Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Saudi Arabia’s medical devices sector represents one of the largest healthcare technology markets in the Middle East, supported by strong public healthcare investment and rapid hospital infrastructure expansion. Based on a recent historical assessment, the KSA medical devices market was valued at approximately USD ~ billion according to data published by the Saudi Food and Drug Authority and international healthcare trade statistics. Demand is driven by hospital modernization, rising chronic disease prevalence, increasing diagnostic requirements, and continuous procurement of advanced imaging, monitoring, and surgical technologies across healthcare facilities.

Riyadh, Jeddah, and Dammam dominate the medical devices market due to the concentration of large tertiary hospitals, advanced private healthcare networks, and government medical cities equipped with high-technology treatment infrastructure. These metropolitan healthcare hubs host major procurement programs for imaging systems, surgical robotics, and diagnostic technologies. Strong logistics connectivity, presence of international healthcare providers, and centralized procurement channels further strengthen device distribution and technology adoption across major Saudi healthcare institutions and specialty clinics.

Market Segmentation

By Product Type

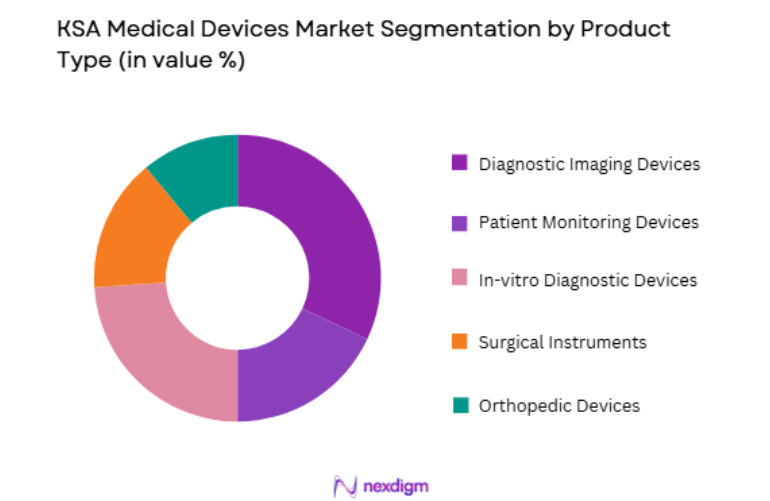

KSA Medical Devices market is segmented by product type into Diagnostic Imaging Devices, Patient Monitoring Devices, In-vitro Diagnostic Devices, Surgical Instruments, and Orthopedic Devices. Recently, Diagnostic Imaging Devices has a dominant market share due to factors such as strong hospital investment in radiology infrastructure, rising diagnostic testing demand, increasing chronic disease screening programs, and high procurement of advanced imaging technologies across tertiary hospitals. Healthcare authorities continue investing in CT scanners, MRI systems, and digital radiography platforms to improve diagnostic accuracy and early disease detection. Large government medical cities and specialized oncology centers require advanced imaging systems to support complex clinical procedures and multidisciplinary treatment programs.

By End User

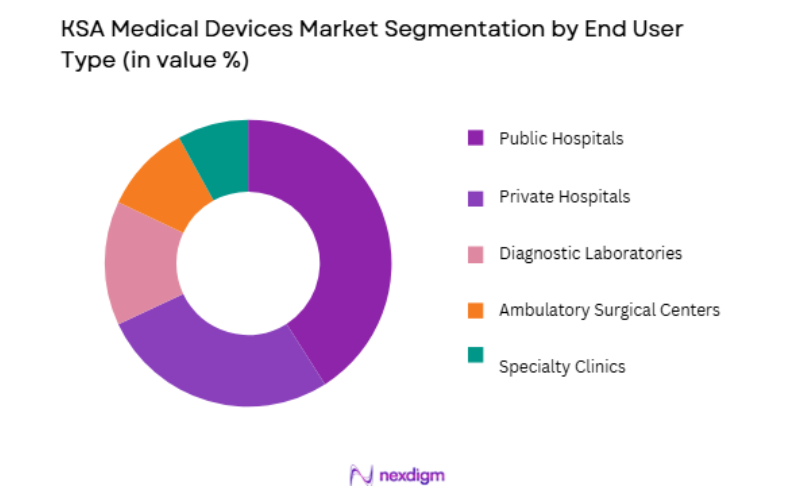

KSA Medical Devices market is segmented by end user into Public Hospitals, Private Hospitals, Diagnostic Laboratories, Ambulatory Surgical Centers, and Specialty Clinics. Recently, Public Hospitals has a dominant market share due to factors such as large government healthcare infrastructure, centralized procurement policies, and extensive expansion of national medical cities under the healthcare transformation program. Government hospitals represent the backbone of Saudi Arabia’s healthcare system and are responsible for providing advanced medical services across the population. Large procurement contracts for diagnostic equipment, surgical technologies, and patient monitoring systems are executed through government healthcare authorities. Public hospitals also operate specialized treatment centers including cardiac institutes, oncology centers, and transplant facilities, which require high-value medical devices.

Competitive Landscape

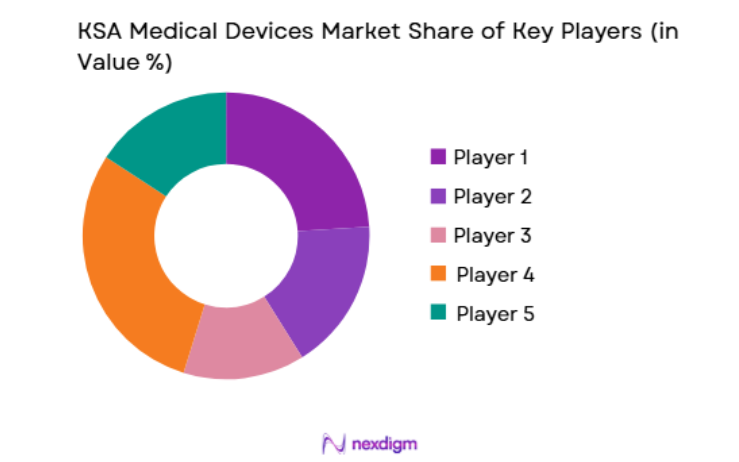

The KSA medical devices market is moderately consolidated with a strong presence of multinational manufacturers that dominate high-technology medical equipment supply across imaging, diagnostics, and surgical technologies. Global companies maintain partnerships with local distributors and healthcare authorities to strengthen regulatory compliance and procurement access. Large international manufacturers benefit from strong brand recognition, extensive product portfolios, and long-term hospital supply agreements. Local distributors and regional healthcare technology firms support equipment installation, maintenance, and technical service operations, creating an integrated ecosystem supporting advanced medical device adoption across Saudi healthcare facilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Local Distribution Partnerships |

| Siemens Healthineers | 1847 | Germany | ~ | ~ | ~ | ~ | ~ |

| GE Healthcare | 1892 | United States | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Netherlands | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | United States | ~ | ~ | ~ | ~ | ~ |

| Abbott Laboratories | 1888 | United States | ~ | ~ | ~ | ~ | ~ |

KSA Medical Devices Market Analysis

Growth Drivers

Expansion of Vision 2030 Healthcare Infrastructure Investment

Saudi Arabia’s national healthcare transformation program is significantly expanding hospital capacity, specialized treatment centers, and digital health infrastructure across the country. Government investments in large medical cities, tertiary hospitals, and regional healthcare clusters are increasing procurement of diagnostic imaging systems, surgical equipment, laboratory analyzers, and patient monitoring technologies. Public healthcare authorities are upgrading hospitals with advanced medical technologies to improve treatment quality, clinical efficiency, and healthcare accessibility for a growing population. Major projects such as King Salman Medical City and other regional hospital developments require large volumes of advanced medical devices to support modern healthcare delivery. These investments increase demand for diagnostic imaging equipment, minimally invasive surgical systems, and intensive care monitoring technologies required for complex treatment procedures. Private healthcare providers are also expanding hospital infrastructure in response to healthcare privatization initiatives and rising patient demand for specialized medical services. As new hospitals and specialty clinics become operational across major Saudi cities, procurement requirements for advanced medical devices increase significantly. Healthcare modernization programs also emphasize digital hospital environments, requiring integrated medical technologies and smart clinical systems.

Rising Prevalence of Chronic Diseases and Advanced Diagnostic Demand

Increasing incidence of chronic diseases such as diabetes, cardiovascular disorders, cancer, and respiratory illnesses is driving significant demand for advanced diagnostic and monitoring technologies in Saudi Arabia. Chronic disease management requires continuous diagnostic testing, imaging procedures, and clinical monitoring, creating strong demand for medical devices across hospitals and diagnostic laboratories. Healthcare providers rely on advanced imaging technologies including MRI, CT scanners, and ultrasound systems to detect diseases at early stages and support effective treatment planning. Diagnostic laboratories also require automated in-vitro diagnostic equipment to process growing testing volumes associated with chronic disease screening programs. Rising lifestyle-related health conditions further increase the need for continuous patient monitoring systems used in intensive care units and specialized treatment centers. Oncology treatment programs also require sophisticated diagnostic technologies to support early cancer detection and personalized treatment approaches. Government healthcare initiatives promoting early disease detection and preventive healthcare further expand diagnostic testing volumes across hospitals and laboratories. As healthcare providers focus on improving treatment outcomes and reducing long-term healthcare costs, adoption of advanced medical devices continues to accelerate.

Market Challenges

Regulatory Approval Complexity and Device Registration Requirements

Medical device manufacturers entering the Saudi healthcare market must comply with stringent regulatory approval processes governed by the Saudi Food and Drug Authority. Device registration procedures require detailed technical documentation, clinical validation data, and compliance with international quality standards before products can be marketed within the country. These regulatory processes can extend product launch timelines and increase administrative costs for manufacturers seeking market entry. International medical device companies must also establish local authorized representatives to manage regulatory submissions and compliance requirements. Variations between regulatory frameworks across global markets can require additional documentation adjustments for Saudi approval. Regulatory audits, post-market surveillance requirements, and product certification renewals further increase operational complexity for device suppliers. Companies must maintain continuous compliance with evolving regulatory standards and healthcare procurement policies implemented by government authorities. Smaller manufacturers and emerging technology firms may face greater challenges navigating complex regulatory frameworks due to limited local regulatory expertise. Compliance costs associated with device certification and documentation also increase market entry barriers for new suppliers.

High Dependence on Imported Medical Device Technologies

Saudi Arabia relies heavily on imported medical devices due to limited domestic manufacturing capabilities in high-technology healthcare equipment. Advanced diagnostic imaging systems, surgical robotics, laboratory automation equipment, and critical care monitoring devices are primarily supplied by international manufacturers. This reliance on imports increases exposure to global supply chain disruptions, currency fluctuations, and international trade constraints affecting medical equipment availability. Logistics challenges and shipping delays can influence equipment delivery timelines for large hospital procurement projects. Healthcare providers must also rely on international suppliers for spare parts, technical maintenance services, and equipment upgrades. Import dependence can increase procurement costs for hospitals and healthcare authorities due to transportation expenses and distributor margins. Limited domestic manufacturing capacity also restricts local innovation and technology development within the medical device sector. Although Saudi Arabia is promoting healthcare localization initiatives, establishing advanced medical technology manufacturing capabilities requires significant investment and technical expertise.

Opportunities

Expansion of Local Medical Device Manufacturing and Healthcare Localization Initiatives

Saudi Arabia is actively promoting healthcare localization initiatives to strengthen domestic production of medical devices and reduce reliance on imported technologies. Government industrial development programs encourage international manufacturers to establish local production facilities through investment incentives and strategic partnerships with domestic companies. Industrial zones dedicated to medical technology manufacturing are emerging within national economic diversification initiatives. Local production of diagnostic equipment, consumables, and hospital devices can significantly improve supply chain resilience and reduce procurement costs for healthcare providers. Partnerships between international medical device manufacturers and Saudi industrial firms enable technology transfer and workforce skill development within the healthcare manufacturing sector. Domestic production also supports national objectives for job creation and industrial diversification under broader economic transformation strategies. Increasing local manufacturing capacity could enable Saudi Arabia to become a regional medical technology production hub serving Middle Eastern healthcare markets. Government procurement programs may prioritize locally manufactured devices, further strengthening demand for domestic production.

Adoption of Digital Health Technologies and Smart Hospital Systems

Rapid digital transformation across Saudi healthcare facilities is creating new opportunities for advanced medical device integration with digital health technologies. Hospitals are increasingly implementing smart hospital infrastructure that combines connected medical devices, artificial intelligence diagnostics, and digital health platforms to enhance clinical decision-making. Integration of medical devices with hospital information systems enables real-time monitoring, remote diagnostics, and improved patient management across healthcare facilities. Telemedicine expansion also increases demand for portable diagnostic equipment and remote patient monitoring devices capable of supporting virtual healthcare services. Artificial intelligence powered imaging analysis tools are improving diagnostic accuracy while reducing physician workload in radiology departments. Healthcare providers are investing in digital intensive care systems that combine monitoring devices with predictive analytics for critical patient care management. These digital health innovations require modern medical devices capable of connectivity and interoperability within integrated hospital technology ecosystems. As Saudi hospitals continue implementing advanced healthcare technology platforms, demand for digitally enabled medical devices is expected to expand significantly.

Future Outlook

The KSA medical devices market is expected to experience sustained growth over the next five years as healthcare infrastructure expansion and modernization programs continue across the country. Government healthcare transformation initiatives and hospital construction projects will increase demand for advanced diagnostic and surgical technologies. Digital health integration and smart hospital development will further accelerate adoption of connected medical devices. Growing private healthcare investment and rising demand for specialized treatment services are also expected to support long-term market expansion.

Major Players

- Siemens Healthineers

- GE Healthcare

- Philips Healthcare

- Medtronic

- Abbott Laboratories

- Boston Scientific

- Becton Dickinson

- Stryker Corporation

- Johnson & Johnson MedTech

- Canon Medical Systems

- Fujifilm Healthcare

- Mindray Medical International

- Zimmer Biomet

- Smith & Nephew

- Terumo Corporation

Key Target Audience

- Hospitals and healthcare providers

- Medical device manufacturers

- Diagnostic laboratory chains

- Healthcare infrastructure developers

- Pharmaceutical companies

- Healthcare technology companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying critical variables influencing the KSA medical devices market including healthcare infrastructure development, diagnostic demand, regulatory frameworks, and technology adoption trends. Industry databases, government healthcare statistics, and international trade data are reviewed to establish foundational parameters for the analysis.

Step 2: Market Analysis and Construction

Comprehensive analysis is conducted using healthcare expenditure data, device procurement records, and hospital infrastructure statistics to construct the market structure. Market segmentation is developed by evaluating device categories, healthcare facility usage patterns, and procurement distribution across Saudi healthcare institutions.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses are validated through consultations with healthcare technology specialists, medical device distributors, and regulatory experts familiar with the Saudi healthcare ecosystem. These discussions help refine market assumptions and confirm technology adoption trends across hospitals and diagnostic laboratories.

Step 4: Research Synthesis and Final Output

The final research output is generated through synthesis of primary insights, secondary research findings, and quantitative healthcare market indicators. The analysis integrates macroeconomic healthcare data, regulatory developments, and technology innovation trends to produce a comprehensive market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Increasing healthcare investments under Vision 2030 healthcare transformation plans

Rising demand for advanced diagnostic and treatment technologies

Expansion of private healthcare facilities and specialty medical centers - Market Challenges

High dependence on imported medical devices and technologies

Strict regulatory approval processes for medical device registration

High procurement and maintenance costs for advanced medical equipment - Market Opportunities

Development of local medical device manufacturing capabilities

Adoption of AI enabled diagnostic and robotic surgical systems

Expansion of home healthcare and remote monitoring devices - Trends

Integration of smart connected medical devices with digital health platforms

Growing adoption of minimally invasive surgical technologies - Government Regulations

Medical device registration and approval under Saudi Food and Drug Authority

Regulatory standards governing import and distribution of medical devices

Quality and safety compliance requirements for healthcare equipment - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Diagnostic Imaging Devices

Patient Monitoring Devices

Surgical and Operating Room Devices

In Vitro Diagnostic Devices

Therapeutic and Rehabilitation Devices - By Platform Type (In Value%)

Hospital Medical Device Systems

Diagnostic Center Equipment Platforms

Home Healthcare Medical Devices

Ambulatory Surgical Center Equipment

Mobile and Portable Medical Devices - By Fitment Type (In Value%)

New Medical Device Installations

Device Replacement and Upgrade Programs

Leased Medical Equipment Systems

Integrated Smart Medical Device Systems - By End User Segment (In Value%)

Public Hospitals and Government Healthcare Providers

Private Hospitals and Specialty Clinics

Diagnostic Laboratories and Imaging Centers

Home Healthcare Service Providers

- Market Share Analysis

- Cross Comparison Parameters (Device Technology Complexity, Regulatory Approval Status, Clinical Application Range, Equipment Pricing Structure, After Sales Service Support)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Siemens Healthineers

GE HealthCare

Philips Healthcare

Medtronic

Abbott Laboratories

Johnson and Johnson MedTech

Boston Scientific

Becton Dickinson

Stryker Corporation

Zimmer Biomet

Fujifilm Healthcare

Canon Medical Systems

Mindray Medical

Olympus Medical Systems

Terumo Corporation

- Government hospitals investing in advanced diagnostic and treatment equipment

- Private hospitals expanding specialty departments with modern medical devices

- Diagnostic laboratories adopting high precision diagnostic technologies

- Home healthcare providers deploying portable monitoring and therapeutic devices

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now