Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA hand gloves market is valued at approximately USD ~ billion in 2025, supported by demand from healthcare, oil & gas, food processing, and industrial safety sectors. Saudi Arabia recorded healthcare expenditure exceeding USD 50 billion, while the Ministry of Health operates over 290 hospitals and 2,300 primary healthcare centers, creating continuous consumption of medical gloves. Industrial activity, supported by non-oil GDP of USD ~ billion, further drives glove demand across manufacturing and construction sectors. Rising workforce participation and regulatory compliance for hygiene and safety contribute significantly to market expansion.

The KSA hand gloves market is concentrated in Riyadh, Jeddah, Eastern Province, and Makkah due to strong industrial, healthcare, and logistics infrastructure. Riyadh dominates due to the presence of government hospitals, corporate healthcare chains, and procurement hubs. Eastern Province supports demand through oil & gas facilities and petrochemical industries. Jeddah and Makkah contribute through food processing, hospitality, and large-scale pilgrim inflow requiring hygiene products. These regions benefit from advanced infrastructure, higher population density, and concentration of industrial zones, making them key demand centers for gloves.

Market Segmentation

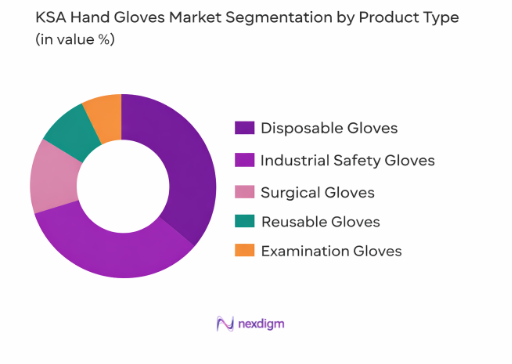

By Product Type

KSA hand gloves market is segmented by product type into disposable gloves, reusable gloves, surgical gloves, examination gloves, and industrial safety gloves. Disposable gloves dominate the market due to their widespread usage across healthcare facilities, food handling, and cleaning applications. Hospitals and clinics require single-use gloves to maintain infection control standards, especially with increasing patient volumes and surgical procedures. Additionally, food safety regulations and hygiene standards in restaurants and catering services drive disposable glove usage. The ease of use, lower contamination risk, and regulatory compliance requirements make disposable gloves the preferred choice across sectors. Industrial safety gloves also have significant demand, but disposable gloves lead due to continuous consumption in healthcare and hygiene-sensitive environments.

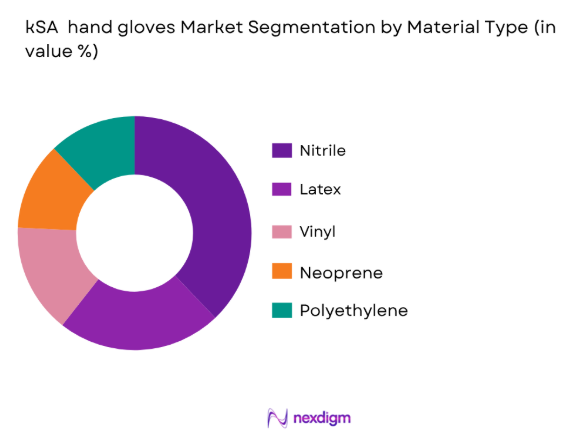

By Material Type

KSA hand gloves market is segmented by material type into latex gloves, nitrile gloves, vinyl gloves, neoprene gloves, and polyethylene gloves. Nitrile gloves dominate the market due to their superior durability, chemical resistance, and hypoallergenic properties compared to latex gloves. Healthcare providers prefer nitrile gloves to avoid allergic reactions, while industrial sectors use them for handling chemicals and hazardous materials. Additionally, nitrile gloves offer better puncture resistance and longer shelf life, making them suitable for oil & gas and manufacturing applications. The increasing focus on safety compliance and high-performance protective equipment has led to a shift from latex to nitrile gloves, strengthening their dominance in the market.

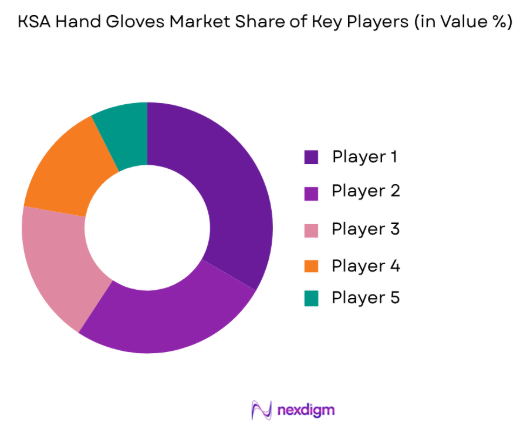

Competitive Landscape

The KSA hand gloves market is characterized by the presence of both international and regional players, with strong competition driven by product quality, pricing, and distribution networks. Global manufacturers such as Ansell and Top Glove supply high-quality products, while regional companies focus on cost competitiveness and local distribution. The market remains moderately fragmented, with key players leveraging partnerships with healthcare institutions and industrial buyers to strengthen their presence.

| Company | Establishment Year | Headquarters | Product Focus | Production Capacity | Distribution Network | Key Industries Served | Import/Local Presence | Competitive Advantage |

| Ansell Limited | 1893 | Australia | ~ | ~ | ~ | ~ | ~ | ~ |

| Top Glove Corporation | 1991 | Malaysia | ~ | ~ | ~ | ~ | ~ | ~ |

| Hartalega Holdings | 1988 | Malaysia | ~ | ~ | ~ | ~ | ~ | ~ |

| SPIMACO | 1986 | Saudi Arabia | ~ | ~ | ~ | ~ | ~ | ~ |

| 3M Gulf | 1902 | USA | ~ | ~ | ~ | ~ | ~ | ~ |

KSA Hand Gloves Market Analysis

Growth Drivers

Expansion of Healthcare Infrastructure and Medical Services

KSA hand gloves demand is strongly driven by the expanding healthcare system, which requires continuous consumption of surgical and examination gloves. Saudi Arabia operates more than 290 hospitals and over 2,300 primary healthcare centers, ensuring steady usage of medical consumables. Government health expenditure exceeded USD 50 billion, reflecting strong institutional procurement capacity. The population reached 36.4 million, increasing patient volumes and medical procedures. Additionally, Vision 2030 focuses on privatization and healthcare expansion, leading to new hospital projects and diagnostic centers, further increasing glove consumption across public and private healthcare facilities and strengthening demand for infection-control products.

Growth in Industrial and Oil & Gas Sector Activities

KSA hand gloves demand is significantly supported by industrial expansion and oil & gas activities requiring worker safety equipment. Saudi Arabia’s oil production exceeded 9 million barrels per day, while the energy sector remains a major employer requiring protective gear. Non-oil GDP reached USD 453 billion, driven by manufacturing, construction, and logistics sectors. Industrial cities such as Jubail and Yanbu host petrochemical complexes and factories where gloves are essential for chemical handling and worker protection. The presence of over 10,000 industrial facilities across the Kingdom creates continuous demand for industrial safety gloves across multiple sectors.

Market Challenges

High Dependence on Imports

KSA hand gloves market faces challenges due to reliance on imported gloves and raw materials. Saudi Arabia imports a significant portion of its medical and industrial gloves from countries such as Malaysia, China, and Thailand. Total imports of medical devices exceeded USD 4 billion, reflecting dependency on foreign suppliers. Disruptions in global supply chains, shipping delays, and geopolitical factors can affect availability and lead times. The absence of large-scale domestic glove manufacturing facilities increases reliance on imports, making the market vulnerable to external supply shocks and limiting local production capabilities.

Regulatory Compliance and Quality Standards

KSA hand gloves market is influenced by strict regulatory frameworks governing medical and industrial safety products. The Saudi Food and Drug Authority regulates medical devices, requiring certification, testing, and compliance before market entry. Industrial gloves must also comply with occupational safety standards enforced by labor authorities. Companies must adhere to international standards such as ISO certifications, increasing operational complexity. Delays in approvals and compliance requirements can affect product availability. Additionally, maintaining consistent product quality across imported and locally distributed gloves remains a challenge for suppliers operating in the Kingdom.

Opportunities

Growth in Local Manufacturing Initiatives

KSA hand gloves market has strong opportunities through local manufacturing initiatives supported by Vision 2030. Saudi Arabia aims to increase domestic production of medical supplies, reducing reliance on imports. The industrial sector contributes significantly to GDP, with ongoing investments in manufacturing zones and industrial clusters. Government programs such as the National Industrial Development and Logistics Program support local production capabilities. Establishing glove manufacturing plants can leverage access to regional markets and reduce supply chain risks. Increasing localization efforts provide opportunities for domestic players to enter the glove manufacturing sector and strengthen supply resilience.

Increasing Demand for Nitrile and Powder-Free Gloves

KSA hand gloves market is witnessing rising demand for nitrile and powder-free gloves due to safety and hygiene requirements. Healthcare facilities prefer nitrile gloves to reduce allergic reactions associated with latex, while industrial sectors require chemical-resistant gloves. The growing number of hospitals and diagnostic centers increases demand for high-quality disposable gloves. Food processing and hospitality sectors also require powder-free gloves to maintain hygiene standards. With increasing awareness of infection control and workplace safety, demand for advanced glove materials continues to rise, creating opportunities for manufacturers and suppliers to expand their product portfolios.

Future Outlook

Over the next five years, the KSA hand gloves market is expected to experience steady growth driven by healthcare expansion, industrial diversification, and rising hygiene awareness. Government initiatives under Vision 2030 aim to enhance healthcare infrastructure and local manufacturing capabilities, which will increase demand for medical and industrial gloves.

The oil & gas sector and construction industry will continue to drive demand for industrial safety gloves, while the food processing and hospitality sectors will support disposable glove consumption. Increasing adoption of nitrile gloves and advancements in manufacturing technology will further contribute to market development.

Major Players

- Top Glove Corporation

- Hartalega Holdings Berhad

- Kossan Rubber Industries

- Ansell Limited

- Supermax Corporation

- Riverstone Holdings

- Kimberly-Clark Corporation

- Medicom Group

- Sempermed

- AMMEX Corporation

- SPIMACO

- Arabian Medical Products Manufacturing Company

- B. Braun Saudi Arabia

- 3M Gulf

- Al Gihaz Medical Supplies

Key Target Audience

- Healthcare providers and hospital procurement departments

- Industrial manufacturing companies

- Oil and gas companies

- Food processing and hospitality businesses

- Retail and wholesale distributors

- Investments and venture capitalist firms

- Government and regulatory bodies

- Occupational safety and compliance organizations

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping stakeholders in the KSA hand gloves market, including manufacturers, distributors, healthcare institutions, and industrial users. Secondary data sources such as government publications and trade statistics are used to identify key variables affecting demand and supply dynamics.

Step 2: Market Analysis and Construction

Historical data is analyzed to understand consumption trends, industrial output, and healthcare utilization. The study evaluates glove usage across sectors and distribution channels to construct a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts are consulted to validate assumptions and provide insights into demand patterns, pricing strategies, and operational challenges. These interactions ensure the reliability of market estimates.

Step 4: Research Synthesis and Final Output

The final phase integrates primary and secondary research findings to deliver a validated market assessment. Data triangulation ensures accuracy and consistency in the analysis.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Consolidated Research Approach, Understanding Market Potential Through In-Depth Industry Interviews, Primary Research Approach, Limitations and Future Conclusions)

- Definition and Scope

- Market Dynamics Overview

- Market Genesis

- Major Players and Market Timeline

- Business Cycle and Trends

- Supply Chain and Value Chain Analysis

- Growth Drivers

Expansion of Healthcare Infrastructure and Medical Services

Growth in Industrial and Oil & Gas Sector Activities

Increasing Focus on Workplace Safety and Hygiene

Rising Demand from Food Processing and Hospitality Sector - Market Challenges

High Dependence on Imports

Price Sensitivity and Competitive Market Structure

Fluctuations in Raw Material Availability

Regulatory Compliance and Quality Standards - Opportunities

Growth in Local Manufacturing Initiatives

Increasing Demand for Nitrile and Powder-Free Gloves

Expansion of E-commerce and Medical Supply Chains

Rising Healthcare Investments under Vision 2030

- Key Trends

Shift toward nitrile and synthetic gloves

Rising demand for disposable single use gloves

Growth in industrial safety glove applications

Increasing focus on workplace safety compliance

Innovation in high performance glove products - Government Regulation

- SWOT Analysis

- Porter’s Five Forces

- By Value, 2020–2025

- By Volume, 2020–2025

- By Average Price, 2020–2025

- By Product Type (In Value %)

Disposable Gloves

Reusable Gloves

Surgical Gloves

Examination Gloves

Industrial Safety Gloves - By Material Type (In Value %)

Latex

Nitrile

Vinyl

Neoprene

Polyethylene - By Application (In Value %)

Healthcare

Industrial Manufacturing

Food Processing

Oil and Gas

Household and Cleaning - By Distribution Channel (In Value %)

Direct Sales

Distributors and Wholesalers

Retail Pharmacies

Online Channels - By Region (In Value %)

Riyadh

Jeddah

Eastern Province

Makkah

- Market Share of Major Players by Value/Volume

- Market Share of Major Players by Product Type

- Cross Comparison Parameters (Company Overview, Business Strategies, Recent Developments, Strength, Weakness, Organizational Structure, Revenues, Revenues by Product Type, Number of Touchpoints, Distribution Channels, Number of Dealers and Distributors, Margins, Production Plant, Capacity, Unique Value Offering and Others)

- SWOT Analysis of Major Players

- Pricing Analysis Based on Product Categories for Major Players

- Detailed Profiles of Major Companies

Top Glove Corporation

Hartalega Holdings Berhad

Kossan Rubber Industries

Ansell Limited

Supermax Corporation

Riverstone Holdings

Kimberly-Clark Corporation

Medicom Group

Sempermed

AMMEX Corporation

Al Gihaz Medical Supplies

Arabian Medical Products Manufacturing Company

Saudi Pharmaceutical Industries and Medical Appliances Corporation

B. Braun Saudi Arabia

3M Gulf

- Market Demand and Utilization

- Purchasing Power and Budget Allocations

- Regulatory and Compliance Requirements

- Needs, Desires, and Pain Point Analysis

- Decision-Making Process

- By Value, 2026–2035

- By Volume, 2026–2035

- By Average Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now