Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the KSA Cloud Infrastructure Market, which encompasses cloud compute, storage, networking, and data center platforms, was valued at approximately USD ~ billion according to credible market research data reflecting revenue generated across public and private cloud services. The market is driven by government Vision 2035 digital transformation agendas, increasing enterprise and government cloud adoption for scalable IT workloads, and substantial investments from global hyper scalers and local service providers to expand cloud and data center footprints.

Dominant urban centers driving the cloud infrastructure market include Riyadh, Jeddah, and Dammam, where economic diversification initiatives, concentration of enterprise IT spending, and investment in smart city and AI programs create strong demand for cloud services and underlying infrastructure. These cities host a significant portion of financial services, government digital services, and enterprise IT modernization projects that require scalable, secure cloud platforms supported by global providers and local partners capable of delivering advanced compute, storage, and networking infrastructure.

Market Segmentation

By Service Model

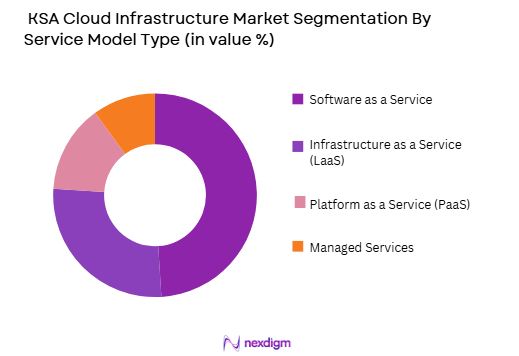

KSA Cloud Infrastructure Market is segmented by service model into Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS), and Managed Services. Recently, Software as a Service (SaaS) has a dominant market share due to high demand from enterprises and government entities for ready‑to‑use business applications, strong adoption of productivity and collaboration tools, lower implementation complexity compared to foundational infrastructure services, and well‑established global vendor ecosystems offering localized solutions. SaaS delivers immediate value in digital transformation programs, enabling organizations to accelerate cloud migration without deep in‑house cloud expertise, which reinforces its prominence in cloud spending patterns across sectors such as banking, healthcare, and public services.

By Deployment Type

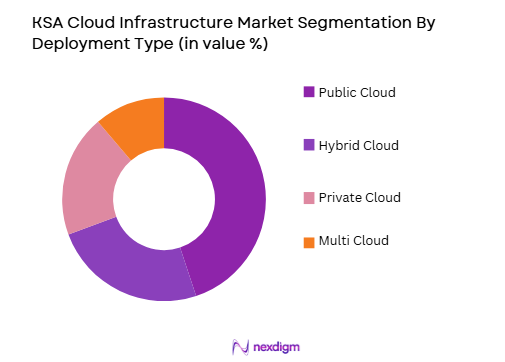

KSA Cloud Infrastructure Market is segmented by deployment type into Public Cloud, Private Cloud, Hybrid Cloud, and Multi‑Cloud. Recently, Public Cloud has a dominant market share due to factors such as scalability and cost efficiency driving adoption among enterprises of all sizes, strong presence and investment by global hyperscalers in local data center regions, and regulatory support that facilitates secure public cloud deployment. Public cloud also supports flexible consumption models that appeal to organizations seeking rapid digital transformation and innovation without heavy upfront infrastructure costs.

Competitive Landscape

The KSA Cloud Infrastructure Market is competitive and includes global cloud service providers, regional telecom operators, and data center infrastructure companies expanding local capabilities through partnerships, investment, and compliance with regulatory frameworks. Consolidation is driven by major hyperscalers establishing local cloud regions, telcos offering managed and hybrid cloud services, and strategic alliances that enhance service portfolios and geographic reach within the Kingdom’s digital economy.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Local Data Center Capacity |

| Amazon Web Services (AWS) | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | USA | ~ | ~ | ~ | ~ | ~ |

| Google Cloud | 2008 | USA | ~ | ~ | ~ | ~ | ~ |

| STC Cloud | 2016 | Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Oracle Cloud | 1977 | USA | ~ | ~ | ~ | ~ | ~ |

KSA Cloud Infrastructure Market Analysis

Growth Drivers

Digital Transformation Acceleration Across Public and Private Sectors

The demand for cloud infrastructure in Saudi Arabia is predominantly propelled by digital transformation initiatives across both government and corporate sectors seeking to modernize their IT environments and support innovation agendas. Many organizations are migrating legacy systems to cloud platforms to achieve greater agility, resilience, and cost‑efficiency while leveraging advanced capabilities such as big data analytics, artificial intelligence, and machine learning. Government mandates such as cloud‑first policies encourage public entities to adopt cloud services, which stimulates infrastructure deployment and service consumption. Enterprises in banking, healthcare, and telecommunications are also investing significantly in cloud solutions to support customer experience enhancements, remote work enablement, and digital service delivery. Such transformation efforts require scalable compute, storage, and network resources that only cloud infrastructure can efficiently deliver. Additionally, hyperscale cloud providers are expanding local data center capacity, which further accelerates adoption by reducing latency and enhancing compliance with data residency requirements. Enterprise adoption patterns indicate prioritized cloud spend on mission‑critical workloads, disaster recovery, and hybrid deployments that integrate on‑premises systems with public cloud platforms. This strategic shift towards cloud‑native architectures reinforces ongoing demand for foundational infrastructure expansion and aligns with broader economic diversification goals.

Enterprise Cost Optimization and IT Modernization Requirements

Another significant factor driving the expansion of cloud infrastructure in the Kingdom lies in enterprise initiatives aimed at optimizing IT costs and modernizing legacy systems. Cloud adoption enables companies to reduce reliance on capital‑intensive on‑premises data centers, shift to operational expenditure models, and scale computing resources in alignment with business demand. Organizations can achieve highly elastic resource provisioning, which helps manage peak workloads during seasonal or project‑based demands without incurring fixed infrastructure overhead. Hybrid cloud models allow enterprises to balance sensitive workloads in private environments while leveraging public cloud for less critical tasks, improving utilization and cost efficiency. Cloud migration also supports digital innovation initiatives, enabling businesses to experiment with new services without long procurement cycles or infrastructure deployments. With local cloud regions under development, enterprises benefit from improved latency, enhanced security, and better adherence to compliance requirements. The availability of managed cloud services further reduces in‑house staffing challenges and streamlines operational complexity, which is particularly attractive for small and medium‑sized businesses with limited IT resources. These cost and modernization imperatives are central in shaping cloud infrastructure expansion across the KSA market landscape.

Market Challenges

Data Sovereignty and Regulatory Compliance Complexities

Despite strong adoption momentum, cloud infrastructure growth in Saudi Arabia faces challenges linked to evolving regulatory requirements around data sovereignty, privacy, and cybersecurity frameworks. Organizations must ensure compliance with national standards mandating that sensitive data be stored and processed within the Kingdom, which can constrain choices around cloud service providers and deployment models. Regulatory changes require careful governance strategies and monitoring to avoid non‑compliance risks, and enterprises often need to invest in legal, security, and audit expertise to align cloud operations with policy requirements. Differing interpretations of compliance frameworks across business sectors can add complexity to procurement and deployment processes. Additionally, multinational companies operating in Saudi Arabia must navigate both local regulations and global data protection standards, which may create conflicts or require bespoke hybrid solutions. These compliance pressures can elevate cloud adoption costs and extend project timelines if organizations lack internal capabilities to coordinate regulatory alignment. Trust and transparency concerns around data residency and cross‑border data flows may also influence enterprise decision‑making, potentially favoring vendors with robust compliance track records. Standardizing regulatory interpretations and providing clearer guidance could mitigate some challenges.

Talent Shortages and Skill Gaps in Cloud Technologies

Another important challenge for the KSA Cloud Infrastructure Market involves talent shortages and skill gaps in cloud technologies among local IT workforces. Cloud infrastructure deployment, management, and optimization require specialized skill sets including cloud architecture design, security operations, network engineering, and DevOps practices. While many enterprises aggressively pursue cloud modernization, the availability of certified professionals within the Kingdom is limited, leading to reliance on expatriate talent or external service partners. This talent gap can slow down project execution, increase consulting and outsourcing costs, and hinder internal capability building within organizations. Training programs and certification initiatives supported by government and industry collaborations are in progress, but skill development often lags behind rapid infrastructure adoption. Organizations may also face retention challenges as skilled cloud professionals are in high demand globally, prompting competitive compensation requirements. Addressing the talent shortage requires strategic investments in education, certification programs, and workforce development initiatives that align with cloud technology needs. Failure to bridge these gaps may slow long‑term cloud infrastructure scaling and reduce the efficiency gains expected from cloud transformation.

Opportunities

Expansion of Hybrid and Multi‑Cloud Adoption Models

As enterprises evolve their cloud strategies, there is a compelling opportunity for cloud infrastructure providers to support hybrid and multi‑cloud adoption models that balance security, performance, and cost considerations. Hybrid cloud environments enable organizations to retain sensitive workloads on private platforms while leveraging public cloud scalability for less critical use cases, delivering a flexible architecture that aligns with data residency requirements. Multi‑cloud strategies further enhance resilience and service optimization by allowing enterprises to distribute workloads across multiple cloud vendors, reducing vendor lock‑in and enhancing business continuity. Cloud infrastructure providers that can offer seamless integration, unified management tools, and security frameworks tailored for hybrid and multi‑cloud environments are well‑positioned to capture this evolving demand. Investment in platforms that support mesh networking, containerization, and orchestration technologies like Kubernetes can enhance interoperability across disparate cloud ecosystems. Training and certification programs aligned with hybrid cloud skills can further empower IT teams to manage complex multi‑vendor deployments. In KSA’s context, hybrid and multi‑cloud adoption aligns with regulatory needs while providing enterprises with strategic flexibility, which creates a significant avenue for infrastructure service differentiation and revenue growth.

AI‑Optimized Cloud Services and Edge Infrastructure Deployment

The increasing focus on artificial intelligence, machine learning, and edge computing presents another strategic opportunity for the KSA Cloud Infrastructure Market. As enterprises and government agencies adopt AI workloads and analytics‑driven applications, cloud infrastructure providers can deliver optimized services that support high‑performance compute, GPU‑accelerated instances, and localized data processing capabilities. Edge infrastructure deployments in urban centers can improve latency and support IoT, real‑time analytics, and smart city initiatives integral to Vision 2030 goals. Partnerships between cloud providers and local data center operators to deploy edge nodes expand service reach and create differentiated offerings that address performance‑critical use cases. Integration with AI toolchains and data pipelines enhances enterprise capabilities to deploy intelligent applications on cloud platforms. Demand for cloud‑native security services and managed AI infrastructure further opens service monetization avenues. These initiatives align with KSA’s broader digital economy targets and position cloud infrastructure providers to participate in next‑generation computing ecosystems.

Future Outlook

The KSA Cloud Infrastructure Market is expected to grow robustly over the next five years as digital transformation agendas, enterprise cloud migration initiatives, and government programs continue to drive demand for scalable, secure compute and storage platforms. Expansion of local cloud regions by hyperscalers, regulatory developments that support data residency and cybersecurity, and investments in hybrid and multi‑cloud architectures will shape future infrastructure capacity. Adoption of AI‑ready cloud services and edge computing will further diversify service offerings. Continued economic diversification under Vision 2030 will stimulate cloud demand across industries.

Major Players

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- Oracle Cloud

- IBM Cloud

- STC Cloud

- Mobily Cloud

- Zain Cloud

- Alibaba Cloud

- Huawei Cloud

- SAP

- Salesforce

- Dell Technologies Cloud

- VMware Cloud

- Tencent Cloud

Key Target Audience

- Cloud service providers and hyper scalers

- Telecommunications operators

- Enterprise CIOs and CTOs

- Investments and venture capitalist firms

- Government and regulatory bodies

- Data center operators

- AI and digital transformation solution providers

- Managed service providers

Research Methodology

Step 1: Identification of Key Variables

Core variables such as cloud service models, deployment types, regional infrastructure capabilities, regulatory frameworks, and technology adoption drivers were defined to structure the market analysis and segmentation.

Step 2: Market Analysis and Construction

Market size and segmentation were developed using authoritative cloud computing revenue data, regional digital transformation indicators, and enterprise cloud adoption patterns to derive structure and growth patterns across service models and deployment types.

Step 3: Hypothesis Validation and Expert Consultation

Research assumptions about drivers, challenges, and opportunities were validated through synthesis of credible industry sources, regulatory context, and enterprise cloud strategies to ensure alignment with actual market dynamics.

Step 4: Research Synthesis and Final Output

Validated insights were integrated into a comprehensive report covering market overview, segmentation, competitive landscape, market drivers, challenges, opportunities, future outlook, and target audience.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National digital transformation and cloud first policies

Expansion of hyperscale data center investments

Enterprise migration to cloud and hybrid architectures - Market Challenges

Data sovereignty and localization compliance requirements

High capital and operational cost of hyperscale infrastructure

Cybersecurity and data protection risks - Market Opportunities

Growth of sovereign and government cloud platforms

Expansion of AI and data analytics cloud infrastructure

Regional cloud hub development in the Middle East - Trends

Shift toward hybrid and multi cloud architectures

Edge cloud deployment for low latency applications

AI optimized cloud infrastructure expansion - Government regulations

Data localization and cloud compliance frameworks

Cybersecurity and national cloud certification policies

Digital economy and cloud adoption incentives - SWOT Analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Public Cloud Infrastructure

Private Cloud Infrastructure

Hybrid Cloud Infrastructure

Edge Cloud Infrastructure

High Performance Computing Cloud - By Platform Type (In Value%)

IaaS Platforms

PaaS Platforms

Container and Kubernetes Platforms

Serverless Computing Platforms

AI and Data Analytics Cloud Platforms - By Fitment Type (In Value%)

Hyperscale Data Center Infrastructure

Enterprise Cloud Deployments

Government Cloud Zones

Industry Specific Cloud Environments

Multi Cloud Orchestration Systems - By End User Segment (In Value%)

Government and Public Sector

Telecom and Digital Service Providers

Financial Services Institutions

Energy and Industrial Enterprises

Ecommerce and Digital Native Firms - By Procurement Channel (In Value%)

Direct Hyper scaler Contracts

Cloud Managed Service Providers

Telecom Cloud Partnerships

Government Procurement Programs

System Integrators and Resellers

- Market Share Analysis

- Cross Comparison Parameters (Data Center Scale Capacity, Cloud Service Portfolio Breadth, AI and HPC Infrastructure Capability, Hybrid and Multi Cloud Integration, Data Sovereignty and Compliance Support)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services

Microsoft Azure

Google Cloud

Oracle Cloud

Alibaba Cloud

STC Cloud

Mobily Cloud

Saudi Telecom Company

Aramco Digital

NEOM Tech and Digital

Huawei Cloud

IBM Cloud

SAP Cloud

Dell Technologies Cloud

Equinix

- Government agencies adopting sovereign cloud

- Telecom operators deploying edge cloud platforms

- Enterprises migrating mission critical workloads

- Digital firms scaling cloud native infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now