Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the KSA semiconductor infrastructure market is part of an overall semiconductor industry valued at approximately USD ~ billion according to credible industry research on the national semiconductor market size, reflecting demand for semiconductor components, manufacturing ecosystem establishment, and digital infrastructure investment within the Kingdom. Growth is driven by government Vision 2035 initiatives prioritizing technology diversification, investment funds targeting chip design and manufacturing, and rising demand from telecommunications, data centers, and smart infrastructure sectors that require robust semiconductor infrastructure.

Dominant regions within the KSA semiconductor infrastructure landscape include Riyadh and the Eastern Province, where strategic governmental and public investment fund–backed projects concentrate semiconductor fabrication facilities, design hubs, and supporting digital infrastructure. The Kingdom’s smart city initiatives, data center expansions, and partnerships with global technology firms further reinforce these urban centers as focal points due to existing technological ecosystems, international connectivity, and infrastructure capable of supporting advanced manufacturing, data processing, and semiconductor ecosystem growth.

Market Segmentation

By Product Type

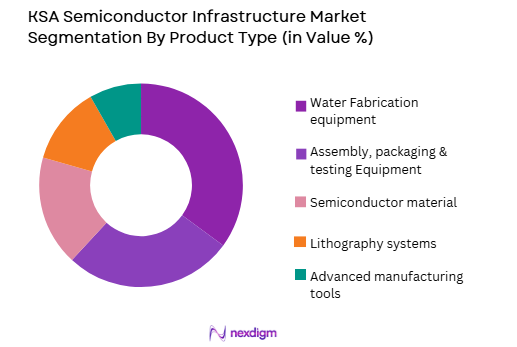

KSA Semiconductor Infrastructure market is segmented by product type into wafer fabrication equipment, assembly, packaging and testing, semiconductor materials, lithography systems, and advanced manufacturing tools. Recently, wafer fabrication equipment has a dominant market share due to factors such as high demand for localized chip production capacity, government incentives under Vision 2030 prioritizing onshore semiconductor manufacturing, strong infrastructure development in Riyadh and Eastern Province supporting cleanroom facilities, and international OEM presence supplying top-tier fabrication machinery. These drivers collectively position wafer fabrication equipment as foundational for establishing a domestic semiconductor value chain, reflecting procurement emphasis on front‑end production capability over downstream segments in the early stages of ecosystem development.

By End‑Use Infrastructure

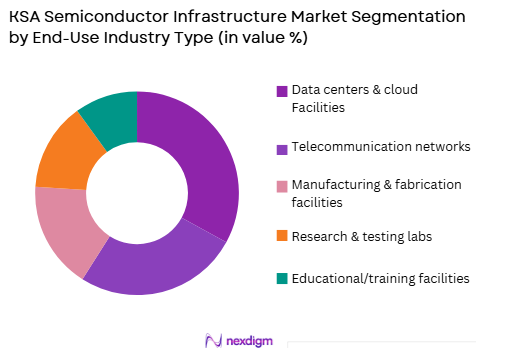

KSA Semiconductor Infrastructure market is segmented by end‑use infrastructure into data centers and cloud facilities, telecommunication networks, manufacturing and fabrication facilities, research and testing labs, and educational/training facilities. Recently, data centers and cloud facilities have a dominant market share due to factors such as rapid expansion of hyperscale and enterprise data centers in Riyadh and Dammam, Saudi partnerships with global technology firms deploying AI and cloud infrastructure, robust government digital transformation agendas requiring compute and storage capacity, and the strategic emphasis on AI and digital services requiring advanced semiconductor foundations. This concentration of investment supports data center infrastructure as the primary driver of semiconductor infrastructure demand within the national ecosystem.

Competitive Landscape

The KSA Semiconductor Infrastructure market is at an early but rapidly evolving stage characterized by strategic partnerships between domestic entities and global semiconductor technology firms, government‑backed investment funds, and ecosystem builders such as national hubs and manufacturing initiatives. Competition centers on securing fabrication capacity, advanced equipment, and design capabilities, with a mix of international OEMs and emerging local champions participating in infrastructure development to support Vision 2035 objectives of technology sovereignty and value‑added manufacturing.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Infrastructure Role |

| Alat | 2024 | Riyadh, Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Applied Materials | 1967 | USA | ~ | ~ | ~ | ~ | ~ |

| ASML | 1984 | Netherlands | ~ | ~ | ~ | ~ | ~ |

| KLA Corporation | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

| Lam Research | 1980 | USA | ~ | ~ | ~ | ~ | ~ |

KSA Semiconductor Infrastructure Market Analysis

Growth Drivers

Strategic Vision 2035 Technology Diversification Imperatives

Saudi Arabia’s semiconductor infrastructure market is significantly propelled by the strategic priorities defined under Vision 2035, which emphasize economic diversification through technology, manufacturing, and high‑value industrial development, catalyzing substantial public investment, policy support, and strategic partnerships aimed at building local semiconductor capabilities. The Kingdom’s deliberate focus on reducing dependency on oil revenue has translated into funding allocations and incentives for semiconductor infrastructure, including fabrication plant development, equipment procurement, and workforce training initiatives, creating an enabling environment for ecosystem growth. Vision 2035’s roadmap encourages collaboration with global semiconductor firms to transfer technology, establish cleanroom and fabrication capacity, and develop end‑to‑end semiconductor supply chains that address both domestic demand and regional export potential. Public investment vehicles, such as the Saudi Public Investment Fund, have launched multi‑billion‑dollar initiatives and strategic funds dedicated to attracting chip design, manufacturing, and assembly players, thereby directly stimulating infrastructure deployment. These initiatives signal long‑term government commitment to semiconductor industrialization, reinforcing investor confidence and reducing entry barriers for international technology partners aiming to establish local operations. Programmatic support also includes fiscal incentives, facilitation of regulatory approvals, and development of special economic zones tailored for advanced manufacturing. The combination of strategic vision, financial backing, and enabling policy environments forms a core structural driver of sustained market momentum.

Data Center and Cloud Infrastructure Expansion Demands

The semiconductor infrastructure market in Saudi Arabia is further accelerated by the rapid expansion of data centers and cloud computing facilities driven by increasing digital transformation, artificial intelligence applications, and enterprise IT modernization across public and private sectors, which necessitate robust semiconductor foundations, advanced compute hardware, and supporting fabrication and supply chain capabilities. As organizations increasingly adopt cloud solutions and AI services requiring significant computing power, the demand for cutting‑edge semiconductor components and infrastructure to support these deployments intensifies, prompting major investments in data center build‑outs, advanced server deployments, and memory and processing platforms. Saudi Arabia’s strategic positioning as a regional digital hub under Vision 2035 includes plans to host hyperscale data centers and cloud regions that serve domestic and international markets, thereby reinforcing demand for semiconductor materials, fabrication capacity, and associated infrastructure. Partnerships between local entities and global cloud service providers further amplify this demand, ensuring that infrastructure investments align with evolving technological requirements such as high‑density storage, AI accelerators, and low‑latency connectivity. The emphasis on digital services, smart city initiatives, and enterprise modernization compels semiconductor infrastructure enhancements that extend beyond traditional manufacturing into compute, storage, and networking ecosystems critical for next‑generation digital services.

Market Challenges

Global Semiconductor Supply Chain Concentration Risk Impacts Infrastructure Development

The KSA Semiconductor Infrastructure market encounters notable challenges due to the highly concentrated nature of the global semiconductor supply chain, where advanced fabrication, equipment, and materials are predominantly controlled by established players in East Asia and Western markets, constraining Saudi Arabia’s ability to independently source critical equipment, intellectual property, and talent necessary for building a comprehensive local infrastructure. The reliance on imported lithography systems, deposition and etch tools, and specialized materials subjects domestic infrastructure projects to geopolitical risks, export control regimes, and supply volatility that can delay fabrication plant development and increase project costs. Securing long‑lead items like extreme ultraviolet lithography (EUV) equipment requires navigating export regulations and competing demands from leading semiconductor hubs, necessitating intricate coordination between government, international partners, and OEMs. Additionally, the scarcity of indigenous suppliers for core semiconductor technologies means domestic firms must forge deep partnerships with global technology leaders to ensure consistent access to critical inputs, which can be complex and resource‑intensive. Training local engineers and technicians to operate and maintain sophisticated fabrication infrastructure also poses a barrier, requiring complementary investments in education and skills development that lag infrastructure deployment timelines. The cumulative effect of these supply chain dependencies challenges the speed and scalability with which Saudi Arabia can realize a fully sovereign semiconductor infrastructure.

High Capital Intensity and ROI Uncertainty for Semiconductor Infrastructure Projects

Another significant market challenge for semiconductor infrastructure development in Saudi Arabia relates to the immense capital expenditure required to build and operate fabrication facilities, cleanrooms, and supporting logistics, coupled with uncertainties regarding return on investment given the long gestation periods typical of semiconductor manufacturing projects. Construction of fabrication plants, procurement of advanced equipment, and development of qualified workforce pipelines demand substantial upfront financial resources, often necessitating multi‑year commitments before production yields revenue, which creates financial risk considerations for both public and private stakeholders. Uncertainties in global demand cycles, competitive pressures from established semiconductor hubs, and potential shifts in technology standards contribute to ROI ambiguity, making stakeholders cautious in committing to large‑scale infrastructure projects. The operational costs associated with maintaining ultra‑clean environments, energy requirements, and ongoing capital refresh for next‑generation equipment further complicate financial planning. Market entrants must balance strategic ambitions with pragmatic financial models that account for cyclical semiconductor demand, technology obsolescence risks, and competitive pricing pressures. These financial and economic considerations form substantive challenges to scaling semiconductor infrastructure projects.

Opportunities

Localized Semiconductor Manufacturing and Design Ecosystem Development

The KSA Semiconductor Infrastructure market presents substantial opportunity through localized semiconductor manufacturing and design ecosystem development, enabling Saudi Arabia to move beyond consumption toward value‑added production, intellectual property creation, and export‑oriented semiconductor solutions tailored to regional needs. By fostering local design centers, fabrication plants, and collaborative innovation hubs, the Kingdom can leverage its strategic investments to attract global technology firms seeking new manufacturing bases while nurturing domestic startups and engineering talent. Partnerships with established semiconductor companies provide knowledge transfer and integration of advanced manufacturing processes that enhance local capabilities. Domestic fabrication capacity reduces reliance on imports, improves supply chain resilience, and supports adjacent sectors such as automotive electronics, telecommunications, and AI hardware development. As the semiconductor value chain expands locally, opportunities arise for ancillary industries like materials production, testing services, and equipment maintenance. Government incentives that support R&D, workforce development, and infrastructure financing further entice investors and technology partners to participate in ecosystem building, amplifying the opportunity for Saudi Arabia to establish itself as a competitive regional semiconductor infrastructure hub.

Greenfield Advanced Technology Zones and Public‑Private Collaboration Models

Another key opportunity lies in developing greenfield advanced technology zones integrated with public‑private collaboration models that provide tailored environments for semiconductor infrastructure growth, including specialized utilities, tax incentives, streamlined regulatory processes, and access to research institutions. These zones can attract multinational semiconductor firms looking for strategic advantages such as lower energy costs, proximity to Middle East, African, and Asian markets, and government backing that mitigates entry risks. Public‑private partnerships facilitate shared investment burdens and align strategic objectives between government bodies and industry players, fostering innovation clusters that integrate design, fabrication, testing, and supply chain activities under unified development frameworks. Such collaboration enhances competitive positioning in the global semiconductor landscape and creates scalable platforms for future technological advancements, including AI accelerator manufacturing and next‑generation semiconductor materials research.

Future Outlook

The KSA Semiconductor Infrastructure market is poised for continued expansion as government‑led strategic initiatives, international partnerships, and digital transformation agendas stimulate substantial infrastructure investment. Expected growth trends include build‑out of fabrication facilities, enhancement of data center capabilities, and integration of advanced manufacturing technologies. Regulatory support, fiscal incentives, and Vision 2035 alignment will sustain demand for robust semiconductor ecosystems. Demand‑side factors such as AI, 5G networks, and smart city development will drive further infrastructure deployment across the Kingdom.

Major Players

- Alat

- Applied Materials

- ASML

- KLA Corporation

- Lam Research

- Samsung Foundry (partner)

- TSMC (partner initiative)

- Intel (infrastructure partnerships)

- Micron Technology

- Texas Instruments

- STMicroelectronics

- GlobalFoundries

- Synopsys

- Cadence Design Systems

Key Target Audience

- Semiconductor and infrastructure investors

- Technology OEMs and equipment suppliers

- Government and regulatory bodies

- Data center developers

- Telecommunication network operators

- AI and cloud service providers

- Public Investment Funds

- Manufacturing and fabrication facility planners

Research Methodology

Step 1: Identification of Key Variables

Key variables such as semiconductor infrastructure components, fabrication and packaging segments, end‑use infrastructure categories, government policies, and technology adoption drivers were identified and defined for market assessment. Supply chain dynamics, capital investment factors, and ecosystem development indicators were mapped to contextualize structural demand.

Step 2: Market Analysis and Construction

Market construction involved consolidation of credible industry research, national semiconductor market valuations, and infrastructure investment data. Segmentation was applied across product types and end‑use infrastructure categories to derive market structure and relative contributions.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses concerning infrastructure drivers, challenges related to supply chain and capital intensity, and opportunities tied to localization and collaboration were validated through synthesis of industry reports, expert commentary, and strategic national initiatives. Cross‑verification ensured alignment with observed ecosystem developments.

Step 4: Research Synthesis and Final Output

Validated insights were merged into a comprehensive analysis covering overview, segmentation, competitive landscape, drivers, challenges, opportunities, and future outlook. The final deliverable reflects measured assessment of the KSA semiconductor infrastructure market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National semiconductor localization and diversification strategy

Expansion of advanced electronics and digital economy sectors

Government investment in high technology manufacturing infrastructure - Market Challenges

High capital intensity and technology transfer complexity

Dependence on global semiconductor supply chain expertise

Workforce skill gap in semiconductor manufacturing - Market Opportunities

Development of regional semiconductor fabrication hubs

Partnerships with global semiconductor equipment leaders

Growth in compound and power semiconductor production - Trends

Shift toward advanced node and specialty semiconductor fabs

Integration of automation and smart fab technologies

Localization of semiconductor supply chain infrastructure - Government regulations

National industrial and semiconductor localization policies

Foreign investment and technology transfer regulations

Export control and semiconductor compliance frameworks - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Semiconductor Fabrication Facilities

Assembly and Packaging Facilities

Semiconductor Materials Infrastructure

Cleanroom and Contamination Control Systems

Semiconductor Equipment Support Infrastructure - By Platform Type (In Value%)

300mm Wafer Fabrication Platforms

200mm Wafer Fabrication Platforms

Advanced Packaging Platforms

Power and Analog Semiconductor Platforms

Compound Semiconductor Platforms - By Fitment Type (In Value%)

Greenfield Semiconductor Facilities

Brownfield Expansion Infrastructure

Modular Fab Infrastructure Systems

High Purity Utility Infrastructure

Automated Material Handling Infrastructure - By End User Segment (In Value%)

Integrated Device Manufacturers

Foundry Service Providers

Outsourced Semiconductor Assembly and Test Providers

Government Semiconductor Programs

Research and Development Facilities - By Procurement Channel (In Value%)

Direct EPC Contracts

Semiconductor Equipment OEM Partnerships

Engineering and Construction Integrators

Government Procurement Programs

Technology Licensing and Joint Ventures

- Market Share Analysis

- Cross Comparison Parameters (Fab Technology Node Capability, Wafer Size Platform Support, Cleanroom Class and Scale, Utility Infrastructure Integration, Automation and Material Handling Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Saudi Aramco Technologies

King Abdulaziz City for Science and Technology

Saudi Semiconductor Manufacturing Company

ACWA Power Industrial Solutions

Advanced Electronics Company

STC Industrial Investments

PIF Semiconductor Initiatives

GlobalFoundries

TSMC Infrastructure Partners

Intel Foundry Services

Samsung Semiconductor

ASE Technology Holding

Amkor Technology

Applied Materials

ASML

- Government programs driving semiconductor infrastructure investment

- IDMs establishing regional manufacturing presence

- Foundries targeting specialty semiconductor production

- R&D centers supporting technology localization

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now