Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Saudi Arabia’s telemedicine sector has expanded rapidly as digital healthcare services become integral to improving healthcare accessibility and clinical efficiency across the country. Based on a recent historical assessment, the KSA telemedicine market was valued at approximately USD ~ million according to digital health industry statistics and healthcare technology adoption data published by the Ministry of Health and international healthcare IT databases. Market expansion is driven by growing demand for remote consultations, expansion of digital healthcare infrastructure, and increasing integration of telehealth platforms across hospital networks.

Riyadh, Jeddah, and Dammam serve as the primary telemedicine adoption centers due to the presence of advanced hospital networks, digital health innovation initiatives, and strong telecommunications infrastructure. These metropolitan healthcare ecosystems host major hospitals, telehealth providers, and technology firms implementing remote consultation services and digital patient management systems. High smartphone penetration, widespread internet connectivity, and government-supported digital health programs further accelerate telemedicine adoption across these major urban healthcare hubs.

Market Segmentation

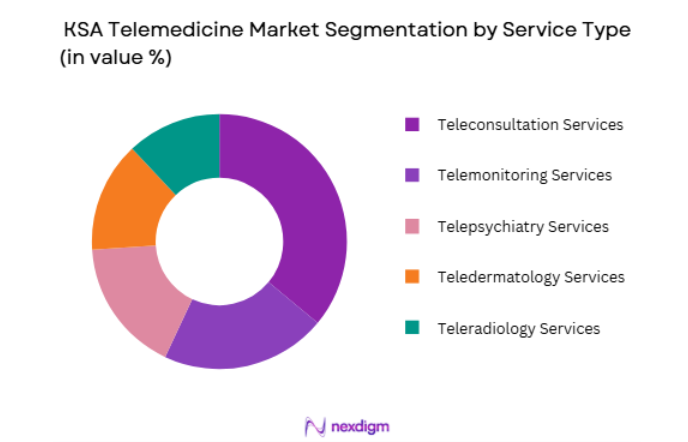

By Service Type

KSA Telemedicine market is segmented by service type into Teleconsultation Services, Telemonitoring Services, Telepsychiatry Services, Teledermatology Services, and Teleradiology Services. Recently, Teleconsultation Services has a dominant market share due to factors such as increasing patient demand for remote healthcare access, strong adoption among hospitals and private clinics, and expanding integration of video consultation platforms within digital healthcare ecosystems. Teleconsultation enables patients to connect with physicians remotely, reducing hospital visits and improving healthcare accessibility for individuals living in remote regions. Hospitals and telehealth providers increasingly deploy digital consultation platforms to manage outpatient appointments and follow-up consultations. Government healthcare programs promoting digital care delivery further strengthen teleconsultation adoption across healthcare institutions. In addition, private telehealth platforms offer mobile applications enabling patients to schedule virtual consultations, access prescriptions, and receive medical advice without visiting healthcare facilities.

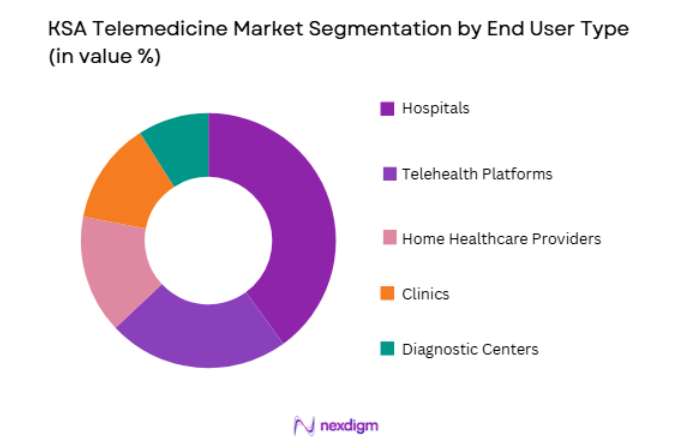

By End User

KSA Telemedicine market is segmented by end user into Hospitals, Telehealth Platforms, Home Healthcare Providers, Clinics, and Diagnostic Centers. Recently, Hospitals has a dominant market share due to factors such as strong hospital-led digital healthcare initiatives, integration of telehealth services within hospital information systems, and rising demand for remote patient consultation and monitoring services. Hospitals increasingly incorporate telemedicine platforms into clinical workflows to provide virtual consultations, post-treatment follow-ups, and remote patient monitoring services. Large tertiary hospitals also deploy telemedicine networks that allow specialists to provide consultations to regional healthcare centers and rural medical facilities. Telemedicine also supports hospitals in managing patient volumes more efficiently while improving access to specialized care. Integration of telemedicine platforms with electronic health records further strengthens hospital adoption by enabling physicians to access patient information during virtual consultations.

Competitive Landscape

The KSA telemedicine market includes international digital health technology companies, regional telehealth service providers, and local digital healthcare startups delivering remote medical consultation platforms. Global healthcare technology firms supply telehealth infrastructure and integrated hospital information systems, while regional companies focus on digital consultation platforms and mobile health services. Strategic partnerships between healthcare providers, telecommunications companies, and technology firms enable widespread deployment of telemedicine services across Saudi Arabia’s healthcare ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Telemedicine Platform Capability |

| Teladoc Health | 2002 | United States | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Netherlands | ~ | ~ | ~ | ~ | ~ |

| Vezeeta | 2012 | Egypt | ~ | ~ | ~ | ~ | ~ |

| Altibbi | 2011 | Jordan | ~ | ~ | ~ | ~ | ~ |

| Babylon Health | 2013 | United Kingdom | ~ | ~ | ~ | ~ | ~ |

KSA Telemedicine Market Analysis

Growth Drivers

Government Support for Digital Healthcare and Telemedicine Infrastructure Development

Saudi Arabia’s healthcare transformation strategy strongly promotes the integration of telemedicine services into national healthcare delivery systems to improve accessibility and healthcare efficiency. Government health authorities are investing in digital healthcare infrastructure that enables hospitals and healthcare providers to offer remote consultations and digital medical services to patients across the country. Telemedicine platforms are increasingly integrated into national healthcare networks to support specialist consultations, remote diagnosis, and patient monitoring services. These digital services are particularly valuable for improving healthcare access in remote regions where specialized medical expertise may not be readily available. Government initiatives also promote interoperability between telemedicine systems and hospital information platforms to enable seamless patient data exchange across healthcare institutions. Healthcare authorities are encouraging hospitals and clinics to implement telehealth services as part of broader digital healthcare transformation initiatives. As a result, telemedicine adoption is expanding across public hospitals, private healthcare providers, and specialized medical centers. National digital health strategies also promote investment in telecommunication infrastructure and digital platforms that support virtual healthcare delivery. This sustained government support continues to strengthen telemedicine adoption throughout the Saudi healthcare ecosystem.

Rising Demand for Remote Healthcare Services and Virtual Patient Consultations

Patients in Saudi Arabia increasingly prefer remote healthcare services that allow them to consult physicians without visiting healthcare facilities. Telemedicine platforms enable patients to schedule video consultations, receive digital prescriptions, and access medical advice through mobile applications and online healthcare portals. This digital healthcare model reduces travel time, shortens waiting periods, and improves access to healthcare services for individuals living outside major urban centers. Telemedicine also enables physicians to monitor chronic disease patients remotely using connected health devices and digital monitoring systems. Hospitals and clinics increasingly deploy teleconsultation platforms to manage outpatient appointments and follow-up consultations more efficiently. Digital healthcare services also allow specialists located in major medical centers to provide consultations to regional healthcare facilities. The growing adoption of smartphones and high-speed internet connectivity further supports telemedicine usage among patients and healthcare providers. Telemedicine services also improve healthcare system efficiency by reducing unnecessary hospital visits and optimizing physician workload management. As digital healthcare adoption continues expanding across Saudi Arabia, remote consultation services remain a major driver of telemedicine market growth.

Market Challenges

Regulatory Compliance and Licensing Requirements for Telemedicine Services

Telemedicine providers operating in Saudi Arabia must comply with strict regulatory frameworks governing digital healthcare services and patient data protection. Healthcare authorities require telemedicine platforms to meet specific licensing requirements before offering digital medical consultation services within the country. Compliance with national healthcare regulations ensures that telemedicine providers maintain high standards of patient safety, medical ethics, and service quality. However, regulatory approval procedures can sometimes delay market entry for new telemedicine platforms and digital health startups. Telemedicine providers must also ensure compliance with healthcare data privacy laws governing the storage and transmission of patient information across digital platforms. These regulatory requirements require continuous investment in legal compliance, cybersecurity systems, and secure digital infrastructure. Healthcare providers offering telemedicine services must also ensure that licensed physicians conduct remote consultations in accordance with national healthcare guidelines. Regulatory complexity can therefore create operational challenges for telemedicine companies seeking to expand digital healthcare services across the Saudi healthcare system.

Limited Digital Health Literacy and Patient Adoption Barriers in Certain Demographics

Although telemedicine adoption is increasing across Saudi Arabia, some patient groups still face barriers related to digital health literacy and familiarity with virtual healthcare technologies. Older patients and individuals living in rural areas may have limited experience using digital healthcare platforms and mobile health applications. These users may prefer traditional in-person medical consultations due to lack of familiarity with telemedicine technologies. Healthcare providers must therefore invest in patient education initiatives that demonstrate how telemedicine services can improve healthcare access and convenience. Telemedicine platforms must also design user-friendly interfaces that allow patients to easily schedule appointments and communicate with healthcare professionals. Digital literacy gaps can slow the adoption of telemedicine services in certain regions and demographic groups. Healthcare providers and government authorities must therefore implement awareness campaigns that promote digital healthcare services and encourage patient adoption. Addressing these digital literacy barriers remains essential for achieving widespread telemedicine adoption across the Saudi population.

Opportunities

Expansion of Artificial Intelligence Integration in Telemedicine Platforms

Artificial intelligence technologies offer significant opportunities for enhancing telemedicine platforms by improving diagnostic accuracy, patient triage, and healthcare workflow automation. AI-powered systems can analyze patient symptoms, medical histories, and diagnostic images to assist physicians during remote consultations. Telemedicine platforms can integrate AI-driven symptom assessment tools that guide patients through preliminary health evaluations before virtual consultations with physicians. These technologies help healthcare providers prioritize urgent medical cases and improve consultation efficiency. AI-based analytics platforms can also analyze patient health data collected through remote monitoring devices to identify potential health risks and alert physicians. Integration of AI technologies within telemedicine systems therefore enhances clinical decision-making and improves patient care outcomes. As healthcare providers increasingly adopt advanced digital health technologies, demand for telemedicine platforms capable of supporting AI-based analytics and diagnostic tools is expected to expand significantly.

Development of Integrated Remote Patient Monitoring and Home Healthcare Ecosystems

The growth of remote patient monitoring technologies creates major opportunities for telemedicine platforms to support continuous patient care outside traditional hospital environments. Remote monitoring systems allow healthcare providers to track patient health indicators such as heart rate, blood pressure, and glucose levels using connected medical devices. Telemedicine platforms can integrate these monitoring systems to enable physicians to remotely supervise patients suffering from chronic diseases and long-term health conditions. Home healthcare providers increasingly adopt telemedicine technologies to support elderly patient care and post-treatment recovery monitoring. These integrated digital healthcare ecosystems allow healthcare professionals to provide continuous medical supervision while reducing hospital admissions and healthcare costs. As remote healthcare services expand across Saudi Arabia, telemedicine providers that offer integrated monitoring solutions and home healthcare support platforms will benefit from significant market growth opportunities.

Future Outlook

The KSA telemedicine market is expected to expand rapidly over the next five years as digital healthcare services become increasingly integrated within national healthcare systems. Teleconsultation services, remote patient monitoring technologies, and AI-driven healthcare platforms will continue transforming healthcare delivery models. Government digital health initiatives and expanding telecommunications infrastructure will further support telemedicine adoption. Growing patient demand for convenient and accessible healthcare services is also expected to accelerate telehealth platform deployment across Saudi Arabia.

Major Players

- Teladoc Health

- Philips Healthcare

- Vezeeta

- Altibbi

- Babylon Health

- Siemens Healthineers

- GE Healthcare

- Cerner Corporation

- Epic Systems

- Oracle Health

- Qualcomm Life

- Amwell

- Medtronic Care Management

- MDLive

- Doctor On Demand

Key Target Audience

- Hospitals and healthcare providers

- Telemedicine platform developers

- Digital health technology companies

- Healthcare IT solution providers

- Home healthcare service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying critical variables influencing the KSA telemedicine market including telehealth adoption rates, digital healthcare infrastructure development, regulatory frameworks, and patient demand for remote healthcare services. Government healthcare reports, digital health industry databases, and telecommunication statistics are reviewed to establish baseline market indicators.

Step 2: Market Analysis and Construction

Market construction is conducted through analysis of telemedicine platform adoption across hospitals, clinics, and home healthcare providers. Telehealth service deployment, digital consultation volumes, and healthcare infrastructure data are used to build market segmentation and identify key growth patterns.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses are validated through discussions with healthcare technology experts, telemedicine platform developers, and hospital administrators operating within the Saudi healthcare ecosystem. These consultations help confirm adoption trends and identify key operational challenges within telemedicine services.

Step 4: Research Synthesis and Final Output

The final report integrates primary insights and secondary research findings to present a comprehensive market outlook. Data from healthcare institutions, digital health providers, and regulatory authorities is synthesized to produce an accurate representation of the KSA telemedicine market landscape.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government initiatives promoting telehealth adoption under Vision 2030 healthcare programs

Increasing demand for remote healthcare services across urban and rural regions

Rising smartphone and internet penetration enabling digital healthcare access - Market Challenges

Data privacy and cybersecurity concerns in telemedicine platforms

Integration challenges with existing hospital information systems

Limited awareness and adoption among certain patient groups - Market Opportunities

Expansion of teleconsultation services for remote and underserved populations

Integration of AI based diagnostic support in telemedicine platforms

Partnerships between hospitals and digital health technology providers - Trends

Rapid adoption of mobile based teleconsultation applications

Integration of wearable health monitoring devices with telemedicine platforms - Government Regulations

Telemedicine practice guidelines issued by the Ministry of Health

Health data protection and cybersecurity regulations

Licensing frameworks for telemedicine service providers - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Real Time Video Consultation Platforms

Store and Forward Telemedicine Systems

Remote Patient Monitoring Systems

Mobile Telemedicine Applications

AI Enabled Teleconsultation Platforms - By Platform Type (In Value%)

Hospital Integrated Telemedicine Platforms

Cloud Based Telemedicine Platforms

Government Telehealth Service Platforms

Mobile Health Teleconsultation Platforms

Wearable Device Integrated Telemedicine Platforms - By Fitment Type (In Value%)

Standalone Telemedicine Applications

Integrated Hospital Telemedicine Systems

Cloud Hosted Telemedicine Infrastructure

AI Enabled Clinical Teleconsultation Systems - By End User Segment (In Value%)

Hospitals and Multi Specialty Clinics

Diagnostic Centers and Laboratories

Individual Patients and Remote Healthcare Users

- Market Share Analysis

- Cross Comparison Parameters (Consultation Platform Capability, Data Security Compliance, Integration with Hospital Systems, AI Assisted Diagnostic Support, Teleconsultation Quality)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Seha Virtual Hospital

Altibbi

Vezeeta

Okadoc

Teladoc Health

Cerner Corporation

Epic Systems

Philips Healthcare

Siemens Healthineers

IBM Watson Health

GE HealthCare

Medtronic Digital Health

Healthigo

Doctify

Tawuniya Digital Health

- Hospitals deploying telemedicine platforms to extend healthcare outreach

- Diagnostic centers using telemedicine for remote reporting and consultations

- Patients adopting digital consultations for convenience and accessibility

- Insurance providers integrating telemedicine services for preventive healthcare programs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now