Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the KSA home finance market reached approximately USD ~ billion in new residential mortgage originations, while the total outstanding housing loan portfolio stood near USD ~ billion, reflecting sustained credit expansion supported by state housing initiatives and banking sector liquidity. Market activity is driven by subsidized mortgage programs, urban household formation, and institutional lending growth, with regulated Sharia-compliant financing structures strengthening borrower accessibility and long-tenor affordability across residential segments nationwide.

Riyadh and Jeddah dominate the KSA home finance market due to concentration of population, employment hubs, and large-scale residential developments aligned with national housing programs. These cities host major lenders, developers, and digital mortgage platforms, enabling faster origination volumes and diversified property supply. Dammam and Eastern Province also show strong financing activity supported by industrial employment clusters and planned housing communities, reinforcing urban dominance in mortgage demand formation and loan disbursement intensity.

Market Segmentation

By Product Type

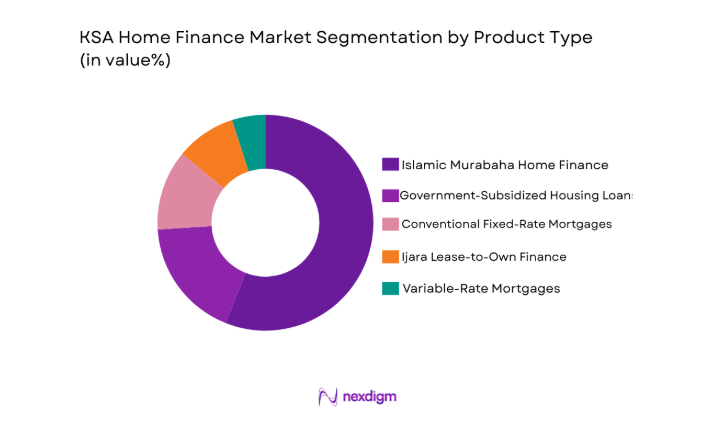

KSA home finance market is segmented by product type into conventional fixed-rate mortgages, variable-rate mortgages, Islamic Murabaha home finance, Ijara lease-to-own finance, and government-subsidized housing loans. Recently, Islamic Murabaha home finance has a dominant market share due to alignment with Sharia compliance requirements, strong bank product availability, regulatory endorsement, and borrower preference for fixed repayment certainty within long-term housing finance contracts across Saudi nationals.

By Platform Type

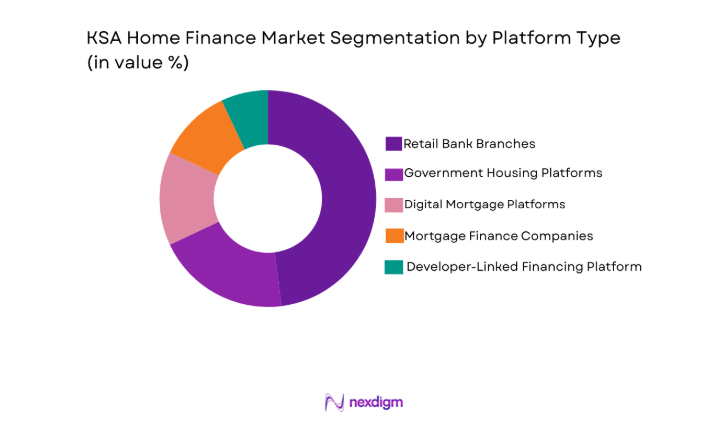

KSA home finance market is segmented by platform type into retail bank branches, digital mortgage platforms, mortgage finance companies, government housing portals, and developer-linked financing platforms. Recently, retail bank branches have a dominant market share due to established customer trust, nationwide physical distribution, payroll-linked lending relationships, and integration with government subsidy processing channels that facilitate mortgage approvals and disbursements at scale across primary urban housing markets.

Competitive Landscape

The KSA home finance market is moderately consolidated, with large domestic banks controlling the majority of mortgage portfolios through subsidized lending channels and Sharia-compliant product dominance. Specialized housing finance companies compete in niche borrower segments and refinancing markets, while digital origination platforms are expanding partnerships with developers and government programs, increasing competitive intensity and innovation in underwriting, processing speed, and borrower acquisition strategies.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Portfolio Size |

| Al Rajhi Bank | 1957 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Saudi National Bank | 1953 | Jeddah | ~ | ~ | ~ | ~ | ~ |

| Riyad Bank | 1957 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Bidaya Home Finance | 2011 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Dar Al Tamleek | 2008 | Jeddah | ~ | ~ | ~ | ~ | ~ |

KSA Home Finance Market Analysis

Growth Drivers

Vision-Aligned Homeownership Expansion Programs

Vision-Aligned Homeownership Expansion Programs are transforming the KSA home finance market by structurally increasing mortgage demand through large-scale subsidized lending initiatives, eligibility expansion, and supply-side housing development partnerships that collectively elevate household borrowing capacity and formal financing penetration. Government-backed housing programs provide down-payment support, interest subsidies, and guaranteed funding lines to banks, enabling lenders to extend long-tenor Sharia-compliant mortgages to previously underserved middle-income households and first-time buyers across urban regions. These programs stimulate residential construction pipelines, ensuring a continuous flow of financeable housing inventory aligned with national homeownership targets and population growth trajectories. Banks benefit from reduced credit risk exposure due to subsidy structures and repayment guarantees, allowing portfolio expansion while maintaining regulatory capital stability. Mortgage accessibility has improved through standardized underwriting frameworks and centralized subsidy processing platforms that accelerate approval timelines and reduce borrower entry barriers. Rising homeownership aspiration among young Saudi households further amplifies uptake of subsidized mortgages, reinforcing structural demand visibility for lenders and developers. Institutional funding channels supporting housing finance liquidity have strengthened balance sheet capacity of major banks and specialized mortgage firms, enabling sustained loan origination growth. Integration of government housing portals with banking systems enhances borrower acquisition efficiency and market transparency, supporting scale expansion. The cumulative effect of policy-led financing expansion and demographic demand ensures long-term structural growth momentum across the KSA home finance ecosystem.

Banking Sector Digital Mortgage Transformation

Banking Sector Digital Mortgage Transformation is accelerating efficiency and accessibility in the KSA home finance market by shifting origination, underwriting, and approval processes toward integrated digital platforms that reduce processing time and enhance borrower experience across major urban lending hubs. Digital onboarding systems allow applicants to submit income data, property details, and subsidy eligibility information remotely, reducing dependency on physical branch visits and enabling nationwide reach for lenders. Automated credit scoring models and property valuation analytics improve risk assessment accuracy, allowing faster loan approvals and consistent underwriting standards across institutions. Integration with national identity databases and employer payroll systems enhances verification reliability and fraud mitigation, strengthening lender confidence in extending housing finance. Digital mortgage journeys shorten approval cycles significantly, improving conversion rates and borrower satisfaction, particularly among younger technology-oriented households entering the housing market. Banks also benefit from lower operational costs and scalable processing capacity, enabling higher loan volumes without proportional branch expansion. Partnerships between lenders, developers, and digital platforms create seamless property-finance ecosystems where buyers can secure financing at point of sale, reinforcing mortgage penetration. Regulatory support for digital banking innovation further legitimizes remote mortgage origination and electronic documentation acceptance. The transition toward digital mortgage infrastructure is therefore a central growth catalyst improving market efficiency, reach, and scalability across the KSA home finance sector.

Market Challenges

Housing Affordability Constraints Amid Price Inflation

Housing Affordability Constraints Amid Price Inflation are creating structural pressures within the KSA home finance market as residential property prices in major cities increase faster than household income growth, reducing effective borrowing capacity even under subsidized mortgage frameworks. Elevated land costs and construction expenses raise property values, requiring larger loan amounts and higher down-payment contributions from borrowers. Although subsidies offset financing costs, total repayment obligations remain substantial for middle-income households, constraining eligibility thresholds under regulated debt-burden ratios. Affordability gaps are particularly visible in Riyadh and Jeddah where demand concentration and limited affordable housing supply drive price escalation across primary residential zones. Lenders face rising loan-to-value risk exposure when financing higher-priced properties, necessitating stricter underwriting criteria that further restrict borrower access. Developers also prioritize higher-margin housing segments, limiting inventory of affordable units suitable for subsidized mortgage beneficiaries. Inflation in construction materials and labor compounds housing cost pressures, reinforcing upward price trends in new developments. Borrowers increasingly rely on extended tenors to manage repayment burdens, raising lifetime financing costs and default sensitivity. The interaction of price inflation, income constraints, and supply limitations therefore remains a persistent affordability challenge affecting mortgage growth inclusivity across the KSA home finance ecosystem.

Interest Rate Sensitivity and Financing Cost Volatility

Interest Rate Sensitivity and Financing Cost Volatility represent a significant challenge for the KSA home finance market as mortgage pricing remains influenced by monetary policy cycles and funding cost fluctuations affecting bank lending rates and borrower affordability thresholds. Rising benchmark rates increase monthly repayment obligations on new mortgages and refinancing loans, reducing effective demand among price-sensitive households and delaying purchase decisions. Although subsidized programs mitigate some cost increases, unsubsidized and higher-income borrowers remain exposed to full interest rate movements. Banks also experience higher funding costs in wholesale and deposit markets, compressing lending margins and constraining mortgage portfolio expansion incentives. Rate volatility creates uncertainty for borrowers considering long-term commitments, particularly in variable-rate financing structures linked to interbank benchmarks. Housing transaction volumes typically soften during tightening cycles, reducing loan origination growth and affecting lender revenue stability. Developers may also experience slower property absorption rates when financing costs rise, indirectly impacting mortgage demand pipelines. Refinancing activity becomes cyclical and sensitive to rate direction, adding variability to loan portfolio dynamics. Sustained rate volatility therefore introduces macro-financial risk factors that complicate planning and growth predictability across the KSA home finance sector.

Opportunities

Affordable Housing Finance Expansion for Middle-Income Households

Affordable Housing Finance Expansion for Middle-Income Households represents a major opportunity in the KSA home finance market as demographic growth and policy priorities create strong demand for financing solutions tailored to salaried families seeking primary homeownership within regulated affordability thresholds. Government housing strategies emphasize increasing ownership penetration among middle-income nationals, creating sustained demand for appropriately priced residential units and accessible mortgage structures. Lenders can design targeted financing products with optimized tenors, subsidy integration, and reduced down-payment requirements aligned with this demographic segment’s income profile. Developers partnering with financiers to deliver standardized affordable housing communities can unlock large-scale mortgage origination pipelines in expanding urban corridors. Digital underwriting tools enable precise assessment of borrower repayment capacity, allowing lenders to safely extend credit to previously underserved households. Expansion of secondary mortgage markets and securitization can provide liquidity to support high-volume affordable housing finance portfolios. Regional housing development initiatives outside core cities further broaden geographic financing opportunities while reducing land cost pressures. Employer-linked housing programs can also facilitate stable borrower acquisition among salaried workers. The convergence of demographic demand, policy support, and scalable financing models positions affordable housing finance as a central growth opportunity in the KSA home finance market.

Digital End-to-End Mortgage Ecosystem Integration

Digital End-to-End Mortgage Ecosystem Integration offers substantial opportunity for the KSA home finance market by connecting lenders, developers, government platforms, and property registries into unified digital transaction environments that streamline the entire housing purchase and financing journey. Integrated platforms allow buyers to search properties, verify eligibility, secure financing approvals, and complete documentation within a single digital interface, significantly improving transaction efficiency and user experience. Lenders benefit from direct access to verified property listings and developer inventory, enabling faster loan-to-property matching and disbursement processes. Government subsidy approvals can be embedded into digital workflows, reducing administrative delays and enhancing transparency for borrowers. Blockchain-enabled title verification and electronic registration systems can strengthen transaction security and reduce fraud risk in mortgage origination. Data integration across institutions supports advanced analytics for credit risk modeling and demand forecasting, improving portfolio performance and strategic planning. Digital ecosystems also enable cross-selling of insurance, refinancing, and home improvement loans, expanding revenue streams for financiers. Partnerships among banks, fintech firms, and developers accelerate innovation and market reach. The development of fully integrated digital mortgage ecosystems therefore represents a transformative opportunity for efficiency, scale, and customer engagement in the KSA home finance sector.

Future Outlook

The KSA home finance market is expected to expand steadily over the coming five years, supported by sustained housing policy programs, demographic growth, and continued urban residential development. Digital mortgage platforms and integrated property-finance ecosystems will improve access and processing efficiency across lenders. Subsidized financing and affordable housing supply expansion are likely to strengthen middle-income borrower participation. Regulatory alignment and banking sector liquidity will remain key enablers of long-term mortgage portfolio growth and market stability.

Major Players

- Al Rajhi Bank

- Saudi National Bank

- Riyad Bank

- Banque Saudi Fransi

- Arab National Bank

- Alinma Bank

- Bank Aljazira

- Saudi Investment Bank

- Saudi Awwal Bank

- Gulf International Bank

- Saudi Home Loans

- Dar Al Tamleek

- Bidaya Home Finance

- Abdul Latif Jameel Finance

- Deutsche Gulf Finance

Key Target Audience

- Commercial banks

- Mortgage finance companies

- Real estate developers

- Housing ministries and regulatory authorities

- Sovereign wealth funds

- Investment and venture capitalist firms

- Institutional investors

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including mortgage volumes, housing supply, borrower demographics, subsidy programs, and financing structures were identified through regulatory datasets and financial disclosures. These variables define demand drivers, lending capacity, and structural constraints shaping market dynamics.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using banking sector lending data, housing transaction statistics, and mortgage portfolio disclosures. Cross-validation across lenders and housing agencies ensured consistency in market representation and segmentation allocation.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from banking, housing policy, and real estate sectors validated assumptions on demand drivers, affordability trends, and financing adoption patterns. Feedback refined segmentation dominance and structural growth interpretations.

Step 4: Research Synthesis and Final Output

All validated datasets and insights were synthesized into structured market analysis, ensuring alignment with regulatory frameworks and housing policy context. Final outputs present consistent segmentation, competitive mapping, and growth outlook for the KSA home finance market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Vision 2030 homeownership expansion targets

Government subsidized mortgage programs scale up

Urban population growth in Riyadh and major cities

Digital banking adoption for retail lending

Expansion of mortgage refinancing liquidity - Market Challenges

Housing affordability pressure from price inflation

Rising mortgage rates reducing buyer capacity

Supply mismatch in affordable housing segments

Regulatory repayment caps on borrower leverage

Volatility in residential transaction volumes - Market Opportunities

Expansion of Islamic digital mortgage products

Mortgage securitization and refinancing market growth

Affordable housing finance for mid income households - Trends

Shift toward digital mortgage origination platforms

Growth of government backed subsidized mortgages

Increase in refinancing and balance transfer loans

Integration of developer and lender financing

Data driven credit scoring adoption - Government Regulations & Defense Policy

Saudi Central Bank mortgage lending rules

Housing subsidy and Sakani program expansion

Loan to income and repayment cap policies - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Conventional Fixed Rate Home Loans

Variable Rate Home Loans

Islamic Murabaha Home Finance

Ijara Lease to Own Finance

Subsidized Government Supported Mortgages - By Platform Type (In Value%)

Retail Bank Branch Channels

Digital Mortgage Platforms

Mortgage Finance Companies

Government Housing Platforms

Developer Linked Financing Platforms - By Fitment Type (In Value%)

Ready Property Purchase Financing

Off Plan Property Financing

Self Construction Financing

Home Improvement Financing

Balance Transfer Refinancing - By End User Segment (In Value%)

First Time Saudi Homebuyers

Middle Income Salaried Households

High Net Worth Individuals

Expatriate Residents

Real Estate Investors

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Loan Type, Interest Structure, Financing Tenor, Loan to Value Ratio, Subsidy Eligibility, Digital Origination Capability, Processing Time, Target Income Segment, Property Type Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Al Rajhi Bank

Saudi National Bank

Riyad Bank

Banque Saudi Fransi

Arab National Bank

Alinma Bank

Bank Aljazira

Saudi Investment Bank

Saudi Awwal Bank

Gulf International Bank

Saudi Home Loans

Dar Al Tamleek

Bidaya Home Finance

Abdul Latif Jameel Finance

Deutsche Gulf Finance

- Saudi nationals dominate demand due to ownership programs

- First time buyers drive subsidized mortgage uptake

- Urban salaried households form core borrower base

- Expat financing demand remains niche segment

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now