Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the KSA Last-Mile Delivery market generated approximately USD ~ billion in logistics service revenue, supported by rapid growth in e-commerce transactions, food delivery platforms, and digital retail expansion. The market is driven by rising online consumer purchases, increased demand for express delivery services, and the expansion of integrated logistics infrastructure. Government initiatives supporting digital commerce, logistics modernization, and smart mobility also contribute to operational growth, enabling logistics providers to enhance delivery networks, fleet capacity, and technology-enabled dispatch systems.

Major logistics activity is concentrated in Riyadh, Jeddah, and Dammam where dense urban populations, strong retail infrastructure, and high digital adoption drive parcel delivery demand. Riyadh functions as the primary logistics coordination hub supported by government institutions, corporate headquarters, and national distribution centers. Jeddah benefits from its role as a commercial gateway through Jeddah Islamic Port, while Dammam supports industrial supply chains linked to the Eastern Province manufacturing and energy sectors. These metropolitan areas provide advanced road infrastructure, large consumer bases, and proximity to fulfillment centers that support efficient last-mile delivery operations.

Market Segmentation

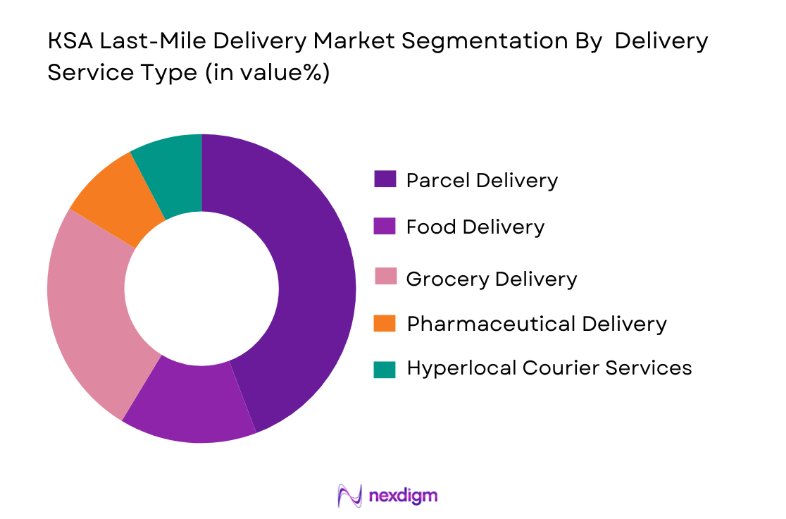

By Delivery Service Type

KSA Last-Mile Delivery market is segmented by delivery service type into parcel delivery, food delivery, grocery delivery, pharmaceutical delivery, and hyperlocal courier services. Recently, parcel delivery has a dominant market share due to factors such as strong e-commerce growth, rising cross-border online retail orders, and increasing consumer expectations for rapid home deliveries. Large online marketplaces and retailers rely heavily on parcel logistics networks to manage high daily shipment volumes. Logistics providers have expanded automated sorting hubs, micro-fulfillment centers, and digital route optimization systems to manage rising order flows. Retailers are integrating omnichannel strategies combining physical stores with online fulfillment, further boosting parcel delivery demand. Additionally, government support for logistics infrastructure development and digital commerce has strengthened parcel delivery networks across major cities and secondary urban areas.

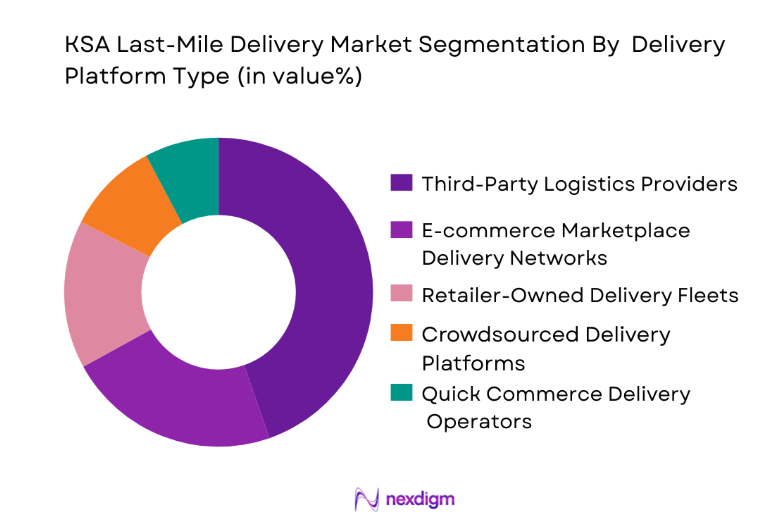

By Delivery Platform Type

KSA Last-Mile Delivery market is segmented by delivery platform type into third-party logistics providers, e-commerce marketplace delivery networks, retailer-owned delivery fleets, crowdsourced delivery platforms, and quick commerce delivery operators. Recently, third-party logistics providers have a dominant market share due to their established logistics infrastructure, extensive fleet networks, and partnerships with multiple retailers and e-commerce platforms. These providers offer scalable delivery capacity that allows businesses to outsource last-mile logistics operations efficiently. Advanced tracking technologies, integrated warehouse management systems, and route optimization software enable high delivery efficiency. Third-party logistics companies also benefit from long-standing partnerships with international courier firms and local distribution networks, which help support nationwide delivery coverage and reliable service quality.

Competitive Landscape

The KSA Last-Mile Delivery market features a moderately consolidated competitive structure where a mix of international logistics firms, regional courier companies, and digital delivery platforms compete for market share. Global players leverage advanced logistics technology and established supply chains, while local companies benefit from regional knowledge and partnerships with domestic retailers. Increasing e-commerce activity has encouraged investments in automated fulfillment centers, digital delivery management systems, and route optimization platforms. Strategic collaborations between retailers, logistics providers, and technology companies continue to shape competitive positioning.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Delivery Fleet Size |

| Aramex | 1982 | Dubai, UAE | ~ | ~ | ~ | ~ | ~ |

| Saudi Post SPL | 1926 | Riyadh, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| SMSA Express | 1994 | Riyadh, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| DHL eCommerce | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| UPS | 1907 | Atlanta, USA | ~ | ~ | ~ | ~ | ~ |

KSA Last-Mile Delivery Market Analysis

Growth Drivers

Expansion of E-commerce Platforms and Digital Retail Infrastructure

The rapid growth of digital commerce ecosystems across Saudi Arabia has significantly accelerated demand for last-mile delivery services. Increasing smartphone penetration, digital payment adoption, and online retail platforms have transformed consumer purchasing behavior across urban centers. Major e-commerce platforms including Amazon, Noon, and regional digital retailers process large daily order volumes that require reliable parcel distribution networks. Logistics companies are investing heavily in automated sorting hubs, advanced dispatch software, and route optimization technologies to manage rising delivery volumes efficiently. Retail companies are integrating omnichannel distribution models combining physical retail outlets with online order fulfillment systems to improve delivery speed. Government programs supporting digital transformation and entrepreneurship encourage the expansion of online businesses that depend on efficient logistics networks. The growth of cross-border e-commerce shipments also increases demand for international parcel delivery services within the country. Urban population concentration in major cities further supports high order density which improves delivery efficiency for logistics operators. These factors collectively strengthen the operational scale and revenue generation potential of last-mile logistics companies operating in the Saudi market.

Rising Demand for Express Delivery and Same-Day Logistics Services

Consumer expectations for faster delivery timelines have transformed logistics operations across Saudi Arabia’s retail and e-commerce sectors. Online shoppers increasingly expect same-day or next-day delivery services for products including electronics, groceries, and household items. Food delivery platforms have normalized rapid order fulfillment within short timeframes, influencing expectations for other retail categories as well. Logistics providers are expanding micro-fulfillment centers and dark stores located near urban neighborhoods to reduce delivery distances and improve operational efficiency. Technology-driven route optimization systems enable delivery drivers to complete more orders within shorter time windows. Retailers are partnering with specialized logistics firms to ensure reliable express delivery coverage across major metropolitan regions. Investments in advanced logistics management software and real-time order tracking platforms further enhance customer experience and operational transparency. These improvements support higher order volumes and improve service reliability for delivery providers. As digital commerce continues expanding, rapid delivery capabilities are becoming a critical competitive differentiator for logistics companies operating within the Saudi last-mile ecosystem.

Market Challenges

High Operational Costs and Complex Urban Delivery Networks

Operating last-mile delivery services across Saudi Arabia presents substantial operational challenges due to high transportation costs and complex urban logistics conditions. Delivery companies must maintain large vehicle fleets, distribution centers, and driver networks to manage growing order volumes. Fuel costs, vehicle maintenance expenses, and labor costs significantly increase operating expenditures for logistics providers. Traffic congestion in major metropolitan areas such as Riyadh and Jeddah can also reduce delivery efficiency and extend delivery times. Logistics companies must invest in advanced route optimization technologies to improve operational productivity and reduce delays. Additionally, expanding delivery coverage into suburban and remote areas requires additional logistics infrastructure and increases operational complexity. Maintaining consistent service quality while managing large delivery networks requires sophisticated logistics management systems and operational expertise. Competition among logistics providers also puts pressure on delivery pricing which reduces profit margins. These factors collectively create operational cost pressures for companies operating in the last-mile delivery market.

Workforce Management and Driver Availability Constraints

The availability and management of delivery workforce remains a major challenge for logistics providers operating in the Saudi last-mile delivery ecosystem. Rapid growth in order volumes requires companies to continuously recruit and train new delivery drivers. Managing large driver networks requires advanced workforce scheduling systems and performance monitoring technologies. Logistics companies must also ensure compliance with labor regulations and transportation safety standards which increase administrative complexity. Driver retention can be difficult due to demanding work schedules and fluctuating delivery volumes during peak seasons. Delivery providers must offer competitive compensation and incentives to maintain stable workforce capacity. Training programs are also required to ensure drivers are familiar with navigation technologies, customer service practices, and delivery procedures. High driver turnover can disrupt delivery operations and reduce service quality if not managed effectively. Logistics companies must therefore invest in workforce management platforms and human resource strategies to maintain stable delivery capacity.

Opportunities

Development of Smart Logistics Infrastructure and Automation Technologies

Rapid technological innovation across logistics and supply chain management is creating significant opportunities for the Saudi last-mile delivery market. Logistics providers are adopting artificial intelligence driven route planning systems that optimize delivery paths and reduce operational costs. Automated sorting facilities and robotic warehouse technologies improve parcel handling efficiency and accelerate order processing. Real-time shipment tracking platforms enhance customer visibility and operational transparency for logistics providers. Delivery management software allows companies to coordinate drivers, track delivery performance, and optimize fleet utilization across multiple distribution hubs. Smart logistics infrastructure also includes advanced data analytics systems that analyze delivery demand patterns and improve operational planning. These technologies enable logistics companies to improve service quality while reducing operational expenses. As Saudi Arabia invests heavily in digital transformation initiatives and smart city development, logistics companies are expected to adopt more automation technologies that enhance delivery efficiency and scalability across urban logistics networks.

Expansion of Quick Commerce and Hyperlocal Delivery Ecosystems

The emergence of quick commerce platforms and hyperlocal retail logistics is creating new growth opportunities for last-mile delivery providers in Saudi Arabia. Quick commerce platforms specialize in delivering groceries, pharmaceuticals, and convenience products within short timeframes through localized distribution centers. These operations rely heavily on dense urban delivery networks and digital order management systems. Retailers are establishing dark stores and micro fulfillment facilities located near residential neighborhoods to accelerate order processing and reduce delivery times. Hyperlocal delivery models also support small businesses and restaurants that rely on digital platforms to reach consumers. Logistics companies that partner with these platforms gain access to high-frequency delivery demand across urban areas. The growth of food delivery and grocery delivery platforms further strengthens this ecosystem by increasing daily delivery volumes. As consumer demand for convenience and rapid delivery continues expanding, quick commerce logistics models are expected to become a major revenue source for last-mile delivery service providers.

Future Outlook

The KSA Last-Mile Delivery market is expected to experience strong growth driven by continued expansion of e-commerce platforms and digital retail infrastructure. Logistics companies are likely to invest heavily in automation technologies, smart logistics systems, and electric delivery vehicles to improve operational efficiency. Government support for logistics sector development under national economic diversification strategies will strengthen infrastructure investments. Growing demand for faster delivery services, combined with rising online retail penetration, will continue driving expansion of last-mile delivery networks across major urban and suburban regions.

Major Players

- Aramex

- SMSA Express

- Saudi Post SPL

- DHL eCommerce

- UPS

- FedEx

- NaqelExpress

- Careem Express

- Fetchr

- ShipaDelivery

- Amazon Logistics

- Mrsool

- Jahez

- ToYou

- Noon Logistics

Key Target Audience

- Logistics and supply chain companies

- E-commerce and online retail companies

- Food delivery platform operators

- Retail distribution companies

- Transportation infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Technology andlogisticssoftware providers

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying critical variables that influence the KSA Last-Mile Delivery market including logistics infrastructure, e-commerce transaction volumes, delivery fleet capacity, consumer purchasing patterns, and regulatory frameworks affecting logistics operations.

Step 2: Market Analysis and Construction

Market size estimation and structural analysis are conducted using trade datasets, logistics industry reports, government transport statistics, and financial disclosures of logistics companies operating in Saudi Arabia.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics operators, supply chain specialists, and transportation analysts are consulted to validate market assumptions, operational challenges, and emerging technology adoption trends.

Step 4: Research Synthesis and Final Output

All collected data and expert insights are synthesized into a structured analytical framework that presents comprehensive market insights, segmentation analysis, and strategic industry outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Expansion of E-commerce Platforms Across Saudi Arabia

Rising Demand for Same-Day and Express Delivery Services

Government Investments in Digital Commerce and Logistics Infrastructure - Market Challenges

High Operational Costs in Urban Delivery Networks

Traffic Congestion and Last-Mile Route Optimization Issues

Workforce Management and Driver Availability Constraints - Market Opportunities

Expansion of Quick Commerce and Hyperlocal Delivery Models

Adoption of Smart Logistics Technologies and Route Optimization Systems

Growth in Delivery Demand from SMEs and Digital Retail Startups - Trends

Integration of Artificial Intelligence for Delivery Route Optimization

Expansion of Electric Delivery Vehicles and Sustainable Logistics

Growth of Dark Stores and Micro Fulfillment Centers - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Delivery Services

Same-Day Delivery Services

On-Demand Delivery Services

Food & Grocery Delivery Services

Hyperlocal Delivery Services - By Platform Type (In Value%)

E-commerce Marketplace Platforms

Retailer-Owned Delivery Platforms

Third-Party Logistics Platforms

Aggregator Delivery Platforms

Quick Commerce Platforms - By Fitment Type (In Value%)

In-House Delivery Fleet

Third-Party Delivery Partners

Crowdsourced Delivery Networks

Hybrid Delivery Models

Contracted Logistics Providers - By EndUser Segment (In Value%)

E-commerce Retailers

Food and Beverage Platforms

Grocery and Quick Commerce Providers

Pharmaceutical and Healthcare Retailers

Consumer Electronics and Lifestyle Retailers - By Procurement Channel (In Value%)

Direct Logistics Service Contracts

Platform-Based Delivery Procurement

Retailer Managed Delivery Agreements

- Market Share Analysis

- CrossComparison Parameters (Delivery Network Coverage, Technology Platform Integration, Average Delivery Time, Fleet Size and Vehicle Types, Pricing Structure)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Aramex

SMSA Express

Saudi Post SPL

Fetchr

Naqel Express

Careem Express

Jeeny Logistics

Jahez

Mrsool

ToYou

DHL eCommerce

UPS Saudi Arabia

FedEx Saudi Arabia

Amazon Logistics

hipa Delivery

- E-commerce Retailers Driving High Volume Parcel Delivery Demand

- Food Delivery Platforms Expanding On-Demand Logistics Operations

- Retail Chains Investing in Integrated Omnichannel Delivery Systems

- Healthcare and Pharmacy Retailers Increasing Home Delivery Services

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now