Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA Cold Chain Logistics market generated approximately USD ~ billion in logistics service revenue based on recent assessments compiled from the Saudi Ministry of Transport and Logistics Services and industry data from the Saudi Food and Drug Authority. Growth in the sector is driven by rising demand for temperature-controlled storage and distribution across food imports, pharmaceuticals, and modern retail supply chains. Increasing refrigerated warehousing capacity, expansion of food retail networks, and large-scale infrastructure investments under national logistics development programs continue to support cold chain logistics demand.

Riyadh, Jeddah, and Dammam dominate cold chain logistics activity due to concentration of distribution hubs, food processing facilities, and large population centers requiring high volumes of temperature-controlled products. Major logistics corridors linking ports and inland consumption centers enable efficient refrigerated transport networks. Industrial zones and logistics parks located near King Abdulaziz Port, Jeddah Islamic Port, and King Khalid International Airport provide integrated cold storage infrastructure supporting food imports, pharmaceutical distribution, and supermarket supply chains across the Kingdom.

Market Segmentation

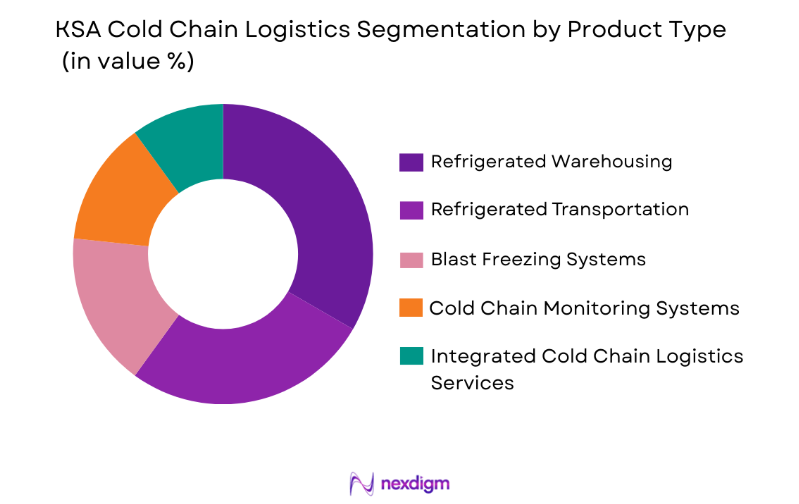

By Product Type

KSA Cold Chain Logistics market is segmented by product type into refrigerated warehousing, refrigerated transportation, blast freezing systems, cold chain monitoring systems, and integrated cold chain logistics services. Recently, refrigerated warehousing has a dominant market share due to increasing demand for large temperature-controlled storage facilities supporting food imports, pharmaceutical products, and frozen food distribution. Rapid expansion of supermarket chains and foodservice operators has created strong demand for centralized cold storage hubs capable of maintaining strict temperature standards. Saudi Arabia relies heavily on imported perishable food products including dairy, seafood, meat, and fresh produce, requiring large refrigerated storage infrastructure near major ports and urban consumption centers. Pharmaceutical distribution networks also require specialized storage facilities to maintain temperature stability for vaccines and biologics. Logistics companies are expanding warehouse capacity within industrial logistics parks located near Riyadh, Jeddah, and Dammam to support regional distribution networks. Investments in automated storage systems, digital temperature monitoring, and energy-efficient refrigeration technologies further strengthen the role of warehousing infrastructure within the cold chain logistics ecosystem.

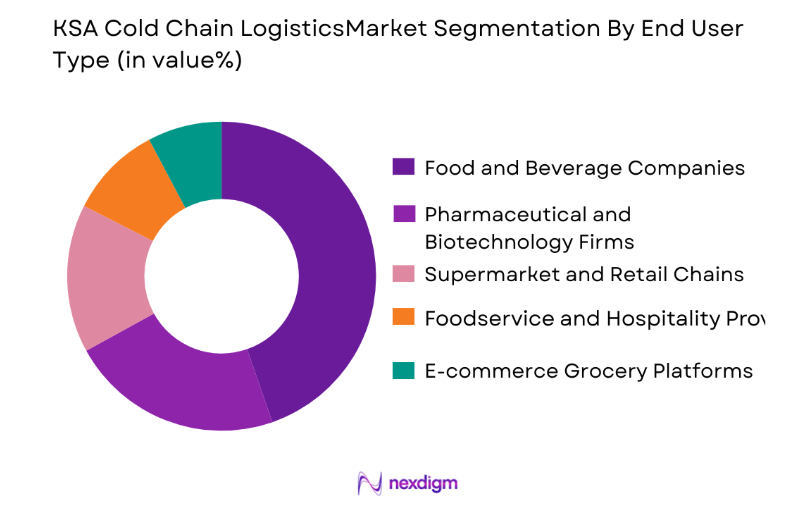

By End User Industry

KSA Cold Chain Logistics market is segmented by end user industry into food and beverage companies, pharmaceutical and biotechnology firms, supermarket and retail chains, foodservice and hospitality providers, and e-commerce grocery platforms. Recently, food and beverage companies have a dominant market share due to strong demand for temperature controlled logistics across dairy products, meat processing, seafood imports, and frozen food distribution. Saudi Arabia imports large quantities of perishable food products due to limited domestic agricultural production in certain categories, increasing reliance on cold chain infrastructure. Food processing companies and large dairy producers maintain strict temperature management requirements during transportation and storage to preserve product quality and shelf life. The expansion of supermarket chains and food distribution networks also increases demand for refrigerated logistics operations. Cold chain providers support these operations through refrigerated trucks, distribution hubs, and specialized storage facilities located near food manufacturing plants and urban retail markets. Continuous growth in food consumption and expansion of organized retail networks further reinforce the dominance of the food and beverage sector within the market.

Competitive Landscape

The KSA Cold Chain Logistics market is moderately consolidated with a mix of domestic logistics providers and international supply chain companies operating across refrigerated storage and transportation segments. Large logistics companies maintain competitive advantages through nationwide distribution networks, integrated warehousing infrastructure, and advanced temperature monitoring systems. Strategic partnerships with food producers, pharmaceutical companies, and retail chains enable major operators to secure long-term logistics contracts and expand cold chain capacity across key logistics corridors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Cold Storage Capacity |

| Agility Logistics | 1979 | Kuwait City | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Bonn | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Schindellegi | ~ | ~ | ~ | ~ | ~ |

| Aramex | 1982 | Dubai | ~ | ~ | ~ | ~ | ~ |

| CEVA Logistics | 2007 | Marseille | ~ | ~ | ~ |

KSA Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of Temperature-Controlled Food Supply Chains Driven by Rising Food Imports

Saudi Arabia relies heavily on imported food products to meet domestic consumption demand, which significantly strengthens the requirement for efficient temperature-controlled logistics networks across the Kingdom. Large volumes of meat, seafood, dairy products, fruits, and frozen foods are imported through seaports such as Jeddah Islamic Port and King Abdulaziz Port, requiring specialized refrigerated storage and transportation systems to maintain product quality during distribution. Modern retail expansion across Riyadh, Jeddah, and Dammam increases demand for reliable cold storage facilities capable of handling large inventory volumes for supermarkets and hypermarkets. Food processing companies also require refrigerated logistics to distribute packaged food products nationwide while maintaining strict temperature standards. Growing consumer demand for fresh and frozen food products continues to expand cold chain transportation requirements linking ports, warehouses, and retail outlets. Logistics companies are investing heavily in refrigerated fleets and advanced cold storage infrastructure to support the country’s evolving food distribution ecosystem. Government food security initiatives further encourage expansion of food supply chains and increase investments in logistics infrastructure supporting perishable goods distribution. Digital monitoring technologies are increasingly used to track temperature conditions during transportation and storage to ensure regulatory compliance and product safety. Rising consumption of packaged foods and frozen products among urban consumers continues to strengthen demand for temperature-controlled logistics networks across the national food supply system.

Rapid Growth of Pharmaceutical and Biopharmaceutical Distribution Requiring Strict Temperature Control

Pharmaceutical distribution networks represent one of the most important growth drivers for cold chain logistics across Saudi Arabia due to strict temperature requirements associated with modern medicines, vaccines, and biologic treatments. Pharmaceutical companies rely on specialized cold chain infrastructure to transport temperature-sensitive drugs safely across long distances without compromising product stability. Healthcare expansion and increasing demand for advanced medical treatments significantly increase pharmaceutical distribution volumes across hospitals, clinics, and pharmacies nationwide. Temperature-controlled logistics ensures that vaccines, biologics, and specialty drugs remain effective throughout transportation and storage processes. Pharmaceutical regulators enforce strict compliance requirements that require logistics providers to maintain precise temperature monitoring and quality assurance systems. Logistics operators increasingly adopt advanced monitoring technologies including real-time sensors and digital tracking platforms to ensure temperature stability during shipment. Expanding pharmaceutical manufacturing and import activity across the Kingdom further increases demand for specialized cold chain storage and distribution facilities. The growth of biotechnology medicines, which require highly controlled temperature conditions, further strengthens the need for advanced refrigerated logistics networks. Healthcare infrastructure development programs and expansion of pharmaceutical distribution networks create long-term demand for temperature-controlled logistics operations supporting the medical supply chain.

Market Challenges

High Capital Investment Requirements for Cold Storage Infrastructure Development

Cold chain logistics infrastructure requires significant capital investment due to the high cost associated with building refrigerated warehouses, purchasing specialized transportation fleets, and installing advanced refrigeration equipment capable of maintaining precise temperature ranges. Developing large temperature-controlled storage facilities involves complex engineering requirements including insulation systems, refrigeration compressors, backup power infrastructure, and monitoring technologies. Logistics providers must also invest heavily in energy-efficient refrigeration technologies to ensure operational reliability while managing electricity consumption costs. Establishing cold chain networks across large geographic areas within Saudi Arabia requires construction of multiple distribution hubs located near ports, airports, and urban consumption centers. Maintaining refrigerated transportation fleets also requires significant capital investment in specialized vehicles equipped with temperature-controlled containers. Operational expenses associated with refrigeration systems further increase logistics costs due to high electricity consumption. Smaller logistics providers often face financial barriers that limit their ability to expand cold storage capacity or upgrade refrigeration technology. As a result, market growth can be constrained by the high capital requirements needed to establish and maintain advanced cold chain infrastructure. Continuous investment in maintenance, monitoring technology, and energy efficiency improvements further increases operational costs for logistics companies operating in the sector.

Energy Consumption and Operational Cost Pressures in Refrigerated Logistics Operations

Refrigerated logistics systems consume large amounts of electricity due to continuous operation of cooling equipment required to maintain stable temperature conditions inside storage facilities and transportation vehicles. Cold storage warehouses operate refrigeration compressors and cooling units around the clock to maintain product safety and prevent spoilage. Energy costs represent one of the largest operational expenses for logistics providers managing refrigerated storage infrastructure. Saudi Arabia’s hot climate conditions further increase cooling requirements for refrigerated facilities and transport vehicles. Maintaining temperature stability during long transportation distances also requires high-capacity refrigeration systems within refrigerated trucks and shipping containers. Logistics companies must invest in advanced insulation technology and energy-efficient refrigeration systems to reduce operating costs while maintaining temperature standards. Rising electricity consumption in cold storage facilities increases pressure on logistics companies to adopt sustainable refrigeration technologies and renewable energy solutions. Operational efficiency becomes critical for cold chain providers seeking to maintain profitability while managing rising energy expenses. These cost pressures can limit expansion of cold chain infrastructure in certain regions and increase overall logistics service pricing across the market.

Opportunities

Development of Large Integrated Cold Chain Logistics Parks Supporting National Food Security Programs

Saudi Arabia continues to invest heavily in logistics infrastructure development under national economic diversification strategies designed to strengthen supply chain resilience and food security. Large logistics parks and integrated distribution hubs provide significant opportunities for cold chain operators to expand refrigerated storage capacity and transportation networks. These logistics zones are strategically located near ports, airports, and industrial centers to support efficient distribution of perishable goods across domestic markets. Integrated cold chain infrastructure allows logistics providers to consolidate warehousing, packaging, and distribution operations within centralized logistics parks. Such facilities enable efficient handling of imported food products while maintaining strict temperature control during storage and distribution. Government support for logistics infrastructure development encourages private investment in cold chain facilities that support food supply chains across the Kingdom. Expansion of food processing industries further increases demand for refrigerated logistics services connecting manufacturing plants with national retail distribution networks. Integrated logistics parks equipped with advanced cold storage facilities provide scalable solutions for handling growing food import volumes and expanding food distribution networks across Saudi Arabia.

Adoption of Smart Cold Chain Technologies and Digital Temperature Monitoring Systems

Technological innovation within cold chain logistics presents major opportunities for logistics companies seeking to improve operational efficiency and product safety. Advanced digital monitoring systems allow logistics operators to track temperature conditions in real time across warehouses and transportation vehicles. Internet-of-Things sensors installed inside refrigerated containers continuously monitor temperature levels and alert operators when deviations occur. Digital logistics platforms also allow companies to track shipment conditions throughout the supply chain and ensure compliance with regulatory requirements for pharmaceutical and food distribution. Smart monitoring technology improves transparency within the cold chain ecosystem while reducing product spoilage and operational risk. Automation technologies are increasingly integrated within refrigerated warehouses to improve inventory management and handling efficiency. Energy-efficient refrigeration systems and smart energy management platforms also reduce operational costs for cold storage facilities. As logistics companies invest in digital infrastructure and automation technologies, cold chain networks become more reliable and scalable, creating new opportunities for advanced temperature-controlled logistics services across Saudi Arabia.

Future Outlook

The KSA Cold Chain Logistics market is expected to experience steady expansion as food consumption, pharmaceutical distribution, and modern retail networks continue to grow across the Kingdom. Increasing investment in logistics infrastructure and industrial logistics zones will strengthen refrigerated warehousing capacity and distribution efficiency. Adoption of digital monitoring technologies and automated storage systems will enhance operational reliability and product safety. Government logistics development strategies and food security initiatives are likely to further accelerate investments in temperature-controlled logistics infrastructure across major logistics corridors.

Major Players

- Agility Logistics

- DHL Supply Chain

- Kuehne + Nagel

- DB Schenker

- CEVA Logistics

- Aramex

- Almajdouie Logistics

- Bahri Logistics

- Al Jabr Logistics

- SAL Logistics Services

- Mosolf Logistics Saudi Arabia

- Hellmann Worldwide Logistics

- Expeditors International

- Nippon Express

- RSA Cold Chain

Key Target Audience

- Logistics and supply chain companies

- Food and beverage manufacturers

- Pharmaceutical and biotechnology companies

- Supermarket and retail chains

- Cold storage infrastructure developers

- E-commerce grocery companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Researchers identify core variables influencing the KSA Cold Chain Logistics market including refrigerated infrastructure capacity, transportation networks, food import volumes, pharmaceutical logistics demand, and government logistics policies shaping supply chain operations.

Step 2: Market Analysis and Construction

Market size and structure are analyzed using logistics industry datasets, government trade statistics, and infrastructure capacity data to construct a comprehensive framework representing cold chain logistics activities across storage, transport, and distribution.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, logistics operators, and supply chain professionals provide insights validating market assumptions, infrastructure capacity trends, operational challenges, and technological developments shaping cold chain logistics operations.

Step 4: Research Synthesis and Final Output

Data from multiple sources is synthesized to generate a structured analysis of market size, segmentation patterns, competitive dynamics, operational challenges, and emerging opportunities shaping the KSA Cold Chain Logistics market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of Food Retail and Supermarket Chains Increasing Refrigerated Logistics Demand

Growth in Pharmaceutical and Biopharmaceutical Distribution Requiring Temperature-Controlled Transport

Rising Imports of Perishable Food Products Strengthening Cold Storage Infrastructure - Market Challenges

High Capital Investment Required for Cold Storage Infrastructure Development

Energy Consumption and Operational Cost Pressures in Refrigerated Facilities

Limited Skilled Workforce for Managing Advanced Cold Chain Systems - Market Opportunities

Development of Large-Scale Cold Logistics Hubs Supporting Food Security Initiatives

Expansion of E-commerce Grocery and Online Food Delivery Requiring Cold Distribution

Networks

Adoption of Smart Temperature Monitoring and IoT-Enabled Cold Chain Systems - Trends

Integration of IoT-Based Temperature Monitoring in Cold Logistics Operations

Growth of Automated Cold Storage Warehouses and High-Density Refrigeration Facilities

Increasing Investment in Sustainable and Energy-Efficient Refrigeration Technologies - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Warehousing Facilities

Refrigerated Transportation Fleet

Temperature Monitoring & Tracking Systems

Blast Freezing and Quick Freezing Systems

Cold Storage Distribution Centers - By Platform Type (In Value%)

Road-Based Refrigerated Transport

Air Cargo Cold Chain Logistics

Seaport Cold Storage Logistics

Integrated Multimodal Cold Chain Systems

Urban Last-Mile Refrigerated Delivery - By Fitment Type (In Value%)

Built-in Refrigerated Truck Bodies

Containerized Reefer Units

Modular Cold Storage Installations

Portable Refrigeration Systems

Integrated Cold Chain Logistics Systems - By EndUser Segment (In Value%)

Food and Beverage Producers

Pharmaceutical and Biotech Companies

Retail and Supermarket Chains

- Market Share Analysis

- CrossComparison Parameters (Cold Storage Capacity, Refrigerated Fleet Size, Temperature Monitoring Technology, Geographic Coverage, EndUser Industry Focus)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Agility Logistics

GWC Logistics

Almarai Logistics

NAQEL Express

SAL Logistics Services

Bahri Logistics

Almajdouie Logistics

Al Jabr Logistics

Mosolf Logistics Saudi Arabia

CEVA Logistics

DHL Supply Chain

Kuehne + Nagel

DB Schenker

Aramex Logistics

RSA Cold Chain

- Food Processing Companies Expanding Cold Storage Capacity to Support National Food Security Goals

- Pharmaceutical Distributors Increasing Demand for Temperature-Controlled Transportation Networks

- Modern Retail Chains Requiring Advanced Refrigerated Distribution Systems for Fresh Produce

- E-commerce Grocery Platforms Driving Demand for Urban Refrigerated Last-Mile Delivery

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now