Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Saudi Arabia’s semiconductor manufacturing ecosystem is expanding as the government prioritizes domestic electronics production, digital infrastructure, and advanced manufacturing capacity. Based on a recent historical assessment, the semiconductor manufacturing ecosystem connected to fabrication, packaging, and semiconductor supply chains in Saudi Arabia generated approximately USD ~ according to data published by the Saudi Ministry of Investment and global semiconductor trade statistics compiled by the Semiconductor Industry Association. Demand is driven by growth in telecommunications infrastructure, consumer electronics imports, automotive electronics integration, and large-scale data center investments supporting digital transformation.

Riyadh and NEOM technology development zones are emerging as dominant semiconductor investment centers due to strong government incentives, strategic industrial infrastructure, and proximity to national technology programs supporting electronics manufacturing. International technology partnerships with companies from the United States, Taiwan, South Korea, and Europe also support semiconductor ecosystem development. Industrial cities such as Jeddah and Dammam benefit from logistics infrastructure, port connectivity, and industrial clusters that support electronics assembly, semiconductor packaging, and integrated circuit testing operations across the country.

Market Segmentation

By Product Type

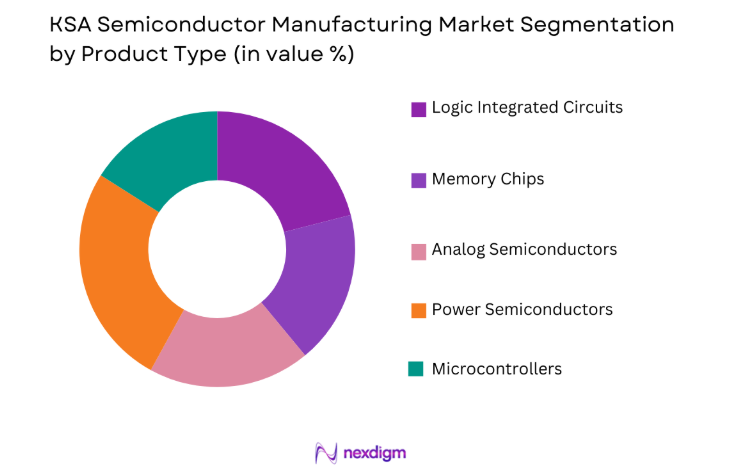

KSA Semiconductor Manufacturing market is segmented by product type into Logic Integrated Circuits, Memory Chips, Analog Semiconductors, Power Semiconductors, and Microcontrollers. Recently, Power Semiconductors has a dominant market share due to factors such as demand patterns, industrial electrification, renewable energy infrastructure development, and electric vehicle electronics adoption. Power semiconductors are essential components used in energy conversion, electric mobility systems, solar power systems, and smart grid technologies. Saudi Arabia’s renewable energy expansion programs and increasing investments in electric mobility infrastructure significantly increase demand for power management integrated circuits and high efficiency semiconductor devices used in power conversion and energy management technologies.

By Application Industry

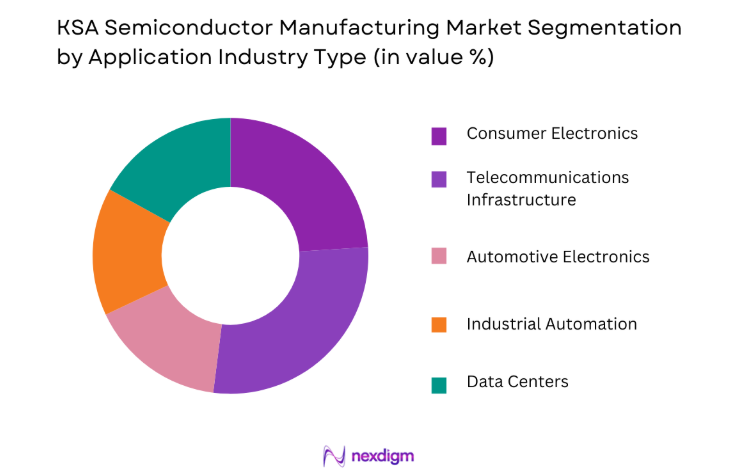

KSA Semiconductor Manufacturing market is segmented by application industry into Consumer Electronics, Telecommunications Infrastructure, Automotive Electronics, Industrial Automation, and Data Centers. Recently, Telecommunications Infrastructure has a dominant market share due to factors such as demand patterns, national digital infrastructure expansion, and advanced communication network deployments across the country. Semiconductor devices are essential for wireless communication equipment, base stations, network routers, and data transmission systems supporting high speed connectivity. Rapid expansion of 5G networks, smart city infrastructure programs, and digital connectivity initiatives across Saudi Arabia significantly increase demand for high performance communication semiconductor chips.

Competitive Landscape

The KSA Semiconductor Manufacturing market is characterized by strategic partnerships between global semiconductor companies and Saudi government backed industrial programs. The competitive environment remains moderately concentrated because semiconductor fabrication requires extremely high capital investment and advanced technological expertise. International semiconductor companies collaborate with Saudi technology investment funds and industrial development programs to establish manufacturing partnerships, packaging facilities, and semiconductor research initiatives supporting the national electronics manufacturing ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fabrication Capability |

| Intel Corporation | 1968 | United States | ~ | ~ | ~ | ~ | ~ |

| Taiwan Semiconductor Manufacturing Company | 1987 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| Samsung Electronics | 1969 | South Korea | ~ | ~ | ~ | ~ | ~ |

| GlobalFoundries | 2009 | United States | ~ | ~ | ~ | ~ | ~ |

| STMicroelectronics | 1987 | Switzerland | ~ | ~ | ~ | ~ | ~ |

KSA Semiconductor Manufacturing Market Analysis

Growth Drivers

Government Led Semiconductor Industrial Development Programs Supporting Domestic Electronics Production

Saudi Arabia’s national industrial transformation strategy significantly encourages investment in semiconductor manufacturing and advanced electronics production capabilities. Government economic diversification programs aim to reduce dependence on imported electronics and develop domestic technology manufacturing capacity supporting digital economy growth. Large sovereign investment funds support semiconductor partnerships with international technology companies capable of establishing wafer fabrication facilities packaging plants and integrated circuit design centers. Strategic technology programs also encourage semiconductor research collaboration between industrial companies universities and international semiconductor technology providers. National industrial zones provide tax incentives infrastructure support and financing mechanisms encouraging semiconductor manufacturing investment within the country. These policy frameworks stimulate semiconductor ecosystem development including chip design research materials supply chains and semiconductor equipment services. Semiconductor production capacity becomes strategically important because digital infrastructure telecommunications networks and advanced computing technologies depend heavily on semiconductor availability. National security considerations also encourage governments to establish domestic semiconductor capabilities capable of supporting defense electronics aerospace systems and cybersecurity technologies. These government supported programs collectively accelerate semiconductor manufacturing development across Saudi Arabia’s emerging advanced technology industrial ecosystem.

Rapid Expansion of Digital Infrastructure and Telecommunications Networks Increasing Semiconductor Demand

Saudi Arabia’s digital transformation initiatives significantly expand demand for semiconductor devices used in telecommunications networks data centers and high performance computing systems. Nationwide deployment of advanced mobile communication networks requires large volumes of semiconductor components including radio frequency chips signal processors network switching circuits and communication controllers. Expansion of fiber optic networks cloud computing infrastructure and hyperscale data centers further increases demand for advanced integrated circuits used in networking equipment storage systems and server processors. Smart city infrastructure programs also integrate large numbers of semiconductor powered devices including sensors monitoring systems surveillance technologies and intelligent transportation infrastructure. Telecommunications equipment manufacturers supplying base stations network routers and optical communication systems depend heavily on advanced semiconductor technologies supporting high speed data processing capabilities. Semiconductor components also support emerging technologies including artificial intelligence platforms machine learning systems and edge computing infrastructure deployed across digital networks. Increasing digital connectivity across industries such as healthcare finance transportation and education further accelerates demand for semiconductor components used in computing systems and digital devices. These expanding digital infrastructure investments therefore significantly drive semiconductor manufacturing development within Saudi Arabia’s technology ecosystem.

Market Challenges

Extremely High Capital Investment Requirements for Semiconductor Fabrication Facilities

Semiconductor manufacturing facilities require extremely sophisticated equipment advanced cleanroom infrastructure and precision manufacturing technologies which significantly increase capital investment requirements for market entry. Construction of advanced semiconductor fabrication plants requires billions of dollars in investment because fabrication equipment lithography systems wafer processing machines and materials handling technologies are highly specialized and expensive. Semiconductor manufacturing also requires continuous upgrades in fabrication technology as chip manufacturing nodes become smaller and more complex requiring additional investment in research development and equipment modernization. These high financial barriers limit the number of companies capable of establishing semiconductor fabrication operations within emerging markets. Saudi Arabia’s semiconductor ecosystem therefore depends heavily on partnerships with established international semiconductor companies capable of providing technical expertise manufacturing technology and operational experience. Development of supporting supply chains including semiconductor materials equipment maintenance services and advanced engineering expertise also requires significant long term investment commitments. Skilled workforce development becomes another challenge because semiconductor manufacturing requires highly specialized engineers technicians and researchers trained in microelectronics manufacturing processes. These financial and technological barriers slow the speed at which domestic semiconductor fabrication capacity can expand within Saudi Arabia.

Limited Domestic Semiconductor Supply Chain and Skilled Workforce Availability

Semiconductor manufacturing ecosystems require extensive supply chains including semiconductor materials chemicals manufacturing equipment maintenance services design software and specialized engineering expertise. Saudi Arabia’s semiconductor industry remains in an early development phase where many supporting supply chain components must still be imported from international suppliers. Semiconductor fabrication processes require extremely specialized materials such as high purity silicon wafers advanced photoresists chemical deposition materials and precision manufacturing equipment that are typically produced by established global suppliers. Limited domestic supply chain capacity increases operational costs and supply chain risks for semiconductor manufacturing operations within the country. Skilled workforce availability also presents a challenge because semiconductor manufacturing requires engineers trained in microelectronics process engineering materials science nanotechnology and semiconductor device design. Developing specialized educational programs and technical training institutions capable of producing highly skilled semiconductor engineers takes significant time and investment. Companies entering the Saudi semiconductor manufacturing sector therefore often rely on international talent and technology partnerships to support manufacturing operations. Strengthening domestic supply chains and workforce capabilities remains essential for long term semiconductor industry growth within the national technology ecosystem.

Opportunities

Development of Semiconductor Manufacturing Clusters within Emerging Technology Cities

Saudi Arabia’s large scale technology development zones such as NEOM and advanced industrial cities create strong opportunities for semiconductor manufacturing cluster development. Technology clusters encourage collaboration between semiconductor manufacturers electronics companies research institutions and technology startups capable of creating integrated semiconductor innovation ecosystems. Concentration of semiconductor companies within specialized industrial zones allows companies to share infrastructure research facilities testing laboratories and advanced manufacturing equipment. Semiconductor cluster development also improves supply chain efficiency because semiconductor materials suppliers equipment manufacturers and logistics providers can operate within the same industrial ecosystem. These clusters encourage innovation by enabling collaboration between chip design companies fabrication facilities and electronics manufacturers developing new semiconductor applications. Government supported research funding programs and technology incubators further encourage semiconductor innovation across these emerging technology zones. Semiconductor manufacturing clusters also attract international technology investment because global semiconductor companies benefit from government incentives advanced infrastructure and strategic geographic access to global technology markets. These technology cities therefore provide a strategic opportunity for Saudi Arabia to develop competitive semiconductor manufacturing ecosystems supporting regional electronics manufacturing industries.

Increasing Regional Demand for Semiconductor Components Across Middle Eastern Technology Markets

Rapid digitalization across Middle Eastern economies significantly increases demand for semiconductor devices used in telecommunications infrastructure consumer electronics automotive electronics and industrial automation systems. Regional governments invest heavily in digital infrastructure smart city programs artificial intelligence technologies and advanced computing platforms which require large quantities of semiconductor components. Saudi Arabia’s strategic geographic position between Europe Asia and Africa provides an opportunity to develop semiconductor manufacturing capacity capable of supplying semiconductor devices to regional technology markets. Local semiconductor manufacturing facilities could support electronics production across Gulf Cooperation Council countries where demand for digital devices communication infrastructure and industrial automation technologies continues expanding rapidly. Regional semiconductor supply capabilities reduce dependency on imported semiconductor components and improve supply chain resilience for technology industries across the Middle East. Semiconductor manufacturing investment within Saudi Arabia could therefore position the country as a strategic semiconductor supply hub supporting regional electronics manufacturing and digital infrastructure development across emerging technology markets.

Future Outlook

The KSA semiconductor manufacturing market is expected to experience sustained growth as the country continues implementing industrial diversification strategies and digital infrastructure development programs. Increasing demand for advanced electronics, telecommunications infrastructure, and artificial intelligence technologies will significantly expand semiconductor consumption across multiple industries. Government supported technology investment programs and international semiconductor partnerships will accelerate ecosystem development. Expanding smart city initiatives, data center investments, and renewable energy technologies will further strengthen semiconductor demand across the country.

Major Players

- Intel Corporation

- Taiwan Semiconductor Manufacturing Company

- Samsung Electronics

- GlobalFoundries

- STMicroelectronics

- Qualcomm Technologies

- Texas Instruments

- Micron Technology

- Infineon Technologies

- NXP Semiconductors

- Broadcom Inc.

- Analog Devices

- SK Hynix

- Renesas Electronics

- ASE Technology Holding

Key Target Audience

- Semiconductor Manufacturing Companies

- Consumer Electronics Manufacturers

- Telecommunications Infrastructure Companies

- Automotive Electronics Manufacturers

- Industrial Automation Equipment Manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the KSA Semiconductor Manufacturing Market were identified through analysis of semiconductor trade statistics, electronics manufacturing demand, digital infrastructure expansion, and national industrial development programs.

Step 2: Market Analysis and Construction

Market size estimation was constructed using semiconductor supply chain data, electronics production statistics, and technology investment reports combined with regional semiconductor consumption patterns.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including semiconductor engineers, electronics manufacturers, and technology investment specialists validated the market assumptions through structured consultations and technical analysis.

Step 4: Research Synthesis and Final Output

All validated insights were integrated into a structured analytical framework combining industry data, economic indicators, and technology investment patterns to produce the final market report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government Technology Diversification Programs Supporting Semiconductor Industry Development

Expansion of Data Center and Digital Infrastructure Across Saudi Arabia

Strategic Investments in Electronics Manufacturing and Advanced Technology Ecosystems - Market Challenges

High Capital Requirements for Semiconductor Fabrication Facilities

Limited Domestic Semiconductor Engineering Talent and Specialized Workforce

Dependence on Imported Semiconductor Equipment and Advanced Materials - Market Opportunities

Development of Regional Semiconductor Packaging and Testing Hubs

Rising Demand for Semiconductor Chips Supporting Artificial Intelligence and Cloud Infrastructure

Strategic Partnerships with Global Semiconductor Foundries and Technology Companies - Trends

Increasing Focus on Advanced Semiconductor Packaging Technologies

Growing Demand for High Performance Chips Supporting Data Center Infrastructure - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Semiconductor Wafer Fabrication Systems

Semiconductor Assembly and Packaging Systems

Semiconductor Testing Systems

Semiconductor Manufacturing Equipment

Semiconductor Materials and Specialty Chemicals - By Platform Type (In Value%)

Consumer Electronics Manufacturing

Automotive Electronics Manufacturing

Telecommunications Infrastructure Manufacturing

Industrial Electronics Manufacturing - By Fitment Type (In Value%)

Front End Semiconductor Fabrication

Back End Assembly and Packaging

Integrated Semiconductor Manufacturing Facilities

Outsourced Semiconductor Manufacturing Services - By End User Segment (In Value%)

Electronics and Consumer Device Manufacturers

Telecommunications Infrastructure Providers

Automotive and Industrial Electronics Manufacturers

- Market Share Analysis

- Cross Comparison Parameters (Technology Node Capability, Fabrication Capacity, Packaging Technology, Equipment Integration, Supply Chain Partnerships, Pricing Structure, Innovation Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Intel Corporation

Taiwan Semiconductor Manufacturing Company

Samsung Electronics

GlobalFoundries

United Microelectronics Corporation

STMicroelectronics

Infineon Technologies

Texas Instruments

ASE Technology Holding

Amkor Technology

Applied Materials

ASML Holding

KLA Corporation

Lam Research

Siltronic AG

- Data Center Operators Increasing Demand for High Performance Semiconductor Chips

- Telecommunications Companies Expanding Semiconductor Requirements for 5G Infrastructure

- Consumer Electronics Manufacturers Driving Integrated Circuit Demand

- Automotive Technology Firms Requiring Semiconductor Components for Electric Vehicle Systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now