Download PDF

Download PDFMarket Overview

KSA Fats and Oil Market is valued at USD ~ billion, based on a five-year historical analysis, and is forecasted to grow at a CAGR of ~% during the forecast period. Demand is driven by corn oil, sunflower oil, palm oil, vegetable ghee, butter ghee, olive oil, bakery fats, frying oils and HoReCa bulk packs. Saudi Arabia’s GDP reached USD 1.24 trillion, GDP per capita reached USD 35,121.7 and population reached 35 million, supporting household and foodservice consumption. Riyadh, Jeddah, Makkah, Madinah, Dammam, Khobar and Jubail dominate KSA Fats and Oil Market because of modern retail density, foodservice concentration, port access, institutional procurement, pilgrimage catering and industrial food processing. Saudi tourism reached 116 million tourists, including 29.7 million inbound tourists and 86.2 million domestic tourists, strengthening edible oil demand across hotels, restaurants, catering, QSR chains, cloud kitchens and pilgrimage-linked meal preparation.

Market Segmentation

By Product Type

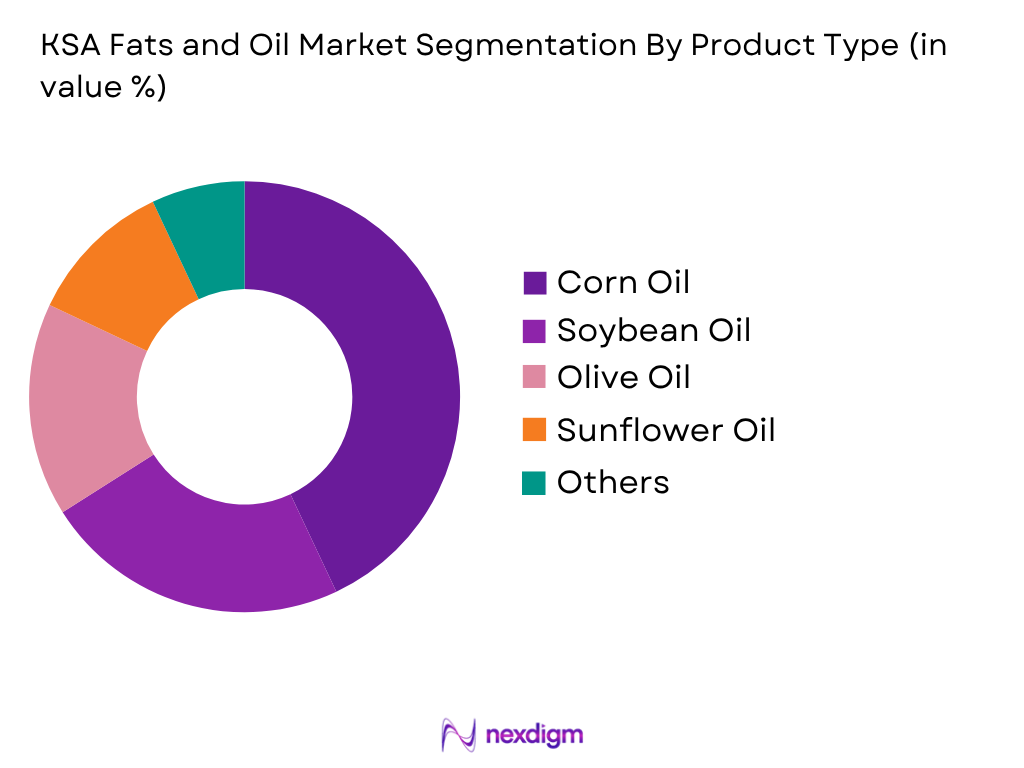

KSA Fats and Oil Market is segmented by product type into corn oil, sunflower oil, palm oil, palm olein, soybean oil, canola oil, olive oil, coconut oil, vegetable oil blends, vegetable ghee, butter ghee, butter, margarine, shortening, bakery fats, frying oils and specialty fats. Recently, corn oil has had a dominant market share under the product type segmentation due to its strong household acceptance, long-standing brand presence, health-oriented positioning and compatibility with Saudi, Levantine, South Asian and everyday home cooking. Brands such as Afia and Mazola have built high consumer familiarity in corn oil and blended oil categories. Palm oil and palm olein remain essential in foodservice frying, bakery, confectionery and institutional cooking due to stability and functionality. Sunflower oil is widely used in household cooking, while olive oil is stronger in premium urban retail. Corn oil remains dominant in value terms because it combines household trust, premium positioning and broad retail visibility.

By Distribution Channel

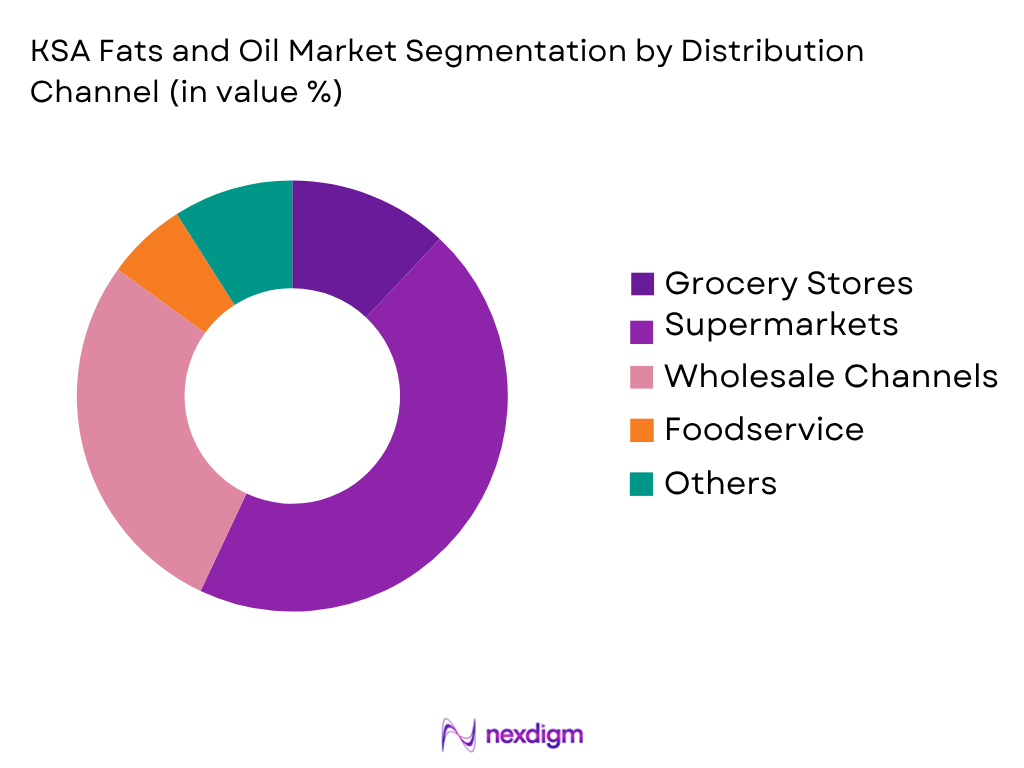

KSA Fats and Oil Market is segmented by distribution channel into hypermarkets and supermarkets, baqala and independent grocery stores, convenience stores, cash-and-carry wholesalers, online grocery, quick commerce, foodservice distributors, hotel and catering suppliers, industrial ingredient suppliers and institutional procurement channels. Recently, hypermarkets and supermarkets have had the dominant market share under the distribution channel segmentation because cooking oils and fats are purchased as planned grocery items in family-size bottles, tins, multipacks, economy packs and private-label formats. Large retail chains provide wide comparison across corn oil, sunflower oil, olive oil, palm oil, ghee, canola oil and blended oils. Baqala outlets remain relevant for top-up purchases, while foodservice distributors serve restaurants, QSR chains, hotels, cafeterias and caterers. Hypermarkets dominate because they combine assortment depth, promotions, family shopping baskets, imported brands, private labels and premium oil visibility.

Competitive Landscape

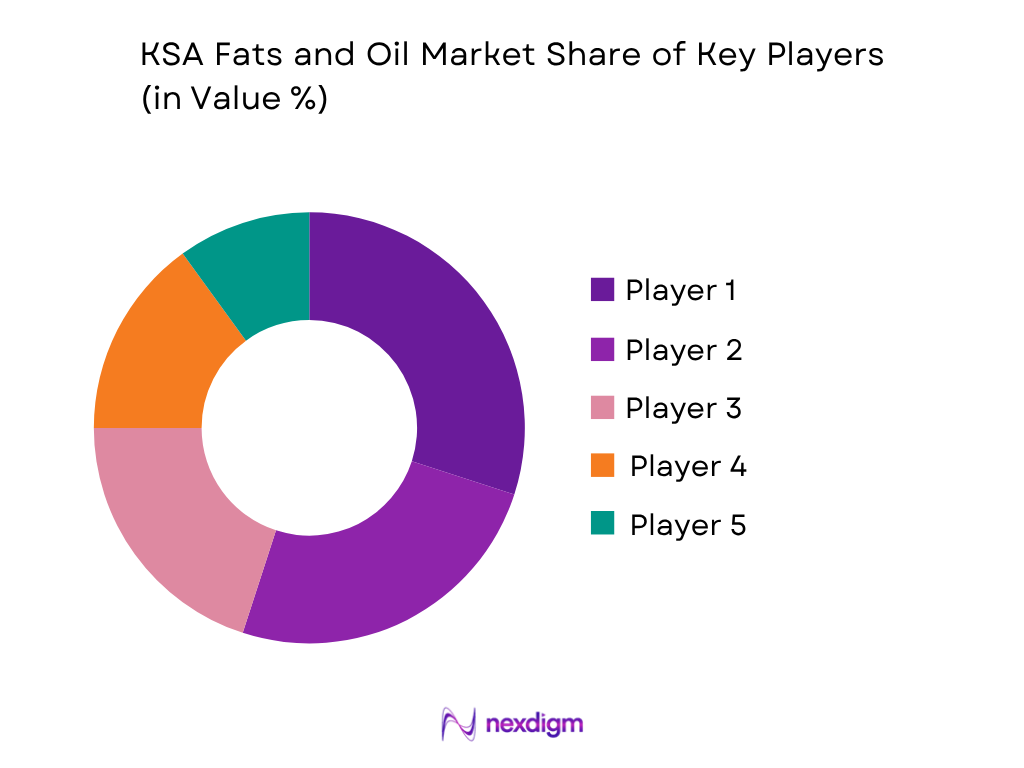

KSA Fats and Oil Market is led by domestic edible oil brands, GCC food companies, importers, refiners, ghee manufacturers, private-label suppliers and foodservice oil distributors. Savola Foods, Afia International, Delmon Products, IFFCO Arabia and United Foods are major players due to branded oil portfolios, corn oil and sunflower oil positioning, bulk supply capability, regional manufacturing access, retail presence and institutional demand coverage. Savola’s food portfolio includes edible oils and ghee brands such as Afia, Shams, Alarabi, Rawabi and Janna, and Afia has operated as a recognized Arab-market cooking oil brand since 1980.

| Company | Establishment Year | Headquarters | Core Portfolio | Processing / Supply Strength | Key End Users | Channel Strength | Compliance / Positioning Focus | Market-Specific Advantage |

| Savola Foods | 1979 | Jeddah, KSA | ~ | ~ | ~ | ~ | ~ | ~ |

| Afia International Company | 1980 | Jeddah, KSA | ~ | ~ | ~ | ~ | ~ | ~ |

| Delmon Products Limited | 1981 | Jeddah, KSA | ~ | ~ | ~ | ~ | ~ | ~ |

| IFFCO Arabia | 1975 group origin | Jeddah / GCC operating base | ~ | ~ | ~ | ~ | ~ | ~ |

| United Foods Company | 1976 | Dubai, UAE | ~ | ~ | ~ | ~ | ~ | ~ |

KSA Fats and Oil Market Analysis

Growth Drivers

Household Cooking, Urban Foodservice and Pilgrimage Catering Demand

Household cooking, urban foodservice and pilgrimage catering are core growth drivers for the KSA Fats and Oil Market because corn oil, sunflower oil, palm olein, vegetable ghee, butter ghee, olive oil, shortening and bakery fats are used across homes, restaurants, QSR chains, hotels, cafeterias and institutional kitchens. World Bank data records Saudi Arabia’s GDP at USD 1.24 trillion, GDP per capita at USD 35,121.7, GDP growth at 2.0 and population at 35 million, supporting high-volume food retail and HoReCa consumption. DataSaudi records 116 million tourists, including 29.7 million inbound tourists and 86.2 million domestic tourists, with religious travel as the largest inbound purpose, directly supporting Makkah, Madinah and Jeddah catering demand. IMF lists Saudi Arabia’s 2026 population at 36.726 million and projected real GDP change at 3.1, indicating continued demand scale. This driver is market specific because pilgrimage kitchens, hotel buffets, QSR fryers, baqala retail, family-size oil packs and bakery manufacturers require continuous supply of cooking oils and fats.

Import Availability, Domestic Bottling and Food Manufacturing Linkages

Import availability and domestic bottling capacity drive the KSA Fats and Oil Market because Saudi Arabia relies on global palm, sunflower, corn, soybean, canola and olive oil supply while local companies convert imported bulk oils into branded retail packs, ghee, frying oils, bakery fats and institutional formats. World Bank WITS records Saudi Arabia’s crude palm oil imports at 601,691,000 kilograms, valued at USD 591,870.44 thousand, with Indonesia supplying 374,320,000 kilograms and Malaysia supplying 227,088,000 kilograms. The same import base supports palm olein frying, bakery shortening, confectionery fats, foodservice drums and industrial fat blends. World Bank data records GDP at USD 1.24 trillion and GDP per capita at USD 35,121.7, while IMF records 2026 GDP at USD 1.39 trillion and GDP per capita at USD 37.81 thousand. These indicators support investment in refining, storage, bottling, private-label packing and food manufacturing. The driver is market specific because imported feedstock must be converted into SKU-level formats for hypermarkets, baqala stores, HoReCa distributors, caterers and packaged food producers.

Market Challenges

High Import Dependence and Global Supply Exposure

High import dependence is a major challenge for the KSA Fats and Oil Market because the country depends on external suppliers for palm oil, sunflower oil, corn oil, soybean oil, canola oil, olive oil, coconut oil and specialty fats. World Bank WITS records crude palm oil imports of 601,691,000 kilograms, with Indonesia and Malaysia together supplying almost all recorded crude palm oil volume through 374,320,000 kilograms and 227,088,000 kilograms, respectively. SFDA notes that Saudi Arabia imports over 80 out of every 100 food products, making imported food-product compliance commercially important for edible oils and fats. World Bank data records GDP at USD 1.24 trillion and population at 35 million, while IMF lists 2026 population at 36.726 million. This demand base must be supplied continuously despite shipping disruption, supplier-country crop variation, documentation controls and bulk-storage limits. The challenge is market specific because palm olein fry oils, corn oil retail packs, sunflower household oils, olive oil premium SKUs, ghee substitutes and bakery fats all depend on uninterrupted import flows and food-grade logistics.

SFDA Compliance, Trans-Fat Elimination and SKU-Level Quality Control

SFDA compliance and SKU-level quality control restrain the KSA Fats and Oil Market because edible oils and fats must meet food safety, Arabic labeling, Halal, shelf-life, nutrition disclosure and trans-fat requirements across retail packs, bulk drums, institutional cans, bakery fats and foodservice blends. SFDA states that Saudi Arabia eliminated artificial trans fats from the food supply in January 2020 and continues to prioritize implementation and compliance, affecting local manufacturers and imported food products. This is directly relevant to margarine, shortening, bakery fats, frying oils, vegetable ghee and palm-based specialty fats, where formulation control and supplier documentation are essential. World Bank data records Saudi GDP per capita at USD 35,121.7 and GDP growth at 2.0, while DataSaudi records 116 million tourists, creating diversified demand across premium retail and high-volume institutional foodservice. The challenge is operational because suppliers must maintain consistent fatty-acid specifications, batch testing, label accuracy, Halal documentation, storage discipline and traceability while serving hypermarkets, baqala stores, online grocery, hotels, caterers, bakeries and pilgrimage meal providers.

Market Opportunities

Premium, Health-Positioned and Cuisine-Specific Oils

Premium, health-positioned and cuisine-specific oils create a future growth opportunity for the KSA Fats and Oil Market because Saudi households and expatriate communities use different oils for Saudi, Levantine, South Asian, Egyptian, Filipino and Western cuisines. World Bank data records GDP per capita at USD 35,121.7 and population at 35 million, supporting demand for corn oil, sunflower oil, olive oil, canola oil, avocado oil, pure ghee, butter ghee and cholesterol-free branded oils. IMF’s 2026 profile lists GDP per capita at USD 37.81 thousand and population at 36.726 million, indicating continued premium retail capacity. DataSaudi records 116 million tourists, including 29.7 million inbound tourists, strengthening restaurant and hotel demand for olive oil, frying oils, ghee and specialty fats suited to international menus. This opportunity is market specific because suppliers can segment products by cuisine use, Halal assurance, cholesterol-free claims, trans-fat-free positioning, omega messaging, premium origin, family-size packs, foodservice bulk formats and online grocery bundles, while protecting margins through differentiated retail SKUs rather than commodity oil competition.

Foodservice Frying Systems, Institutional Bulk Supply and Sustainable Palm Sourcing

Foodservice frying systems, institutional bulk supply and sustainable palm sourcing create future growth opportunities for the KSA Fats and Oil Market because hotels, QSR chains, caterers, Hajj and Umrah meal providers, bakeries and packaged food manufacturers need stable oils with consistent fry life, neutral flavor, smoke-point reliability and compliance documentation. DataSaudi records 116 million tourists, with 86.2 million domestic tourists and 29.7 million inbound tourists, supporting bulk demand from Makkah, Madinah, Riyadh, Jeddah and Eastern Province foodservice clusters. World Bank WITS records crude palm oil imports of 601,691,000 kilograms, including 374,320,000 kilograms from Indonesia and 227,088,000 kilograms from Malaysia, confirming the feedstock base for palm olein, shortening, bakery fats and frying blends. World Bank records GDP at USD 1.24 trillion, while IMF lists 2026 projected real GDP change at 3.1. This opportunity is direct for suppliers offering high-stability frying oils, foodservice drums, bulk delivery, fryer-management support, used-oil handling, RSPO-oriented palm sourcing, Arabic-English documentation, Halal traceability and institutional procurement support.

Future Outlook

KSA Fats and Oil Market is expected to expand steadily during the forecast period, supported by household cooking oil demand, pilgrimage catering, hospitality growth, QSR expansion, online grocery adoption, food manufacturing, bakery demand and premium oil consumption. Corn oil and sunflower oil will remain important in household retail, while palm oil and palm olein will remain essential in frying, bakery, confectionery and institutional applications. Vegetable ghee and butter ghee will continue serving Saudi, South Asian and Arab cooking uses. Foodservice will be a central growth platform. Tourism reached 116 million tourists, including 29.7 million inbound tourists and 86.2 million domestic tourists, creating large-scale demand from hotels, restaurants, cafés, caterers, Hajj and Umrah meal providers, airport catering, QSR chains and cloud kitchens.

The market will remain import-dependent for palm oil, sunflower oil, olive oil, soybean oil, canola oil and specialty fats. Suppliers with flexible sourcing, port storage access, bulk supply reliability, private-label capabilities and SFDA-compliant labeling systems will be better positioned. Premiumization will remain visible in olive oil, cholesterol-free oils, omega-positioned oils, trans-fat-free oils and high-stability frying blends. However, mainstream corn oil, sunflower oil, palm olein and ghee will remain central due to daily cooking habits and foodservice affordability.

Major Players

- Savola Foods

- Afia International Company

- Delmon Products Limited

- IFFCO Arabia

- Basateen Foods Saudi Arabia

- Arab Malaysian Vegetable Oil Products Company

- United Flowers for Vegetable Oils

- Almarai

- NADEC

- Al Jouf Agricultural Development Company

- Al-Riyadh Company for Vegetable Oil Industry

- Al-Hussan Factory for Food Products

- Mazola Saudi Arabia

- Areej Vegetable Oils and Derivatives

- United Foods Company

Key Target Audience

- Edible Oil Manufacturers

- Edible Oil Importers, Refiners and Bottlers

- Food Processing Companies

- HoReCa and QSR Operators

- Hypermarket, Supermarket and Baqala Buyers

- Institutional and Pilgrimage Catering Operators

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (Saudi Food and Drug Authority, Ministry of Environment Water and Agriculture, Ministry of Commerce, Zakat Tax and Customs Authority, Saudi Standards Metrology and Quality Organization)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the KSA Fats and Oil Market. This includes importers, refiners, bottlers, blenders, hypermarket chains, baqala wholesalers, foodservice distributors, hotel procurement teams, institutional caterers, industrial food manufacturers and regulators. The objective is to define variables such as product type, source, application, channel, region, pack format, import dependency and compliance requirement.

Step 2: Market Analysis and Construction

In this phase, historical data is compiled and analyzed for the KSA Fats and Oil Market. The assessment covers corn oil, sunflower oil, palm oil, olive oil, vegetable ghee, butter ghee, foodservice frying oils, industrial bakery fats, shortening, margarine and private-label cooking oils. Top-down validation uses macroeconomic, trade and regulatory datasets, while bottom-up validation uses SKU mapping, distributor checks and channel-level assessment.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through computer-assisted telephone interviews with edible oil brands, importers, refiners, supermarket category managers, baqala distributors, HoReCa suppliers, hotel procurement teams and industrial ingredient buyers. These consultations provide insights into sourcing, price sensitivity, pack-size movement, foodservice oil performance, pilgrimage demand, health positioning, private-label activity and SFDA compliance requirements.

Step 4: Research Synthesis and Final Output

The final phase integrates desk research, trade-flow assessment, retail audits, distributor interviews, foodservice buyer inputs and competitive benchmarking into a consolidated market model. Supplier inputs are compared with observed shelf presence, bulk oil movement, institutional procurement and industrial fat usage. The final output provides a validated view of market size, segmentation, competition, future outlook and strategic implications.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Edible Fats and Oils Classification, Vegetable Oil and Animal Fat Inclusion Criteria, Packaged Cooking Oil vs Bulk Oil Inclusion Criteria, Palm Oil and Soft Oil Import Mapping, Domestic Refining and Bottling Assessment, Retail vs HoReCa vs Industrial Demand Mapping, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Saudi Import and Refining Flow Assessment, GCC Foodservice Demand Mapping, Retail SKU Audits, Distributor and HoReCa Channel Interviews, Industrial Ingredient Buyer Interviews, Primary Industry Interviews, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Business Cycle and Seasonal Demand Pattern

- Vegetable Oil Import and Refining Value Chain Analysis

- Palm Oil and Specialty Fat Value Chain Analysis

- Growth Drivers (High Household Cooking Oil Consumption, Hajj and Umrah Catering Demand, Vision-Led Hospitality and Tourism Expansion, HoReCa and QSR Growth, Imported Palm and Soft Oil Availability, Domestic Refining and Bottling Capability, Bakery and Confectionery Ingredient Demand, Private Label Growth Across Modern Retail, Health-Oriented Corn and Sunflower Oil Adoption)

- Market Challenges (High Import Dependency, Global Palm and Sunflower Oil Price Volatility, Freight and Currency Exposure, Foodservice Margin Pressure, Retail Shelf Competition, Premium Oil Affordability, SFDA Labeling and Food Safety Compliance, Halal Documentation Requirements, Supply Exposure to Major Exporting Countries)

- Market Opportunities (Premium Olive Oil Expansion, Corn and Sunflower Health Oil Positioning, Foodservice Frying Oil Management, Sustainable Palm Oil Sourcing, Private Label Cooking Oils, Bakery and Confectionery Specialty Fats, Institutional and Pilgrimage Catering Bulk Supply, Online Grocery Multipacks, Clean Label and Trans-Fat-Free Industrial Fats)

- Market Trends (Corn Oil Brand Strength, Sunflower Oil Household Preference, Palm-Based Foodservice Frying Use, Vegetable Ghee and Butter Ghee Demand, Olive Oil Premiumization, Cholesterol-Free Claims, Private Label Expansion, Online Grocery Replenishment, Sustainable Palm Certification, High-Stability Frying Oil Adoption)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Selling Price (2020-2025)

- By Product Type (In Value %)

Corn Oil

Sunflower Oil

Palm Oil

Palm Olein

Palm Kernel Oil

Soybean Oil - By Source Type (In Value %)

Vegetable Oils

Dairy-Based Fats

Animal-Based Fats

Blended Oils and Fats

Imported Tropical Oils - By Distribution Channel (In Value %)

Hypermarkets and Supermarkets

Baqala and Independent Grocery Stores

Convenience Stores

Cash-and-Carry and Wholesale Channels

Cooperatives and Community Retail - By Region (In Value %)

Riyadh Region

Makkah Region

Jeddah Retail and Port Cluster

Eastern Province

Dammam and Jubail Industrial Cluster

- Market Share of Major Players (By Value, Volume, Product Type, Application, Channel, Source Type)

- Competitive Positioning Matrix (Import Sourcing Strength, Refining and Bottling Capacity, Branded Cooking Oil Portfolio, Retail Distribution Reach, HoReCa Bulk Supply, Private Label Capability, Premium Oil Portfolio, Institutional Catering Access)

- Cross Comparison Parameters (Refining and Bottling Capacity, Corn-Sunflower-Palm Oil Portfolio Breadth, Branded Cooking Oil SKU Count, Hypermarket and Baqala Distribution Reach, HoReCa Bulk Oil Capability, Private Label Manufacturing Strength, Halal and SFDA Compliance Coverage, Institutional and Pilgrimage Catering Supply Network)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Savola Foods

Afia International Company

Delmon Products Limited

IFFCO Arabia

Basateen Foods Saudi Arabia

Arab Malaysian Vegetable Oil Products Company

United Flowers for Vegetable Oils

Almarai

NADEC

Al Jouf Agricultural Development Company

Al-Riyadh Company for Vegetable Oil Industry

Al-Hussan Factory for Food Products

Mazola Saudi Arabia

Areej Vegetable Oils and Derivatives

United Foods Company

- Household Consumption Behavior Assessment

- Cuisine-Based Oil Preference Assessment

- HoReCa Demand Assessment

- Pilgrimage Catering Demand Assessment

- Industrial Food Manufacturer Demand Assessment

- Health and Wellness Influence on Purchase Decisions

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now