Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA Lane Departure Warning Systems (LDWS) market is valued at approximately USD ~ million for 2024. This market’s growth is driven by the increasing adoption of Advanced Driver Assistance Systems (ADAS) in Saudi Arabia, supported by both consumer demand for safety and government regulations focused on road safety and accident reduction. With a growing fleet of vehicles and the enforcement of new automotive safety laws, LDWS technology is experiencing higher penetration in both passenger and commercial vehicles. This growth is further fueled by collaborations between international technology providers and local automotive manufacturers, allowing the technology to become more accessible to the Saudi market. Dominant Cities/Countries That Dominate the Market and Why Saudi Arabia’s urban centers, especially Riyadh, Jeddah, and Dammam, dominate the KSA LDWS market due to their high vehicle ownership rates, rapid urbanization, and ongoing infrastructure improvements. Riyadh, as the capital, has seen significant investments in transportation safety technologies, driving the demand for ADAS features such as LDWS. Additionally, the KSA government’s strong push for safer road systems, along with rising consumer awareness about the benefits of vehicle safety systems, further reinforces the demand in these regions. Moreover, government-backed initiatives and a booming automotive market in these areas fuel the growth of LDWS.

Market Segmentation

By Product Type

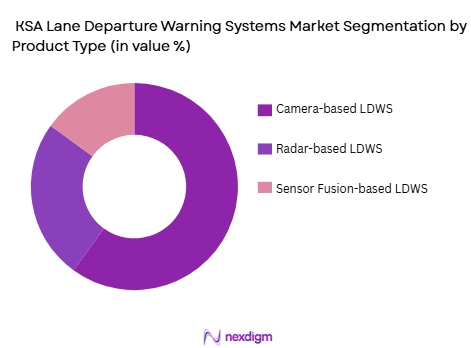

The KSA Lane Departure Warning Systems market is segmented by product type into camera-based systems, radar-based systems, and sensor fusion systems. Among these, camera-based LDWS has the dominant market share in 2024, owing to its affordability, ease of integration, and high efficiency in detecting lane markings, which are crucial for accurate lane departure alerts. The widespread adoption of camera-based systems is largely attributed to their lower cost compared to sensor fusion solutions, making them a preferred option in budget-conscious vehicle models. Furthermore, advancements in camera technologies, including enhanced image processing algorithms, have made these systems more reliable, contributing to their market dominance.

By Vehicle Type

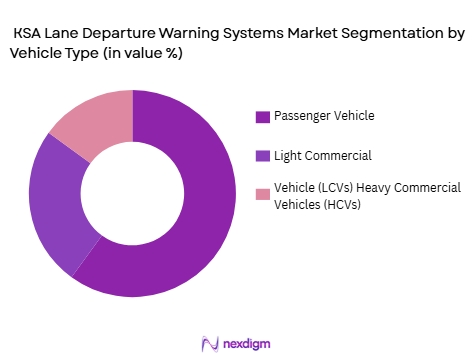

The LDWS market in Saudi Arabia is segmented by vehicle type into passenger vehicles, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs). The passenger vehicle segment holds the largest market share in 2024, driven by the growing demand for ADAS features in private cars, spurred by rising safety awareness and consumer preference for premium features. As the adoption of ADAS technologies in passenger cars grows, LDWS systems have become an essential feature in mid to high-end vehicles. Additionally, the expansion of automotive production by international OEMs in Saudi Arabia, focusing on consumer safety, has fueled the market demand for LDWS in passenger vehicles.

Competitive Landscape

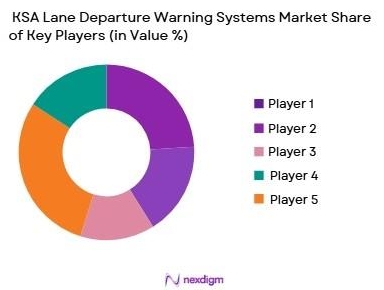

The KSA LDWS market is characterized by a blend of global automotive players and local technology providers. Leading companies such as Robert Bosch, Continental, and Mobileye dominate the market due to their established presence in the ADAS industry, robust R&D capabilities, and strong distribution networks. Additionally, local manufacturers and tier-1 suppliers in Saudi Arabia are expanding their operations to meet the growing demand for automotive safety features. As a result, strategic partnerships and joint ventures between global suppliers and local players are emerging to accelerate the market penetration of LDWS systems in Saudi Arabia.

|

Company Name |

Establishment Year |

Headquarters |

Technology Focus |

Market Presence |

R&D Capabilities |

Distribution Channels |

|

Robert Bosch GmbH |

1886 |

Germany |

~ |

`~ |

~ |

~ |

|

Continental AG |

1871 |

Germany |

~ |

~ |

~ |

~ |

|

Mobileye (Intel) |

1999 |

Israel |

~ |

~ |

~ |

~ |

|

Denso Corporation |

1949 |

Japan |

~ |

~ |

~ |

~ |

|

Aptiv PLC |

1994 |

Ireland |

~ |

~ |

~ |

~ |

Indonesia Air Quality Monitoring System Market Analysis

Growth Drivers

Urbanization

Urbanization in Indonesia is rapidly increasing, with over ~ of the population now residing in urban areas, a trend that is expected to continue as more people migrate to cities in search of better employment opportunities. In 2022, the urban population reached approximately 164 million out of a total population of ~million. As cities like Jakarta face growing traffic congestion and industrial activity, air quality issues have become a serious concern. The demand for air quality monitoring systems is being fueled by the need for real-time data to manage pollution in these increasingly populated areas. This rise in urbanization necessitates the expansion of air quality monitoring infrastructure to ensure compliance with health standards.

Industrialization

Indonesia’s industrial sector has been a major contributor to the country’s economic growth, accounting for approximately ~ of GDP in 2024. This sector includes oil refineries, cement plants, and manufacturing facilities, all of which are significant sources of air pollution, especially in key industrial regions like Java and Sumatra. The increase in industrial activities has intensified the demand for air quality monitoring systems to mitigate pollution risks. Indonesia’s heavy reliance on coal for energy production further exacerbates the situation, requiring more robust monitoring and regulatory enforcement to control emissions and improve public health outcomes.

Restraints

High Initial Costs

The installation and maintenance of air quality monitoring systems in Indonesia are cost-prohibitive, especially in regions outside major urban areas. Advanced monitoring technologies like reference-grade sensors and the integration of IoT-based devices can cost millions of dollars. The initial cost of setting up a national or provincial network of air quality monitoring stations is a significant barrier, particularly for regional governments with limited budgets. Despite funding from international organizations, high upfront costs for equipment, installation, and calibration often delay the widespread deployment of comprehensive air monitoring systems.

Technical Challenges

Indonesia faces various technical challenges in deploying effective air quality monitoring systems. The maintenance and calibration of air quality monitoring sensors, which require technical expertise, are often hindered by the lack of skilled labor and remote locations. Additionally, integrating data from various sensors, such as particulate matter detectors and gas analyzers, into a cohesive system that provides reliable real-time data is technically demanding. These technical challenges limit the ability of smaller cities and rural areas to benefit from real-time pollution data, ultimately reducing the effectiveness of nationwide air quality monitoring efforts.

Opportunities

Technological Advancements

Technological advancements present significant opportunities for improving Indonesia’s air quality monitoring infrastructure. The integration of IoT-based sensors has drastically reduced the cost of deploying air quality monitoring systems. These sensors offer high precision and can be easily scaled across large urban and rural areas. Additionally, machine learning algorithms are enhancing the predictive capabilities of air quality monitoring systems, enabling authorities to forecast pollution spikes and respond proactively. As Indonesia moves toward a smart city vision, incorporating advanced technologies into air quality management will play a pivotal role in improving air quality and health outcomes.

International Collaborations

International collaborations have significantly boosted Indonesia’s air quality monitoring efforts. Initiatives like the Clean Air Asia Program have facilitated the transfer of advanced technology and expertise, helping local agencies implement more accurate air quality monitoring systems. These partnerships also provide financial assistance for setting up monitoring networks in areas that are otherwise underserved. Indonesia’s collaboration with global environmental organizations strengthens its ability to address air pollution effectively and accelerates the deployment of necessary technologies for widespread air quality assessment.

Future Outlook

Over the next five years, the KSA Lane Departure Warning Systems market is projected to witness substantial growth. This growth will be driven by continuous government support for road safety and the widespread adoption of ADAS technologies, which will become standard in many vehicle models. Furthermore, advancements in sensor fusion and AI technology will further enhance the capabilities of LDWS systems, contributing to better accuracy and lower costs. The rise of electric vehicles (EVs) and the integration of ADAS in EV platforms will also provide new opportunities for LDWS deployment, paving the way for further market expansion.

Major Players

- Robert Bosch GmbH

- Continental AG

- Mobileye (Intel)

- Denso Corporation

- Aptiv PLC

- Magna International Inc.

- Valeo SA

- Hyundai Mobis Co. Ltd.

- Autoliv Inc.

- NXP Semiconductors NV

- Hella GmbH & Co. KGaA

- Infineon Technologies AG

- Bosch Mobility Solutions

- ZF Friedrichshafen AG

- Nissan Motor Co.

Key Target Audience

- Automotive OEMs

- Tier-1 Automotive Suppliers

- Automotive Component Manufacturers

- Fleet Management Companies

- Insurance Companies

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies Automotive Distributors and Dealerships

Research Methodology

Step 1: Identification of Key Variables

The first phase of the research involves identifying all the key variables that influence the KSA Lane Departure Warning Systems market. This includes understanding vehicle safety standards, local market dynamics, and consumer demand for ADAS technologies. We will utilize both secondary and primary data from automotive manufacturers, suppliers, and regulatory bodies.

Step 2: Market Analysis and Construction

The second step involves gathering historical market data to analyze trends and project future growth. This will include vehicle fleet data, penetration rates of ADAS features, and regulatory trends from the Saudi government, offering insights into the expected demand for LDWS systems.

Step 3: Hypothesis Validation and Expert Consultation

We will conduct expert consultations with automotive industry leaders, tier-1 suppliers, and technology developers to validate hypotheses regarding market growth drivers, consumer preferences, and barriers to adoption.

Step 4: Research Synthesis and Final Output

In this phase, we will synthesize all collected data to present a comprehensive market analysis. This includes validating data through in-depth consultations with industry experts, OEMs, and local dealers, ensuring that the final report is both reliable and actionable.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing demand for advanced safety features in vehicles

Rising adoption of ADAS in both passenger and commercial vehicles

Government regulations promoting road safety standards - Market Challenges

High costs associated with advanced sensor technologies

Complexity in integration with existing vehicle systems

Limited awareness and adoption in some vehicle segments - Market Opportunities

Growth in electric vehicle adoption

Increasing demand for autonomous driving solutions

Development of affordable and scalable ADAS systems - Trends

Shift towards fully integrated safety systems

Technological advancements in sensor fusion and AI

Growing focus on driver assistance systems for all vehicle types - Government regulations

Mandates for lane-keeping assistance systems

Government incentives for vehicle safety features

Regulations for vehicle automation and autonomous driving - SWOT analysis

Strength: High demand for safety and driver assistance features

Weakness: High implementation costs

Opportunity: Expansion of ADAS features in electric and autonomous vehicles - Porters 5 forces

Threat of new entrants: High due to technological innovation

Bargaining power of buyers: Moderate as adoption rates grow

Bargaining power of suppliers: High with reliance on sensor manufacturers

- By Market Value ,2019-2025

- By Installed Units ,2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Camera-based systems

Radar-based systems

Lidar-based systems

Infrared-based systems

Multi-sensor fusion systems - By Platform Type (In Value%)

Standalone systems

Integrated vehicle systems

Aftermarket systems

OEM vehicle systems

ADAS (Advanced Driver Assistance Systems) platform - By Fitment Type (In Value%)

Factory-installed systems

Aftermarket systems

OEM fitment systems

Retrofit systems

Modular systems - By EndUser Segment (In Value%)

Passenger vehicles

Commercial vehicles

Heavy-duty trucks

Electric vehicles

Autonomous vehicles - By Procurement Channel (In Value%)

Direct sales

Online distribution

Automotive dealerships

OEM partnerships

Third-party distributors

- Cross Comparison Parameters(Market share, System type, Technological advancements, Vehicle segment, Regulatory compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Bosch

Continental AG

Denso Corporation

Valeo

Magna International

Autoliv

Aptiv

ZF Friedrichshafen

Gentex Corporation

TRW Automotive

Mobileye

Delphi Automotive

Eaton Corporation

Harman International

Marelli

- Passenger vehicle manufacturers increasingly adopting ADAS

- Commercial vehicle fleets investing in safety solutions

- Integration of lane departure systems in electric and autonomous vehicles

- Emerging aftermarket installation of ADAS systems in older vehicles

- Forecast Market Value ,2026-2030

- Forecast Installed Units ,2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform ,2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now