Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA Blind Spot Detection Systems market is valued at approximately USD ~ million in 2024. This market is driven by the increasing focus on automotive safety systems, particularly as government regulations become stricter regarding vehicle safety features. The adoption of Advanced Driver Assistance Systems (ADAS) in vehicles, supported by consumer demand for enhanced safety and vehicle automation, is also accelerating market growth. Moreover, the growing automotive sector in Saudi Arabia, coupled with a rise in awareness of road safety, is pushing the demand for such technologies.

Source: Saudi Arabian General Investment Authority.

The KSA market for blind spot detection systems is primarily dominated by major cities such as Riyadh, Jeddah, and Dammam, due to their central roles in the automotive industry and urban development. Riyadh, as the capital, sees significant demand from both high-end and mid-range vehicle segments. Additionally, Saudi Arabia’s large road networks and a rising number of private and commercial vehicles are key drivers in cities like Jeddah, where traffic accidents are a significant concern. These cities are central to the increasing adoption of safety systems, including blind spot detection.

Market Segmentation

By Technology

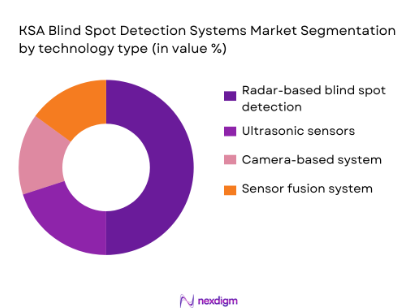

The KSA Blind Spot Detection Systems market is segmented by technology into radar-based systems, ultrasonic sensors, camera-based systems, and sensor fusion systems. Radar-based systems dominate the market due to their high reliability and performance under various driving conditions. Radar systems offer longer-range detection and better functionality in adverse weather conditions, which are critical in Saudi Arabia’s hot and sandy climate. This technology has also been adopted by OEMs as part of their safety feature packages, contributing to its dominance.

By Application

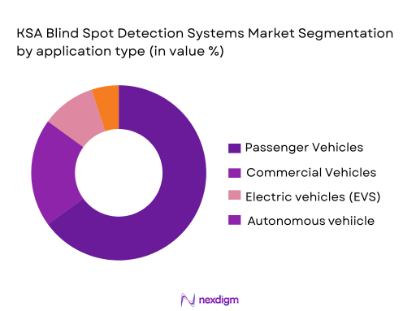

The market is segmented by application into passenger vehicles, commercial vehicles, and electric vehicles (EVs). Passenger vehicles represent the largest segment, driven by the increasing adoption of ADAS and consumer demand for enhanced vehicle safety. As more consumers opt for vehicles equipped with advanced driver assistance systems, passenger vehicles are the primary market for blind spot detection. This segment benefits from regulatory mandates and OEM initiatives aimed at improving the safety features of mass-market cars, which are increasingly including these systems in base models.

Competitive Landscape

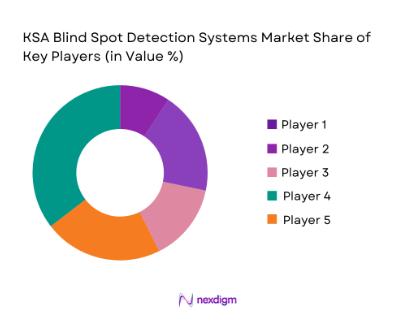

The KSA Blind Spot Detection Systems market is highly competitive, with both global players and regional companies vying for market share. The market is dominated by key global suppliers like Bosch, Continental AG, and Denso Corporation, who lead in terms of technological innovations and supply chain capabilities. Additionally, regional players such as Saudi-based automotive component manufacturers are rapidly gaining ground by offering localized solutions tailored to the unique driving conditions in Saudi Arabia. These companies benefit from strong partnerships with local OEMs and the government’s push toward increasing road safety.

| Company Name | Establishment Year | Headquarters | Technology Offered | Key Markets | Production Capacity |

| Bosch | 1886 | Germany | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ |

| Denso Corporation | 1949 | Japan | ~ | ~ | ~ |

| ZF Friedrichshafen | 1915 | Germany | ~ | ~ | ~ |

| Autoliv | 1953 | Sweden | ~ | ~ | ~ |

KSA Blind Spot Detection Systems Market Analysis

Growth Drivers

Rising Consumer Demand for Vehicle Safety Features

Consumer demand for advanced vehicle safety features, including blind spot detection, has been steadily increasing in Saudi Arabia. The country reported over 9,000 traffic fatalities in 2023, according to the Saudi Arabian Ministry of Health, which has led to a growing demand for safety technologies like ADAS (Advanced Driver Assistance Systems). As safety becomes a priority, more consumers seek vehicles equipped with innovative safety features. The government’s focus on reducing traffic accidents has also encouraged this trend

Technological Advancements in ADAS and Sensor Technologies

Technological advancements in ADAS and sensor technologies have significantly contributed to the growth of blind spot detection systems. For instance, radar and camera-based systems offer improved detection capabilities. The International Energy Agency (IEA) highlighted the shift towards more advanced sensor technologies in 2023, with increasing integration of radar and ultrasonic sensors for accurate detection, especially in low-visibility conditions. These advancements are enhancing system reliability, making them a key factor in the growing adoption of blind spot detection systems.

Market Challenges

High Initial Costs of Advanced Sensor Technologies

The high upfront cost of advanced sensor technologies remains a significant barrier for the widespread adoption of blind spot detection systems in Saudi Arabia. According to the World Bank, the cost of implementing ADAS features, including blind spot detection, in vehicles can increase the price of a vehicle by 15-20%. This price increase is particularly challenging for the mass-market vehicle segment, where affordability is crucial for consumers. The high cost limits the technology’s accessibility, especially in non-luxury vehicle segments.

Integration Challenges with Existing Vehicle Systems

Integrating blind spot detection systems with existing vehicle platforms poses significant challenges. Vehicles, particularly older models, are not designed to accommodate advanced technologies like radar, cameras, and ultrasonic sensors. The cost and time required for retrofitting these systems into older vehicle models are considerable. The Saudi Arabian automotive market, with a significant number of older vehicles still in operation, faces integration issues, delaying the adoption of these systems across all vehicle segments.

Opportunities

Growth in Autonomous Vehicle Deployment

The deployment of autonomous vehicles in Saudi Arabia offers significant opportunities for the blind spot detection systems market. With the government’s investment in smart cities and autonomous transportation technologies, Saudi Arabia is positioned to become a leader in autonomous vehicle adoption in the Middle East. These vehicles require advanced safety systems like blind spot detection for navigation in urban and highway environments. As autonomous vehicle deployment accelerates, so too will the need for such technologies.

Expansion of Blind Spot Detection Systems in Mid-Range Vehicles

While blind spot detection systems were initially confined to premium vehicles, their expansion into mid-range vehicles presents a key growth opportunity. According to the Saudi Arabian Motor Federation, there has been a marked increase in the integration of ADAS in mid-range vehicles as consumer demand for safety features rises. As automakers seek to differentiate their models, mid-range vehicles are becoming a significant segment for blind spot detection systems adoption. This trend is expected to continue, driven by growing safety awareness.

Future Outlook

Over the next 5 years, the KSA Blind Spot Detection Systems market is expected to show significant growth, driven by continued advancements in automotive safety technology, increased vehicle sales, and the government’s emphasis on road safety standards. Additionally, the rising adoption of autonomous vehicles and electric vehicles (EVs) will contribute to the market’s expansion, as these vehicles require advanced safety systems like blind spot detection for autonomous operation. As more vehicles on the road are equipped with ADAS, the demand for such systems will continue to increase.

Major Players in the Market

- Bosch

- Continental AG

- Denso Corporation

- ZF Friedrichshafen

- Autoliv

- Valeo

- Magna International

- Delphi Technologies

- Panasonic Automotive

- Mobileye

- Hyundai Mobis

- Aptiv

- Koito Manufacturing

- Lear Corporation

- Hella

Key Target Audience

- Automotive Manufacturers

- Tier 1 Suppliers

- Electric Vehicle Manufacturers

- Autonomous Vehicle Developers

- Government Regulatory Bodies (Saudi Arabian Ministry of Transport)

- Investments and Venture Capitalist Firms

- Automotive Safety Consultants

- OEM and Aftermarket Suppliers

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying key variables influencing the Blind Spot Detection Systems market, such as technological advancements, consumer preferences, regulatory impacts, and automotive industry growth. This is done through secondary research from industry reports, government regulations, and market data from trusted sources.

Step 2: Market Analysis and Construction

Market data is compiled to assess market penetration, adoption rates, and growth potential. This includes evaluating current and future market trends, such as the rise of autonomous vehicles, and assessing the adoption of safety systems across different vehicle segments.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through consultations with industry experts, automotive manufacturers, and technology providers. These interviews provide key insights into the operational and financial aspects of the Blind Spot Detection Systems market.

Step 4: Research Synthesis and Final Output

The final phase consolidates all findings and synthesizes them into a comprehensive report, covering market size, segmentation, and growth projections for the KSA Blind Spot Detection Systems market.

- Executive Summary

- Research Methodology ( Market Definitions and Assumptions ,Blind Spot Detection, ADAS, Sensor Types, etc, Abbreviations and Key Terms Radar, LIDAR, Ultrasonic Sensors, etc, Market Sizing Approach Top-Down and Bottom-Up Methodologies,, Tier-1 Suppliers, Technology Providers)

- Definition and Scope

- Overview Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers

Rising Consumer Demand for Vehicle Safety Features

Technological Advancements in ADAS and Sensor Technologies

Government Regulations on Automotive Safety and Autonomous Driving

Increased Adoption of Electric and Autonomous Vehicles - Market Challenges

High Initial Costs of Advanced Sensor Technologies

Integration Challenges with Existing Vehicle Systems

Limited Awareness in Non-Premium Vehicle Segments - Opportunities

Growth in Autonomous Vehicle Deployment

Expansion of Blind Spot Detection Systems in Mid-Range Vehicles

Growing Demand for Energy-Efficient and Sustainable Automotive Solutions - Trends

Increasing Integration with ADAS and Autonomous Systems

Shift Towards Sensor Fusion Technologies

Advancements in Machine Learning for Enhanced Detection Accuracy - Government Regulation

- SWOT Analysis

- Stakeholder Ecosystem

- Porter’s Five Forces

- Competition Ecosystem

- By Value (USD), 2019-2024

- By Volume (Units Installed), 2019-2025

- By Average Price (Per Unit/System), 2019-2025

- By Technology (In Value %)

Radar-Based Blind Spot Detection

Ultrasonic-Based Blind Spot Detection

Camera-Based Blind Spot Detection

Sensor Fusion-Based Blind Spot Detection - By Application (In Value %)

Passenger Vehicles

Commercial Vehicles

Electric Vehicles (EVs)

Autonomous Vehicles - By Vehicle Type (In Value %)

OEM (Original Equipment Manufacturers)

Aftermarket Installations - By Region (In Value %)

Central Region

Eastern Region

Western Region

Southern Region - By Distribution Channel (In Value %)

OEM Direct Sales

Aftermarket Retailers

Online Sales Channels

Market Share of Major Players

Cross Comparison Parameters (Company Overview, Business Strategies, Technological Innovations, Distribution Channels, Partnerships, Organizational Structure)

Detailed Profiles of Major Companies

Continental AG

Bosch

Denso Corporation

Valeo

Autoliv

ZF Friedrichshafen

Mobileye

Magna International

Hyundai Mobis

Aisin Seiki

Lear Corporation

Koito Manufacturing

Aptiv

Panasonic Automotive

Hella

- Market Demand and Utilization Trends

- Purchasing Power and Budget Allocations for Blind Spot Detection Systems

- Regulatory and Compliance Requirements for Automotive Safety Systems

- Needs, Desires, and Pain Point Analysis for Consumers

- Decision-Making Process for Vehicle Manufacturers and Consumers

- By Value (USD), 2025-2030

- By Volume (Units Installed), 2025-2030

- By Average Price (Per Unit/System), 2025-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now