Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA CEP Market generated approximately USD ~ billion in courier, express, and parcel logistics revenue based on a recent historical assessment, according to logistics sector insights from the Saudi Ministry of Transport and Logistics Services and the Communications, Space & Technology Commission. Rapid growth of online retail transactions, cross-border e-commerce imports, and domestic parcel shipping volumes has significantly expanded demand for express logistics networks. Increasing digital commerce adoption, logistics platform investments, and the expansion of integrated delivery infrastructure have also strengthened courier, express, and parcel services across Saudi Arabia.

Riyadh and Jeddah dominate the KSA CEP Market due to their strong logistics infrastructure, dense population clusters, and concentration of major e-commerce distribution facilities. Riyadh functions as the country’s largest parcel distribution hub because it hosts regional headquarters of logistics providers and advanced fulfillment centers supporting online retail. Jeddah plays a critical role due to its proximity to major seaports and international trade routes, while Dammam benefits from industrial manufacturing activity and logistics operations linked to Eastern Province industrial zones.

Market Segmentation

By Product Type

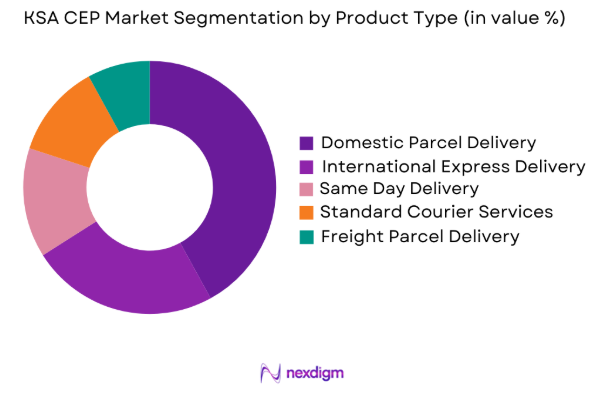

KSA CEP Market is segmented by product type into Domestic Parcel Delivery, International Express Delivery, Same Day Delivery, Standard Courier Services, and Freight Parcel Delivery. Recently, Domestic Parcel Delivery has a dominant market share due to strong expansion of e-commerce logistics, growth of digital marketplaces, and high parcel volumes generated by online retail platforms operating within Saudi Arabia. Domestic delivery networks benefit from shorter transit routes, integrated distribution centers, and advanced last-mile delivery capabilities concentrated in urban regions. Logistics providers have invested heavily in automated sorting facilities and digital tracking platforms to handle rising parcel volumes efficiently. Increasing smartphone penetration and digital payment adoption have accelerated online shopping activity across Saudi cities, significantly boosting demand for domestic parcel services. Retail platforms rely on domestic courier operators for fast order fulfillment, same-day delivery options, and nationwide coverage, strengthening the role of domestic logistics networks within the CEP ecosystem.

By End User

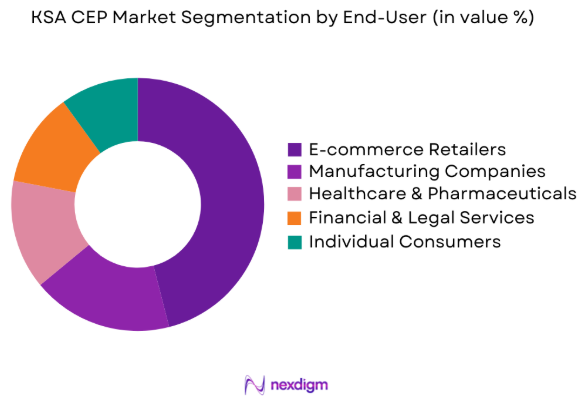

KSA CEP Market is segmented by end user into E-commerce Retailers, Manufacturing Companies, Healthcare & Pharmaceuticals, Financial & Legal Services, and Individual Consumers. Recently, E-commerce Retailers have a dominant market share due to the rapid growth of online retail platforms, digital payment adoption, and nationwide logistics fulfillment expansion. Online marketplaces generate high parcel volumes through consumer purchases of electronics, fashion products, groceries, and household goods. Logistics providers partner with major digital commerce platforms to manage warehousing, order processing, and last-mile delivery networks, strengthening parcel distribution across Saudi cities. Fulfillment centers established by logistics firms support rapid order dispatch and real-time parcel tracking systems that enhance delivery transparency. E-commerce retailers also benefit from integrated logistics technologies including automated sorting, route optimization, and digital customer notification systems, enabling efficient parcel movement across the Kingdom.

Competitive Landscape

The KSA CEP Market demonstrates moderate consolidation with several global logistics companies operating alongside regional courier providers and national postal operators. Large international logistics firms benefit from advanced logistics technology, global distribution networks, and integrated air cargo capabilities that strengthen cross-border parcel delivery. Regional logistics companies maintain strong domestic distribution networks and last-mile delivery capabilities within Saudi cities. Government support for logistics sector development and investments in digital logistics infrastructure continue to encourage competition and innovation among courier, express, and parcel service providers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Size |

| DHL Express | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| Aramex | 1982 | Dubai, UAE | ~ | ~ | ~ | ~ | ~ |

| FedEx | 1971 | Tennessee, USA | ~ | ~ | ~ | ~ | ~ |

| UPS | 1907 | Georgia, USA | ~ | ~ | ~ | ~ | ~ |

| Saudi Post SPL | 1926 | Riyadh, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

KSA CEP Market Analysis

Growth Drivers

Expansion of E-commerce Platforms and Online Retail Logistics Demand

Rapid expansion of digital commerce platforms across Saudi Arabia has significantly increased demand for courier, express, and parcel services as online shopping generates high parcel volumes requiring efficient logistics networks. Major e commerce marketplaces operate fulfillment centers and rely heavily on courier operators to distribute products across cities and suburban regions. Rising smartphone usage, strong internet connectivity, and digital payment adoption have accelerated online purchasing behavior. Logistics companies are expanding distribution hubs, automated sorting facilities, and parcel tracking technologies to manage growing shipment volumes. Retailers also partner with courier providers to improve order fulfillment speed and delivery reliability while expanding last mile delivery networks across urban areas.

Government Investment in Logistics Infrastructure and Vision 2030 Supply Chain Development

Large scale government investments in logistics infrastructure are strengthening the courier, express, and parcel industry in Saudi Arabia by improving transportation networks and distribution efficiency. National logistics transformation initiatives under Vision 2030 aim to position the country as a regional logistics hub connecting Asia, Europe, and Africa. Development of advanced logistics zones, freight corridors, and smart ports is enhancing cargo movement and supply chain connectivity. Airports and seaports are expanding cargo handling capabilities to support faster parcel processing. Authorities are also promoting digital logistics technologies and automated distribution centers. Expansion of highways, rail corridors, and cargo terminals improves connectivity between cities and industrial regions.

Market Challenges

High Last Mile Delivery Costs and Urban Logistics Complexity

Last mile delivery operations pose a major challenge for courier, express, and parcel companies because transporting parcels from distribution hubs to final destinations requires significant logistics resources. Urban congestion, complex routing, and fluctuating delivery demand often reduce operational efficiency and increase delivery costs. Logistics providers must operate large vehicle fleets, maintain multiple distribution centers, and employ substantial driver networks to manage shipments effectively. Rising fuel prices and vehicle maintenance expenses further elevate operational costs. Managing deliveries in dense urban environments also requires advanced routing software and digital logistics platforms. Increasing consumer demand for same day or next day delivery intensifies operational pressure on courier companies.

Regulatory Compliance and Cross Border Shipping Constraints

Regulatory procedures and customs clearance requirements create operational challenges for courier, express, and parcel companies involved in international deliveries because cross border shipments must comply with extensive documentation and inspection protocols. Parcels entering Saudi Arabia often require customs declarations, import duty verification, and regulatory approvals before release. These procedures can delay deliveries and increase operational costs for logistics providers managing international shipments. Compliance with global shipping regulations and security standards requires specialized administrative expertise and dedicated compliance systems. Differences in regulatory frameworks across countries further complicate cross border logistics operations. As international e commerce shipments grow, efficient customs management remains a significant challenge for logistics companies.

Opportunities

Expansion of Smart Logistics and Automated Parcel Processing Infrastructure

Rapid development of smart logistics infrastructure is creating strong opportunities for courier, express, and parcel companies across Saudi Arabia as automation technologies significantly improve parcel processing efficiency. Automated sorting facilities, robotic warehouses, and AI driven logistics platforms allow companies to manage higher shipment volumes with greater accuracy. These systems reduce manual handling and speed up operations within distribution centers. Logistics providers are investing in automated warehouses and digital parcel management tools to enhance productivity. Advanced route optimization and predictive analytics help improve delivery planning and reduce transit times. Internet of Things technologies enable real time parcel tracking and operational monitoring. Such innovations allow logistics companies to scale services while maintaining reliable delivery performance.

Growth of Same Day and On Demand Delivery Services in Urban Regions

Rising consumer expectations for rapid deliveries are encouraging logistics companies to expand same day and on demand parcel services across major Saudi cities. Urban shoppers increasingly expect products purchased through digital marketplaces to arrive within hours rather than days. Courier companies are therefore building specialized express delivery networks supported by strategically located fulfillment centers and real time parcel tracking systems. Retailers integrate delivery solutions directly into e-commerce platforms to enable faster dispatch and order scheduling. Growth of quick commerce models such as grocery delivery is further increasing demand for ultra fast logistics. To support these services, companies are expanding urban hubs and deploying smaller delivery vehicles that improve efficiency within dense city environments.

Future Outlook

The KSA CEP Market is expected to experience sustained growth due to expanding e-commerce activity, investments in logistics infrastructure, and increasing adoption of digital logistics technologies. Automated warehouses, AI driven route optimization, and real-time parcel tracking platforms will enhance delivery efficiency across logistics networks. Government initiatives aimed at strengthening Saudi Arabia’s role as a regional logistics hub will further support market expansion. Rising consumer expectations for faster deliveries and increasing cross-border e-commerce shipments will continue to shape future demand across courier, express, and parcel logistics services.

Major Players

- DHL Express

- Aramex

- FedEx

- UPS

- Saudi Post SPL

- SMSA Express

- NaqelExpress

- AJEX Logistics Services

- Saudi Logistics Services SAL

- ZajilExpress

- Fetchr

- Aramex Saudi Arabia

- UPS Saudi Arabia

- DHL Saudi Arabia

- SMSA Logistics

Key Target Audience

- E-commerce Retail Platforms

- Logistics and Supply Chain Companies

- Manufacturing and Industrial Enterprises

- Retail Distribution Companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Transportation Infrastructure Developers

- International Trade and Export Companies

Research Methodology

Step 1: Identification of Key Variables

Key logistics indicators including parcel shipment volume, courier network coverage, digital commerce penetration, and logistics infrastructure capacity were identified. These variables were analyzed to understand factors influencing CEP market demand and operational performance across Saudi Arabia.

Step 2: Market Analysis and Construction

Market data was compiled from logistics industry databases, government transportation statistics, and corporate disclosures. Analytical frameworks were applied to assess parcel shipment flows, delivery infrastructure development, and technology adoption within courier and express logistics networks.

Step 3: Hypothesis Validation and Expert Consultation

Industry insights were validated through consultations with logistics professionals, supply chain analysts, and transportation experts. Expert feedback helped confirm operational trends, regulatory developments, and infrastructure investments affecting the courier, express, and parcel sector.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative findings were synthesized into a comprehensive market framework. This final stage integrated industry data, technology trends, infrastructure developments, and expert insights to present a structured evaluation of the KSA CEP Market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of ECommerce and Online Retail Platforms

Growth in Cross Border Trade and International Logistics Demand

Government Investment in Logistics Infrastructure and Smart Ports - Market Challenges

High Operational Costs and Last Mile Delivery Complexity

Regulatory Compliance and Customs Clearance Delays

Infrastructure Gaps in Remote Delivery Regions - Market Opportunities

Expansion of Smart Logistics and Automated Warehousing

Growth of Same Day and On Demand Delivery Services

Integration of Artificial Intelligence in Route Optimization - Trends

Increasing Adoption of Autonomous Delivery Technologies

Rising Integration of Digital Parcel Tracking Platforms

Expansion of Fulfilment Centres Supporting ECommerce Growth - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Domestic Parcel Delivery Services

International Express Delivery Services

Same Day Delivery Services

Standard Courier Services

Freight and Heavy Parcel Delivery Services - By Platform Type (In Value%)

Ground Transportation Networks

Air Cargo Networks

Integrated Logistics Platforms

Digital Parcel Management Platforms

Automated Distribution Centers - By Fitment Type (In Value%)

Business to Business Delivery Solutions

Business to Consumer Delivery Solutions

Consumer to Consumer Delivery Services

Hybrid Logistics Integration Solutions

Cross Border Logistics Solutions - By End User Segment (In Value%)

ECommerce Retailers

Manufacturing and Industrial Enterprises

Healthcare and Pharmaceutical Companies

Financial and Legal Services Firms

Individual Consumers - By Procurement Channel (In Value%)

Direct Corporate Contracts

Online Logistics Platforms

Government Procurement Programs

Third Party Logistics Integrators

ECommerce Marketplace Partnerships

- Market Share Analysis

- Cross Comparison Parameters (Delivery Network Coverage, Logistics Technology Integration, Pricing Structure, Delivery Speed Capability, Cross Border Logistics Capacity)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Saudi Post SPL

Aramex

DHL Express

FedEx

UPS

SMSA Express

Naqel Express

AJEX Logistics Services

Saudi Logistics Services SAL

Zajil Express

Fetchr

Aramex Saudi Arabia

UPS Saudi Arabia

DHL Saudi Arabia

SMSA Logistics

- Growing Demand from Rapidly Expanding ECommerce Retailers

- Manufacturing Sector Reliance on Efficient Distribution Networks

- Healthcare Industry Demand for Secure Medical Logistics

- Increasing Consumer Adoption of Online Shopping Platforms

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now