Download PDF

Download PDF Download PDF

Download PDFMarket Overview

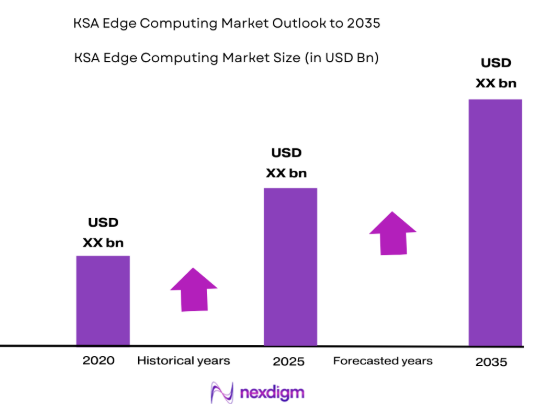

Based on a recent historical assessment, the KSA edge computing market reached approximately USD ~ billion, driven by rapid deployment of distributed data processing infrastructure across telecommunications, energy, and public sector digital platforms. Investments in localized data processing to support latency-sensitive applications such as video analytics, automation, and AI inference accelerated adoption. Expansion of 5G networks and national digital transformation initiatives further stimulated demand for micro data centers, edge servers, and intelligent gateways across enterprise and industrial environments.

Riyadh and NEOM dominate deployment activity due to concentration of hyperscale data initiatives, smart city programs, and advanced telecom infrastructure investments supported by national digital strategies. Eastern Province industrial clusters, including Dhahran and Jubail, lead industrial edge adoption because of oil, gas, and petrochemical automation requirements requiring real-time analytics near operations. Jeddah shows strong logistics and port-centric edge deployments driven by smart mobility, trade digitization, and urban infrastructure modernization priorities.

Market Segmentation

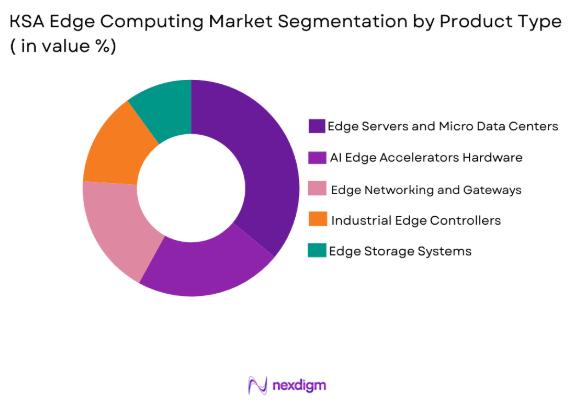

By Product Type

KSA Edge Computing market is segmented by product type into edge servers and micro data centers, edge AI accelerators and processing units, edge networking and gateways, industrial edge controllers, and edge storage systems. Recently, edge servers and micro data centers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

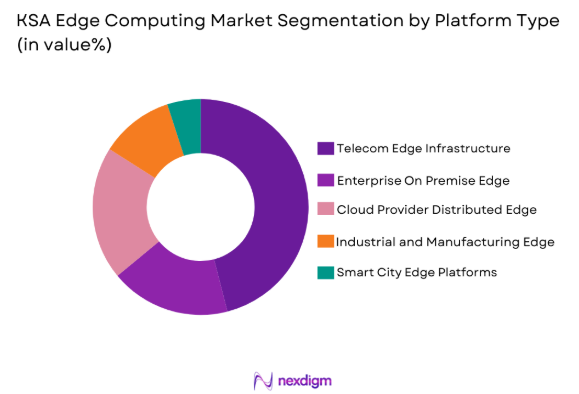

By Platform Type

By Platform Type: KSA Edge Computing market is segmented by product type into telecom edge infrastructure, enterprise on premise edge, cloud provider distributed edge, industrial and manufacturing edge, and smart city edge platforms. Recently, telecom edge infrastructure has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

Competitive Landscape

The KSA edge computing market shows moderate consolidation with telecom operators, global IT infrastructure vendors, and industrial technology providers shaping competitive dynamics. Telecom companies leverage nationwide network assets to deploy distributed edge platforms, while global hardware vendors supply micro data center and edge server solutions through local partnerships. Government-aligned digital firms and sovereign technology initiatives further influence procurement and localization requirements across critical infrastructure deployments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Edge Deployment Model |

| Saudi Telecom Company | 1998 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Mobily | 2004 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Zain Saudi Arabia | 2008 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Aramco Digital | 2023 | Dhahran | ~ | ~ | ~ | ~ | ~ |

| SITE Saudi Information Technology Company | 2017 | Riyadh | ~ | ~ | ~ | ~ | ~ |

KSA Edge Computing Market Analysis

Growth Drivers

5G Network Expansion and Low Latency Application Demand

The rapid expansion of nationwide fifth-generation mobile infrastructure across Saudi Arabia is fundamentally reshaping digital architecture requirements by enabling ultra-low latency connectivity essential for distributed computing deployment across industrial, urban, and enterprise environments. Telecom operators are integrating multi-access edge computing platforms within base station and aggregation layers to support emerging use cases such as autonomous mobility systems, augmented and virtual reality services, smart surveillance analytics, and mission-critical communications that cannot rely on centralized cloud processing. Enterprise digital transformation strategies across sectors including manufacturing, logistics, energy, and public services increasingly depend on real-time analytics and control capabilities located near operational data sources to minimize latency, reduce bandwidth usage, and enhance reliability in critical applications. The proliferation of connected devices and sensors across smart infrastructure ecosystems is generating massive data volumes that require localized processing nodes to ensure efficient data handling and regulatory compliance with national data residency requirements. Government-backed digital infrastructure programs are incentivizing telecom-cloud convergence architectures that embed computing resources into access networks, thereby expanding edge computing footprint nationwide. Hyperscale cloud providers partnering with telecom operators are deploying distributed edge zones to extend cloud capabilities closer to enterprise users, accelerating market penetration. Industrial automation and Industry 4.0 initiatives require deterministic latency and secure localized compute environments, further driving adoption of ruggedized edge systems across factories and energy facilities. Smart city platforms integrating traffic management, surveillance, utilities monitoring, and environmental analytics rely on edge processing to enable real-time decision-making and reduce network congestion. As 5G standalone networks mature, network slicing capabilities enable dedicated low-latency services for enterprises, reinforcing sustained demand for distributed computing infrastructure integrated with telecom networks.

Vision 2035 Digital Transformation and Smart Infrastructure Investments

National economic diversification strategies centered on digital transformation and smart infrastructure development are creating sustained structural demand for distributed computing capabilities across urban development, industrial modernization, and public sector service digitization initiatives. Large-scale smart city projects such as NEOM and other giga-developments are embedding pervasive sensor networks, autonomous systems, intelligent mobility platforms, and real-time environmental monitoring architectures that require extensive edge computing layers to process and act on data locally. Government programs promoting artificial intelligence adoption across healthcare, security, energy, and municipal services are accelerating deployment of AI inference hardware at the network edge to support analytics close to data generation points. Public safety and surveillance modernization initiatives across major cities are integrating high-resolution video analytics platforms dependent on localized processing infrastructure to deliver immediate insights without transmitting massive data volumes to centralized data centers. Industrial diversification policies encouraging advanced manufacturing and digital oilfield transformation are fostering edge deployment across refineries, petrochemical complexes, and industrial zones requiring real-time control and predictive maintenance analytics. Data sovereignty and cybersecurity regulations mandating localized processing and storage of sensitive national and citizen data are reinforcing domestic edge infrastructure deployment rather than reliance on offshore cloud resources. National cloud and sovereign digital infrastructure initiatives are promoting distributed data architectures that extend computing nodes across regions to enhance resilience and reduce latency for government and enterprise services. Digital healthcare and telemedicine programs rely on localized data processing for medical imaging analytics and connected care platforms, contributing to sectoral demand. Logistics and port modernization initiatives across trade hubs such as Jeddah are adopting edge platforms for real-time tracking, automation, and predictive operations management across transport networks. These coordinated public investment programs are establishing long-term structural foundations for sustained expansion of distributed computing infrastructure across the kingdom.

Market Challenges

High Deployment Costs and Distributed Infrastructure Complexity

Establishing distributed computing environments across geographically dispersed industrial sites, telecom networks, and urban infrastructure locations requires substantial capital investment in ruggedized hardware, specialized enclosures, power systems, cooling solutions, and secure connectivity architectures suited for harsh operating conditions. Unlike centralized data centers, edge nodes must be replicated across numerous locations to achieve coverage, significantly increasing cumulative infrastructure expenditure and complicating lifecycle management across heterogeneous deployment environments. Integration of edge systems with legacy operational technology platforms in industrial sectors such as oil, gas, and manufacturing requires customized engineering and interoperability validation, adding to deployment costs and extending implementation timelines. Operational expenditure is also elevated due to maintenance challenges in remote or unmanned environments where skilled technical personnel are limited, necessitating remote management tools and resilient system design. Energy supply constraints and cooling requirements in desert climates further increase infrastructure costs and limit feasible deployment densities in certain locations. Supply chain dependence on imported specialized computing hardware exposes projects to cost volatility and procurement delays, complicating budget planning for large-scale distributed rollouts. Standardization across vendors and platforms remains immature, requiring bespoke integration layers and reducing economies of scale achievable in centralized architectures. Security hardening of numerous distributed nodes against cyber threats requires additional investment in encryption, monitoring, and physical protection mechanisms. These combined factors raise total cost of ownership and can slow enterprise adoption, particularly among organizations lacking large-scale digital infrastructure budgets or operational expertise in distributed computing systems.

Cybersecurity Risks and Data Governance Requirements in Distributed Environments

Edge computing architectures expand the digital attack surface by distributing processing and storage across numerous geographically dispersed nodes, increasing vulnerability exposure compared to centralized cloud or data center environments. Each deployed node represents a potential entry point for unauthorized access, malware injection, or data interception, particularly in industrial or remote settings where physical security controls may be weaker. Ensuring secure communication between edge nodes, core networks, and cloud platforms requires robust encryption, identity management, and continuous monitoring frameworks that increase system complexity and operational overhead. Regulatory requirements governing national data sovereignty and critical infrastructure protection mandate strict compliance controls over where and how sensitive data is processed and stored, placing additional design constraints on distributed computing architectures. Industrial edge deployments integrated with operational technology systems introduce risks of cross-domain cyber threats that could disrupt physical processes in energy, manufacturing, or transportation sectors. Heterogeneous hardware and software stacks across multiple vendors complicate patch management, vulnerability mitigation, and lifecycle security assurance across distributed estates. Limited cybersecurity expertise in industrial and enterprise environments adopting edge solutions can result in configuration gaps and insufficient monitoring, elevating breach risk. Continuous updates and remote management of edge devices require secure orchestration platforms capable of operating across unreliable connectivity conditions common in remote industrial areas. These security and governance challenges necessitate advanced security architectures and ongoing operational investment, potentially slowing adoption among risk-averse sectors handling critical national infrastructure or sensitive data.

Opportunities

Industrial Edge Deployment in Energy and Petrochemical Operations

Saudi Arabia’s extensive oil, gas, and petrochemical infrastructure spanning remote extraction fields, pipelines, refineries, and processing complexes creates substantial demand for localized computing platforms capable of supporting real-time monitoring, automation, and predictive maintenance across distributed operations. Edge systems enable processing of high-frequency sensor and control data directly at production sites, allowing immediate detection of anomalies, equipment failures, or safety risks without reliance on distant data centers. Digital oilfield initiatives integrating advanced analytics, machine learning models, and automated control loops require deterministic low-latency compute environments embedded within operational technology networks, making ruggedized edge platforms essential infrastructure. Harsh environmental conditions in energy facilities necessitate specialized industrial-grade edge hardware capable of operating reliably under temperature extremes, vibration, and dust exposure, creating a differentiated market niche. Integration of private 5G networks across energy sites is further enhancing feasibility of distributed computing deployment by providing secure, high-bandwidth connectivity between sensors, machines, and edge nodes. Predictive maintenance applications processing equipment telemetry locally reduce downtime and maintenance costs while improving operational safety and asset utilization. Remote monitoring and automation enabled by edge computing reduce dependence on on-site personnel in hazardous environments, supporting workforce safety and efficiency objectives. Energy companies are increasingly adopting digital twin models requiring localized simulation and analytics near physical assets, reinforcing edge infrastructure demand. Environmental monitoring and emissions tracking initiatives across energy facilities rely on real-time data processing at source locations to ensure compliance and operational responsiveness. As energy sector digital transformation accelerates under national industrial modernization strategies, edge computing deployments across upstream and downstream operations represent a major sustained market growth opportunity.

Sovereign Edge Cloud and Smart City Infrastructure Platforms

National priorities emphasizing digital sovereignty, data localization, and secure processing of sensitive government and citizen data are driving development of sovereign distributed cloud architectures that incorporate edge computing layers across cities and regions. Smart city ecosystems integrating transportation management, surveillance, utilities optimization, public safety, and environmental monitoring generate continuous real-time data streams requiring localized processing to enable immediate operational responses. Edge platforms embedded within urban infrastructure enable rapid analytics and control functions such as traffic signal optimization, crowd monitoring, emergency response coordination, and infrastructure health assessment without latency associated with centralized processing. Government-backed digital infrastructure programs are encouraging deployment of regional edge zones to support localized service delivery for e-government applications, healthcare systems, and municipal operations. Integration of artificial intelligence inference engines within city-level edge nodes enables advanced video analytics, predictive urban management, and autonomous mobility coordination across urban environments. Sovereign cloud initiatives extending compute resources across regions improve resilience, redundancy, and disaster recovery capabilities for critical public services. Public sector procurement frameworks promoting domestic data processing and storage strengthen demand for locally deployed edge infrastructure integrated with national cloud ecosystems. Smart mobility and autonomous transport pilots in advanced urban developments rely on ultra-low latency compute layers distributed along transportation corridors and intersections. Urban energy and utilities management platforms leveraging IoT sensors depend on localized processing for grid optimization and resource management. As large-scale urban digitization projects expand across multiple Saudi cities, sovereign edge cloud and smart city infrastructure platforms represent a foundational long-term opportunity for distributed computing providers.

Future Outlook

The KSA edge computing market is expected to expand steadily as nationwide 5G standalone deployment, industrial automation, and smart city ecosystems mature. Increasing convergence between telecom networks and cloud platforms will extend distributed computing layers across urban and industrial regions. Government digital sovereignty policies and national infrastructure investments will reinforce domestic edge deployment. Energy, manufacturing, and public sector digitalization initiatives will sustain demand for low-latency localized processing capabilities.

Major Players

- Saudi Telecom Company

- Mobily • Zain Saudi Arabia

- Aramco Digital

- SITE Saudi Information Technology Company

- Hewlett Packard Enterprise

- Dell Technologies

- Cisco Systems

- Nokia • Ericsson

- Huawei

- Schneider Electric

- Vertiv

- Lenovo

- IBM

Key Target Audience

- Telecom Operators

- Oil and Gas Companies

- Industrial Manufacturing Enterprises

- Smart City Authorities

- Cloud Service Providers

- Government and Regulatory Bodies

- Investments and Venture Capitalist Firms

- Logistics and Port Operators

Research Methodology

Step 1: Identification of Key Variables

Key market variables including edge infrastructure deployment scale, sectoral digitalization intensity, telecom network expansion, and industrial automation adoption were identified through secondary research and industry frameworks. Technology architecture trends, regulatory influences, and demand-side drivers across telecom, energy, and public sectors were mapped to define scope and segmentation structure.

Step 2: Market Analysis and Construction

Market sizing and segmentation were constructed using supply-side deployment indicators, vendor presence analysis, and infrastructure investment mapping across telecom and industrial sectors. Value chain assessment incorporated hardware, software, integration, and service components of distributed computing architecture across national deployment programs.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding dominant segments, adoption drivers, and deployment patterns were validated through industry expert perspectives and cross-sector digital infrastructure benchmarks. Vendor capability analysis and sector adoption maturity assessments refined competitive positioning and market dynamics interpretation.

Step 4: Research Synthesis and Final Output

Validated data points and qualitative insights were synthesized into structured market analysis covering segmentation, competitive landscape, and strategic outlook. Consistency checks ensured alignment between national digital initiatives, sectoral demand drivers, and distributed computing adoption patterns across Saudi Arabia.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

5G network expansion enabling low latency applications

Vision 2030 smart city and digital infrastructure programs

Industrial automation and predictive maintenance adoption

Growth of AI and real time analytics workloads

Data localization and sovereignty requirements - Market Challenges

High deployment and integration costs in distributed environments

Power and cooling constraints in remote locations

Limited edge skilled workforce and ecosystem maturity

Cybersecurity risks across distributed nodes

Interoperability issues across vendors and platforms - Market Opportunities

Edge deployment in oilfield and remote energy operations

Private 5G and industrial edge convergence solutions

Sovereign cloud and national edge infrastructure initiatives - Trends

Convergence of telecom and cloud edge architectures

Rise of AI inference at the edge for video and IoT analytics

Containerized and modular micro data center adoption

Integration of edge with private 5G networks

Expansion of managed edge services by operators - Government Regulations & Defense Policy

National data residency and cybersecurity regulations

Smart city digital infrastructure mandates

Critical infrastructure localization policies

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Edge Servers and Micro Data Centers

Edge AI Accelerators and Processing Units

Edge Networking and Gateways

Industrial Edge Controllers

Edge Storage Systems - By Platform Type (In Value%)

Telecom Edge Infrastructure

Enterprise On Premise Edge

Cloud Provider Distributed Edge

Industrial and Manufacturing Edge

Smart City Edge Platforms - By Fitment Type (In Value%)

Indoor Enterprise Edge Installations

Outdoor Ruggedized Edge Deployments

Embedded Edge within Equipment

Modular Containerized Edge Units

Tower and Base Station Integrated Edge - By End User Segment (In Value%)

Telecommunications Operators

Oil and Gas and Energy Companies

Government and Smart City Authorities

Manufacturing and Industrial Enterprises

Retail and Logistics Operators - By Procurement Channel (In Value%)

Direct OEM Procurement

Telecom Operator Partnerships

System Integrator Contracts

Government Tenders and Frameworks

Cloud and Managed Service Providers - By Material / Technology (in Value %)

GPU and AI Accelerator Based Edge

ARM Based Low Power Edge Systems

FPGA and ASIC Accelerated Edge

Ruggedized Industrial Grade Hardware

5G Integrated Edge Platforms

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Edge Hardware Portfolio, Edge Software Stack, Telecom Integration Capability, Industrial Solutions Depth, Local Presence, Managed Services Offering, AI Acceleration Support, Deployment Models, Strategic Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Saudi Telecom Company

Mobily

Zain Saudi Arabia

Aramco Digital

SITE Saudi Information Technology Company

Hewlett Packard Enterprise

Dell Technologies

Cisco Systems

Nokia

Ericsson

Huawei

Schneider Electric

Vertiv

Lenovo

IBM

- Telecom operators deploying edge to monetize 5G enterprise services

- Energy sector requiring edge for remote monitoring and automation

- Government entities adopting edge for smart city platforms

- Industrial enterprises integrating edge with automation systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now