Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA Green Hydrogen market has witnessed significant growth due to the Kingdom’s ambitious sustainability goals and its strategic commitment to diversify its energy sector. Based on a recent historical assessment, the market size for green hydrogen in the region is substantial, driven by strong governmental support, large-scale projects, and the country’s vast renewable energy potential. The demand for hydrogen is fueled by the rising need for clean energy sources, especially for use in industrial applications and transportation. The total market value for green hydrogen production and consumption is projected to reach USD ~ billion, with expected exponential growth in the coming years due to increasing investment from both the public and private sectors.

The Kingdom’s dominance in the green hydrogen market is largely due to its abundant renewable energy resources, particularly solar and wind power, which provide the foundation for green hydrogen production. Additionally, KSA’s strategic position as a regional leader in energy markets has further strengthened its competitive edge. Cities like Riyadh and Jeddah, along with government-backed initiatives like NEOM, are key hubs driving the green hydrogen sector. The government’s long-term strategy, as outlined in Vision 2030, promotes investments in renewable energy technologies and the development of hydrogen infrastructure, positioning Saudi Arabia as a leader in the global green hydrogen economy.

Market Segmentation

By Product Type:

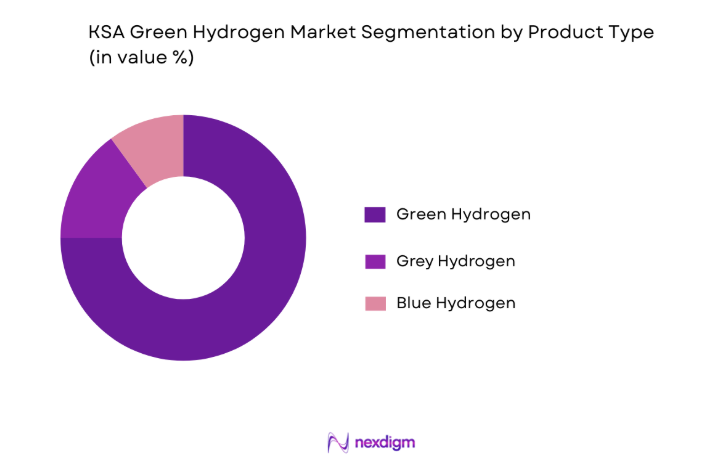

The KSA Green Hydrogen market is segmented by product type into green hydrogen, grey hydrogen, and blue hydrogen. Recently, green hydrogen has gained a dominant market share due to the rising demand for sustainable energy solutions. Factors such as the government’s focus on clean energy adoption, environmental concerns, and technological advancements in electrolysis processes have driven this shift. Additionally, large-scale investments in renewable energy projects aimed at increasing green hydrogen production are anticipated to further solidify its market share. The government’s dedication to creating a hydrogen economy has made green hydrogen the preferred choice in both domestic and international markets.

By End User Segment:

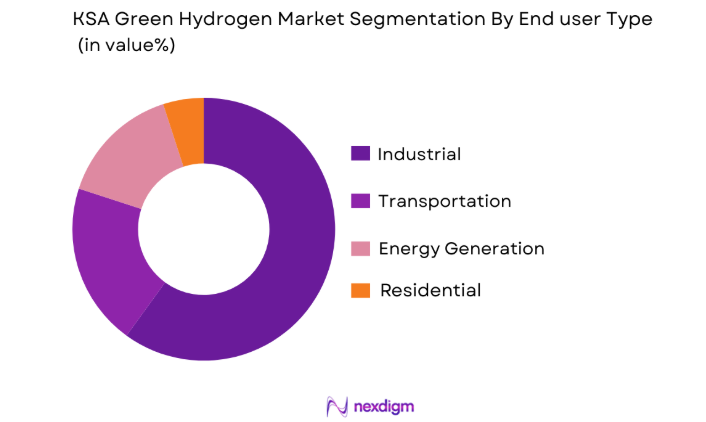

The KSA Green Hydrogen market is segmented by end user into industrial, transportation, energy generation, and residential sectors. The industrial sector currently holds the dominant market share, driven by its demand for clean energy sources for heavy industries such as refining, chemicals, and steel manufacturing. Green hydrogen is increasingly viewed as a crucial alternative to traditional fossil fuels in these industries, especially with the growing focus on reducing carbon emissions. The energy generation sector also shows strong potential, as green hydrogen can be used for power generation, storage, and in fuel cells, further contributing to the sector’s dominance in the market.

Competitive Landscape

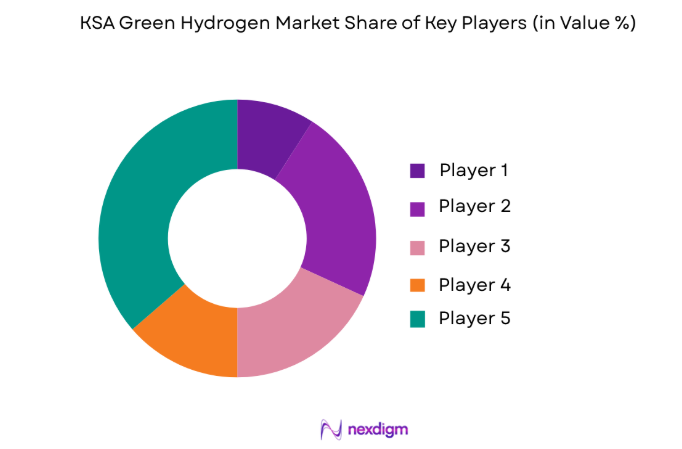

The KSA Green Hydrogen market is characterized by a competitive landscape driven by global and local players investing in large-scale projects and technological innovations. The market has seen considerable consolidation, with major energy firms forming strategic alliances to support green hydrogen production. Key players are focusing on developing the necessary infrastructure to increase production capacities, reduce costs, and enhance hydrogen distribution capabilities. As the market is in its early stages, the competitive dynamics are heavily influenced by government policies, subsidies, and long-term investments in renewable energy infrastructure.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Market Parameter |

| Saudi Aramco | 1933 | Dhahran, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| ACWA Power | 2002 | Riyadh, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Air Products | 1940 | Allentown, USA | ~ | ~ | ~ | ~ | ~ |

| Linde | 1879 | Munich, Germany | ~ | ~ | ~ | ~ | ~ |

| ENGIE | 2008 | Paris, France | ~ | ~ | ~ | ~ | ~ |

KSA Green Hydrogen Market Analysis

Growth Drivers

Government Support for Renewable Energy:

The Saudi government has aggressively supported renewable energy, with green hydrogen as a core part of its Vision 2030. This support comes in the form of regulatory incentives, tax breaks, and infrastructure investments, which are designed to accelerate the development of hydrogen production facilities. These policies are coupled with significant funding allocated to research and development of green hydrogen technologies, making it a leading driver in the growth of the green hydrogen market. As the government pushes towards a carbon-neutral future, the demand for green hydrogen, particularly for industrial and energy generation sectors, has grown significantly. Additionally, international collaborations and partnerships have enhanced the technological capabilities of the market, further driving growth in the sector.

Private Sector Investment and Technological Advancements:

The surge in private sector investments, driven by the demand for sustainable energy solutions, has been pivotal in the growth of the green hydrogen market. Large-scale hydrogen production projects, backed by global energy firms and local players, are expanding rapidly, significantly increasing production capacities. The ongoing advancements in electrolysis technology have made hydrogen production more efficient and cost-effective, which is crucial for the widespread adoption of green hydrogen in various sectors. These advancements, along with the increasing interest from international players, have resulted in a rapidly growing market, poised for significant development in the coming years.

Market Challenges

High Production Costs:

One of the primary challenges facing the KSA Green Hydrogen market is the high production cost of green hydrogen, which remains significantly higher than that of grey hydrogen. The costs associated with the electrolysis process, along with the infrastructure required for its production and distribution, contribute to the high overall cost. Although technological advancements are expected to bring down these costs over time, the current financial barriers hinder the market’s growth potential. Despite government subsidies and initiatives, the private sector is still hesitant to invest heavily without substantial cost reductions, which remains a significant challenge to the market’s wider adoption.

Lack of Infrastructure for Hydrogen Distribution:

The KSA Green Hydrogen market also faces challenges due to the lack of an established infrastructure for hydrogen storage, distribution, and refueling. While production capabilities are expanding, the current distribution network is insufficient to meet the growing demand for hydrogen, especially in the transportation sector. Building a hydrogen infrastructure requires significant investments in pipelines, storage facilities, and refueling stations, which poses logistical and financial challenges. Without a robust infrastructure, the widespread adoption of green hydrogen remains limited, especially in sectors that require reliable and efficient hydrogen delivery.

Opportunities

International Partnerships for Technology Sharing:

One significant opportunity for the KSA Green Hydrogen market lies in international collaborations that focus on sharing green hydrogen technologies. Saudi Arabia’s commitment to becoming a global leader in hydrogen production has led to partnerships with global energy companies and technology firms. These collaborations enable the exchange of knowledge, technology, and capital, which will accelerate the development of green hydrogen infrastructure and technologies. By leveraging the expertise of international firms, Saudi Arabia can reduce production costs, enhance technological capabilities, and develop a competitive edge in the global green hydrogen market.

Growing Demand in Transportation Sector:

As the global transportation sector increasingly focuses on reducing carbon emissions, there is a growing opportunity for KSA to tap into the hydrogen-powered vehicle market. Hydrogen fuel cell vehicles (FCVs) offer a clean alternative to traditional internal combustion engine vehicles, and their adoption is expected to rise sharply in the coming years. Saudi Arabia, with its strong energy sector and significant investments in green hydrogen, is well-positioned to capitalize on the transportation sector’s growing demand for hydrogen. This shift offers an immense opportunity for growth in both the domestic and international markets, further solidifying KSA’s position as a global hydrogen leader.

Future Outlook

The KSA Green Hydrogen market is expected to experience substantial growth over the next five years, driven by technological advancements, government support, and increasing demand for clean energy. The Kingdom’s push towards a sustainable, carbon-neutral economy is set to propel green hydrogen production and consumption across various sectors, including transportation and energy. Technological innovations in hydrogen production and storage will lower costs, while increasing infrastructure investments will enable widespread adoption. With strategic investments and international partnerships, Saudi Arabia is poised to become a dominant player in the global green hydrogen market, contributing significantly to the worldwide energy transition.

Major Players

- Saudi Aramco

- ACWA Power

- Air Products

- Linde

- ENGIE

- Shell

- TotalEnergies

- Siemens Energy

- Air Liquide

- Thyssenkrupp

- McKinsey & Company

- Vestas

- Mitsubishi Power

- Black & Veatch

- General Electric

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Energy companies

- Green technology developers

- Manufacturing and industrial sectors

- Transportation and automotive companies

- Hydrogen infrastructure developers

- Environmental organizations

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying key market drivers, challenges, and trends impacting the KSA Green Hydrogen market. This includes assessing technological innovations, government regulations, and economic factors that could influence market growth.

Step 2: Market Analysis and Construction

Market data is collected from multiple sources, including industry reports, market studies, and expert opinions, to create a comprehensive market model. This helps in understanding the current landscape and future trends.

Step 3: Hypothesis Validation and Expert Consultation

The developed hypotheses are validated by consulting industry experts, stakeholders, and key players. Insights gained from consultations help refine market projections and assumptions.

Step 4: Research Synthesis and Final Output

The final market report is synthesized, combining both qualitative and quantitative data. The results are presented in a detailed format, outlining key findings, future forecasts, and strategic recommendations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government support and policies for green hydrogen initiatives

Increased demand for clean energy solutions

Technological advancements in hydrogen production - Market Challenges

High capital investment requirements

Lack of infrastructure for widespread adoption

Regulatory and compliance barriers - Market Opportunities

Partnerships with international green hydrogen players

Development of storage and distribution infrastructure

Emerging demand from industrial sectors - Trends

Integration of green hydrogen in energy transition plans

Rise in adoption of hydrogen-powered vehicles

Increased investments in renewable energy technologies - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Electrolysis Systems

Green Hydrogen Storage Solutions

Green Hydrogen Transportation Systems

Renewable Power Generation for Hydrogen

Hydrogen Distribution Systems - By Platform Type (In Value%)

Ground Platforms

Offshore Platforms

Marine Platforms

Integrated Platforms

Modular Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Integrated Solutions

Modular Solutions - By EndUser Segment (In Value%)

Energy Sector

Industrial Applications

Transportation Sector

Government & Public Infrastructure

- Market Share Analysis

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

ACWA Power

Saudi Aramco

Air Products and Chemicals

National Industrialization Company (Tasnee)

NEOM

Siemens Energy

Hydrogenics

BASF

ENGIE

Linde

Shell

TotalEnergies

Babcock & Wilcox

Mitsubishi Power

Black & Veatch

McKinsey & Company

- Energy sector’s growing reliance on hydrogen solutions

- Industrial sectors seeking low-carbon alternatives

- Transport sector investments in hydrogen-based vehicles

- Private sector’s shift towards sustainable energy sources

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now