Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA EV Insulation Materials Market is valued at USD ~, reflecting the cumulative value of insulation materials deployed across battery systems, power electronics, electric motors, and high-voltage components within electric vehicles manufactured or assembled in the Kingdom. Market demand is structurally linked to the rapid buildup of domestic EV manufacturing capacity, rising deployment of high-voltage architectures, and the need to ensure thermal stability and electrical safety under harsh operating conditions. Consumption is further driven by the integration of advanced battery safety layers, sealing systems, and thermal interface materials as EV platforms transition from pilot volumes to industrial-scale production.

Within Saudi Arabia, demand is concentrated in industrial and policy-driven hubs such as the Central Region and Western Region, where EV manufacturing facilities, component integration centers, and logistics infrastructure are clustered. These regions dominate due to proximity to OEM plants, access to skilled industrial labor, and alignment with national industrialization initiatives. From a technology and supply perspective, global insulation material innovation and formulations continue to be influenced by mature automotive material ecosystems in advanced manufacturing economies, which shape product specifications and qualification benchmarks adopted by EV programs operating in the Kingdom.

Market Segmentation

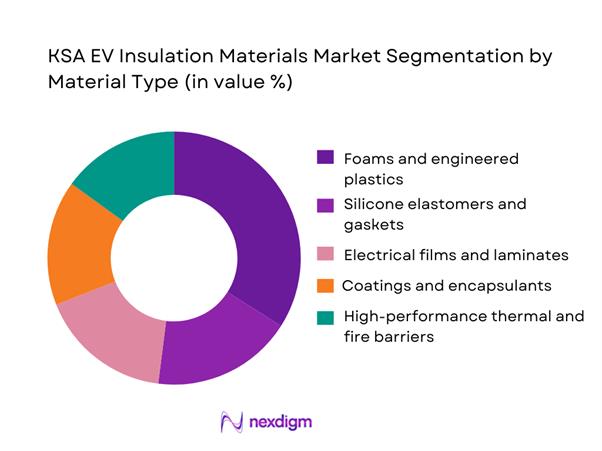

By Material Type

Foams and engineered plastics dominate the KSA EV Insulation Materials Market by material type due to their versatility, cost efficiency, and broad applicability across multiple EV subsystems. These materials are widely used in battery pack enclosures, sealing interfaces, vibration damping zones, and structural insulation components. Their dominance is reinforced by ease of processing, compatibility with automated assembly lines, and availability through regional polymer supply chains. In high-temperature operating environments, engineered foams provide effective thermal buffering while maintaining lightweight characteristics critical for EV efficiency. Additionally, local availability of base polymer feedstocks enables faster lead times and supports localized converting operations, making foams and plastics the preferred choice during early and mid-stage EV production scaling.

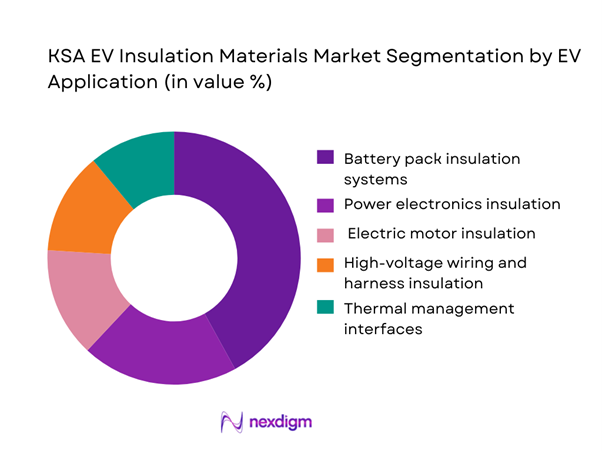

By EV Application

Battery pack insulation systems represent the dominant application segment in the KSA EV Insulation Materials Market due to the critical role batteries play in vehicle safety, performance, and regulatory compliance. Battery packs require multi-layer insulation solutions to manage thermal loads, prevent electrical short circuits, and mitigate the risk of thermal runaway. These requirements intensify in Saudi Arabia’s climatic conditions, where elevated ambient temperatures place additional stress on battery systems. OEMs and Tier-1 suppliers prioritize robust insulation designs within battery modules and packs, leading to higher material intensity compared to other EV subsystems. As domestic EV manufacturing expands, battery insulation remains the focal point of qualification, sourcing, and localization efforts.

Competitive Landscape

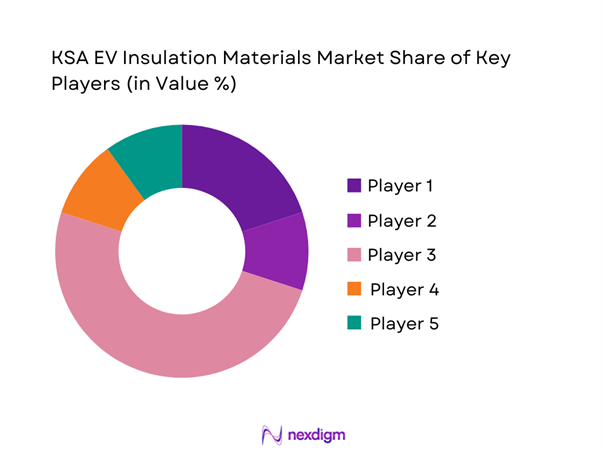

The KSA EV Insulation Materials Market is dominated by a few major players, including SABIC and global or regional brands like 3M, Saint-Gobain, DuPont, and Henkel. This consolidation highlights the significant influence of these key companies.

| Company | Est. year | HQ | KSA presence model | EV subsystem coverage focus | Qualification strengths | Fire/thermal barrier portfolio | Electrical dielectric portfolio | Converting/kitting capability |

| 3M | 1902 | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Saint-Gobain | 1665 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| DuPont | 1802 | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Henkel | 1876 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| SABIC | 1976 | Saudi Arabia | ~ | ~ | ~ | ~ | ~ | ~ |

KSA EV Insulation Materials Market Analysis

Growth Drivers

EV manufacturing localization initiatives

EV manufacturing localization initiatives are a major structural growth driver for the KSA EV Insulation Materials Market, closely aligned with Saudi Arabia’s industrial diversification and automotive localization agenda. As EV OEMs and Tier-1 suppliers establish assembly, battery pack integration, and component manufacturing operations within the Kingdom, procurement strategies increasingly shift toward suppliers capable of supporting local production footprints. This transition directly elevates demand for insulation materials used in battery enclosures, high-voltage cabling, power electronics, and electric motors. Localization drives higher consumption of insulation materials that meet automotive-grade performance, traceability, and compliance requirements. Furthermore, local manufacturing enables closer technical collaboration between OEMs, integrators, and material suppliers, accelerating product qualification cycles and customization. Reduced dependence on cross-border logistics also improves supply continuity, making insulation materials a strategically critical input for sustaining EV production operations within Saudi Arabia.

Battery safety and thermal regulation requirements

Battery safety and thermal regulation requirements are a fundamental driver shaping insulation material demand in Saudi Arabia’s EV ecosystem. Modern EV batteries operate at high energy densities, which increases the risk of thermal runaway, electrical short circuits, and heat accumulation under extreme operating conditions. Insulation materials play a critical role in mitigating these risks by providing electrical isolation, heat resistance, and flame-retardant protection across battery modules and pack assemblies. In Saudi Arabia’s hot climate, thermal management challenges are amplified, making robust insulation solutions essential for maintaining battery performance and lifecycle stability. As EV platforms transition toward higher voltage architectures and faster charging systems, insulation specifications become more stringent, requiring advanced materials with higher dielectric strength and thermal stability. This trend increases per-vehicle insulation content and drives demand for technologically advanced insulation solutions across EV platforms.

Challenges

Limited local availability of specialty materials

Limited local availability of specialty insulation materials represents a significant challenge for the KSA EV Insulation Materials Market. High-performance materials such as fire-resistant battery barriers, thermally conductive electrically insulating compounds, and advanced ceramic or mica-based solutions are often sourced from global suppliers with limited regional production capacity. This reliance on imports results in longer lead times, higher inventory costs, and exposure to supply chain disruptions. For OEMs and Tier-1 suppliers operating under tight production schedules, delays in receiving critical insulation components can disrupt vehicle program timelines and manufacturing continuity. Additionally, imported materials often require additional regulatory documentation and conformity assessments, adding complexity to procurement processes. The absence of a fully developed domestic specialty materials ecosystem can also constrain innovation and customization, limiting the ability of manufacturers to rapidly adapt insulation solutions to evolving EV platform requirements.

Lengthy qualification and certification cycles

Lengthy qualification and certification cycles pose another major challenge in the KSA EV Insulation Materials Market. EV insulation materials must comply with rigorous automotive performance standards related to electrical insulation, thermal endurance, flame resistance, chemical stability, and long-term durability. Achieving approval requires extensive laboratory testing, validation under real-world operating conditions, and close coordination with OEM engineering teams. These processes are time-intensive and demand substantial technical expertise and documentation. For new entrants or locally emerging suppliers, navigating these qualification pathways can significantly delay market entry and restrict their ability to compete with established global players. In addition, repeated testing is often required when materials are modified or localized, further extending approval timelines. As a result, qualification complexity can limit supplier diversification and slow the pace of innovation within the insulation materials landscape.

Opportunities

Localization of converting and kitting operations

The localization of converting and kitting operations presents a strong growth opportunity within the KSA EV Insulation Materials Market. Rather than manufacturing raw insulation materials, local players can add significant value by converting imported base materials into application-specific components such as die-cut pads, laminated insulation stacks, gaskets, and pre-assembled insulation kits. These localized operations enable faster response times, improved customization, and closer integration with OEM and Tier-1 production workflows. Converting and kitting also reduce waste, improve material utilization efficiency, and lower logistics complexity. From a strategic perspective, localized conversion supports Saudi Arabia’s industrial development objectives by creating skilled manufacturing jobs and strengthening domestic supply chains. As EV production volumes increase, demand for just-in-time, application-ready insulation components is expected to grow, positioning localized converters as critical enablers of the EV ecosystem.

Development of battery fire barrier materials

The development and localization of battery fire barrier materials represent a high-value opportunity in the KSA EV Insulation Materials Market. Increasing regulatory focus and OEM emphasis on battery safety are driving demand for advanced materials capable of preventing or delaying thermal runaway propagation within battery packs. Fire barrier solutions, including ceramic-based layers, mica composites, and high-temperature insulation systems, are becoming essential components in EV battery design. Currently, much of this technology is supplied by global specialists, creating an opportunity for regional suppliers to invest in materials science capabilities and local production. Suppliers that successfully develop or localize fire barrier technologies can secure long-term supply contracts and premium positioning within EV value chains. As EV programs scale and safety expectations rise, fire barrier materials are likely to remain one of the most strategically important insulation segments in Saudi Arabia’s EV market.

Future Outlook

The KSA EV Insulation Materials Market is expected to evolve alongside the Kingdom’s broader electric mobility ecosystem, characterized by increased vehicle production volumes, deeper localization, and higher technical standards. Strategic focus on battery safety, thermal management, and high-voltage system reliability will drive sustained demand for advanced insulation solutions. Competitive advantage will increasingly depend on local technical support, supply reliability, and the ability to deliver application-specific insulation systems rather than commodity materials.

Major Players

- SABIC

- Tasnee

- Sipchem

- 3M

- Saint-Gobain

- DuPont

- Henkel

- BASF

- Dow

- Covestro

- Rogers Corporation

- Morgan Advanced Materials

- Von Roll

- SGL Carbon

Key Target Audience

- EV original equipment manufacturers

- Battery pack manufacturers

- Power electronics and inverter suppliers

- Charging infrastructure developers

- Automotive component Tier-1 suppliers

- Fleet and mobility service operators

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The study begins by identifying critical variables influencing the KSA EV Insulation Materials Market, including EV production scale, insulation intensity per vehicle, and regulatory requirements. Desk research and ecosystem mapping are used to define scope and boundaries.

Step 2: Market Analysis and Construction

Historical demand patterns are analyzed alongside EV manufacturing activity to construct the market framework. Application-level material usage is assessed to understand revenue attribution.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through structured consultations with industry stakeholders, including material suppliers, converters, and OEM procurement teams, ensuring alignment with real-world practices.

Step 4: Research Synthesis and Final Output

Findings are synthesized into a cohesive market narrative, integrating quantitative structures and qualitative insights to produce a client-ready analysis.

- Executive Summary

- Research Methodology (Market Definitions and Inclusions/Exclusions, Abbreviations, Topic-Specific Taxonomy, Market Sizing Framework, Revenue Attribution Logic Across Use Cases or Care Settings, Primary Interview Program Design, Data Triangulation and Validation, Limitations and Data Gaps)

- Definition and Scope

- Market Genesis and Evolution

- EV Insulation Usage and Value-Chain Mapping

- Business Cycle and Demand Seasonality

- KSA EV Manufacturing and Supply Architecture

- Growth Drivers

EV manufacturing localization initiatives

Battery safety and thermal regulation requirements

High-voltage platform adoption

Extreme climate operating conditions

Expansion of charging infrastructure - Challenges

Limited local availability of specialty materials

Lengthy qualification and certification cycles

Dependence on imported high-performance inputs

Cost pressures from advanced formulations

Evolving regulatory compliance requirements - Opportunities

Localization of converting and kitting operations

Development of battery fire barrier materials

OEM–supplier co-development programs

Aftermarket and service insulation demand

Export potential to regional EV programs - Trends

Advanced thermal runaway mitigation materials

Multifunctional insulation designs

Lightweight and space-optimized materials

Automation-compatible insulation formats

Enhanced traceability and compliance documentation - Regulatory & Policy Landscape

- SWOT Analysis

- Stakeholder & Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Average Price, 2019–2024

- By Material Type (in Value %)

Foams and engineered plastics

Silicone elastomers and gaskets

Electrical films and laminates

Coatings and encapsulants

High-performance thermal and fire barriers - By EV Application (in Value %)

Battery pack insulation systems

Power electronics insulation

Electric motor insulation

High-voltage wiring and harness insulation

Thermal management interfaces - By Technology / Product Type (in Value %)

Thermally conductive insulating materials

Dielectric insulation materials

Fire-retardant and thermal runaway barriers

Vibration and acoustic insulation solutions

Multifunctional hybrid insulation systems - By Deployment / Distribution Model (in Value %)

OEM direct sourcing

Tier-1 supplier integration

Local converters and fabricators

Authorized distributors and stockists - By End-Use Customer Type (in Value %)

EV OEMs

Battery pack manufacturers

Power electronics suppliers

Charging infrastructure developers

Fleet and mobility operators - By Region (in Value %)

Central Region

Western Region

Eastern Region

Southern Region

Northern Region

- Competition ecosystem overview

- Cross Comparison Parameters (dielectric strength, thermal conductivity, maximum operating temperature, fire resistance class, material thickness range, local availability lead time, EV-grade certification status, customization capability)

- SWOT analysis of major players

Pricing and commercial model benchmarking - Detailed Profiles of Major Companies

SABIC

Tasnee

Sipchem

3M

Saint-Gobain

DuPont

Henkel

BASF

Dow

Covestro

Rogers Corporation

Morgan Advanced Materials

Von Roll

SGL Carbon

Huntsman

- Buyer personas and decision-making units

- Procurement and contracting workflows

- KPIs used for evaluation

- Pain points and adoption barriers

- By Value, 2025–2030

- By Volume, 2025–2030

- By Average Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now