Download PDF

Download PDF Download PDF

Download PDFMarket Overview

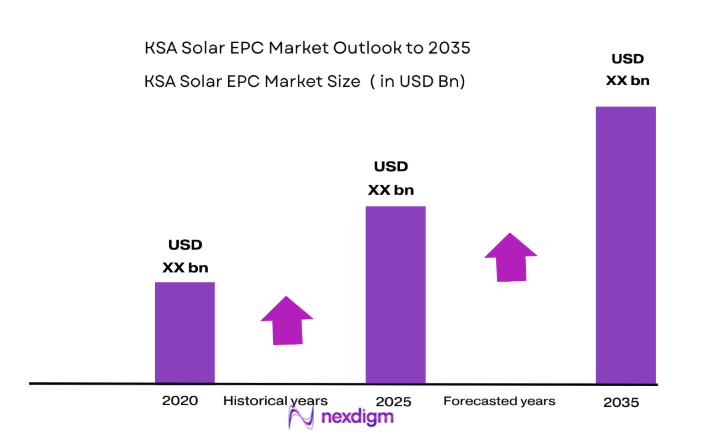

The Saudi Arabian solar EPC market is experiencing rapid expansion, driven by significant investments in renewable energy infrastructure. Based on a recent historical assessment, the market size for solar EPC projects is valued at approximately USD ~ billion. This growth is attributed to the government’s Vision 2030 initiative, which aims to diversify the energy mix and reduce dependence on oil by investing heavily in renewable sources. A key driver is the nation’s commitment to developing 50% of its energy from renewables, primarily through large-scale solar projects.

Saudi Arabia is witnessing dominance in major cities such as Riyadh, Jeddah, and Al Khobar, where the concentration of solar infrastructure projects is high. The government’s proactive policy measures, including incentives for developers and simplified permitting processes, are fostering rapid expansion. Furthermore, the country’s strategic location offers ideal conditions for solar energy generation, with vast desert areas providing ample space for utility-scale solar farms. The overall market is poised to grow as more regional and international players enter the scene, capitalizing on favorable market conditions.

Market Segmentation

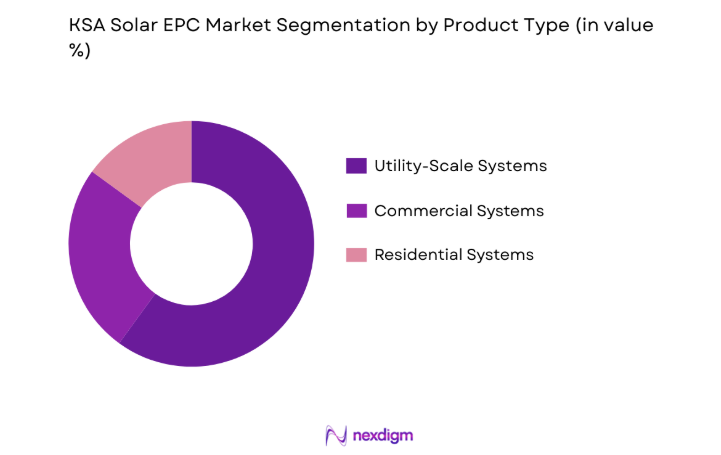

By Product Type:

The Saudi Arabian solar EPC market is segmented by product type into utility-scale, commercial, and residential solar systems. Recently, utility-scale solar projects have captured a dominant market share due to the vast investments made in large solar farms as part of the national renewable energy targets. These projects benefit from high levels of government support, favorable climatic conditions, and the demand for significant energy generation to power cities and industries. Utility-scale solar has seen extensive growth due to its ability to deliver large amounts of energy at competitive costs, attracting both local and international investment.

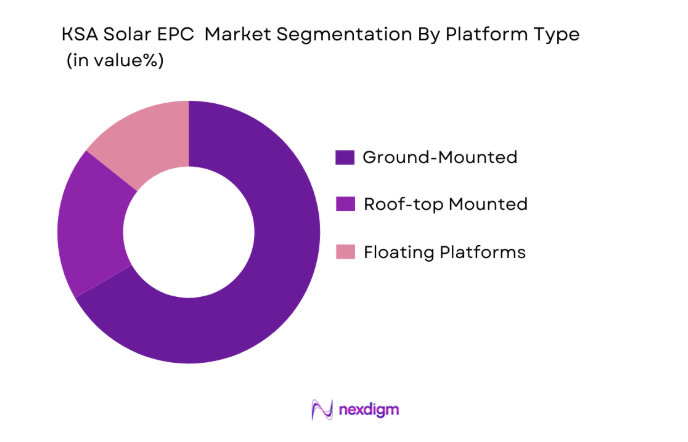

By Platform Type:

The Saudi Arabian solar EPC market is segmented by platform type into ground-mounted, roof-top mounted, and floating solar platforms. The ground-mounted platform is the dominant sub-segment due to its widespread use in large-scale solar projects across vast desert areas. These systems allow for easy deployment and maintenance, benefiting from optimal sunlight exposure in desert regions. Additionally, government incentives for large-scale solar farms make ground-mounted systems highly attractive, contributing to their leading market share.

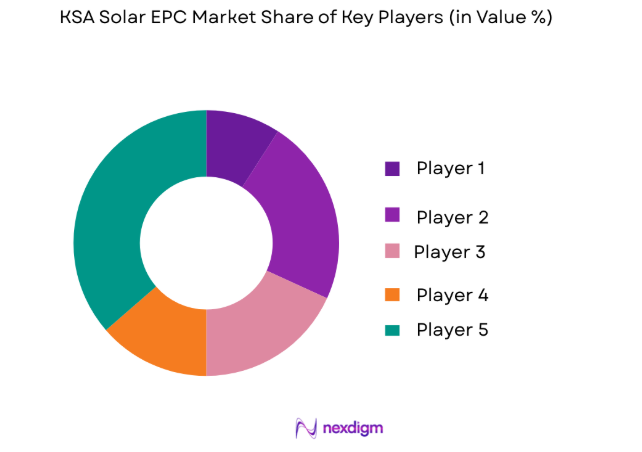

Competitive Landscape

The competitive landscape of Saudi Arabia’s solar EPC market is characterized by a mix of international and local players. Major players have been consolidating their positions by acquiring smaller firms and forming strategic partnerships to secure large-scale projects. The entry of international firms has brought advanced technology and financing solutions, further accelerating market growth. These companies are capitalizing on the government’s favorable policies and large-scale infrastructure projects aimed at meeting the 2030 renewable energy targets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| First Solar | 1999 | USA | ~ | ~ | ~` | ~ | ~ |

| JinkoSolar | 2006 | China | ~ | ~ | ~ | ~ | ~ |

| ACWA Power | 2004 | Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Saudi Aramco | 1933 | Saudi Arabia | ~ | ~ | ~ | ~ | ~ |

| Enel Green Power | 2008 | Italy | ~ | ~ | ~ | ~ | ~ |

KSA Solar EPC Market Analysis

Growth Drivers

Government Initiatives and Investments:

The Saudi Arabian government’s Vision 2030 has been a key growth driver in the solar EPC market. With its goal to diversify the economy and reduce dependence on fossil fuels, the government has committed to generating 50% of its electricity from renewable sources by 2030. This ambitious target has led to the introduction of various initiatives, such as subsidies for solar energy systems, tax incentives for developers, and simplified permitting processes. These efforts have attracted international solar companies and investors, propelling market growth. Furthermore, Saudi Arabia’s abundant natural resources and ideal climatic conditions for solar energy generation contribute to making large-scale solar projects economically viable, with substantial returns on investment. This combination of favorable government policies and natural advantages makes the country a prime destination for solar energy investments, further supporting the expansion of the solar EPC market.

Technological Advancements:

Another significant growth driver for Saudi Arabia’s solar EPC market is the continuous advancement in solar technology. Innovations in photovoltaic (PV) panel efficiency, energy storage, and solar tracking systems have played a crucial role in driving down the cost of solar installations, making solar energy increasingly competitive with traditional energy sources. Furthermore, the integration of AI and smart grids with solar power systems has allowed for better energy management, leading to improved grid stability and optimized power distribution. These technological improvements enhance the performance and cost-effectiveness of solar projects, encouraging both government and private sector investments. The increasing interest in hybrid solar systems, which combine solar power with energy storage, is further boosting the market. This trend towards technological innovation ensures the long-term growth and sustainability of the solar EPC market in Saudi Arabia.

Market Challenges

High Initial Capital Investment:

One of the main challenges facing the solar EPC market in Saudi Arabia is the high initial capital required for large-scale solar projects. Despite the long-term savings and environmental benefits, the high upfront costs can be a significant barrier for investors, particularly for smaller firms or emerging businesses looking to enter the market. This challenge is further compounded by the complex financial structures involved in securing funding for such large-scale projects. Although the government provides incentives and subsidies, the initial cost burden remains a key challenge for developers and stakeholders. Additionally, the long payback period for large solar installations can deter private sector investments, particularly in uncertain economic conditions. As a result, addressing the financial barriers to entry remains critical for sustained growth in the Saudi solar EPC market.

Grid Integration and Infrastructure Limitations:

While Saudi Arabia has made significant strides in developing solar infrastructure, the integration of solar energy into the existing grid remains a major challenge. The variability and intermittency of solar power generation, coupled with the need for grid modernization, can lead to inefficiencies in energy distribution and grid instability. This challenge is particularly critical as solar energy capacity continues to grow, and the need for a reliable, smart grid becomes more urgent. The lack of sufficient grid infrastructure in certain remote areas further complicates the situation, as it limits the ability to efficiently distribute solar-generated power to high-demand regions. To overcome this challenge, substantial investments in grid expansion, storage systems, and smart grid technologies are required. Addressing these infrastructure limitations is crucial for ensuring the smooth integration of solar energy into Saudi Arabia’s broader energy landscape.

Opportunities

Hybrid Solar Systems and Energy Storage:

One of the most promising opportunities in the Saudi Arabian solar EPC market is the growing demand for hybrid solar systems that combine photovoltaic (PV) power generation with energy storage solutions. These systems allow for the storage of excess solar power generated during the day, ensuring a constant and reliable power supply even during non-sunny hours. As Saudi Arabia moves towards a more sustainable energy future, the integration of solar energy with advanced storage technologies will become increasingly important. This trend is expected to drive significant demand for hybrid systems, particularly in commercial and industrial applications. The government’s incentives for solar-plus-storage projects, coupled with the declining cost of storage technologies, creates a favorable environment for these solutions to thrive. Additionally, the demand for off-grid solar solutions in remote and rural areas presents a significant market opportunity for hybrid solar systems with storage capabilities.

Solar Energy for Water Desalination:

Another significant opportunity for the Saudi solar EPC market lies in the integration of solar power with water desalination systems. Saudi Arabia, being one of the largest producers of desalinated water, has a strong demand for energy-efficient and sustainable solutions for water production. The integration of solar energy into desalination processes can help reduce the high energy costs associated with traditional desalination methods, which are primarily powered by fossil fuels. Solar-powered desalination offers a cleaner and more cost-effective alternative, aligning with the country’s renewable energy goals. Given the urgent need for water security in the region, the government is likely to increase its investments in solar desalination projects, creating substantial market opportunities for solar EPC companies. This integration not only supports sustainable water production but also contributes to the broader environmental objectives of Saudi Arabia’s Vision 2030 initiative.

Future Outlook

Over the next five years, the Saudi Arabian solar EPC market is poised for significant growth, driven by continued government support for renewable energy projects. Technological advancements in solar energy generation and storage, along with expanding infrastructure, will further enhance the competitiveness of solar power. The market will continue to benefit from increased private sector participation and international investments, with a growing focus on hybrid solar systems and energy storage solutions. The government’s ambitious renewable energy targets, combined with favorable regulations, will further propel the market, ensuring its role in diversifying the energy mix.

Major Players

- First Solar

- JinkoSolar

- ACWA Power

- Saudi Aramco

- Enel Green Power

- Trina Solar

- SunPower Corporation

- Canadian Solar

- Hanwha Q CELLS

- Meyer Burger Technology

- Risen Energy

- Siemens Gamesa

- Vestas

- GE Renewable Energy

- ABB

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Energy developers

- Solar equipment manufacturers

- EPC contractors

- Renewable energy consultants

- Utility companies

- Large commercial and industrial solar users

Research Methodology

Step 1: Identification of Key Variables

Identification of market drivers, trends, challenges, and growth factors based on industry reports, surveys, and expert consultations.

Step 2: Market Analysis and Construction

Analysis of market data, segmentation, competitive landscape, and future projections to build a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Validation of market assumptions and growth projections through consultations with industry experts, stakeholders, and government bodies.

Step 4: Research Synthesis and Final Output

Compilation of research findings into a structured market report, ensuring accurate and actionable insights for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government Initiatives for Renewable Energy

Technological Advancements in Solar Technology

Increase in Private Sector Investment - Market Challenges

High Initial Investment Costs

Land Acquisition and Permitting Issues

Grid Integration Challenges - Market Opportunities

Growth in Residential Solar Installations

Increasing Demand for Hybrid Systems

Expansion of Solar Farms in Rural Areas - Trends

Rise in Solar Energy Storage Solutions

Integration of Smart Solar Technologies

Adoption of Solar + Storage Systems - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Utility-Scale Solar Projects

Commercial Solar Installations

Residential Solar Installations

Hybrid Solar Systems

Off-grid Solar Solutions - By Platform Type (In Value%)

Ground-mounted Systems

Roof-top Mounted Systems

Floating Solar Systems

Integrated Solar Platforms

Hybrid Platforms - By Fitment Type (In Value%)

On-site Solar Solutions

Off-site Solar Solutions

Modular Solar Installations

Portable Solar Solutions

Hybrid Fitments - By EndUser Segment (In Value%)

Government Sector

Commercial Sector

Industrial Sector

Residential Sector

- Market Share Analysis

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

First Solar

JinkoSolar

Enel Green Power

Saudi Aramco

ACWA Power

Abengoa Solar

Meyer Burger Technology

Risen Energy

Canadian Solar

Hanwha Q CELLS

SunPower Corporation

Trina Solar

Sungrow Power Supply

Larsen & Toubro

Tata Power Solar Systems

- Government’s Role in Solar Initiatives

- Private Sector’s Growing Demand for Solar

- Residential Sector Adoption Trends

- Agricultural Use of Solar for Irrigation

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now