s AI servers and GPU hardware market is expected to expand steadily as sovereign AI cloud infrastructure, hyperscale data centers, and enterprise accelerated computing adoption scale across the Kingdom. Continued investment in national AI initiatives, smart city platforms, and industrial digitalization will drive deployment of high-density GPU clusters and edge AI servers. Advances in liquid cooling, high-bandwidth interconnects, and AI accelerator architectures will improve efficiency and performance. Localization policies and regional cloud positioning are likely to sustain long-term demand growth.

Key Players

- NVIDIA

- Advanced Micro Devices

- Intel • Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- Supermicro

- Cisco Systems

- Huawei

- Inspur

- Fujitsu

- Atos

- GIGABYTE Technology

- Wiwynn

- Tyan

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hyperscale cloud providers

- Telecom operators

- Energy and utilities companies

- Large enterprises

- Defense and security agencies

- Data center developers

Research Methodology

Step 1: Identification of Key Variables

Key variables such as AI server shipments, GPU architecture deployment, hyperscale data center capacity, and sovereign AI investment programs were identified. Demand drivers across government, enterprise, and telecom sectors were mapped. Technology adoption indicators and infrastructure constraints were incorporated to define market boundaries and segmentation logic.

Step 2: Market Analysis and Construction

Market size was constructed using procurement data from hyperscale deployments, sovereign AI programs, and enterprise infrastructure investments. Hardware configuration trends and average GPU server pricing were analyzed. Platform-level deployment patterns across cloud, government, and industrial sectors were synthesized to derive segmentation shares.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding AI infrastructure rollout, GPU cluster scale, and enterprise adoption were validated through industry expert interviews and vendor ecosystem insights. Regional data center operators and system integrators provided deployment benchmarks. Technology roadmaps and policy frameworks were cross-checked against market projections.

Step 4: Research Synthesis and Final Output

All data points were triangulated across supply, demand, and policy indicators to produce final market estimates and segmentation. Competitive positioning and technology trends were analyzed to interpret market structure. Findings were synthesized into a structured analytical framework to support strategic decision-making.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National AI and data center localization programs increasing sovereign compute demand

Rapid hyperscale cloud region expansion requiring GPU dense server deployments

Adoption of generative AI across energy finance and government sectors

Telecom edge AI rollouts linked to 5G and smart city infrastructure

Growth of research supercomputing and AI model development clusters - Market Challenges

High capital cost and power density requirements of GPU infrastructure

Dependence on imported semiconductors and export controls

Data center energy and cooling constraints in desert climates

Shortage of advanced AI hardware engineering expertise

Integration complexity across heterogeneous AI compute stacks - Market Opportunities

Localization of sovereign AI cloud and government GPU clusters

AI compute infrastructure for energy and industrial digitalization

Regional AI hub positioning serving Middle East workloads - Trends

Shift toward GPU superclusters and exascale AI training systems

Adoption of liquid cooling and high density AI racks

Emergence of sovereign AI cloud platforms

Integration of AI accelerators into telecom edge nodes

Co design of AI hardware with hyperscale workloads - Government Regulations & Defense Policy

National data sovereignty and AI localization mandates

Public investment programs for AI and supercomputing centers

Cybersecurity and critical infrastructure compliance standards

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Training GPU Servers

AI Inference GPU Servers

Accelerated HPC AI Servers

Edge AI GPU Appliances

AI Storage Optimized GPU Servers - By Platform Type (In Value%)

Hyperscale Cloud AI Data Centers

Enterprise AI On Premise Data Centers

Government and Sovereign AI Infrastructure

Telecom Edge AI Infrastructure

Research and Academic AI Clusters - By Fitment Type (In Value%)

Rack Scale Integrated AI Systems

Blade Based GPU Server Nodes

Hyperconverged AI Infrastructure

Modular AI Server Pods

Appliance Based AI Systems - By End User Segment (In Value%)

Cloud Service Providers

Government and Public Sector

Telecommunications Operators

Large Enterprises and Conglomerates

Research and Academic Institutions - By Procurement Channel (In Value%)

Direct OEM Procurement

System Integrator and EPC Contracts

Government Tenders and Frameworks

Cloud Infrastructure Partnerships

Distributor and Value Added Reseller - By Material / Technology (in Value %)

NVIDIA CUDA GPU Architectures

AMD CDNA GPU Architectures

Custom AI Accelerators and ASICs

High Bandwidth Memory and Interconnects

Liquid Cooling and Immersion Cooling Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (GPU architecture, Compute density, Interconnect bandwidth, Cooling technology, System scalability, Power efficiency, AI software ecosystem, Deployment model, Local integration capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

Advanced Micro Devices

Intel

Supermicro

Dell Technologies

Hewlett Packard Enterprise

Lenovo

Cisco Systems

Atos

Fujitsu

Huawei

Inspur

GIGABYTE Technology

Wiwynn

Tyan

- Government demand anchored in sovereign AI cloud and national data initiatives

- Energy and industrial enterprises deploying AI HPC for optimization and exploration

- Telecom operators embedding AI inference at network edge sites

- Academic and research institutions expanding AI supercomputing clusters

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now