Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA healthcare infrastructure market is being shaped by a large, state-backed expansion pipeline tied to Vision 2030 and the Health Sector Transformation Program. Based on a recent historical assessment, the market is anchored by more than USD ~ billion in planned healthcare infrastructure investment, covering hospitals, primary care assets, medical cities, and digitally enabled facilities. Growth is being driven by public spending, privatization initiatives, insurance expansion, and a widening role for private operators in healthcare delivery and asset development.

Riyadh and the Makkah region dominate healthcare infrastructure development because they combine high population concentration, stronger hospital density, large referral flows, and priority project execution under national reform programs. Official statistics show Riyadh leading the Kingdom in hospital count, followed by Makkah, while approved Ministry of Health projects also highlight major developments in Riyadh, Jeddah, Dammam, and Al Ahsa. These cities remain central because they offer better specialist availability, stronger reimbursement economics, and greater attractiveness for private healthcare investment.

Market Segmentation

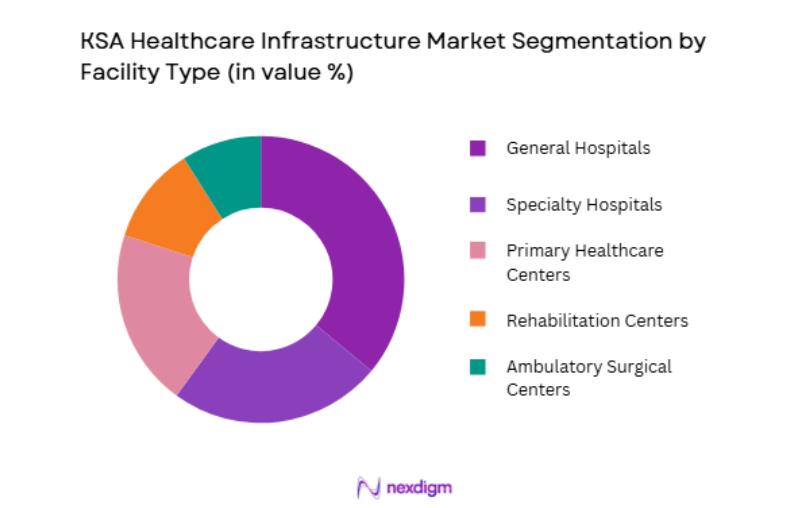

By Facility Type

KSA Healthcare Infrastructure market is segmented by facility type into general hospitals, specialty hospitals, primary healthcare centers, rehabilitation centers, and ambulatory surgical centers. Recently, general hospitals has a dominant market share due to factors such as broad service coverage, higher bed capacity, stronger public funding support, and their central role within regional referral systems. Large public and private operators continue to prioritize general hospitals because they anchor emergency care, inpatient treatment, diagnostics, surgery, maternity services, and specialist referrals within one integrated asset. They also attract the highest capital allocation because they require extensive land, complex engineering systems, medical equipment deployment, and long term facility management.

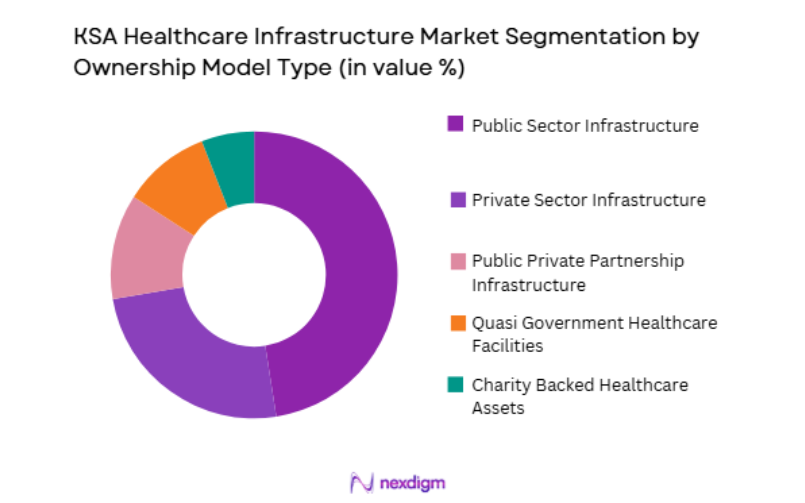

By Ownership Model

KSA Healthcare Infrastructure market is segmented by product type into public sector infrastructure, private sector infrastructure, public private partnership infrastructure, quasi government healthcare facilities, and charity backed healthcare assets. Recently, public sector infrastructure has a dominant market share due to factors such as sovereign funding strength, extensive nationwide coverage, historical ownership of hospital capacity, and the government’s leading role in regional healthcare access. Public entities continue to control the broadest hospital network and remain the principal sponsors of large medical complexes, primary care expansion, and regional capacity additions. Their dominance is reinforced by national health transformation policies that prioritize service availability across all regions and support large scale infrastructure planning through ministries, health clusters, and affiliated state entities.

Competitive Landscape

The KSA healthcare infrastructure market is moderately concentrated around large hospital operators, integrated healthcare groups, and experienced developers that can combine capital deployment with clinical operations and expansion execution. Listed healthcare providers are increasing capacity through new towers, specialty facilities, and multi city networks, while policy reforms continue to draw private capital into hospital development, rehabilitation assets, and specialized care infrastructure. At the same time, the public sector remains the largest anchor for major infrastructure projects through clusters, ministry programs, and long duration expansion plans.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Installed Capacity |

| Dr. Sulaiman Al Habib Medical Services Group | 1993 | Riyadh, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Dallah Healthcare | 1987 | Riyadh, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Mouwasat Medical Services | 1975 | Dammam, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Fakeeh Care Group | 1978 | Jeddah, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Almoosa Health | 1996 | Al Ahsa, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

KSA Healthcare Infrastructure Market Analysis

Growth Drivers

Vision 2030 Health Sector Transformation and PPP Expansion

Saudi Arabia’s healthcare infrastructure market is being driven by a state-led expansion program that combines public spending, cluster restructuring, privatization, and public private partnerships to add hospitals, primary care centers, rehabilitation assets, and digitally enabled care facilities across the Kingdom. The Health Sector Transformation Program has made capacity expansion a core pillar of reform, while sector publications indicate the Kingdom plans to invest more than USD ~ in healthcare infrastructure, creating a large and visible project pipeline for developers, operators, medical technology vendors, and engineering contractors. Official statistics also show the country reached 516 hospitals in 2024, confirming that infrastructure growth is already materializing rather than remaining a purely announced target. The government’s cluster model is reshaping ownership and operational accountability, which is improving project bankability and making infrastructure development more attractive to private investors seeking long term healthcare assets. Parallel reforms in insurance coverage, localization, and service quality are raising utilization expectations, which in turn supports expansion of bed capacity, ambulatory centers, and specialized facilities in major urban corridors. Approved Ministry of Health projects in Riyadh, Jeddah, Dammam, Al Ahsa, and other regions demonstrate that expansion is geographically broad and not limited to one flagship city. Because the program includes design, construction, medical equipment deployment, information systems, and facility management, it stimulates demand across the full healthcare infrastructure value chain rather than only hospital shell construction.

Population Growth Urban Concentration and Rising Utilization of Complex Care Assets

Saudi Arabia’s healthcare infrastructure market is also being accelerated by demographic pressure, urban concentration, and rising demand for higher acuity care assets that require continuous expansion of physical capacity, specialized equipment space, and integrated support services. Large metropolitan regions already carry the highest hospital counts, with official data showing Riyadh at 115 hospitals and Makkah at 99, which reflects where infrastructure demand is most intense and where future additions can be absorbed quickly by growing patient volumes. Population growth, longer life expectancy, noncommunicable disease prevalence, and the broadening of insurance based care are increasing demand for surgery centers, dialysis units, oncology facilities, women’s health assets, rehabilitation infrastructure, and diagnostic platforms. These needs cannot be met only through operational improvement inside existing buildings, because many service lines require purpose built facilities, more beds, upgraded mechanical systems, and technologically advanced layouts. The continued rise of private hospital groups is reinforcing this pattern by expanding multi city networks and investing in new towers, outpatient complexes, and specialty hospitals to capture insured demand and referral flows. At the same time, digital care does not reduce the need for infrastructure in Saudi Arabia, because virtual models still depend on command centers, imaging networks, connected primary care sites, and modern hospitals capable of handling escalated cases. Approved public projects in major cities and secondary regions show that capacity planning is shifting toward broader geographic coverage, but metropolitan centers remain the anchors because they combine population density, specialist availability, airport connectivity, and stronger reimbursement economics.

Market Challenges

Project Execution Complexity and Extended Delivery Timelines

One of the main challenges in the KSA healthcare infrastructure market is the difficulty of executing large healthcare projects on time and within budget while meeting demanding clinical, engineering, digital, and regulatory specifications across multiple regions. Hospitals and medical cities are more complex than ordinary commercial buildings because they require specialized airflow systems, infection control designs, medical gas networks, imaging suites, surgical environments, resilient power systems, and tightly coordinated digital infrastructure. This complexity increases procurement risk and lengthens delivery cycles, especially when projects involve imported equipment, phased commissioning, and integration with existing public health assets or cluster level operating models. The Kingdom’s broader construction surge intensifies the problem by competing for the same pool of contractors, specialist subcontractors, consultants, and materials across housing, transport, tourism, and industrial megaprojects. Even when funding is available, delays in design coordination, utility readiness, land preparation, or licensing can push back completion dates and postpone the start of revenue generating operations for hospital operators. Healthcare projects also face a narrow tolerance for commissioning errors, because any failure in infection control, medical equipment calibration, nurse call systems, or digital record integration can disrupt clinical readiness. As private investors enter through PPP structures and operating concessions, they must manage not only construction risk but also long term service obligations tied to utilization, quality, and maintenance performance. Secondary cities can face additional challenges from thinner contractor ecosystems and more limited availability of specialized project management talent, which may require external mobilization and increase costs.

Workforce Availability Localization Pressure and Operating Readiness Gaps

A second major challenge for the KSA healthcare infrastructure market is that building facilities is easier than making them fully operational, because hospitals and specialty centers require large numbers of qualified clinicians, technicians, managers, biomedical engineers, and support staff before new capacity can function effectively. Official data show sizable workforces across physicians, nurses, pharmacists, and dentists, yet the sector still relies heavily on non Saudi professionals in many clinical areas, which highlights the difficulty of aligning rapid infrastructure growth with workforce localization goals and long term staffing stability. New projects in specialized care segments such as oncology, cardiac services, rehabilitation, and complex surgery need highly trained multidisciplinary teams, and those teams cannot always be recruited at the same pace as buildings are delivered. This creates a risk that newly completed assets may open gradually, operate below design capacity, or require extended ramp up periods before reaching targeted occupancy and case mix. Staffing challenges also affect rural and secondary cities more sharply, because specialist attraction and retention are harder outside major urban centers such as Riyadh, Jeddah, and Dammam. In addition, digital transformation raises the bar for operational readiness by requiring information technology staff, cybersecurity capabilities, telehealth workflows, and data integration teams alongside traditional clinical hiring. Private operators must therefore plan recruitment, training, and retention well in advance, while public authorities must continue to improve workforce pipelines and licensing efficiency. If workforce readiness lags construction activity, infrastructure returns may be diluted and patient access gains may materialize more slowly than planners expect.

Opportunities

PPP Led Development of Integrated Care Networks and Asset Platforms

One of the clearest opportunities in the KSA healthcare infrastructure market is the development of integrated asset platforms through public private partnerships that combine design, financing, construction, operations support, and lifecycle maintenance across hospitals, primary care centers, rehabilitation facilities, and ancillary services. Saudi Arabia’s reform agenda explicitly seeks greater private sector participation, and earlier sector documents from the Ministry of Investment pointed to multiple build and operate opportunities across hospitals, medical cities, and primary care infrastructure. That policy direction creates room not only for single asset concessions but also for scalable portfolios in which investors and operators can standardize procurement, maintenance, digital systems, and clinical support across several facilities. Such platform models are especially attractive in a market where public demand is large, sovereign commitment is visible, and long duration healthcare assets can generate relatively defensive cash flows once utilization stabilizes. Investors that enter early can build local delivery capability, establish relationships with health clusters, and position themselves for repeat mandates as the pipeline broadens. There is also significant whitespace in support infrastructure including laboratories, logistics hubs, rehabilitation assets, long term care, ambulatory surgery facilities, and digitally linked primary care sites that can complement flagship hospitals. Because Vision 2030 reforms increasingly favor networked care rather than isolated institutions, the strongest opportunity may lie in integrated systems that connect referral pathways, diagnostics, specialty treatment, and post acute care under unified operational frameworks. This creates demand for healthcare real estate specialists, medical equipment companies, facility managers, and technology providers alongside hospital operators.

Expansion of Specialized and Digitally Enabled Infrastructure Beyond Core Metropolitan Hospitals

Another major opportunity in the KSA healthcare infrastructure market is the expansion of specialized and digitally enabled assets beyond the largest traditional hospitals, because the Kingdom’s future care model increasingly depends on distributed infrastructure that can manage patients closer to home while still connecting them to advanced tertiary expertise. The Seha Virtual Hospital already supports hundreds of hospitals around the Kingdom and shows that Saudi Arabia is building a hybrid architecture in which command centers, connected facilities, remote diagnostics, and specialist referral networks complement physical hospitals instead of replacing them. This opens a broad investment case for oncology centers, dialysis clinics, rehabilitation hospitals, women’s and children’s facilities, day surgery units, chronic disease centers, diagnostic hubs, and smart primary care sites that are digitally linked into larger clusters. Such assets are often smaller and faster to deliver than full tertiary hospitals, which can improve speed to market and allow investors to target specific regional gaps in access or specialty care. They are also well suited to mixed operating models in which public purchasers, private providers, and technology firms share responsibilities for care delivery, equipment, and data systems. As insurance penetration rises and patient expectations shift toward convenience, shorter travel times, and coordinated care pathways, distributed specialty infrastructure becomes more commercially compelling. Secondary cities and growth corridors represent an especially important opportunity because the national hospital map still shows concentration in Riyadh and Makkah, leaving room for targeted capacity additions elsewhere.

Future Outlook

The KSA healthcare infrastructure market is expected to remain on a strong expansion path over the next five years as Vision 2030 reforms continue to push capacity creation, private participation, and technology enabled models of care. New hospitals, specialty assets, rehabilitation facilities, and distributed primary care infrastructure are likely to expand alongside digital command centers and hybrid delivery systems. Regulatory support for privatization and health cluster transformation should continue improving project visibility for investors and operators.

Major Players

- Dr. Sulaiman Al Habib Medical Services Group

- Dallah Healthcare

- Mouwasat Medical Services

- Fakeeh Care Group

- Almoosa Health

- Saudi German Health

- Care Medical

- National Medical Care Company

- Burjeel Medical City Saudi projects

- Health Holding Company

- NUPCO

- Tamasuk Holding

- Nesma & Partners

- El Seif Engineering Contracting

- Saudi Binladin Group

Key Target Audience

- Private hospital groups

- Healthcare infrastructure developers

- Medical equipment manufacturers

- Health facility management companies

- Health insurance providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Public private partnership investors

Research Methodology

Step 1: Identification of Key Variables

Key variables were identified through review of official healthcare transformation documents, hospital and workforce statistics, ministry project disclosures, and listed healthcare operator filings. The analysis focused on hospital counts, investment commitments, ownership models, regional concentration, privatization trends, and capacity expansion themes shaping infrastructure demand.

Step 2: Market Analysis and Construction

The market structure was constructed by mapping healthcare infrastructure into facility type and ownership model, then aligning each with project activity, operator expansion, and public system dominance. Competitive positioning was developed using company disclosures on revenues, network footprint, and operating assets.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions were validated against official Vision 2030 and health sector materials, exchange disclosures, and operator level reporting to check whether infrastructure growth is translating into active expansion by both public and private stakeholders. This step was used to confirm that hospitals, specialty centers, and digitally enabled assets are all participating in the buildout.

Step 4: Research Synthesis and Final Output

The final output was synthesized by combining official statistics, policy documents, company financials, and project evidence into a single market narrative. Where no single public source provided a full segment share breakdown, the segmentation split was analytically apportioned based on asset intensity, operator mix, and infrastructure concentration.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government investments under Vision 2030 healthcare initiatives

Rising demand for advanced medical facilities due to population growth

Expansion of private hospital networks and specialty care centers - Market Challenges

High capital requirements for healthcare infrastructure projects

Dependence on imported medical equipment and technology

Shortage of specialized healthcare professionals - Market Opportunities

Development of integrated healthcare cities and medical free zones

Expansion of specialty hospitals targeting international patients

Investment in digitally integrated smart hospital infrastructure - Trends

Adoption of smart hospital technologies and AI enabled healthcare systems

Growth of specialized centers for oncology, cardiology, and fertility treatments - Government Regulations

Healthcare licensing and accreditation under Saudi Ministry of Health

Regulatory standards for hospital infrastructure and medical equipment

Policies supporting medical tourism and healthcare infrastructure expansion - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Hospital Infrastructure Development

Specialty Medical Center Infrastructure

Ambulatory Surgical Center Infrastructure

Diagnostic and Imaging Center Infrastructure

Primary Healthcare Clinic Infrastructure - By Platform Type (In Value%)

Public Healthcare Infrastructure

Private Healthcare Infrastructure

Public Private Partnership Healthcare Projects

Medical Free Zone Healthcare Facilities

Integrated Healthcare City Developments - By Fitment Type (In Value%)

New Hospital Construction Projects

Hospital Expansion and Capacity Upgrade Projects

Advanced Medical Equipment Infrastructure Integration

Smart Hospital Digital Infrastructure - By End User Segment (In Value%)

Government Healthcare Authorities

Private Hospital Groups

Diagnostic and Specialty Medical Centers

- Market Share Analysis

- Cross Comparison Parameters (Hospital Bed Capacity Expansion, Infrastructure Investment Scale, Technology Integration Level, Specialty Care Capability, Healthcare Accreditation Standards, Smart Hospital Integration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Saudi German Hospitals

King Faisal Specialist Hospital & Research Centre

Dr. Sulaiman Al Habib Medical Group

Mouwasat Medical Services

Al Hammadi Hospital Group

Al Mouwasat Hospitals

National Guard Health Affairs

Riyadh Care Hospital Group

King Abdulaziz Medical City

Saudi Aramco Medical Services

International Medical Center

Dallah Hospital Group

Al Borg Medical Laboratories

Badr Al Samaa Group

Saudi Medical Services Company

- Government authorities expanding public hospitals and clinics

- Private hospital groups investing in multi specialty medical facilities

- Diagnostic centers deploying advanced imaging and laboratory infrastructure

- Medical tourism providers developing specialized treatment centers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now