Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA insecticide market is estimated at approximately USD ~ million, forming a significant component of the broader Saudi crop protection chemicals market valued at USD ~ million. The market is driven by rising investments in food security, protected agriculture, greenhouse cultivation, and horticultural crop production. Saudi Arabia’s agricultural sector continues to prioritize fruits, vegetables, and date palms, which require intensive pest management.

Government-backed agricultural modernization programs, increasing adoption of precision farming, and growing demand for higher crop yields have accelerated insecticide consumption across commercial farms and greenhouse facilities. The broader crop protection market expanded from approximately USD ~ million to USD ~ million, reflecting sustained demand for pest-control solutions across the Kingdom.

Market Segmentation

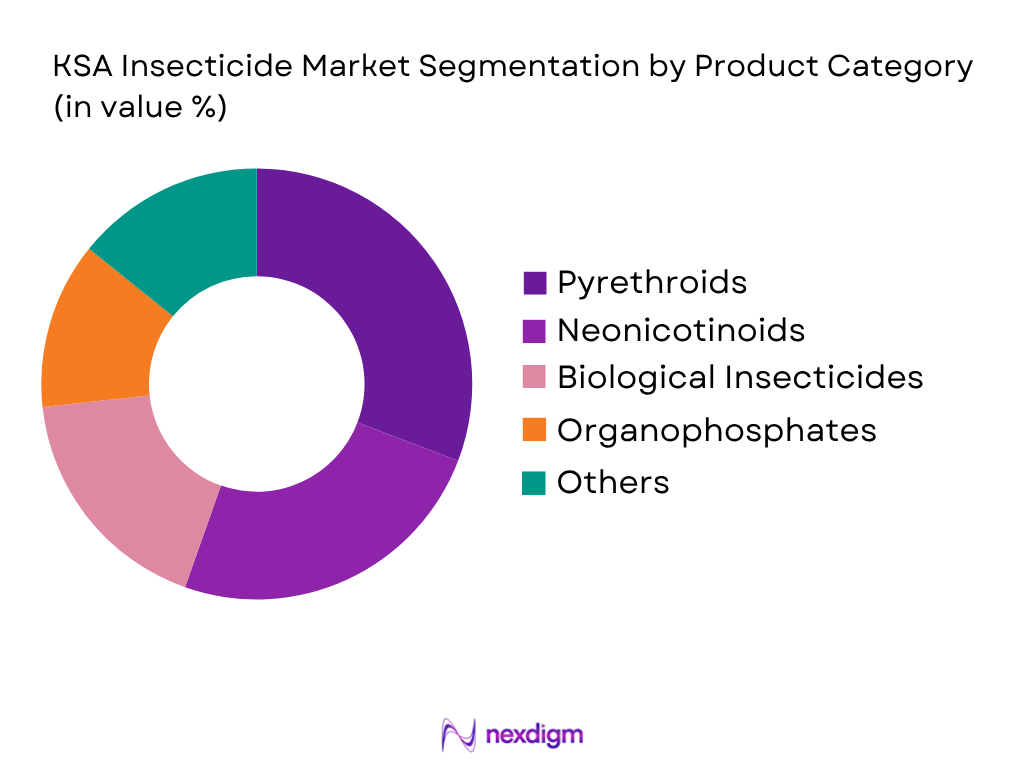

By Product Category

KSA Insecticide Market is segmented by product class into pyrethroids, neonicotinoids, biological insecticides, organophosphates, and others. Recently, pyrethroids have held the dominant market share in Saudi Arabia under product class due to their broad-spectrum efficacy against chewing and sucking insects affecting vegetables, fruits, and date palms. Pyrethroids provide rapid knockdown effects, relatively lower application rates, and compatibility with integrated pest management programs. Farmers widely utilize these products in greenhouse farming systems, where pest outbreaks can rapidly affect crop productivity. Their effectiveness against whiteflies, aphids, thrips, and caterpillars has strengthened adoption across protected cultivation facilities. Furthermore, the growing emphasis on maximizing crop yields under water-constrained conditions has encouraged growers to use highly efficient insecticide solutions, reinforcing pyrethroids’ leadership position within the market.

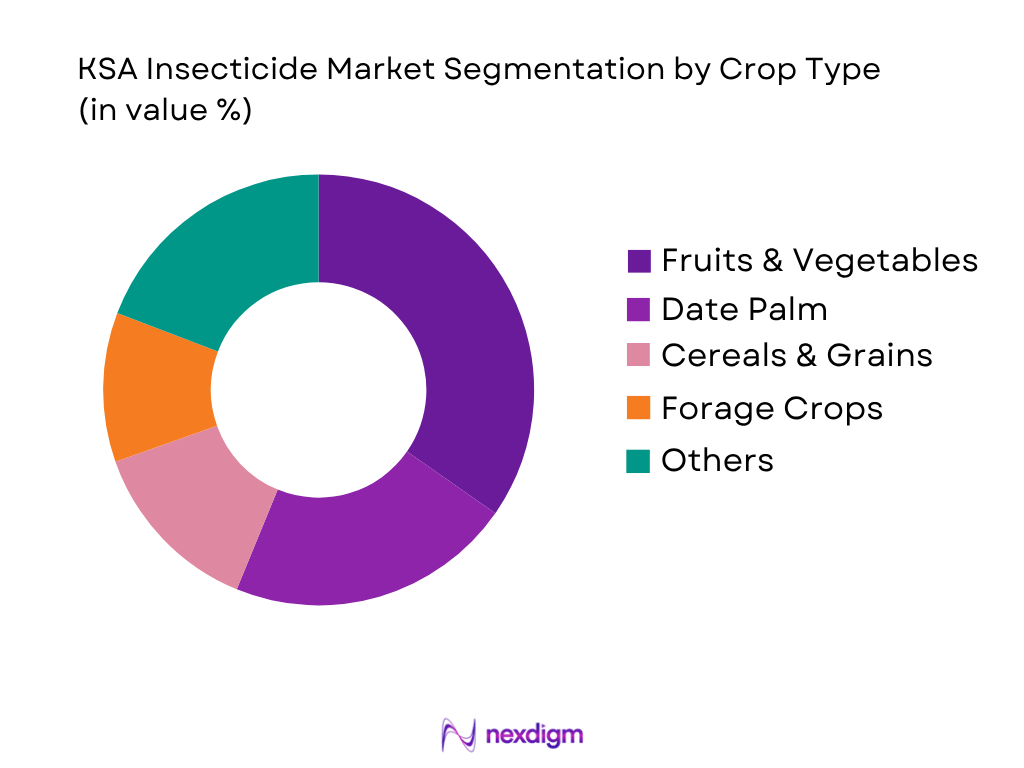

By Crop Type

KSA Insecticide Market is segmented by crop type into fruits and vegetables, date palm, cereals and grains, forage crops, and others. Recently, fruits and vegetables have held the dominant market share in Saudi Arabia under crop type because these crops require intensive insect management throughout the cultivation cycle. Greenhouse-grown tomatoes, cucumbers, peppers, and leafy vegetables are particularly vulnerable to whiteflies, thrips, leaf miners, aphids, and caterpillar infestations. Saudi Arabia has significantly expanded protected agriculture to improve food security and reduce import dependency, creating continuous demand for insecticide applications. High-value horticultural crops also face strict quality and cosmetic standards, requiring proactive pest management. The economic importance of vegetable and fruit production, coupled with increasing adoption of modern greenhouse farming systems, continues to support the segment’s dominance in the insecticide market.

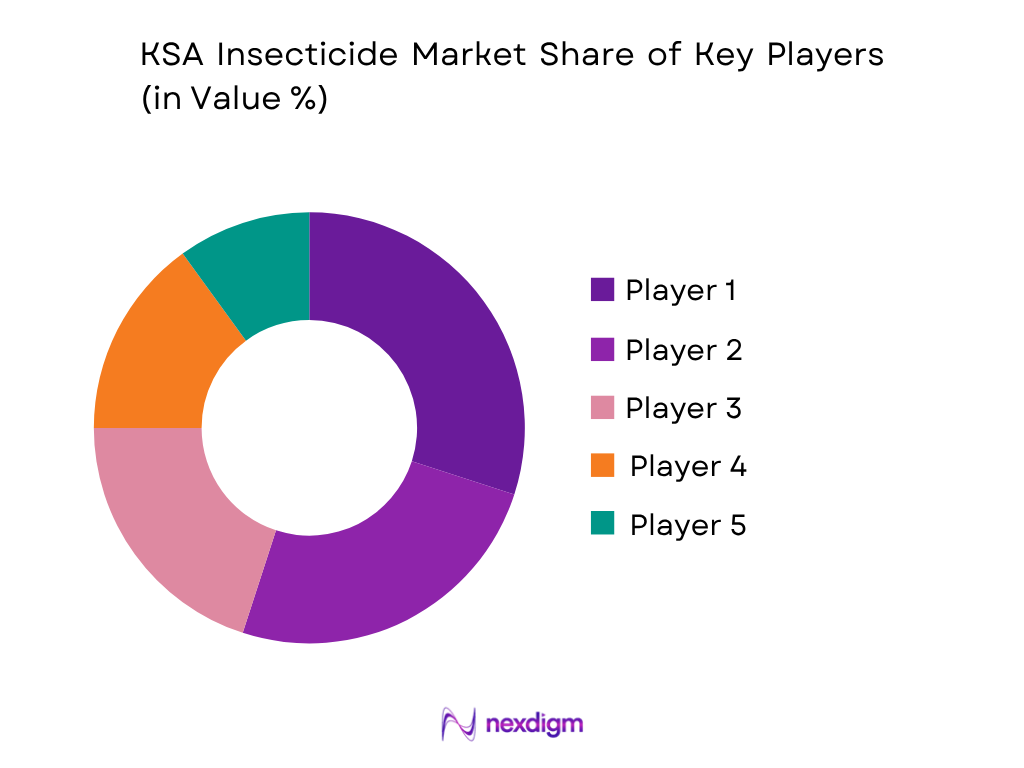

Competitive Landscape

The KSA insecticide market is moderately consolidated, with multinational agrochemical companies dominating through strong product portfolios, regulatory approvals, distribution partnerships, and agronomic support services. Global leaders such as Bayer, Syngenta, BASF, Corteva, and FMC maintain strong positions through extensive insecticide registrations, greenhouse crop solutions, and biological crop protection offerings. Competition is driven by innovation in active ingredients, biological alternatives, precision application technologies, and technical support provided to commercial growers.

| Company | Establishment Year | Headquarters | Product Portfolio Strength | Biological Portfolio | Greenhouse Focus | Distribution Network | Crop Coverage | Technical Support Infrastructure |

| Bayer Crop Science | 1863 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Syngenta | 2000 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| BASF Agricultural Solutions | 1865 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| FMC Corporation | 1883 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Corteva Agriscience | 2019 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

KSA Insecticide Market Analysis

Growth Drivers

Expansion of Food Security Programs and Agricultural Production

Saudi Arabia’s insecticide market is significantly supported by the Kingdom’s food security strategy and agricultural modernization efforts. According to the Saudi General Authority for Statistics (GASTAT), the agricultural sector contributed approximately SAR 114 billion to GDP in 2024, reflecting the growing importance of domestic food production. The Ministry of Environment, Water and Agriculture (MEWA) reported production of more than 1.9 million tonnes of vegetables, over 700 thousand tonnes of fruits, and approximately 1.9 million tonnes of dates annually. Date palms alone exceed 37 million trees, creating continuous demand for insecticides against red palm weevil, dubas bug, and scale insects. Saudi Arabia’s population surpassed 33 million people, increasing pressure on local food supply chains and encouraging greater agricultural output. Additionally, the World Bank reported GDP exceeding USD 1.1 trillion, supporting investment in greenhouse farming, precision agriculture, and crop protection technologies. As protected cultivation and high-value horticulture expand across Riyadh, Al-Qassim, Tabuk, and Eastern Province, growers increasingly rely on insecticides to safeguard yields, reduce pest-related losses, and meet food security objectives. This ongoing agricultural intensification continues to drive demand for insecticide products throughout the Kingdom.

Growth of Greenhouse and Protected Agriculture

Protected agriculture has become one of the strongest drivers of insecticide consumption in Saudi Arabia. According to MEWA, the Kingdom operates more than 8,500 greenhouse units, producing tomatoes, cucumbers, peppers, strawberries, and other high-value crops. Greenhouse environments create favorable conditions for pests such as whiteflies, thrips, aphids, and leaf miners, increasing the frequency of insecticide applications compared with open-field farming. Saudi Arabia’s cultivated agricultural area exceeds 1 million hectares, while greenhouse cultivation continues to expand under Vision 2030 agricultural diversification initiatives. The World Bank reports gross capital formation exceeding USD 300 billion, supporting investments in irrigation systems, climate-controlled agriculture, and precision crop management. Greenhouse production is particularly concentrated in Riyadh, Tabuk, Al-Qassim, and Eastern Province, where commercial farms emphasize year-round crop production. Since protected cultivation systems involve high-value crops and intensive production cycles, growers prioritize advanced insect management solutions to protect profitability and maintain crop quality. Consequently, the expansion of greenhouse farming directly contributes to increasing insecticide consumption across the Kingdom’s agricultural sector.

Market Challenges

Dependence on Imported Active Ingredients

A major challenge facing the KSA insecticide market is its dependence on imported active ingredients and finished crop protection products. According to the World Bank, Saudi Arabia’s merchandise imports exceeded USD 220 billion, reflecting significant reliance on foreign supply chains across multiple industries, including agricultural chemicals. While the Kingdom has developed local fertilizer and petrochemical capabilities, domestic production of insecticide active ingredients remains limited. Most insecticides used in horticulture, greenhouse farming, and date palm cultivation originate from multinational suppliers based in Europe, China, India, and North America. This dependence exposes distributors and farmers to disruptions caused by shipping delays, geopolitical tensions, trade restrictions, and raw material shortages. The Saudi economy supports large-scale agricultural investment through GDP exceeding USD 1.1 trillion, but imported insecticide availability remains vulnerable to external market conditions. In addition, fluctuations in international logistics networks can delay product deliveries during critical planting and pest-management periods. Such dependency creates supply uncertainty for growers and limits the Kingdom’s ability to achieve full self-sufficiency in crop protection inputs.

Water Scarcity and Climate-Related Pest Pressure

Saudi Arabia remains one of the world’s most water-scarce agricultural economies, creating operational challenges for insecticide application and pest management. According to the World Bank, renewable freshwater resources remain below 100 cubic meters per person annually, among the lowest globally. Agriculture continues to rely heavily on groundwater extraction and advanced irrigation technologies to sustain crop production. Rising temperatures and climate variability have increased pest pressure on date palms, vegetables, and fruit crops, leading to more frequent infestations and complex pest-management requirements. MEWA reports more than 37 million date palms across the Kingdom, all vulnerable to red palm weevil attacks. Simultaneously, expanding greenhouse agriculture creates favorable environments for pest reproduction, increasing reliance on insecticide applications. The IMF reports Saudi Arabia’s economy exceeding USD 1.1 trillion, enabling investment in climate-resilient agriculture; however, environmental stress remains a significant challenge. Farmers must balance water conservation objectives with effective pest-control practices, while adapting to evolving pest populations and resistance concerns. These environmental factors complicate insecticide use and increase operational challenges for growers.

Market Opportunities

Expansion of Biological Insecticides and Sustainable Agriculture

Saudi Arabia’s transition toward sustainable agriculture creates a major opportunity for biological insecticides and integrated pest management solutions. The Kingdom’s agricultural modernization programs increasingly emphasize food safety, environmental stewardship, and reduced chemical residues. MEWA oversees agricultural production exceeding 1.9 million tonnes of vegetables and approximately 1.9 million tonnes of dates, creating substantial opportunities for biological pest-control products. Export-oriented horticultural producers face stricter international residue requirements, encouraging adoption of bio-based insecticides. Furthermore, Saudi Arabia’s population exceeding 33 million people increases demand for safe and sustainable food production systems. The World Bank reports agricultural investment supported by GDP surpassing USD 1.1 trillion, providing financial capacity for advanced crop protection technologies. Biological insecticides help growers manage resistance issues while supporting integrated pest management programs. Date palm plantations, greenhouse vegetables, and high-value fruit farms are increasingly evaluating biological alternatives to conventional chemical products. As environmental regulations and sustainability objectives gain importance, biological insecticides are positioned to become one of the fastest-growing opportunities within Saudi Arabia’s crop protection ecosystem.

Precision Agriculture and Smart Pest Monitoring

The adoption of precision agriculture technologies presents a substantial opportunity for the KSA insecticide market. Saudi Arabia has accelerated investments in smart farming systems, digital agriculture, and automated greenhouse operations under Vision 2030. According to the World Bank, information and communications technology infrastructure continues expanding across the Kingdom, supported by GDP exceeding USD 1.1 trillion. Modern farms increasingly utilize drones, satellite imagery, remote sensing systems, and digital monitoring platforms to identify pest outbreaks and optimize insecticide applications. Saudi Arabia’s cultivated agricultural area exceeds 1 million hectares, creating a large addressable market for precision pest-management solutions. Greenhouse operators are particularly adopting sensor-based monitoring systems to track pest populations and improve intervention timing. These technologies reduce unnecessary insecticide applications while improving efficacy and minimizing crop losses. Additionally, smart agriculture aligns with national objectives to improve resource efficiency and agricultural productivity. As digital transformation expands across commercial farming operations, insecticide manufacturers capable of integrating products with precision agriculture platforms will benefit from significant long-term growth opportunities.

Future Outlook

The KSA insecticide market is expected to demonstrate steady growth through the forecast period, supported by Vision 2030 agricultural diversification initiatives, greenhouse expansion, food security investments, and increasing adoption of precision agriculture technologies. The transition toward high-value horticultural production and controlled-environment agriculture will continue to strengthen demand for advanced insect control products. Biological insecticides are expected to gain traction as growers seek sustainable crop protection solutions and compliance with international residue standards. Date palm plantations, greenhouse vegetables, and commercial fruit farms will remain major consumption centers. Additionally, drone-assisted spraying, digital pest monitoring systems, and integrated pest management programs are expected to reshape insecticide application practices across Saudi Arabia.

Major Players

- Bayer Crop Science

- Syngenta Group

- BASF Agricultural Solutions

- Corteva Agriscience

- FMC Corporation

- ADAMA Agricultural Solutions

- UPL Limited

- Sumitomo Chemical

- Nufarm Limited

- Koppert Biological Systems

- Biobest Group

- Reda Chemicals

- SABIC Agri-Nutrients

- Al-Jazeera Agricultural Company

- Saudi Delta Group

Key Target Audience

- Commercial Farm Operators

- Greenhouse Growers

- Date Palm Plantation Companies

- Agricultural Input Distributors

- Agrochemical Manufacturers

- Precision Agriculture Technology Providers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the KSA Insecticide Market. Extensive desk research is conducted using government publications, agricultural databases, trade statistics, company reports, and industry sources. The primary objective is to identify critical variables influencing insecticide demand, including crop acreage, pest incidence, greenhouse expansion, and product registration activity.

Step 2: Market Analysis and Construction

Historical data relating to crop protection consumption, agricultural production, import volumes, and insecticide utilization are compiled and analyzed. Market sizing is developed using both top-down and bottom-up approaches. Segment-level analysis evaluates product class adoption, crop-specific demand, application methods, and regional consumption patterns.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through computer-assisted telephone interviews (CATIS) and consultations with growers, distributors, agronomists, agrochemical companies, greenhouse operators, and government stakeholders. These discussions provide insights into purchasing behavior, pest-management practices, product performance, and future adoption trends.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing primary and secondary research findings to develop a comprehensive market assessment. Direct engagement with market participants validates market sizing, segmentation, competitive positioning, and growth opportunities. The resulting analysis provides actionable insights regarding market dynamics, future outlook, and strategic opportunities.

- Executive Summary

- Research Methodology (Market definitions and assumptions, abbreviations, insecticide market taxonomy, active ingredient classification, agricultural and non-agricultural scope, market sizing approach, top-down and bottom-up triangulation, distributor interviews, farmer surveys, government database validation, import-export analysis, pricing assessment, limitations and future conclusions)

- Definition and Scope

- Overview Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers (Expansion of protected agriculture, date palm cultivation growth, food security initiatives, precision agriculture adoption, greenhouse investments, pest outbreaks, agricultural modernization, Vision 2030 support)

- Market Challenges (Import dependence, active ingredient restrictions, pest resistance, water scarcity, regulatory compliance, counterfeit products)

- Opportunities (Biological crop protection, integrated pest management, precision spraying, drone-based application, smart farming technologies)

- Market Trends (Sustainable crop protection, residue management, biological integration, precision application, digital farming)

- Government Regulation (Pesticide registration, residue standards, environmental compliance, import controls, food safety requirements)

- SWOT Analysis

- Stakeholder Ecosystem

- Porter’s Five Forces

- Competition Ecosystem

- By Market Revenue (2020-2025)

- By Sales Volume (2020-2025)

- By Average Realized Price (2020-2025)

- By Product Category (In Value %)

Pyrethroids

Neonicotinoids

Organophosphates

Biological Insecticides

Others - By Crop Type (In Value %)

Fruits and Vegetables

Date Palm

Cereals and Grains

Forage Crops

Others - By Formulation Type (In Value %)

Liquid Formulations

Wettable Powder (WP)

Suspension Concentrate (SC)

Water Dispersible Granules (WDG)

Others - By Application Method (In Value %)

Foliar Spray

Seed Treatment

Soil Treatment

Chemigation and Drip Irrigation Application

Fumigation - By End User (In Value %)

Commercial Farms

Greenhouse Growers

Date Plantation Operators

Government and Municipality Pest Control Programs

Residential and Institutional Pest Management - By Region (In Value %)

Riyadh Region

Makkah Region

Eastern Province

Madinah Region

Al-Qassim Region

Asir Region

Tabuk Region

Northern and Southern Provinces

- Market Share of Major Players (Market share by value, volume, active ingredient portfolio, crop coverage, distributor reach, regional penetration)

- Cross Comparison Parameters (Product portfolio strength, active ingredient diversity, biological insecticide portfolio, distribution and dealer network, greenhouse farming penetration, date palm crop protection expertise, product registration portfolio, technical support and agronomy services)

- SWOT Analysis of Major Players

- Pricing Analysis Basis SKUs (Lambda-cyhalothrin, Imidacloprid, Chlorpyrifos alternatives, Spinosad, Emamectin Benzoate, Thiamethoxam, Deltamethrin, Abamectin, Bifenthrin, Biological formulations)

- Detailed Profiles of Major Companies

Bayer Crop Science

Syngenta Group

BASF Agricultural Solutions

Corteva Agriscience

FMC Corporation

ADAMA Agricultural Solutions

UPL Limited

Sumitomo Chemical

Nufarm Limited

Biobest Group

Koppert Biological Systems

SABIC Agri-Nutrients

Saudi Delta Group

Al-Jazeera Agricultural Company

Reda Chemicals

- Commercial Farm Demand and Utilization Analysis

- Greenhouse Operator Purchasing Behavior

- Date Palm Plantation Pest Management Analysis

- Government Pest Control Procurement Analysis

- Residential and Institutional Pest Control Consumption Analysis

- Decision-Making Process and Purchase Criteria

- Key Pain Points and Product Preferences

- By Market Value (2026-2035)

- By Sales Volume (2026-2035)

- By Average Realized Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now