Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA Electric Bus Market is experiencing significant growth, driven by increasing demand for sustainable transportation solutions. Based on a recent historical assessment, the market size is projected to reach approximately USD ~ billion. This growth is primarily fueled by government initiatives focused on reducing carbon emissions and the push toward adopting electric vehicles (EVs) to modernize the public transport sector. Furthermore, investments in electric bus infrastructure, including charging stations, are contributing to the market’s expansion, positioning the KSA as a leader in electric mobility in the region.

Saudi Arabia is at the forefront of the electric bus market in the Middle East, driven by the nation’s Vision 2030 initiative aimed at transforming its economy and promoting sustainable development. Key cities such as Riyadh and Jeddah are leading this transformation with large-scale investments in EV infrastructure and electric buses. These cities are benefiting from robust government support, including subsidies and green energy initiatives, which make them attractive locations for both public and private sector adoption of electric buses.

Market Segmentation

By Product Type

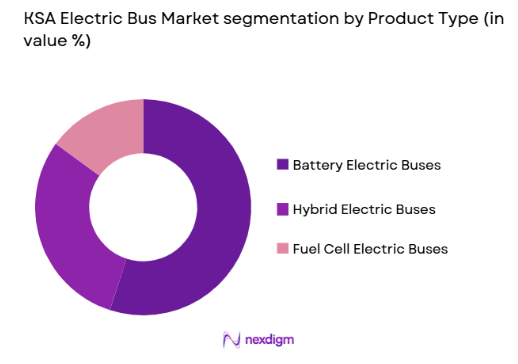

KSA Electric Bus Market is segmented by product type into battery electric buses, hybrid electric buses, and fuel cell electric buses. Recently, battery electric buses have a dominant market share due to their higher efficiency and lower operational costs compared to hybrid and fuel cell alternatives. The demand for battery electric buses is driven by improvements in battery technology, cost reductions, and the strong push for eco-friendly transport solutions.

By Platform Type

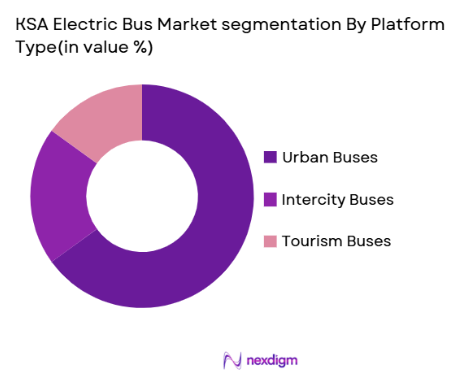

KSA Electric Bus Market is segmented by platform type into urban buses, intercity buses, and tourism buses. Urban buses have the largest share due to their frequent use in public transport networks and the increasing focus on sustainable urban mobility. Urban areas such as Riyadh and Jeddah are investing heavily in electric buses to meet environmental goals, with many new electric bus routes being developed in major city centers.

Competitive Landscape

The KSA Electric Bus Market is witnessing consolidation as major global players partner with local entities to take advantage of the growing demand. The market is dominated by companies that have established manufacturing and operational capabilities in Saudi Arabia, contributing to both local production and the development of EV infrastructure. The influence of these major players is strong, as they are shaping the market’s technological evolution and offering innovative electric bus models and solutions for the region.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Additional Parameter |

| Alstom | 1928 | France | ~ | ~ | ~ | ~ | ~ |

| BYD | 1995 | China | ~ | ~ | ~ | ~ | ~ |

| Volvo | 1927 | Sweden | ~ | ~ | ~ | ~ | ~ |

| New Flyer | 1930 | Canada | ~ | ~ | ~ | ~ | ~ |

| Proterra | 2004 | USA | ~ | ~ | ~ | ~ | ~ |

KSA Electric Bus Market Analysis

Growth Drivers

Government Initiatives

The government’s Vision 2035 program is a major driver of the KSA Electric Bus Market. Through this program, the government has made substantial investments in infrastructure and incentives for electric vehicle adoption. This includes subsidies for electric buses and grants for establishing charging stations in urban areas. The push to reduce carbon emissions is also contributing to the strong demand for sustainable transportation solutions, making electric buses a key component of the government’s efforts to diversify its economy and support sustainable development. With continued support from the public sector, the market for electric buses is expected to grow substantially, with government initiatives laying a solid foundation for long-term growth.

Technological Advancements

Technological advancements in battery systems, charging infrastructure, and electric drivetrains have also played a critical role in driving the growth of the electric bus market. As battery prices have decreased and their performance has improved, electric buses have become more cost-effective, both for public transport operators and private fleets. Additionally, innovations in charging technology, including fast-charging solutions and wireless charging systems, have made electric buses a viable alternative to traditional fossil fuel-powered buses. These advancements have not only made electric buses more affordable but have also improved their operational efficiency, further encouraging adoption across Saudi Arabia.

Market Challenges

High Initial Capital Investment

One of the significant challenges facing the KSA Electric Bus Market is the high initial capital required for electric buses. While the total cost of ownership is lower than traditional diesel buses, the upfront costs of electric buses and their charging infrastructure can be a major barrier for many public transport authorities and fleet operators. This challenge is compounded by the need for government subsidies or financial incentives to make the transition to electric buses financially feasible for operators. Without these financial incentives, many operators may continue to rely on cheaper, conventional buses despite the long-term environmental and economic benefits of electric buses.

Limited Charging Infrastructure

Another challenge is the limited availability of charging infrastructure across Saudi Arabia. While major cities like Riyadh and Jeddah are making strides in developing electric vehicle charging networks, the overall infrastructure required to support large fleets of electric buses is still underdeveloped. This lack of widespread charging stations makes it difficult for fleet operators to integrate electric buses into their operations, particularly for intercity routes where buses travel long distances. Expanding charging infrastructure is crucial to the market’s growth, but it requires significant investment in both hardware and logistics to ensure that electric buses are fully supported throughout their operational life.

Opportunities

Integration with Autonomous Technologies

One of the key opportunities for the KSA Electric Bus Market is the integration of autonomous driving technology into electric buses. With the global shift toward smart cities and autonomous vehicles, the integration of autonomous driving systems in electric buses presents a massive growth opportunity. Saudi Arabia has already begun to focus on smart city developments as part of its Vision 2035 initiative, which includes the introduction of self-driving vehicles in urban environments. Electric buses equipped with autonomous driving technology could reduce operational costs and improve safety, making them highly attractive for both public and private fleet operators. This opportunity is especially important in urban areas, where traffic congestion and the need for efficient, sustainable transportation solutions are pressing concerns.

Partnerships for Green Transportation Solutions

There is a significant opportunity for the KSA Electric Bus Market to expand through strategic partnerships between private sector players, international bus manufacturers, and local governments. These collaborations can help accelerate the deployment of electric buses and the necessary infrastructure, creating a more efficient ecosystem for sustainable transportation. Additionally, as private fleet operators look for ways to enhance their environmental sustainability and meet local regulatory requirements, they are increasingly turning to electric buses. Through these partnerships, the market can benefit from increased investments in electric bus fleets and charging infrastructure, leading to faster market penetration and wider adoption.

Future Outlook

The KSA Electric Bus Market is expected to continue its growth trajectory over the next five years, with increasing governmental and private sector investments supporting the shift towards sustainable urban mobility solutions. Key trends in the market include the rise of autonomous electric buses, advancements in battery and charging technologies, and continued regulatory support. With Saudi Arabia’s Vision 2030 driving infrastructure development and sustainability, the market is positioned to see strong growth in both demand and technological advancements, setting the stage for further adoption of electric buses across the region.

Major Players

- Alstom

- BYD

- Volvo

- New Flyer

- Proterra

- NFI Group

- Yutong

- Scania

- Tesla

- MAN SE

- King Long

- Hyundai Motor Company

- Solaris Bus & Coach

- Tata Motors

- Daimler

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Public transportation authorities

- Electric bus manufacturers

- Electric vehicle infrastructure providers

- Environmental organizations

- Fleet operators

- Automotive technology developers

Research Methodology

Step 1: Identification of Key Variables

The first step involves defining the key variables influencing the KSA Electric Bus Market, including market drivers, technological trends, and regulatory influences. These variables are critical for framing the scope of research and data collection.

Step 2: Market Analysis and Construction

In this step, the collected data is analyzed to construct a comprehensive understanding of the market’s current state, including historical trends and the factors driving growth. This analysis helps define the market segments and potential growth areas.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are tested and refined through consultations with industry experts, stakeholders, and key players in the electric vehicle sector. This ensures the validity of assumptions and adds credibility to the market analysis.

Step 4: Research Synthesis and Final Output

The final research synthesis compiles the analysis, expert feedback, and validated hypotheses into a cohesive report. This step results in a final output that outlines market trends, challenges, opportunities, and future forecasts.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government investment in sustainable transport

Rising demand for eco-friendly public transport

Technological advancements in electric bus infrastructure

Supportive regulatory policies and incentives

Growth in urbanization and population density - Market Challenges

High initial investment costs

Limited charging infrastructure

Range anxiety among consumers

Battery lifecycle and disposal concerns

Technological interoperability issues - Market Opportunities

Expansion in hybrid and fuel cell electric buses

Strategic partnerships for infrastructure development

Demand for eco-friendly buses in public sector transport - Trends

Rise of autonomous electric buses

Integration of AI in electric bus operations

Increased focus on green transport solutions - Government Regulations & Defense Policy

Incentives for electric vehicle adoption

Regulations on emissions and environmental standards

Government-funded electric bus procurement programs - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Battery Electric Buses

Hybrid Electric Buses

Plug-in Hybrid Electric Buses

Fuel Cell Electric Buses

Advanced Bus Control Systems - By Platform Type (In Value%)

Urban Buses

Intercity Buses

Tourist Buses

School Buses

Electric Bus Chargers - By Fitment Type (In Value%)

New-Build Buses

Retrofit Buses

Modular Buses

Integrated Bus Systems

Electric Bus Charging Infrastructure - By EndUser Segment (In Value%)

Government Transportation Authorities

Private Fleet Operators

Tourism and Leisure Sector

Public Transport Operators

Educational Institutions - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors - By Material / Technology (in Value%)

Lithium-ion Batteries

Solid-State Batteries

Fuel Cells

Electric Drivetrains

Autonomous Driving Technology

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Price, Market Share, Technology, System Type, End-User Segment, Procurement Channel, Innovation, Distribution Channels, Customer Satisfaction, Geographic Reach)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Alstom

BYD

New Flyer

Proterra

Volvo

Daimler

Yutong

Tesla

NFI Group

MAN SE

Scania

King Long

Tata Motors

Solaris Bus & Coach

Hyundai Motor Company

- Demand from public sector transport authorities

- Growth in private sector electric bus adoption

- Increased adoption by educational institutions

- Demand from the tourism and leisure sector

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now