Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA mammography equipment market is valued at USD ~ million, driven by the increasing demand for advanced imaging technologies and government investments in healthcare infrastructure. Rising breast cancer awareness and early detection initiatives are expected to further enhance market expansion. The market is supported by a rising prevalence of breast cancer and a growing number of diagnostic centers across the region. The government’s commitment to improving healthcare facilities contributes to the market’s growth potential. Technological advancements in digital mammography are also a significant factor influencing market demand.

Key cities in the KSA mammography equipment market include Riyadh, Jeddah, and Mecca, with Riyadh holding a central position due to its status as the capital and major medical hub. These cities benefit from a concentration of healthcare facilities, research institutes, and medical infrastructure. Riyadh, in particular, hosts numerous hospitals equipped with state-of-the-art technology, while Jeddah and Mecca are growing hubs for healthcare services driven by the large volume of patients seeking treatment and diagnostic services. The dominance of these cities can be attributed to their strong economic development, healthcare policy support, and a higher volume of medical procedures.

Market Segmentation

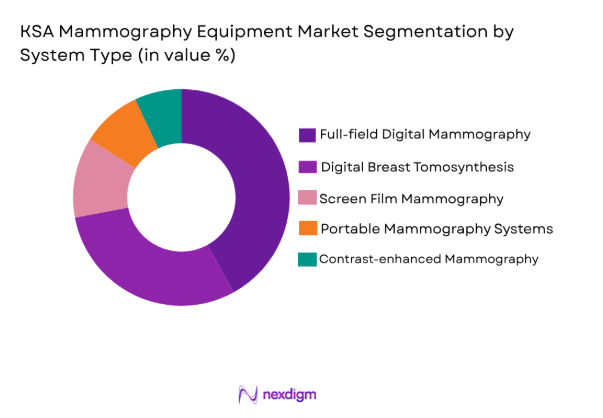

By System Type (In Value%)

The KSA mammography equipment market is segmented by system type into full-field digital mammography (FFDM), digital breast tomosynthesis (DBT), screen film mammography, portable mammography systems, and contrast-enhanced mammography systems. Recently, full-field digital mammography (FFDM) has a dominant market share due to its widespread adoption across hospitals and diagnostic centers, supported by its high image clarity, faster processing time, and compatibility with digital healthcare infrastructure. The system’s cost-effectiveness compared to advanced 3D systems, along with strong government-backed screening programs, has reinforced its leading position in the market.

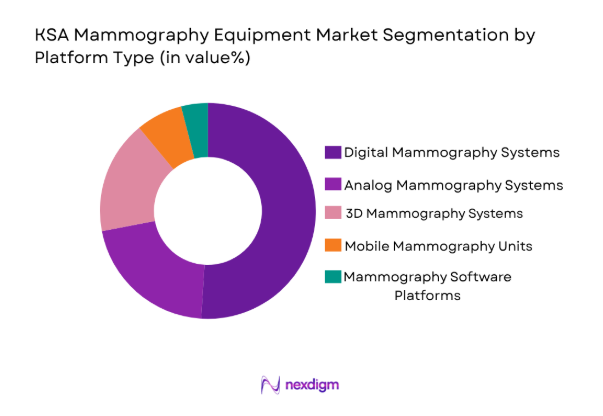

By Platform Type (In Value%)

The KSA mammography equipment market is segmented by platform type into analog mammography systems, digital mammography systems, 3D mammography systems, mobile mammography units, and mammography software platforms. Recently, digital mammography systems have a dominant market share due to their superior diagnostic accuracy, faster image processing, and seamless integration with hospital information systems. The strong shift toward digital healthcare infrastructure, combined with government-supported screening initiatives and increasing preference among radiologists for high-resolution imaging, has reinforced the adoption of digital platforms across major healthcare facilities.

Competitive Landscape

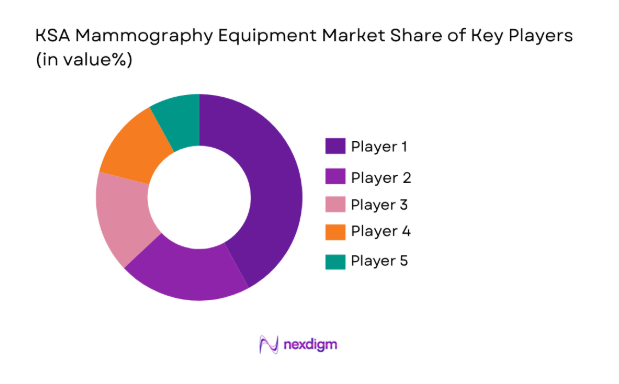

The KSA mammography equipment market is characterized by a mix of global and regional players, with consolidation occurring through mergers and strategic partnerships. Major companies dominate the landscape due to their technological innovations and extensive distribution networks. The competition is also influenced by factors such as service quality, after-sales support, and price competitiveness, leading to increased market dynamics. Additionally, new entrants are targeting emerging regions, capitalizing on the growing healthcare sector and government investments in medical technology.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Million) | Key Parameter |

| GE Healthcare | 1892 | Chicago, USA | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Amsterdam, Netherlands | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Erlangen, Germany | ~ | ~ | ~ | ~ | ~ |

| Hologic Inc. | 1985 | Bedford, USA | ~ | ~ | ~ | ~ | ~ |

| Fujifilm Medical Systems | 1934 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ |

KSA Mammography Equipment Market Analysis

Growth Drivers

Rising Prevalence of Breast Cancer

The rising prevalence of breast cancer is a key growth driver for the KSA mammography equipment market. With an increasing number of diagnosed cases, early detection has become a priority for healthcare systems. As healthcare professionals and institutions emphasize the importance of screening, demand for mammography systems has surged. The growing recognition of the benefits of early detection further drives the adoption of advanced diagnostic tools, including digital and 3D mammography. These systems are crucial in ensuring accurate and timely diagnosis, reducing mortality rates. Additionally, the rising awareness of breast cancer risks among women and healthcare providers has significantly boosted the demand for mammography services. Governments in the region are also implementing policies to increase cancer screening rates, contributing to the market growth. Increased public health campaigns and partnerships with international organizations support the demand for better diagnostic equipment. This ensures that the healthcare infrastructure remains prepared to address the increasing incidence of breast cancer and to meet the needs of patients across the region.

Technological Advancements in Mammography Equipment

Technological advancements in mammography equipment are reshaping the KSA market. The integration of digital breast tomosynthesis (DBT) and the ongoing improvements in image quality, radiation reduction, and system efficiency are driving demand for advanced mammography systems. As healthcare providers continue to prioritize precision medicine and accurate diagnostics, modern technologies offer significant benefits, including improved detection of breast cancer at early stages. The transition from traditional film-based systems to digital mammography systems has also played a crucial role in enhancing diagnostic accuracy. Innovations such as portable mammography units and the development of software that integrates artificial intelligence (AI) to assist radiologists have expanded the reach of these systems. Moreover, the introduction of more affordable and efficient solutions has made it easier for healthcare providers to invest in high-end imaging technologies. These advancements ensure a better user experience for patients and healthcare professionals, contributing to increased adoption rates. Additionally, as global manufacturers focus on technological upgrades and localized solutions, the KSA market is witnessing a steady rise in the demand for cutting-edge imaging devices.

Market Challenges

High Initial Investment Costs

High initial investment costs represent a significant challenge in the KSA mammography equipment market. Despite the growing demand for advanced mammography systems, the high upfront cost of purchasing and installing these systems often limits the number of healthcare facilities able to afford them. This barrier is especially significant for smaller hospitals and diagnostic centers, which may lack the financial resources for such investments. Additionally, the installation and maintenance costs associated with advanced systems, including digital and 3D mammography units, further add to the financial burden. While the long-term benefits of these systems, such as enhanced diagnostic capabilities and improved patient outcomes, are clear, the high capital expenditure required at the outset often results in delayed adoption. This challenge is further compounded by the need for healthcare providers to invest in training medical staff to operate these advanced systems, leading to additional financial and time-related constraints. As a result, healthcare providers must carefully evaluate their budgets and prioritize investments, which can delay the expansion and modernization of mammography services across the region.

Regulatory and Certification Barriers

Regulatory and certification barriers also pose a challenge to the KSA mammography equipment market. The stringent requirements imposed by regulatory authorities on the approval and certification of mammography equipment can delay the introduction of new technologies into the market. Additionally, the complex and time-consuming processes required for ensuring compliance with local and international standards can act as a deterrent for both manufacturers and healthcare providers. Ensuring that equipment meets the required safety, quality, and performance standards necessitates thorough testing, documentation, and validation, which can lead to longer approval timelines. Furthermore, the inconsistent implementation of regulations across different regions within the kingdom can result in delays and complications for companies seeking to expand their operations or introduce new products. As the market grows, manufacturers must navigate this complex regulatory environment while ensuring their products meet the diverse needs of healthcare providers. This challenge can ultimately impact the speed at which healthcare systems can modernize and enhance their diagnostic capabilities.

Opportunities

Expanding Healthcare Infrastructure

One of the most significant opportunities in the KSA mammography equipment market is the expanding healthcare infrastructure. The Saudi government is heavily investing in healthcare facilities as part of its Vision 2030 initiative, which aims to modernize and expand the healthcare sector. These investments provide a tremendous opportunity for manufacturers of mammography equipment to enter the market and cater to the growing demand for high-quality diagnostic systems. The expansion of hospitals, diagnostic centers, and research institutions across both urban and rural areas of KSA is expected to increase the need for advanced mammography technologies. As healthcare providers look to offer better services to the population, the demand for sophisticated imaging equipment will rise. Moreover, the establishment of more specialized centers dedicated to breast cancer screening and early detection will further drive the demand for mammography equipment. As infrastructure continues to expand, there will be a heightened focus on ensuring that new facilities are equipped with state-of-the-art diagnostic tools, creating a lucrative market for mammography system manufacturers.

Government Support for Preventive Healthcare

The Saudi government’s increasing focus on preventive healthcare presents a significant opportunity for the mammography equipment market. As part of its public health strategy, the government is encouraging the implementation of nationwide screening programs, particularly for breast cancer, to detect and treat conditions at earlier stages. These efforts align with the global trend toward early detection and intervention, which helps reduce healthcare costs and improves patient outcomes. Through partnerships with international organizations and local healthcare providers, the government is promoting awareness campaigns and screening programs across the country. This growing focus on preventive healthcare will continue to drive demand for mammography equipment. Moreover, the government is providing financial support and incentives for healthcare facilities to adopt modern technologies that can contribute to better diagnosis and treatment. This policy support, combined with increased public awareness, creates a favorable environment for the continued growth of the mammography equipment market.

Future Outlook

The future outlook for the KSA mammography equipment market is positive, with substantial growth expected over the next five years. The market will benefit from continuous advancements in imaging technologies, including the integration of AI and 3D mammography systems. Increasing government support for preventive healthcare and breast cancer screening programs will further drive demand. The expansion of healthcare infrastructure and rising awareness of early detection will contribute to a significant rise in market value. Technological innovations and regulatory support will play key roles in shaping the market, ensuring continued growth and development.

Major Players

- GE Healthcare

- Philips Healthcare

- Siemens Healthineers

- Hologic Inc.

- Fujifilm Medical Systems

- Canon Medical Systems

- Samsung Medison

- Carestream Health

- Konica Minolta Healthcare

- Agfa Healthcare

- KUB Technologies

- Analogic Corporation

- Mindray Medical International

- Allegers Medical Systems

- BPL Medical Technologies

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hospitals and healthcare systems

- Diagnostic centers

- Medical device distributors

- Healthcare providers and practitioners

- Cancer research organizations

Research Methodology

Step 1: Identification of Key Variables

Key market variables were identified through an in-depth analysis of the healthcare sector in KSA, focusing on mammography equipment usage and demand trends. Additional variables such as pricing trends, procurement cycles, and technology adoption rates were also evaluated to strengthen the analytical framework. Macroeconomic indicators, healthcare expenditure patterns, and demographic factors were incorporated to ensure a comprehensive variable base.

Step 2: Market Analysis and Construction

Market data was collected from credible primary and secondary sources, including healthcare reports, industry surveys, and expert interviews.

Data triangulation techniques were applied to validate consistency across multiple sources and improve reliability. Segment-wise analysis was conducted to construct a detailed and structured representation of the market landscape.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were tested with industry experts, radiologists, and equipment manufacturers to ensure accuracy in the market model. Feedback loops with key opinion leaders helped refine assumptions and align findings with real-world dynamics.

Cross-verification with procurement managers and hospital administrators enhanced the robustness of conclusions.

Step 4: Research Synthesis and Final Output

The findings were synthesized, reviewed, and compiled into a final market report, with conclusions drawn based on validated data and expert insights. Advanced analytical tools and forecasting models were used to generate forward-looking insights. Final outputs were subjected to quality checks to ensure clarity, accuracy, and actionable intelligence.

- Executive Summary

- Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Prevalence of Breast Cancer

Technological Advancements in Imaging Systems

Increased Government Support for Healthcare Initiatives - Market Challenges

High Initial Investment Costs

Shortage of Skilled Professionals

Regulatory and Certification Barriers - Market Opportunities

Expanding Healthcare Infrastructure

Increasing Focus on Early Breast Cancer Detection

Rising Awareness and Adoption of Preventive Healthcare - Trends

Shift Towards 3D Mammography Systems

Integration of AI with Mammography Systems - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Full-field Digital Mammography (FFDM)

Digital Breast Tomosynthesis (DBT)

Screen Film Mammography

Portable Mammography

Contrast-enhanced Mammography - By Platform Type (In Value%)

Digital Mammography Systems

Analog Mammography Systems

3D Mammography Systems

Mobile Mammography Units

Mammography Software Platforms - By Fitment Type (In Value%)

Fixed Mammography Systems

Mobile Mammography Systems

Portable Mammography Systems

Mammography Equipment Components - By End User Segment (In Value%)

Hospitals

Diagnostic Centers

Research and Academic Institutions

- Hospitals and Healthcare Institutions

- Diagnostic Centers and Clinics

- Research Institutes and Academic Organizations

- Private and Public Health Insurance Providers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Forecast Average System Price, 2026-2035

- Forecast by System Complexity Tier, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now