Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA Home Fitness Equipment Market is valued at SAR ~ billion, driven by rising consumer interest in health and wellness combined with the increasing adoption of fitness technologies. A shift toward home-based fitness solutions, amplified by growing health consciousness, has significantly contributed to market expansion. The market is also supported by improvements in disposable income and changing consumer lifestyles that prioritize convenience, which has propelled the demand for home fitness equipment. As more consumers choose to work out at home due to busy schedules, this trend is expected to continue, ensuring sustained growth in the market.

The dominant cities in the KSA Home Fitness Equipment Market are Riyadh, Jeddah, and Dammam. Riyadh, as the capital city, leads the market due to its larger population base, increasing affluence, and greater access to retail and e-commerce channels. Jeddah, with its thriving coastal economy and fitness-conscious population, also contributes significantly to market demand. Dammam, with its industrial and economic influence in the Eastern Province, is another key region driving growth. These cities have witnessed a surge in demand for home fitness equipment due to an increase in disposable income, urbanization, and a rising focus on personal health.

Market Segmentation

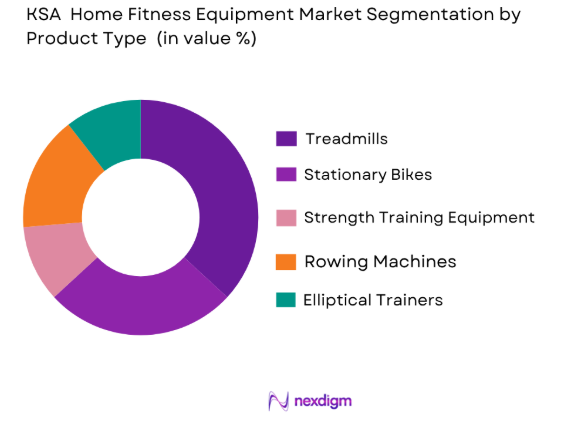

By Product Type

The KSA Home Fitness Equipment Market is segmented by product type into treadmills, stationary bikes, strength training equipment, rowing machines, and elliptical trainers. Among these, treadmills dominate the market share due to their popularity among fitness enthusiasts. The increasing demand for cardio-based fitness solutions has made treadmills a preferred choice for home gyms. With technological advancements such as integrated touch screens, Wi-Fi connectivity, and built-in workout programs, brands like Life Fitness and Technogym have created sophisticated models that attract consumers. The convenience of using a treadmill for cardiovascular training without leaving home has further cemented its place as the leading product in the market.

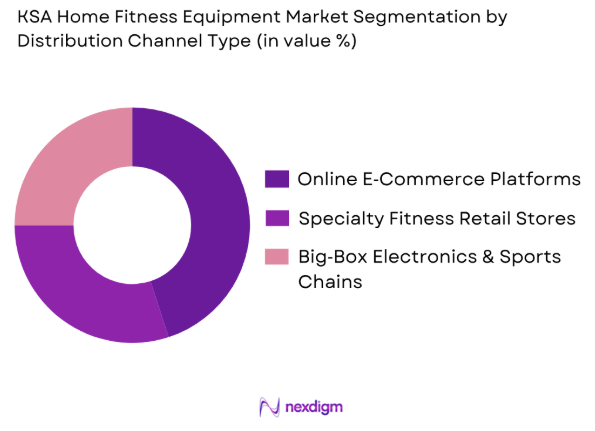

By Distribution Channel

The distribution of home fitness equipment in KSA is primarily driven by e-commerce platforms, specialty retail stores, and large sports chains. E-commerce channels have seen significant growth in recent years due to the rising trend of online shopping and convenience. Platforms like Noon and Souq.com have made purchasing home fitness equipment easier for consumers. Specialty stores and big-box retailers like Carrefour and Sports Corner also contribute substantially to the market due to their widespread presence and ability to offer personalized customer service. However, the increasing penetration of e-commerce will continue to drive the dominance of online channels in the distribution of fitness products.

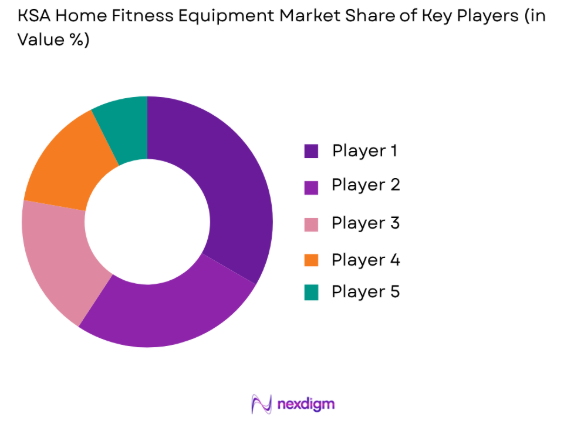

Competitive Landscape

The KSA Home Fitness Equipment Market is dominated by a few key players who are influencing both the product offerings and consumer preferences. Global brands like Life Fitness, Technogym, and NordicTrack, along with local players such as DOMYOS, have established strong positions due to their wide range of products, innovative features, and solid distribution networks. These companies continuously innovate and cater to the growing demand for technologically advanced fitness equipment, with a focus on connected solutions and user-friendly features.

| Company | Establishment Year | Headquarters | Product Range | Market Reach | R&D Investment | Distribution Network |

| Life Fitness | 1968 | USA | ~ | ~ | ~ | ~ |

| Technogym | 1983 | Italy | ~ | ~ | ~ | ~ |

| NordicTrack | 1975 | USA | ~ | ~ | ~ | ~ |

| DOMYOS (Decathlon) | 1999 | France | ~ | ~ | ~ | ~ |

| ProForm | 1977 | USA | ~ | ~ | ~ | ~ |

KSA Home Fitness Equipment Market Analysis

Growth Drivers

Rising Health Awareness and Lifestyle Shift

The growing awareness around health and fitness has significantly influenced consumer behavior in KSA. According to the Saudi Ministry of Health, nearly 70% of the Saudi population is actively seeking healthier lifestyles, reflected in their increased participation in physical activities. The population’s rising health concerns, including obesity, have led to higher demand for fitness-related products. As a result, fitness equipment consumption has surged, driven by changing diets, workout routines, and fitness preferences. Furthermore, a 2023 report by the World Bank indicated that lifestyle-related diseases, such as heart disease and diabetes, have increased by 30% in the region, propelling demand for preventative health measures such as home fitness equipment.

Government Initiatives for Population Health and Obesity Reduction

The Saudi government has significantly invested in improving public health, particularly in combating obesity, which has been a growing concern. In 2022, the Ministry of Health launched a national initiative aimed at reducing the obesity rate, with a target to decrease it by 10% over the next five years. This initiative includes programs promoting physical activity, dietary guidelines, and access to fitness facilities. According to the World Bank, government expenditure on health in KSA increased by 4.5% annually, reaching SAR 162 billion in 2023, which directly impacts the growth of the home fitness equipment market. These initiatives are expected to drive the demand for health and fitness solutions across the country.

Challenges

Import Dependency and Tariff Impacts

Saudi Arabia’s home fitness equipment market is heavily reliant on imports, with approximately 75% of fitness equipment sourced from abroad. This dependency has exposed the market to the challenges of tariff and customs regulation changes. In 2023, the Saudi government introduced a 5% VAT on imported consumer goods, which has increased the cost of fitness equipment. Additionally, the fluctuation in exchange rates, with the SAR depreciating by 2.5% against major currencies in 2023, has added further price volatility. As the market continues to rely on international suppliers, these import-related challenges may limit the market’s accessibility to affordable fitness products.

After-Sales Service / Warranty Infrastructure Gaps

One of the key challenges faced by the KSA home fitness equipment market is the lack of comprehensive after-sales service and warranty infrastructure. While many international brands offer warranties and services, local providers often struggle to match these standards. In 2022, the Saudi Consumer Protection Agency reported that consumer complaints about warranty services for fitness equipment grew by 18%. This issue is exacerbated by the low density of certified repair technicians and service centers, which complicates maintenance and repair procedures. Additionally, consumer reluctance to purchase higher-end products, due to insufficient warranty support, has hindered market growth.

Opportunities

Integration of AR/VR Fitness Experiences

The demand for digital fitness solutions has led to the adoption of AR (Augmented Reality) and VR (Virtual Reality) technologies in the home fitness equipment market. In KSA, digital fitness has gained significant traction, with 1.3 million people using digital fitness apps by 2023. These technologies allow consumers to experience immersive workout environments from their homes, bridging the gap between physical and virtual fitness experiences. Companies like Peloton and Technogym have already integrated VR and AR features into their fitness equipment, and the Saudi market has shown a growing interest in these features, as reflected by the 14% rise in app downloads for fitness-related platforms in 2023. This trend is expected to continue as consumer interest in interactive, engaging fitness experiences increases.

Subscription-Based Equipment Models

With the rise of fitness-as-a-service, subscription-based equipment models are becoming increasingly popular in Saudi Arabia. Consumers are now opting for affordable monthly plans to access high-end fitness machines and virtual workout sessions. By 2023, subscription services in fitness equipment accounted for over 30% of the market share, as per a report by the Saudi Ministry of Commerce. These models allow consumers to avoid large upfront payments and provide flexibility in upgrading or exchanging equipment. As disposable incomes rise, particularly in urban areas, these subscription models are expected to drive the demand for home fitness equipment, particularly among younger generations.

Future Outlook

Over the next 5 years, the KSA Home Fitness Equipment Market is expected to experience significant growth driven by continuous innovation, a shift toward personalized fitness, and the growing trend of connected fitness equipment. Consumers are increasingly inclined toward products that offer more than just basic functions, such as smart features like app integration and real-time tracking. The rising demand for home-based workouts, coupled with government support for wellness initiatives, is expected to boost market growth, as more individuals prioritize health and wellness in their daily routines. Additionally, the post-pandemic focus on home fitness solutions and convenience is likely to sustain demand during this forecasted period.

Major Players in the Market

- Life Fitness

- Technogym

- NordicTrack

- DOMYOS (Decathlon)

- ProForm

- Horizon Fitness

- Sole Fitness

- Peloton

- Schwinn Fitness

- Bowflex

- XTERRA Fitness

- Spirit Fitness

- Kettler

- BH Fitness

- Cybex International

Key Target Audience

- Home Fitness Enthusiasts

- Retailers and E-commerce Platforms

- Fitness Equipment Distributors

- Fitness Equipment Manufacturers

- Investors and Venture Capitalist Firms

- Government and Regulatory Bodies (e.g., Saudi Arabian Ministry of Health)

- Corporate Wellness Program Providers

- Gym and Fitness Studios

Research Methodology

Step 1: Identification of Key Variables

In this initial phase, a comprehensive ecosystem map will be created to identify key stakeholders, including manufacturers, retailers, and consumers within the KSA Home Fitness Equipment Market. Extensive desk research will be conducted using secondary data from industry reports, government publications, and proprietary databases to determine the critical market variables and trends.

Step 2: Market Analysis and Construction

In this phase, historical data will be compiled and analyzed to evaluate the market penetration of various product types. Data on sales volume, revenue, and pricing will be analyzed to determine market trends and identify key growth areas within the home fitness equipment sector. The construction phase will also assess supply chain dynamics, including manufacturing and distribution networks.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses related to market growth drivers and key trends will be validated through consultations with industry experts, including fitness equipment manufacturers, distributors, and retail executives. These consultations will offer valuable insights into consumer behavior and the impact of technological innovations on market growth.

Step 4: Research Synthesis and Final Output

The final research synthesis phase will involve engaging with multiple stakeholders in the fitness industry to validate the collected data and refine the analysis. Primary and secondary data will be integrated to ensure a robust, comprehensive, and validated final report on the KSA Home Fitness Equipment Market.

- Executive Summary

- Research Methodology (Market Definitions and Standardizations, Assumptions and Normalizations, Data Sources and Triangulation Logic, Bottom‑Up Market Sizing and Validation Approach, Top‑Down Opportunity Estimation Protocol, Primary Research Intercept Framework, Limitations and Future Method Refinements)

- Definition and Scope

- Market Genesis and Evolution

- Fitness Culture and Adoption Lifecycle in KSA

- Industry Value Chain and Distribution Architecture

- Growth Drivers

Rising Health Awareness and Lifestyle Shift

Government Initiatives for Population Health and Obesity Reduction

Increase in Disposable Income & Smart Home Adoption

Digital Fitness and Connected Fitness Ecosystem Demand - Challenges

Import Dependency and Tariff Impacts

After‑Sales Service / Warranty Infrastructure Gaps

Consumer Financing and Credit Constraints

Fragmented Demand Patterns Across Regions

- Opportunities

Integration of AR/VR Fitness Experiences

Subscription‑Based Equipment Models

Corporate Workforce Wellness Programs

Logistics & Servicing Franchising Potential - Trends

Connected Equipment Dominance (IoT, AI‑Driven Coaching)

Flexible Payment and Rental Models

Social & Gamified Fitness Engagement

Sustainability and Energy‑Efficient Machines - Regulatory & Compliance Landscape

Product Safety Standards and Certifications

Import Policy & Tariff Regime

Consumer Protection Regulations

Standards for App / Digital Integration - SWOT Analysis

- Ecosystem Mapping

- Porter’s Five Forces Analysis

- By Current Market Size – Value (SAR) & Volume, 2020-2025

- By Market Density, 2020-2025

- By Price Band Analysis, 2020-2025

- By Product (In value %)

Treadmills

Stationary Bikes

Strength Training Systems

Rowing Machines

Elliptical Trainers - By End‑User (In value %)

Individual Fitness Enthusiasts

Family / Multi‑User Households

Professional Coaches & Personal Trainers

Luxury/High‑Affluence Residential Users

Corporate Wellness Programs - By Distribution Channel (In value %)

Online E‑Commerce Platforms

Specialty Fitness Retail Stores

Big‑Box Electronics & Sports Chains - By Price Tier (In Value %)

Economy / Entry‑Level

Mid‑Tier

Premium / Smart Devices

Subscription‑Linked Digital Fitness Systems - By Feature Set (In Value %)

Connected / App‑Integrated Equipment

Non‑Connected Traditional Units

Wearable Ecosystem Bundles - By Geography (In Value %)

Riyadh & Central KSA

Eastern Province

Western Province (Jeddah / Makkah corridor)

Southern KSA

Northern KSA

- Market Share by Value & Volume

- Brand Positioning / Value Proposition Mapping

- Cross‑Comparison Parameters (Company Overview, Product Portfolio Breadth, Retail & Online Channel Reach, After‑Sales Service & Warranty Coverage, Distribution Network Strength, Annual Revenue & Fiscal Growth, R&D and Connected Fitness Investment, Brand Loyalty & Customer Satisfaction Index)

- Competitor Analysis and Profiles

DOMYOS

Horizon Fitness

NordicTrack

ProForm

Life Fitness

Technogym

Matrix Fitness

BH Fitness

Sole Fitness

Peloton

Echelon

XTERRA Fitness

Reebok Home Fitness

Spirit Fitness

Kettler

- Consumer Purchase Patterns

- Usage Frequency and Dwell Metrics

- Loyalty, Repurchase & Brand Elasticity Scores

- Online vs Offline Purchase Preferences

- Price Sensitivity and Value Awareness

- By Current Market Size – Value (SAR) & Volume, 2026-2035

- By Market Density, 2026-2035

- By Price Band Analysis, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now