Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the KSA Diagnostic Labs market is valued at approximately USD ~ billion, supported by rising demand for clinical diagnostics, preventive screening programs, and expanding hospital infrastructure across the healthcare ecosystem. Increased prevalence of chronic diseases such as diabetes and cardiovascular disorders is driving demand for laboratory testing services. Government healthcare modernization initiatives under national healthcare transformation strategies further expand diagnostic capacity by supporting investments in laboratory infrastructure, advanced pathology technologies, and digital laboratory information systems across public and private healthcare providers.

Major urban healthcare hubs such as Riyadh, Jeddah, and Dammam dominate the diagnostic laboratory landscape due to their concentration of tertiary hospitals, private diagnostic chains, and specialized medical centers. These cities host large populations, advanced hospital networks, and major healthcare investments that support higher volumes of diagnostic testing. Expansion of private healthcare facilities and growing medical tourism activity also contribute to diagnostic testing demand, reinforcing the dominance of metropolitan healthcare ecosystems within the KSA diagnostic laboratory services market.

Market Segmentation

Market Segmentation

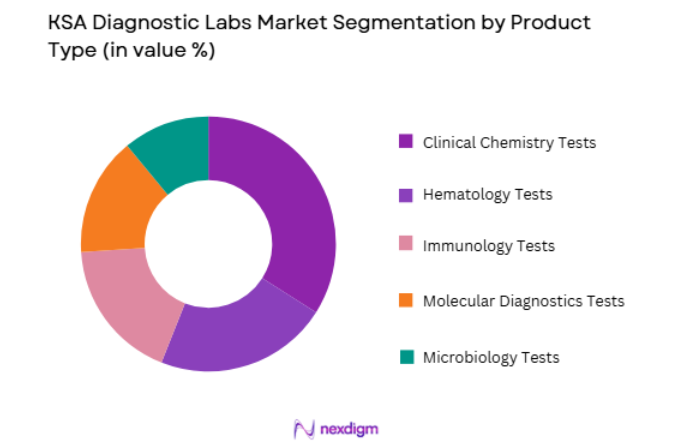

By Product Type

KSA Diagnostic Labs market is segmented by product type into clinical chemistry tests, microbiology tests, hematology tests, immunology tests, and molecular diagnostics tests. Recently, clinical chemistry tests has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Clinical chemistry diagnostics form the backbone of routine healthcare screening programs conducted across hospitals and outpatient clinics. High prevalence of metabolic disorders including diabetes and kidney disease increases demand for blood chemistry analysis. Government preventive health initiatives promote regular testing of glucose, cholesterol, and liver markers, which further increases clinical chemistry testing volumes across diagnostic laboratories nationwide.

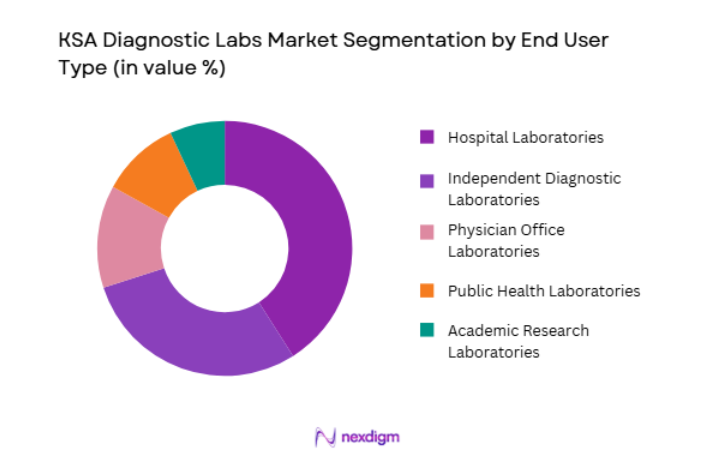

By End User

KSA Diagnostic Labs market is segmented by end user into hospital laboratories, independent diagnostic laboratories, physician office laboratories, academic research laboratories, and public health laboratories. Recently, hospital laboratories has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Hospitals perform large volumes of diagnostic testing linked to inpatient care, emergency services, surgical procedures, and chronic disease management. Large tertiary hospitals maintain fully integrated diagnostic laboratories capable of performing complex tests. Strong patient inflow and integration with hospital information systems support continuous diagnostic demand.

Competitive Landscape

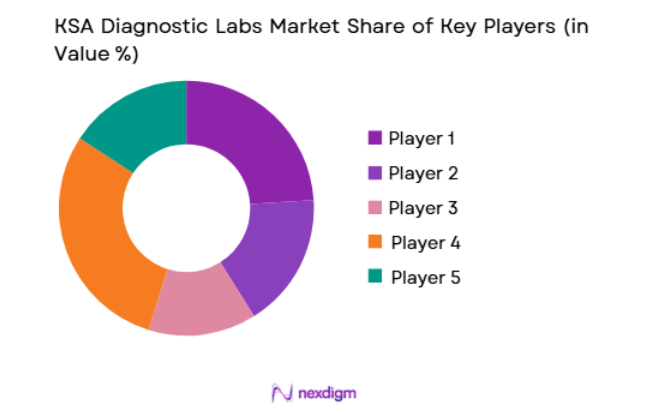

The KSA Diagnostic Labs market is moderately consolidated, with a mix of multinational laboratory service providers and strong domestic diagnostic chains. Large healthcare groups dominate urban diagnostic infrastructure by integrating laboratory services within hospital networks. Private diagnostic laboratory chains continue expanding through partnerships, acquisitions, and regional laboratory networks. Technology adoption including automated analyzers, digital pathology systems, and molecular diagnostic platforms enables competitive differentiation among leading players operating across the Saudi diagnostic ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Laboratory Network Size |

| Al Borg Diagnostics | 1998 | Jeddah | ~ | ~ | ~ | ~ | ~ |

| Al Mokhtabar Laboratories | 2003 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Dr. Sulaiman Al Habib Medical Group | 1995 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Synlab Group | 1998 | Munich | ~ | ~ | ~ | ~ | ~ |

| Quest Diagnostics | 1967 | New Jersey | ~ | ~ | ~ | ~ | ~ |

KSA Diagnostic Labs Market Analysis

Growth Drivers

Expansion of Preventive Healthcare Screening Programs Across Saudi Arabia

Preventive healthcare screening programs significantly expand diagnostic testing demand across Saudi Arabia because early disease detection initiatives require large volumes of laboratory analysis across national healthcare systems. Government healthcare authorities increasingly prioritize population health screening to identify chronic diseases early and reduce long term healthcare expenditure associated with advanced disease treatment. Nationwide screening campaigns target conditions including diabetes cardiovascular disease cancer and kidney disorders that require routine laboratory testing procedures. Large public hospitals and private diagnostic laboratories therefore process millions of blood tests pathology examinations and biomarker screenings annually across urban healthcare centers. Growing health awareness among citizens also encourages individuals to undergo voluntary health checkups which increases diagnostic laboratory utilization rates. Corporate wellness programs implemented by major employers further promote routine laboratory testing through annual employee health assessments conducted by diagnostic laboratories nationwide. Insurance providers increasingly reimburse preventive diagnostic procedures which lowers financial barriers for patients seeking regular medical testing services. Hospitals and diagnostic chains therefore expand laboratory capacity including automated analyzers sample processing systems and digital reporting infrastructure to handle growing testing volumes. Healthcare modernization programs encourage adoption of advanced laboratory technologies capable of processing large numbers of diagnostic tests efficiently while maintaining high clinical accuracy. Rising prevalence of lifestyle diseases including obesity hypertension and metabolic disorders further strengthens long term demand for routine laboratory diagnostics services.

Rapid Expansion of Private Healthcare Infrastructure and Diagnostic Laboratory Chains

Rapid expansion of private healthcare infrastructure across Saudi Arabia significantly drives growth of the diagnostic laboratory services market because modern hospitals depend heavily on laboratory diagnostics to support patient treatment pathways. Large healthcare groups continue investing in advanced hospitals specialty clinics and outpatient care centers that require integrated laboratory facilities capable of conducting thousands of diagnostic tests daily. Private diagnostic laboratory chains expand networks by establishing collection centers and regional testing laboratories across major cities and emerging healthcare regions. This expansion improves patient access to laboratory testing services and reduces turnaround time for medical reports which increases overall testing volumes nationwide. Healthcare providers adopt automated diagnostic platforms including clinical chemistry analyzers hematology analyzers and molecular diagnostic instruments to enhance laboratory productivity and accuracy. Private healthcare providers also collaborate with international diagnostic technology companies to introduce advanced testing solutions including genetic testing infectious disease panels and precision medicine diagnostics. Increasing health insurance penetration encourages patients to seek laboratory testing services through private diagnostic laboratories integrated within hospital ecosystems. Urban population growth and rising middle class income levels increase utilization of private healthcare services including laboratory diagnostics. Healthcare investors therefore allocate capital toward expanding laboratory networks establishing new pathology centers and upgrading diagnostic technologies. The continued development of large hospital networks and specialized medical centers ensures sustained demand for advanced diagnostic laboratory services across the national healthcare landscape.

Market Challenges

High Capital Investment Requirements for Advanced Laboratory Technologies

High capital investment requirements for advanced laboratory technologies create a significant challenge for the KSA diagnostic laboratory services market because modern diagnostic testing increasingly depends on expensive automated equipment and specialized laboratory infrastructure. Diagnostic laboratories must invest heavily in automated analyzers molecular diagnostic instruments digital pathology systems and advanced laboratory information management software to maintain clinical accuracy and operational efficiency. These technologies require substantial financial resources for procurement installation maintenance and technical support. Smaller diagnostic laboratories often struggle to compete with large healthcare groups that possess stronger financial capacity to invest in advanced diagnostic technologies. Laboratory equipment also requires regular calibration servicing and replacement which increases long term operational expenditure for diagnostic service providers. Skilled laboratory technicians and specialized pathologists must be recruited and trained to operate advanced diagnostic systems effectively. Workforce training programs and certification requirements further increase operational costs for laboratories adopting sophisticated diagnostic technologies. Healthcare regulators also impose strict quality control standards requiring laboratories to maintain compliance with accreditation frameworks and laboratory testing guidelines. Meeting these regulatory requirements requires additional investments in quality management systems proficiency testing and laboratory audits. Financial pressure associated with capital intensive diagnostic technologies therefore limits expansion opportunities for smaller laboratories and creates barriers for new entrants attempting to establish diagnostic services within competitive healthcare markets.

Regulatory Compliance Complexity and Laboratory Accreditation Requirements

Regulatory compliance complexity presents a significant operational challenge for diagnostic laboratories operating within Saudi Arabia because laboratory services must comply with multiple healthcare regulatory frameworks governing clinical testing quality safety and patient data management. Healthcare regulators enforce strict standards covering laboratory equipment validation diagnostic test accuracy sample handling procedures and medical reporting protocols. Diagnostic laboratories must obtain accreditation from recognized healthcare quality authorities which requires continuous compliance monitoring documentation management and quality assurance processes. Accreditation audits conducted by regulatory bodies evaluate laboratory infrastructure technical procedures staff qualifications and diagnostic reporting accuracy. Maintaining accreditation therefore requires continuous investment in laboratory quality management systems and staff training programs. Laboratories must also comply with regulations governing medical device approvals diagnostic reagent standards and clinical laboratory operations. Implementation of electronic laboratory information systems must align with national data privacy and healthcare information security regulations which adds technical complexity to digital transformation initiatives. International diagnostic companies operating within Saudi Arabia must also align global laboratory standards with local regulatory frameworks. Compliance costs therefore increase operational burdens particularly for independent diagnostic laboratories with limited administrative resources. The complexity of regulatory frameworks can delay laboratory expansion projects and introduction of new diagnostic technologies which slows innovation across the national diagnostic services ecosystem.

Opportunities

Expansion of Molecular Diagnostics and Genetic Testing Services

Expansion of molecular diagnostics and genetic testing services presents a major opportunity for the KSA diagnostic laboratories market because precision medicine and advanced disease detection technologies are becoming increasingly important within modern healthcare systems. Molecular diagnostic tests enable early detection of infectious diseases genetic disorders and cancer biomarkers which significantly improves patient treatment outcomes. Hospitals and research centers increasingly adopt polymerase chain reaction testing genomic sequencing and biomarker analysis technologies to support personalized medical treatment strategies. Government healthcare transformation initiatives encourage adoption of precision medicine approaches within national healthcare infrastructure which expands demand for advanced diagnostic testing capabilities. Private diagnostic laboratory chains therefore invest in specialized molecular diagnostic laboratories equipped with genomic testing instruments and advanced laboratory automation platforms. Academic medical centers collaborate with biotechnology companies to introduce new diagnostic panels targeting hereditary diseases and cancer mutations. Increasing prevalence of complex chronic diseases strengthens demand for advanced diagnostic tools capable of providing highly accurate molecular level disease insights. Pharmaceutical companies conducting clinical trials also require specialized molecular diagnostic services for biomarker research and patient selection processes. Expansion of biotechnology research activities within Saudi Arabia further stimulates development of advanced diagnostic laboratory capabilities. Growing physician awareness regarding the clinical benefits of molecular diagnostics therefore supports long term expansion of genetic and precision medicine laboratory services across the national healthcare ecosystem.

Digital Transformation and Automation of Diagnostic Laboratory Operations

Digital transformation and laboratory automation represent a significant growth opportunity for diagnostic laboratories across Saudi Arabia because digital healthcare technologies improve laboratory efficiency testing accuracy and operational scalability. Modern laboratories increasingly implement laboratory information management systems automated sample processing robotics and digital pathology imaging platforms that streamline diagnostic workflows. These technologies significantly reduce manual processing errors improve turnaround times and enable laboratories to process larger volumes of diagnostic samples daily. Integration of laboratory information systems with hospital electronic health records enhances data sharing between physicians and diagnostic laboratories which improves clinical decision making. Telepathology and digital diagnostic reporting platforms allow pathologists to remotely analyze test results and collaborate with specialists located in different regions. Healthcare providers therefore adopt cloud based laboratory data management systems capable of handling large volumes of patient diagnostic data securely. Artificial intelligence algorithms also assist laboratories in analyzing pathology images and identifying disease patterns within large diagnostic datasets. Digital transformation reduces operational costs while enabling laboratories to scale services across multiple geographic locations. Expansion of smart healthcare infrastructure under national healthcare modernization initiatives therefore accelerates adoption of digital laboratory technologies across hospital networks and independent diagnostic laboratory chains operating within Saudi Arabia.

Future Outlook

The KSA Diagnostic Labs market is expected to experience steady expansion as healthcare modernization initiatives continue strengthening national diagnostic infrastructure. Increasing adoption of molecular diagnostics, digital pathology systems, and automated laboratory platforms will enhance testing capacity and diagnostic accuracy. Expanding private healthcare investments and national screening programs will further stimulate demand for laboratory services. Growing awareness regarding preventive healthcare and early disease detection will continue supporting sustained growth of diagnostic testing volumes across the country.

Major Players

- Al Borg Diagnostics

- AlMokhtabar Laboratories

- Dr. Sulaiman Al Habib Medical Group

- Saudi German Health

- Synlab Group

- Quest Diagnostics

- Abbott Laboratories

- Roche Diagnostics

- Siemens Healthineers

- Unilabs

- Cerba Healthcare

- Mayo Clinic Laboratories

- Al Hammadi Medical Group

- Bupa Arabia Diagnostic Services

- Al Mouwasat Medical Services

Key Target Audience

- Hospital networks

- Diagnostic laboratory chains

- Biotechnology companies

- Medical device manufacturers

- Healthcare technology companies

- Pharmaceutical companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying critical variables influencing the KSA Diagnostic Labs market including diagnostic test demand, healthcare infrastructure development, disease prevalence patterns, laboratory technology adoption, and regulatory frameworks affecting diagnostic service delivery.

Step 2: Market Analysis and Construction

Market structure is developed by analyzing diagnostic testing volumes, hospital laboratory capacity, private diagnostic chains, and national healthcare investment programs. Data is collected from healthcare authorities, industry databases, and diagnostic service providers.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings are validated through consultations with laboratory managers, healthcare policy specialists, medical technology suppliers, and healthcare economists to ensure data accuracy and realistic market interpretation.

Step 4: Research Synthesis and Final Output

Validated insights are integrated into a structured analytical framework that includes market segmentation, competitive analysis, growth drivers, and future outlook to provide a comprehensive assessment of the KSA Diagnostic Labs market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising prevalence of chronic diseases increasing demand for diagnostic testing

Expansion of private healthcare facilities and diagnostic laboratory chains

Government healthcare investments under Vision 2030 strengthening diagnostic infrastructure - Market Challenges

High capital investment required for advanced diagnostic equipment

Shortage of skilled laboratory technicians and diagnostic specialists

Regulatory compliance requirements for laboratory accreditation and quality standards - Market Opportunities

Expansion of diagnostic laboratory networks in tier two cities

Growth of home sample collection and digital diagnostic reporting services

Adoption of AI powered diagnostic analysis and laboratory automation technologies - Trends

Integration of laboratory information management systems for digital diagnostics

Growing demand for genomic and precision diagnostic testing - Government Regulations

Laboratory accreditation and licensing under the Saudi Ministry of Health

Quality and compliance standards governed by the Saudi Food and Drug Authority

Regulations governing diagnostic laboratory operations and patient data protection - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Pathology Testing Services

Radiology and Imaging Diagnostics

Molecular and Genomic Diagnostics

Point of Care Diagnostic Testing

Preventive Health Screening Services - By Platform Type (In Value%)

Standalone Diagnostic Laboratory Networks

Hospital Based Diagnostic Laboratories

Chain Diagnostic Laboratory Platforms

Home Sample Collection Diagnostic Platforms

Digital Diagnostic Reporting Platforms - By Fitment Type (In Value%)

Central Reference Laboratories

Regional Processing Laboratories

Collection and Sample Processing Centers

Mobile Diagnostic Testing Units - By End User Segment (In Value%)

Public Hospitals and Government Healthcare Providers

Private Hospitals and Specialty Clinics

Corporate Health Screening Programs

- Market Share Analysis

- Cross Comparison Parameters (Testing Portfolio Range, Diagnostic Technology Integration, Turnaround Time for Test Results, Laboratory Network Coverage, Digital Reporting Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Al Borg Diagnostics

Dr Sulaiman Al Habib Medical Laboratories

Mouwasat Medical Services Laboratories

Dallah Healthcare Laboratories

Saudi German Hospital Laboratories

Al Hammadi Hospital Laboratories

King Faisal Specialist Hospital Laboratories

National Guard Health Affairs Laboratories

Al Mana Laboratories

Al Faisaliah Medical Systems

Gulf Specialized Hospital Laboratories

International Medical Center Laboratories

Al Zahra Hospital Laboratories

Riyadh Care Hospital Laboratories

Badr Al Samaa Laboratories

- Government hospitals expanding in house diagnostic laboratories

- Private hospital groups investing in advanced diagnostic and imaging centers

- Corporate organizations adopting preventive health screening programs

- Insurance providers integrating diagnostic testing within healthcare coverage programs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now