Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Saudi Arabia’s digital health sector has emerged as a strategic component of the national healthcare transformation agenda, supported by government investments in health information systems, telemedicine, and electronic medical record platforms. Based on a recent historical assessment, the KSA digital health market was valued at approximately USD ~ billion according to healthcare technology statistics compiled by the Ministry of Health and international health IT industry databases. Market growth is driven by hospital digitization, remote care services, health data integration initiatives, and expanding adoption of digital patient management systems.

Riyadh, Jeddah, and Dammam represent the primary digital health adoption centers due to the concentration of large tertiary hospitals, digital health innovation hubs, and government medical cities deploying integrated healthcare technology systems. These metropolitan healthcare ecosystems host leading hospitals, telemedicine providers, and digital health startups implementing advanced health platforms. Strong telecommunications infrastructure, widespread smartphone adoption, and government-backed health technology programs further support digital healthcare deployment across these major Saudi urban healthcare clusters.

Market Segmentation

By Product Type

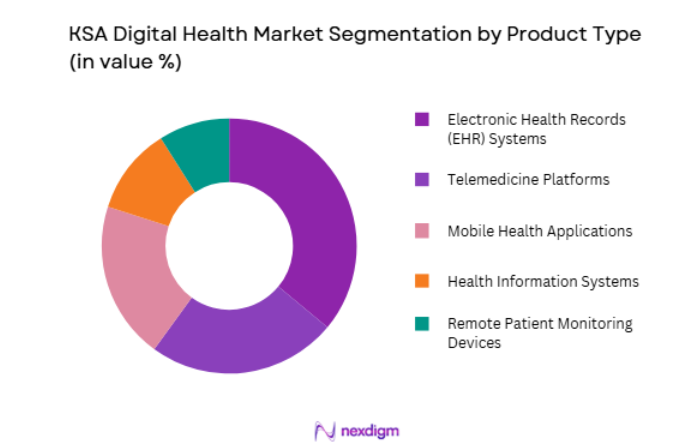

KSA Digital Health market is segmented by product type into Telemedicine Platforms, Electronic Health Records (EHR) Systems, Mobile Health Applications, Health Information Systems, and Remote Patient Monitoring Devices. Recently, Electronic Health Records (EHR) Systems has a dominant market share due to factors such as national hospital digitization initiatives, centralized patient data management requirements, and strong government support for health information interoperability across healthcare institutions. Hospitals across Saudi Arabia increasingly implement EHR systems to streamline patient data access, improve treatment coordination, and enhance clinical documentation efficiency. Government healthcare modernization programs emphasize integrated digital records across public hospitals, specialty medical centers, and primary healthcare clinics. The rapid expansion of private healthcare providers further accelerates demand for EHR platforms to manage growing patient volumes and digital healthcare workflows.

By End User

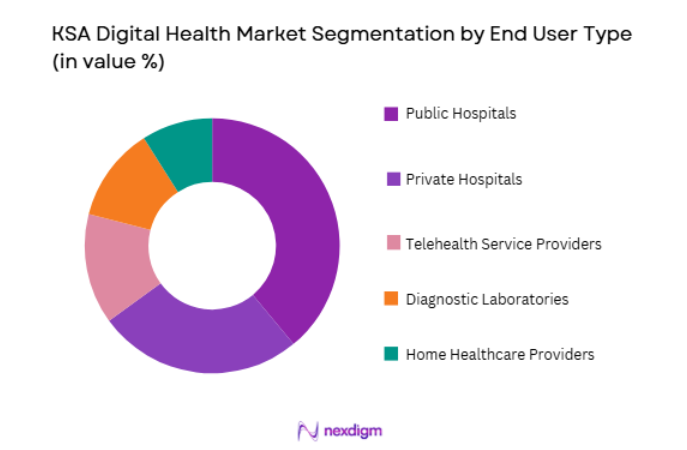

KSA Digital Health market is segmented by end user into Public Hospitals, Private Hospitals, Telehealth Service Providers, Diagnostic Laboratories, and Home Healthcare Providers. Recently, Public Hospitals has a dominant market share due to factors such as large-scale government healthcare digitization programs, centralized medical information infrastructure, and national digital health initiatives implemented across public healthcare institutions. Government hospitals form the backbone of the Saudi healthcare system and therefore lead the adoption of integrated digital healthcare platforms designed to improve patient care management. Large public hospitals implement telemedicine services, digital medical records, and health analytics platforms to enhance operational efficiency and clinical decision support. National digital health initiatives promote interoperability between hospitals and regional healthcare networks, further strengthening technology adoption within government healthcare institutions.

Competitive Landscape

The KSA digital health market is characterized by collaboration between international healthcare technology companies, regional digital health providers, and emerging health technology startups. Large global health IT companies provide electronic health record systems, hospital information platforms, and advanced analytics technologies deployed across Saudi hospitals. Local digital health companies focus on telemedicine services, mobile health applications, and remote patient monitoring platforms tailored for regional healthcare needs. Strategic partnerships between hospitals, technology firms, and government authorities support nationwide digital health adoption.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Digital Health Platform Integration |

| Cerner Corporation | 1979 | United States | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Netherlands | ~ | ~ | ~ | ~ | ~ |

| GE Healthcare | 1892 | United States | ~ | ~ | ~ | ~ | ~ |

| Vezeeta | 2012 | Egypt | ~ | ~ | ~ | ~ | ~ |

| Altibbi | 2011 | Jordan | ~ | ~ | ~ | ~ | ~ |

KSA Digital Health Market Analysis

Growth Drivers

Government-Led Healthcare Digital Transformation Under Vision 2030

Saudi Arabia’s Vision 2030 healthcare transformation program is significantly accelerating digital health adoption across hospitals, clinics, and national healthcare networks. Government authorities are investing heavily in digital infrastructure designed to integrate patient data, improve clinical workflows, and enhance healthcare accessibility throughout the country. Large national programs promote implementation of electronic medical records, telemedicine platforms, and centralized healthcare information systems across public healthcare institutions. These initiatives aim to create a unified national health data ecosystem capable of supporting efficient healthcare delivery and population health management. Public hospitals and medical cities are increasingly deploying integrated digital health platforms to improve patient record management, diagnostic reporting, and clinical decision support capabilities. Digital transformation initiatives also support remote consultation services that allow patients in remote regions to access specialist healthcare without traveling to major cities. Health information exchange programs enable interoperability between hospitals, laboratories, and healthcare authorities, allowing real-time sharing of clinical information across healthcare networks. Investments in digital hospital infrastructure further strengthen demand for advanced health IT systems, analytics platforms, and connected medical technologies.

Rising Demand for Telemedicine and Remote Healthcare Services

Increasing demand for remote healthcare services is driving rapid expansion of telemedicine platforms and digital health solutions throughout Saudi Arabia. Patients are increasingly using telehealth services for medical consultations, follow-up appointments, and chronic disease monitoring, reducing the need for physical hospital visits. Telemedicine platforms allow healthcare providers to deliver medical services through video consultations, mobile health applications, and remote diagnostic tools. These digital services improve healthcare accessibility for patients living in remote regions where specialized medical services may not be readily available. Remote healthcare technologies also support efficient management of chronic diseases by enabling continuous monitoring of patient health conditions through connected medical devices and mobile health platforms. Hospitals and clinics are integrating telemedicine systems into their healthcare delivery models to improve operational efficiency and reduce patient waiting times. Healthcare providers also use digital consultation platforms to expand service reach beyond physical hospital locations. Increased smartphone penetration and strong national telecommunications infrastructure further support the widespread adoption of mobile health applications and digital health platforms.

Market Challenges

Healthcare Data Privacy Regulations and Cybersecurity Risks

Rapid expansion of digital health technologies introduces significant challenges related to healthcare data protection and cybersecurity management. Digital health platforms store large volumes of sensitive patient information including medical histories, diagnostic reports, and treatment records. Protecting this data from cyber threats requires strong cybersecurity infrastructure and strict compliance with healthcare data privacy regulations. Healthcare institutions must invest heavily in cybersecurity systems to safeguard digital health platforms against unauthorized access, data breaches, and ransomware attacks. Compliance with national data protection laws also requires healthcare providers to implement strict data governance policies and secure information storage protocols. Managing cybersecurity risks becomes increasingly complex as hospitals adopt interconnected digital health platforms that integrate medical devices, hospital information systems, and patient portals. Healthcare organizations must continuously update cybersecurity strategies to address emerging digital threats targeting healthcare infrastructure. Lack of specialized cybersecurity expertise within healthcare institutions can further increase vulnerability to cyberattacks.

Integration Challenges Between Legacy Healthcare Systems and Modern Digital Platforms

Many healthcare institutions in Saudi Arabia operate legacy hospital information systems that were not originally designed for modern digital health integration. Implementing new digital platforms within existing healthcare infrastructure can therefore create compatibility and interoperability challenges. Hospitals often face difficulties integrating electronic health records, telemedicine systems, and health analytics platforms with older clinical information systems. Lack of standardized data exchange protocols can further complicate information sharing between healthcare facilities and digital health platforms. Healthcare providers must invest significant resources in system upgrades and data migration processes to ensure seamless digital integration. Staff training is also required to enable healthcare professionals to effectively operate new digital healthcare technologies. Technical integration issues may temporarily disrupt clinical workflows during digital transformation initiatives. Healthcare institutions must carefully plan technology upgrades to ensure smooth transition from legacy systems to modern digital healthcare platforms.

Opportunities

Expansion of Artificial Intelligence Applications in Clinical Decision Support Systems

Artificial intelligence technologies are creating major opportunities for innovation within the KSA digital health ecosystem. AI-powered healthcare platforms are increasingly being used to analyze medical images, predict disease progression, and assist physicians in clinical decision-making processes. Hospitals can integrate AI algorithms into diagnostic imaging systems to improve accuracy in detecting conditions such as cancer, cardiovascular diseases, and neurological disorders. AI-driven analytics platforms also help healthcare providers identify population health trends and optimize treatment strategies. Predictive analytics technologies enable hospitals to monitor patient health indicators and identify potential medical risks before conditions become critical. AI-enabled virtual assistants can also support patient engagement by providing automated health guidance and appointment scheduling services. Integration of artificial intelligence within digital health platforms improves healthcare efficiency while supporting personalized patient care.

Development of Smart Hospitals and Connected Healthcare Ecosystems

Saudi Arabia is actively investing in the development of smart hospitals equipped with connected medical devices, digital patient management systems, and advanced healthcare analytics platforms. Smart hospital infrastructure integrates medical equipment, patient monitoring systems, and digital information platforms into unified healthcare technology ecosystems. These systems enable real-time patient monitoring, automated clinical documentation, and data-driven healthcare decision-making. Hospitals implementing smart healthcare technologies can improve operational efficiency, reduce medical errors, and enhance patient safety. Connected healthcare ecosystems also support seamless data exchange between hospitals, laboratories, pharmacies, and public health authorities. Advanced digital infrastructure allows healthcare providers to deliver personalized treatment plans based on integrated patient data. As Saudi Arabia continues building technologically advanced healthcare facilities, demand for integrated digital health solutions will expand significantly.

Future Outlook

The KSA digital health market is expected to expand significantly over the next five years as healthcare providers continue investing in digital infrastructure and smart healthcare technologies. Telemedicine platforms, remote patient monitoring systems, and integrated electronic health records will play a central role in future healthcare delivery. Government digital health initiatives and expanding private healthcare investment are likely to accelerate technology adoption.

Major Players

- Cerner Corporation

- Philips Healthcare

- GE Healthcare

- Vezeeta

- Altibbi

- Siemens Healthineers

- Epic Systems

- Oracle Health

- IBM Watson Health

- Teladoc Health

- Babylon Health

- Health Catalyst

- Allscripts Healthcare Solutions

- Athenahealth

- Qualcomm Life

Key Target Audience

- Hospitals and healthcare providers

- Digital health technology companies

- Telemedicine service providers

- Medical device manufacturers

- Healthcare IT platform developers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying critical variables influencing the KSA digital health market including healthcare digitization levels, telemedicine adoption rates, regulatory frameworks, and technology infrastructure development.

Step 2: Market Analysis and Construction

Comprehensive market modeling is conducted using healthcare technology adoption data, hospital digitization programs, and digital health service deployment statistics. Market segmentation is constructed by evaluating product categories, healthcare provider adoption patterns, and technology infrastructure across healthcare institutions.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions are validated through consultations with healthcare technology experts, hospital administrators, and digital health platform developers operating within the Saudi healthcare ecosystem. Expert insights help refine adoption trends and validate key market growth drivers.

Step 4: Research Synthesis and Final Output

The final research framework integrates quantitative healthcare technology data with qualitative insights obtained from industry stakeholders. The synthesis process ensures that the final report reflects current digital health trends, regulatory developments, and healthcare infrastructure modernization initiatives shaping the Saudi healthcare market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government initiatives under Vision 2030 promoting digital transformation in healthcare

Increasing smartphone and internet penetration enabling digital healthcare services

Rising demand for remote healthcare monitoring and teleconsultation services - Market Challenges

Data privacy and cybersecurity risks in digital health systems

Integration complexity between legacy hospital systems and modern digital platforms

Limited digital literacy among certain population segments - Market Opportunities

Expansion of AI powered diagnostic platforms and predictive healthcare analytics

Growth of telemedicine services connecting patients in remote regions

Development of integrated national health data platforms - Trends

Adoption of wearable health monitoring devices integrated with digital platforms

Increasing use of artificial intelligence in clinical diagnostics and healthcare analytics - Government Regulations

Digital health initiatives under the Saudi Vision 2030 healthcare transformation plan

Health data protection and cybersecurity regulations

Licensing frameworks for telemedicine and digital healthcare providers - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Telemedicine and Virtual Consultation Platforms

Electronic Health Record Systems

Remote Patient Monitoring Solutions

Mobile Health Applications

AI Powered Clinical Decision Support Systems - By Platform Type (In Value%)

Hospital Integrated Digital Health Platforms

Cloud Based Health Management Platforms

Mobile Health Platforms

Government Digital Health Platforms

Wearable Device Integrated Health Platforms - By Fitment Type (In Value%)

Standalone Digital Health Applications

Integrated Hospital Information Systems

Cloud Hosted Digital Health Platforms

AI Enabled Clinical Analytics Systems - By End User Segment (In Value%)

Hospitals and Healthcare Providers

Diagnostic and Specialty Medical Centers

Individual Patients and Healthcare Consumers

- Market Share Analysis

- Cross Comparison Parameters (Platform Functionality, Data Security Compliance, Integration with Hospital Systems, AI and Analytics Capability, User Interface Accessibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Cerner Corporation

Epic Systems

Philips Healthcare

Siemens Healthineers

Oracle Health

IBM Watson Health

GE HealthCare

Medtronic Digital Health

Altibbi

Vezeeta

Seha Virtual Hospital

Healthigo

Okadoc

Doctify

Tawuniya Digital Health

- Hospitals implementing digital platforms for patient management and clinical data integration

- Diagnostic centers adopting AI based digital diagnostic systems

- Patients increasingly using mobile health applications for remote health monitoring

- Insurance providers integrating digital platforms for claims management and preventive healthcare

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now