Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the KSA Border Security Market was valued at USD ~ billion, supported by officially reported budgetary allocations from the Saudi Ministry of Interior and the Saudi Ministry of Defense. The market size is driven by sustained investments in land border surveillance, coastal monitoring systems, integrated command and control infrastructure, and advanced detection technologies deployed across extensive national frontiers. Procurement activity is further reinforced by counter-smuggling operations, protection of cross-border trade routes, and long-term national security modernization programs embedded within sovereign defense spending frameworks.

Based on a recent historical assessment, border security operations in Saudi Arabia are concentrated in Riyadh, Jeddah, Dammam, Jazan, and the northern border corridors adjoining Jordan and Iraq due to strategic, logistical, and geopolitical priorities. Riyadh functions as the primary hub for centralized command, system integration, and policy coordination, while Jeddah and Dammam support maritime surveillance and port security deployments. Southern regions such as Jazan receive heightened attention because of terrain complexity and proximity to regional instability, necessitating continuous monitoring and rapid-response infrastructure.

Market Segmentation

By Product Type

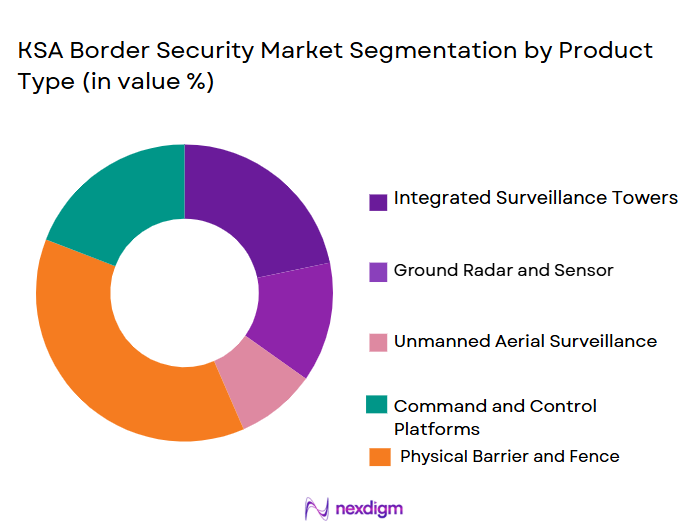

KSA Border Security Market market is segmented by product type into surveillance systems, command and control systems, border fencing solutions, detection and inspection systems, and unmanned security platforms. Recently, surveillance systems have a dominant market share due to sustained requirements for continuous situational awareness across expansive land and maritime borders, coupled with government preference for electro-optical, infrared, radar, and sensor fusion technologies. These systems benefit from scalable deployment, compatibility with existing defense infrastructure, and proven operational effectiveness in harsh desert and coastal environments. The ability of surveillance solutions to integrate with centralized command platforms further reinforces their dominance, as real-time intelligence collection and threat detection remain core national security priorities across border regions.

By Platform Type

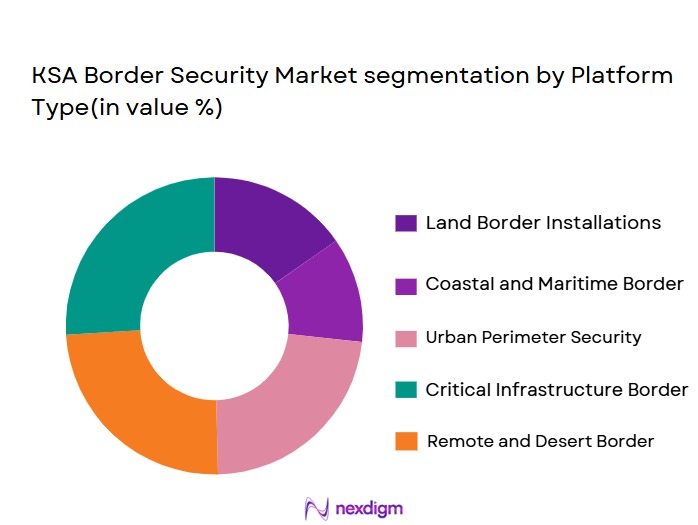

KSA Border Security Market is segmented by platform type into land-based fixed platforms, mobile ground platforms, aerial surveillance platforms, maritime platforms, and integrated multi-domain platforms. Recently, land-based fixed platforms have a dominant market share due to their extensive deployment along long terrestrial borders and critical checkpoints, supported by permanent infrastructure investments. These platforms provide continuous coverage, higher system uptime, and easier integration with power, communications, and monitoring networks. Their dominance is further driven by suitability for harsh desert conditions, lower operational risk compared to mobile or aerial systems, and strong alignment with long-term border fortification strategies adopted by national security agencies.

Competitive Landscape

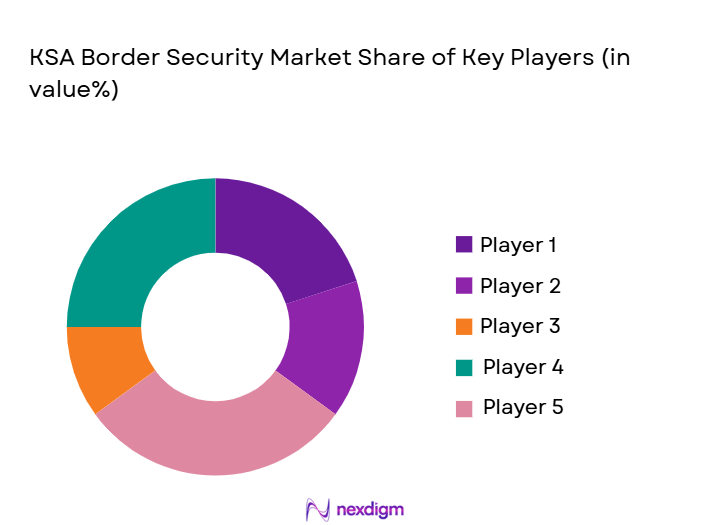

The competitive landscape of the KSA Border Security Market is characterized by moderate consolidation, with a limited number of international defense primes and domestic defense manufacturers dominating large-scale contracts. Long-term government procurement frameworks favor established players with proven system reliability, local manufacturing capabilities, and strong compliance with national security regulations. Strategic partnerships between global technology providers and Saudi defense entities play a critical role in technology transfer, localization, and lifecycle support.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Local Manufacturing Presence |

| Saudi Arabian Military Industries | 2017 | Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Advanced Electronics Company | 1988 | Saudi Arabia | ~

|

~

|

~

|

~

|

~

|

| Thales Saudi Arabia | 2013 | Saudi Arabia | ~

|

~

|

~

|

~

|

~

|

| BAE Systems Saudi Arabia | 1985 | Saudi Arabia | ~

|

~

|

~

|

~

|

~

|

| Lockheed Martin Saudi Arabia | 2016 | Saudi Arabia | ~

|

~

|

~

|

~

|

~

|

KSA Border Security Market Analysis

Growth Drivers

Expansion of National Border Surveillance Infrastructure

Expansion of national border surveillance infrastructure is a critical growth driver for the KSA Border Security Market as Saudi Arabia continues to prioritize territorial integrity, internal stability, and protection of critical national assets across extensive land and maritime borders. Large-scale government programs focus on deploying fixed surveillance towers, long-range radar systems, electro-optical and infrared sensors, ground surveillance radars, and integrated monitoring networks across remote and high-risk border zones. These investments are driven by the need for persistent, round-the-clock situational awareness in challenging desert, mountainous, and coastal environments where manual patrols alone are insufficient. Centralized command centers increasingly rely on real-time data feeds from these surveillance assets to coordinate rapid response, intelligence analysis, and cross-agency operations. Continuous modernization of border infrastructure ensures recurring demand for system upgrades, replacements, and capacity expansion. The scale of Saudi Arabia’s borders necessitates layered surveillance architectures, further increasing procurement volumes. Government-backed funding mechanisms and long-term security planning provide budgetary stability for such infrastructure investments. Integration requirements with existing defense and homeland security systems further amplify demand. Collectively, these factors sustain strong, long-term growth momentum within the market.

Technological Integration and Digital Border Management Systems

Technological integration and digital border management systems represent a major growth driver as Saudi Arabia transitions from conventional border protection toward intelligence-driven, network-centric security models. Digital platforms enable the integration of multiple data sources, including sensors, cameras, radars, and unmanned systems, into unified command and control environments. Artificial intelligence and advanced analytics enhance threat detection accuracy by identifying patterns, anomalies, and potential risks in real time. Secure communication networks allow seamless information sharing across defense forces, border guards, and internal security agencies, improving coordination and response times. Automation reduces reliance on manual monitoring, improving efficiency and lowering long-term manpower requirements. These systems support scalability, allowing authorities to expand coverage as operational needs evolve. Compatibility with legacy infrastructure ensures smoother adoption and protects prior investments. Government emphasis on smart security and digital transformation accelerates procurement of integrated platforms. As digital border management becomes central to national security doctrine, technology-driven demand continues to expand steadily.

Market Challenges

High Capital Expenditure and Long-Term Lifecycle Costs

High capital expenditure and long-term lifecycle costs pose a significant challenge for the KSA Border Security Market, particularly given the complexity and scale of modern border security systems. Advanced surveillance technologies, integrated command platforms, and secure communication networks require substantial upfront investment. Beyond acquisition, ongoing expenses related to maintenance, software upgrades, spare parts, and system calibration significantly increase total cost of ownership. Harsh environmental conditions, including extreme heat, sandstorms, and humidity, accelerate equipment degradation, leading to more frequent repairs and replacements. Budgetary competition with other defense and infrastructure priorities can delay or phase procurement programs. Dependence on imported high-end components exposes projects to currency fluctuations and supply chain disruptions. Specialized training for operators and maintenance personnel further increases operational expenditure. Long procurement cycles and complex contracting frameworks can inflate costs. These financial pressures challenge procurement efficiency and may constrain market expansion despite strong security needs.

System Integration Complexity and Cybersecurity Vulnerabilities

System integration complexity and cybersecurity vulnerabilities represent another major challenge as border security architectures become increasingly interconnected and digitalized. Integrating new technologies with legacy systems requires extensive customization, interoperability testing, and engineering support. Any integration failure can compromise system reliability and operational readiness. Increased connectivity across networks expands exposure to cyber threats targeting sensitive national security data. Ensuring compliance with stringent cybersecurity regulations demands continuous monitoring, upgrades, and risk assessments. Limited availability of specialized cybersecurity expertise further complicates system management. Vendor-specific technologies can create interoperability limitations and long-term dependency risks. Data sovereignty concerns influence technology selection and integration strategies. Addressing these challenges requires additional investment and oversight. Cyber resilience and seamless integration remain persistent operational hurdles for market stakeholders.

Opportunities

Localization and Domestic Defense Manufacturing Development

Localization and domestic defense manufacturing development present a substantial opportunity for the KSA Border Security Market, supported by strong government policies aimed at reducing reliance on foreign suppliers. National initiatives encourage technology transfer, local assembly, and indigenous production of surveillance systems and security platforms. Domestic manufacturing shortens supply chains, improves delivery timelines, and enhances customization for regional operational conditions. Localization also strengthens lifecycle support capabilities, reducing maintenance downtime. Development of local expertise supports workforce skill enhancement and knowledge retention. Partnerships between global defense firms and Saudi entities accelerate industrial capability building. Compliance with local content requirements incentivizes long-term investment commitments. Increased domestic production enhances supply security and strategic autonomy. This opportunity aligns closely with broader national industrial diversification goals and supports sustainable market growth.

Adoption of Autonomous Systems and Advanced Analytics Solutions

Adoption of autonomous systems and advanced analytics solutions offers significant growth opportunities by transforming border security operations through efficiency and precision. Autonomous surveillance platforms reduce dependence on human patrols in remote or high-risk areas. Artificial intelligence-driven analytics enable predictive threat assessment and automated alert generation. Machine learning algorithms continuously improve detection accuracy as data volumes increase. Integration of autonomous systems with existing surveillance infrastructure extends operational reach. Reduced manpower exposure enhances safety and operational sustainability. Government interest in smart and autonomous security technologies accelerates pilot programs and procurement. These solutions support faster decision-making and coordinated responses. As operational confidence grows, autonomous and analytics-driven systems are expected to see broader adoption, creating long-term growth potential.

Future Outlook

The KSA Border Security Market is expected to maintain steady growth over the next five years, driven by continued national security investments and technology modernization initiatives. Advancements in integrated surveillance, digital command platforms, and autonomous systems will shape future deployments. Regulatory support for localization and technology transfer is expected to strengthen domestic capabilities. Demand will remain strong across land and maritime borders due to persistent security requirements and evolving threat landscapes.

Major Players

- Saudi Arabian Military Industries

- Advanced Electronics Company

- Thales Saudi Arabia

- BAE Systems Saudi Arabia

- Lockheed Martin Saudi Arabia

- Raytheon Saudi Arabia

- Leonardo Saudi Arabia

- Northrop Grumman Saudi Arabia

- Saab Saudi Arabia

- HENSOLDT Arabia

- Elbit Systems Arabia

- L3Harris Arabia

- Rheinmetall Denel Munitions Saudi Arabia

- Indra Saudi Arabia

- AirbusDefenceand Space Saudi Arabia

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Defense ministries and internal security agencies

- Border security authorities

- Defense system integrators

- Homeland security departments

- Infrastructure protection agencies

- Port and maritime authorities

Research Methodology

Step 1: Identification of Key Variables

Key variables were identified through analysis of security infrastructure spending, technology adoption patterns, and regulatory frameworks. Primary variables included procurement volumes, system types, and deployment platforms. Secondary variables focused on policy initiatives and industrial localization. These variables formed the analytical foundation.

Step 2: Market Analysis and Construction

Market analysis involved triangulating official budget data with procurement disclosures and industry reports. Segmentation structures were developed based on operational relevance. Data consistency checks ensured reliability. Market construction followed standardized defense market frameworks.

Step 3: Hypothesis Validation and Expert Consultation

Initial hypotheses were validated through expert consultations with defense analysts and industry professionals. Feedback refined assumptions on technology adoption and demand drivers. Cross-verification enhanced accuracy. Insights were incorporated into final assessments.

Step 4: Research Synthesis and Final Output

All findings were synthesized into a structured analytical model. Qualitative and quantitative insights were aligned. Final outputs were reviewed for consistency and compliance. The report reflects validated market intelligence.

- Executive Summary

- KSA Border Security Market Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising emphasis on national sovereignty protection

Expansion of critical infrastructure near border regions

Adoption of integrated surveillance technologies

Increased defense and homeland security budgets

Technological advancements in sensor and analytics systems - Market Challenges

High capital expenditure requirements

Complex integration of legacy and new systems

Harsh environmental and terrain conditions

Cybersecurity and data protection risks

Dependence on foreign technology suppliers - Market Opportunities

Localization of border security manufacturing

Integration of artificial intelligence and automation

Development of multi-agency command platforms - Trends

Shift toward network-centric border security

Increased use of unmanned surveillance systems

Real-time data fusion and analytics adoption

Focus on interoperable and scalable architectures

Growth of predictive threat monitoring solutions - Government Regulations & Defense Policy

Strengthening of national border control regulations

Increased defense policy focus on homeland security

Alignment with international security standards - SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Surveillance and reconnaissance systems

Border fencing and barrier systems

Command and control platforms

Detection and intrusion prevention systems

Integrated border management solutions - By Platform Type (In Value%)

Land-based fixed installations

Mobile ground platforms

Aerial surveillance platforms

Maritime border platforms

Integrated multi-domain platforms - By Fitment Type (In Value%)

New border infrastructure deployment

Retrofit and upgrade installations

Temporary and modular deployments

Mobile and rapid response fitments

Permanent fortified installations - By EndUser Segment (In Value%)

Border guard forces

National armed forces

Internal security agencies

Customs and immigration authorities

Critical infrastructure protection units - By Procurement Channel (In Value%)

Direct government procurement

Defense ministry contracts

Public sector system integrators

Public-private partnership projects

Emergency and rapid acquisition programs - By Material / Technology (in Value %)

Electro-optical and infrared sensors

Radar and ground surveillance technology

Artificial intelligence and analytics software

Secure communication and data fusion systems

Unmanned and autonomous technologies

- Market structure and competitive positioning

- Market share snapshot of major players

Cross Comparison Parameters (Technology integration capability, Local manufacturing presence, System scalability, Cybersecurity robustness, Lifecycle support services, Compliance with regulations, Cost efficiency, Deployment flexibility, Interoperability) - SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Saudi Arabian Military Industries

Advanced Electronics Company

Middle East Defense Systems

Thales Saudi Arabia

BAE Systems Saudi Development & Training

Raytheon Saudi Arabia

Leonardo Saudi Arabia

Lockheed Martin Saudi Arabia

Elbit Systems Arabia

HENSOLDT Arabia

Northrop Grumman Saudi Arabia

Saab Saudi Arabia

L3Harris Arabia

Indra Saudi Arabia

Rheinmetall Denel Munitions Saudi Arabia

- Border forces prioritizing persistent surveillance coverage

- Defense agencies focusing on integrated command capabilities

- Internal security bodies emphasizing rapid response systems

- Customs authorities adopting advanced detection technologies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now