Download PDF

Download PDF Download PDF

Download PDFMarket Overview

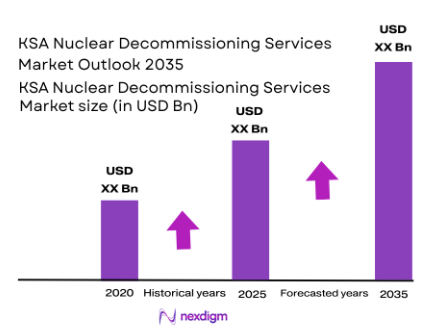

The KSA Nuclear Decommissioning Services market is driven by increasing investments in nuclear facility decommissioning, with growing demand for safe and environmentally responsible methods. The market size is significantly impacted by government-led nuclear decommissioning projects, particularly the decommissioning of older nuclear plants and the management of nuclear waste. In 2025, the market is estimated to reach USD ~billion, reflecting the importance of maintaining nuclear safety and the ongoing trend towards sustainable energy solutions.

Saudi Arabia, along with other GCC nations, dominates the market for nuclear decommissioning services due to large-scale nuclear energy infrastructure and long-term commitments to environmental sustainability. Saudi Arabia has made significant strides in nuclear energy initiatives, including the management of aging plants. The Kingdom’s strategic goals are aligned with decommissioning older facilities while maintaining high safety standards, leading to the dominance of the country in the sector.

Market Segmentation

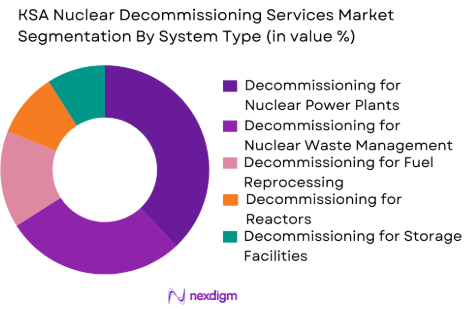

By System Type

The KSA Nuclear Decommissioning Services market is primarily segmented by system type, with the largest share held by decommissioning services for nuclear power plants. These services involve the systematic shutdown, dismantling, and safe disposal of nuclear facilities after their operational life. The dominance of this subsegment is driven by the large number of aging nuclear plants in the region that require decommissioning. As the industry moves towards renewable energy solutions, the demand for these services will continue to rise. The increasing need for managing complex nuclear waste and following rigorous safety standards also contributes to the market’s growth.

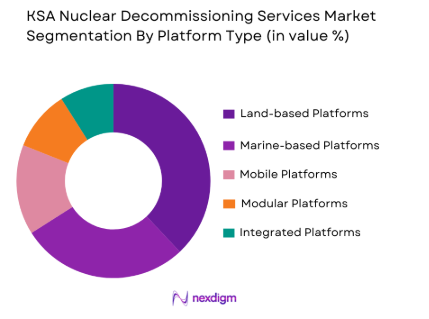

By Platform Type

The KSA Nuclear Decommissioning Services market is also segmented by platform type, with land-based platforms leading the market share. This dominance is attributed to the established infrastructure and logistical advantages of land-based platforms, which are ideal for the safe decommissioning of large facilities. The popularity of land-based systems is bolstered by the convenience they offer in managing complex waste streams and their ability to comply with regulatory frameworks. Marine-based platforms, though present, are less common due to the specialized requirements for maritime nuclear decommissioning.

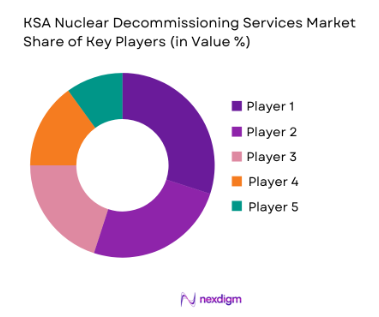

Competitive Landscape

The KSA Nuclear Decommissioning Services market is characterized by the presence of a few major players that dominate the sector due to their technological expertise, financial backing, and regulatory compliance. These companies are well-established in the nuclear industry, providing comprehensive decommissioning solutions that meet stringent safety standards. Major players such as Bechtel Corporation and Fluor Corporation lead the market, with their large-scale infrastructure projects, and are complemented by local firms that play a critical role in regional nuclear decommissioning efforts.

| Company Name | Establishment Year | Headquarters | Technological Capability | Financial Strength | Market Presence | Regulatory Compliance | Sustainability Practices | Service Portfolio | Innovation |

| Bechtel Corporation | 1898 | USA | Advanced Nuclear Tech | High | ~ | ~ | ~ | ~ | ~ |

| Fluor Corporation | 1949 | USA | Engineering & Design | High | ~ | ~ | ~ | ~ | ~ |

| Jacobs Engineering Group | 1947 | USA | Project Management | High | ~ | ~ | ~ | ~ | ~ |

| Westinghouse Electric Company | 1886 | USA | Nuclear Equipment & Services | High | ~ | ~ | ~ | ~ | ~ |

| Orano | 2017 | France | Waste Management Tech | High | ~ | ~ | ~ | ~ | ~ |

KSA Nuclear Decommissioning Services Market Analysis

Growth Drivers

Government Investments in Nuclear Energy Infrastructure

The Kingdom of Saudi Arabia’s Vision 2035 includes significant investments in diversifying energy sources, including nuclear power. As part of this vision, the government is focusing on developing nuclear energy plants, with some plants reaching their end of operational life. This results in an increased demand for nuclear decommissioning services. The government’s commitment to maintaining safety standards and ensuring the environmental sustainability of decommissioned plants is driving the growth of the nuclear decommissioning market. Furthermore, the need to adhere to international nuclear safety protocols enhances the demand for advanced decommissioning services, creating a steady flow of contracts for service providers. These government-driven initiatives in the nuclear sector, combined with increasing awareness of environmental issues, contribute to a strong growth trajectory for the market, creating long-term business opportunities in the nuclear decommissioning services sector.

Technological Advancements in Waste Management and Robotics

Technological advancements in waste management systems and robotics are transforming the nuclear decommissioning process, providing more efficient, cost-effective, and safer solutions for nuclear plant decommissioning. Innovations such as remote-controlled robotics for hazardous environments, automated waste sorting, and AI-driven monitoring systems are significantly improving the speed and accuracy of the decommissioning process. These advancements are helping to reduce human exposure to dangerous environments, ensuring a safer process and lowering labor costs. The development of more advanced, automated systems also helps in mitigating environmental risks associated with nuclear waste, thus enhancing the attractiveness of nuclear decommissioning services. As technology continues to evolve, it is expected that these innovations will play a key role in expanding the nuclear decommissioning market, enabling firms to offer increasingly sophisticated solutions while meeting regulatory and safety requirements.

Market Challenges

High Costs of Nuclear Decommissioning

One of the significant challenges facing the KSA Nuclear Decommissioning Services market is the high cost associated with the decommissioning process. Nuclear power plants are complex, with specialized equipment and materials that must be handled with extreme caution. The cost of dismantling, removing radioactive materials, and safely disposing of waste is substantial. Additionally, these costs often include the long-term monitoring of decommissioned sites to ensure they do not pose any environmental or health risks. As a result, nuclear decommissioning can be a significant financial burden for governments and private plant operators. In some cases, there may be insufficient funding allocated for the decommissioning process, which can result in delays or incomplete decommissioning projects. This financial challenge is a key obstacle for market growth, as cost-effective solutions are needed to make nuclear decommissioning more affordable and accessible.

Regulatory and Safety Compliance Complexities

Nuclear decommissioning is governed by stringent regulatory frameworks and safety standards that vary by country and jurisdiction. In Saudi Arabia, the regulatory environment for nuclear decommissioning is still evolving, and service providers must navigate these complex rules to ensure compliance. The challenge lies in ensuring that all decommissioning activities adhere to international standards while also aligning with local regulations. This includes managing radioactive waste, ensuring the protection of workers, and implementing environmental safeguards. The compliance requirements can be resource-intensive, with regular inspections and reports required from decommissioning companies to confirm adherence to regulatory standards. These regulatory complexities increase operational costs, create delays, and often require specialized knowledge, which can hinder the efficiency of decommissioning projects. The evolving nature of these regulations in Saudi Arabia makes it a challenging market for both domestic and international decommissioning service providers.

Opportunities

Public-Private Partnerships in Nuclear Decommissioning

Public-private partnerships (PPPs) present a significant opportunity for the nuclear decommissioning market in Saudi Arabia. Given the substantial costs and technical expertise required for nuclear decommissioning, government entities are increasingly turning to private sector companies to provide the necessary services. These partnerships enable the government to share the financial burden of decommissioning while also benefiting from the technical capabilities of private firms. By collaborating with private companies, the government can ensure the timely and efficient closure of nuclear plants while also driving innovation in the decommissioning process. The formation of PPPs also allows for risk-sharing and the pooling of resources, which can reduce costs and make the decommissioning process more economically viable. This model offers significant growth prospects for decommissioning service providers, particularly those with the expertise to handle complex nuclear facilities.

Growing Demand for Sustainable Energy Solutions

As global concerns over climate change and environmental sustainability continue to rise, there is increasing pressure on governments and industries to adopt cleaner energy practices. In Saudi Arabia, this growing emphasis on sustainability is creating a significant opportunity for the nuclear decommissioning services market. With nuclear power plants reaching the end of their life cycles, decommissioning them safely and sustainably is critical to the country’s environmental goals. Additionally, there is a growing push for the recycling and reprocessing of nuclear waste, which presents further opportunities for companies specializing in waste management and nuclear facility decommissioning. As the demand for sustainable energy solutions increases, there will be a heightened need for environmentally responsible nuclear decommissioning practices, offering substantial growth opportunities for firms that can offer innovative, eco-friendly, and efficient decommissioning services.

Future Outlook

Over the next decade, the KSA Nuclear Decommissioning Services market is poised for substantial growth. Government policies aimed at environmental sustainability, alongside global pressure to decommission aging nuclear facilities, will drive market demand. Technological innovations in nuclear waste management and robotics will further enhance efficiency and safety in decommissioning operations. The market is set to expand as Saudi Arabia continues to invest in its nuclear infrastructure and modernizes its approach to facility closure and waste management.

Major Players

- Bechtel Corporation

- Fluor Corporation

- Jacobs Engineering Group

- Westinghouse Electric Company

- Orano

- Aecom

- Sargent & Lundy

- Toshiba Energy Systems & Solutions Corporation

- GE Hitachi Nuclear Energy

- Areva Group

- Mitsubishi Heavy Industries

- Brookfield Renewable Partners

- KBR Inc.

- Babcock International Group

- CH2M Hill

Key Target Audience

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Nuclear Power Plant Operators

- Private Nuclear Facility Operators

- Decommissioning Service Providers

- Nuclear Waste Management Companies

- Environmental and Sustainability Consultants

- Energy Infrastructure Development Firms

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves identifying the key variables that influence the KSA Nuclear Decommissioning Services market, focusing on governmental policies, environmental considerations, and technological innovations. Secondary research, including a review of historical data and reports from regulatory bodies, forms the foundation of this step.

Step 2: Market Analysis and Construction

In this phase, we will conduct a detailed analysis of the KSA Nuclear Decommissioning Services market, focusing on historical trends and current market dynamics. This includes understanding the demand for decommissioning services, technological advancements, and the competitive landscape.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be tested through consultations with nuclear industry experts and government agencies. Interviews with stakeholders from decommissioning service providers, energy firms, and regulatory bodies will validate assumptions and provide insights into emerging trends.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing the data collected and refining the market models. This includes validating the market size, identifying future growth areas, and ensuring the accuracy of the forecasts.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Government Investments in Nuclear Decommissioning Projects

Technological Advancements in Waste Management and Recycling

Growing Demand for Sustainable Nuclear Energy Solutions - Challenges

High Initial Investment for Nuclear Decommissioning Projects

Complex Regulatory and Safety Compliance Issues

Limited Availability of Skilled Workforce - Opportunities

Emerging Markets for Advanced Decommissioning Technologies

Public-Private Partnerships for Cost-Effective Decommissioning

Advancements in Robotic and Automation Solutions for Decommissioning - Trends

Shift Towards Eco-friendly and Sustainable Decommissioning Practices

Increased Adoption of AI and Automation in Decommissioning Operations

Growing Demand for Comprehensive Lifecycle Services in Nuclear Energy

- By Market Value 2020-2025

- By Installed Units 2020-2025

- By Average System Price 2020-2025

- By System Complexity Tier 2020-2025

- By System Type (In Value%)

Decommissioning Services for Nuclear Reactors

Decommissioning Services for Nuclear Waste Management

Decommissioning Services for Nuclear Fuel Reprocessing

Decommissioning Services for Nuclear Power Plants

Decommissioning Services for Storage Facilities - By Platform Type (In Value%)

Land-based Nuclear Decommissioning Platforms

Marine-based Nuclear Decommissioning Platforms

Mobile Decommissioning Platforms

Modular Decommissioning Platforms

Integrated Decommissioning Platforms - By Fitment Type (In Value%)

On-site Decommissioning

Off-site Decommissioning

Partial Decommissioning

Full Facility Decommissioning

Decommissioning with Waste Recycling - By End User Segment (In Value%)

Government Nuclear Regulatory Bodies

Private Nuclear Facility Operators

Decommissioning Service Providers

Nuclear Power Plant Operators

Nuclear Waste Management Companies - By Procurement Channel (In Value%)

Direct Procurement from Decommissioning Service Providers

Public Tender Procurement

Private Procurement through Contractors

Government Procurement Programs

Procurement through Third-Party Vendors

- Market Share Analysis

- Cross Comparison Parameters (Market Penetration, Service Differentiation, Technological Innovation, Price Competitiveness, Regulatory Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Aspin Kemp & Associates

Bechtel Corporation

Fluor Corporation

Jacobs Engineering Group

Aecom

Westinghouse Electric Company

Orano

Cameco Corporation

Sargent & Lundy

Toshiba Energy Systems & Solutions Corporation

GE Hitachi Nuclear Energy

Areva Group

Mitsubishi Heavy Industries

Brookfield Renewable Partners

KBR Inc.

- Government bodies looking to secure sustainable decommissioning services

- Private sector operators focusing on cost-efficiency and technology

- Regulatory bodies ensuring compliance with environmental standards

- Service providers increasingly offering end-to-end solut

- Forecast Market Value 2026-2035

- Forecast Installed Units 2026-2035

- Price Forecast by System Tier 2026-2035

- Future Demand by Platform 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now