Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA tennis equipment market is valued at approximately USD ~ million, driven by factors like increasing interest in sports and fitness, alongside a surge in participation in tennis across the kingdom. The rise in disposable income and a growing middle class are also major contributors. Retailers have noted strong demand from both the recreational sector and emerging professional players. The increasing number of tennis academies, clubs, and the investment in infrastructure further bolsters the market. With strong support from local communities and sports initiatives, the market is well-positioned for growth.

Riyadh, Jeddah, and Dammam are the dominant cities in the KSA tennis equipment market due to their dense population, higher per capita income, and the establishment of several high-profile tennis events, which increase visibility and engagement. Riyadh, as the capital, has the highest concentration of tennis clubs and academies. Jeddah, being a major port city, benefits from strong international trade connections, making tennis equipment more accessible. Dammam, with a growing sports culture, is seeing an increase in tennis participation, particularly among youth, and the government’s investment in sports infrastructure enhances its position.

Market Segmentation

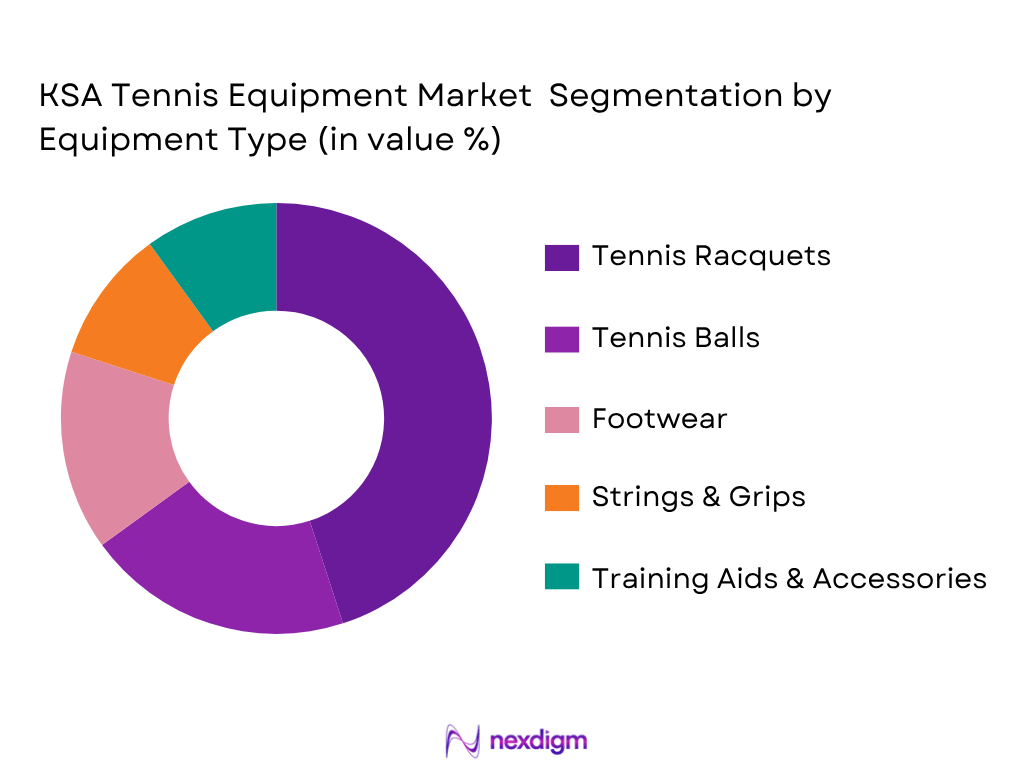

By Equipment Type

The KSA tennis equipment market is segmented by product type into tennis racquets, tennis balls, footwear, strings & grips, and training aids & accessories. The dominant segment in this category is tennis racquets. Racquets are a core product for tennis players, from beginners to professionals. This segment continues to grow due to the continuous innovation in racquet technology, such as lightweight materials and advanced grip designs. Major global brands like Wilson, Head, and Babolat dominate this category, leveraging brand loyalty and technological advancements to maintain their leadership. Racquets’ market share in 2024 is expected to account for 45%.

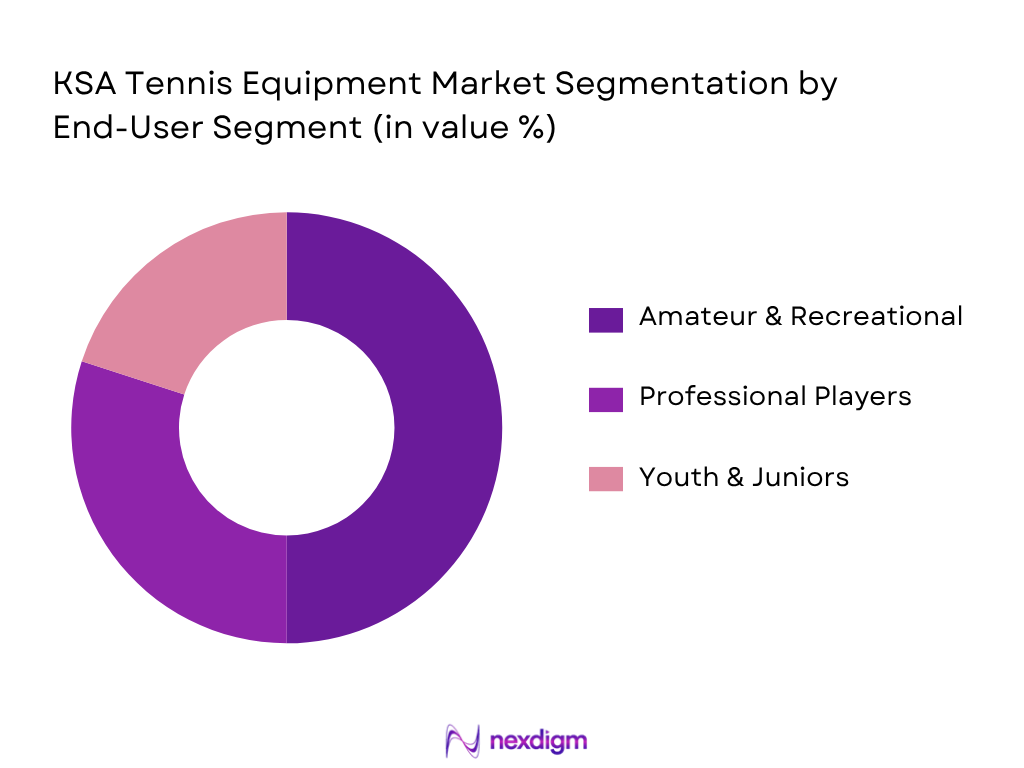

By End-User Segment

The market is also segmented by end-user type, including professional players, amateur & recreational players, and youth & juniors. The amateur & recreational segment dominates due to the widespread adoption of tennis as a recreational activity. This segment is driven by the growing number of tennis clubs, fitness centers, and social initiatives promoting the sport. Additionally, the lower cost of equipment for casual players and the increasing awareness about the health benefits of playing tennis have fueled the growth of this segment. In 2024, this segment is expected to hold a market share of 50%.

Competitive Landscape

The KSA tennis equipment market is dominated by both international and local players, including brands such as Wilson, Head, Babolat, Prince, and Yonex. These global companies maintain their stronghold in the market due to their high-quality products, strong distribution networks, and established brand recognition. The competitive landscape also includes local distributors and retailers who focus on providing affordable alternatives to international brands. These companies are capitalizing on the growing interest in tennis, both in the recreational and professional sectors, by enhancing their product offerings and expanding into new regions within the kingdom.

| Company Name | Establishment Year | Headquarters | Product Portfolio | Regional Reach | Distribution Channels | Online Sales Penetration | Price Range |

| Wilson Sporting Goods | 1914 | USA | ~ | ~ | ~ | ~ | ~ |

| Head Sport GmbH | 1950 | Austria | ~ | ~ | ~ | ~ | ~ |

| Babolat | 1875 | France | ~ | ~ | ~ | ~ | ~ |

| Prince Global Sports | 1970 | USA | ~ | ~ | ~ | ~ | ~ |

| Yonex Co. Ltd. | 1946 | Japan | ~ | ~ | ~ | ~ | ~ |

KSA Tennis Equipment Market Analysis

Growth Drivers

Growth in Tennis Participation Rate

Tennis participation in Saudi Arabia has been increasing, providing a tangible demand impetus for tennis equipment products such as racquets, balls, footwear, and gear. According to national sports club data, there are 177 tennis clubs operating across the Kingdom, which represents a significant rise in organized tennis infrastructure compared with prior years; this expansion correlates with a growing base of registered players now exceeding 2,300 participants, with the under‑14 cohort increasing from 500 to over 1,000 youth players effectively doubling in recent years. The surge in organized participation directly stimulates equipment purchases among both recreational players and academy programs focused on youth development. This foundational growth in participation creates ongoing demand for a diversity of equipment from entry‑level gear to performance‑oriented products used in structured coaching environments. Such participation figures reflect a broader national tilt towards sports engagement as part of public health and lifestyle trends, which supports a more consistent demand stream for the tennis equipment supply chain across Saudi cities.

Expansion of Tennis Academies and Coaching Infrastructure

The structured expansion of tennis academies and coaching infrastructure in Saudi Arabia underpins the demand ecosystem for tennis equipment. The growth of formal coaching institutions and athletic programs provides a channel for recurrent equipment procurement by both institutions and individual players. For example, sports development initiatives have resulted in the establishment of dedicated facilities focused on youth and high‑performance training, fostering deeper engagement with the sport. In Riyadh and other major urban centers, public and private academies including those tied to national sports federations have introduced systematic training programs. This translates into continuous institutional sourcing of racquets, balls, performance footwear, fitness accessories, and training aids to support structured coaching regimes. These developments are supported by broader macro participation data, with Saudi national statistics indicating that 17.4% of individuals aged 15 years and over engage in sports activities for more than 150 minutes per week, reflecting an upward trend in structured sport participation that benefits tennis as an emerging focus area.

Market Challenges

Supply Chain Disruptions and Import Dependency

One of the principal structural challenges for the KSA tennis equipment market relates to its heavy reliance on inbound imports of finished products and components. Saudi Arabia does not have a locally integrated manufacturing base for most tennis equipment categories, causing retailers and distributors to depend on international supply chains originating from Europe, North America, and East Asia. When global transportation costs fluctuate or when logistical bottlenecks occur, such as port congestion or disruptions related to geopolitical tensions, these effects propagate into the Saudi retail ecosystem, leading to delayed product availability, stock shortages, and inventory imbalances. For example, delays in maritime freight from key manufacturing hubs can extend lead times from typical multi‑week windows to over two months, affecting seasonal inventory cycles. Moreover, retailers often face additional import processing and compliance requirements, which can compound delivery timelines and elevate inventory carrying costs. In markets with such import dependency, any disruptions in upstream supply, whether due to factory shutdowns, raw material shortages, or transportation delays, directly impact retail availability and consumer choice within the tennis equipment category, constraining consistent market responsiveness.

Seasonal Demand Fluctuations

Demand for tennis equipment in Saudi Arabia is influenced by seasonal variations in sports participation and consumer purchasing behavior, presenting challenges for inventory planning and sales forecasting. Seasonal demand spikes typically align with school and academic calendars, holiday periods, and the scheduling of prominent sporting events, where participation and interest in tennis rise due to increased availability of leisure time among youth and adults. Conversely, demand tends to soften during the peak summer months when extreme heat can reduce outdoor participation, necessitating adjustments in procurement strategies and marketing efforts. Retailers must plan inventory well in advance of peak demand windows, often carrying significant stock over slower periods, which increases holding costs and the risk of unsold inventory if anticipated seasonal uptake underperforms. Consumer footfall and online traffic can also vary substantially across seasons, driven more broadly by macro consumption patterns in Saudi Arabia’s broader retail environment. For instance, national retail and e‑commerce performance data show large fluctuations in purchase activity linked to cultural and holiday periods, forcing retailers to calibrate strategies to optimize turnover while managing variable demand for sports goods like tennis equipment.

Market Opportunities

Growth in Digital Retail

Digital retail expansion in Saudi Arabia presents a structural opportunity for the tennis equipment market by broadening channel access and consumer reach. The Kingdom’s online commerce ecosystem has rapidly expanded, with the Saudi e‑commerce market reported at USD 222.9 billion in 2024, reflecting the larger shift of consumer purchasing behavior toward digital platforms. Near‑universal internet access, with approximately 33.6 million active e‑commerce users, enhances the potential customer base reachable through online sporting goods channels. Platforms such as Amazon.sa, Noon.com, and specialized sports e‑retailers enable domestic buyers to explore a wider range of tennis equipment options, often with enhanced convenience and delivery speed compared with traditional retail. The growth of digital retail infrastructure is supported by robust digital payment adoption and logistics enhancements, enabling greater penetration of tennis equipment products beyond major cities into secondary markets within the Kingdom. For distributors and brands, this translates into the ability to scale direct‑to‑consumer offerings, implement targeted online promotions, and leverage mobile commerce trends to capture incremental demand from digitally engaged consumer segments. Consequently, digital retail serves as a critical growth vector for expanding market access in the tennis equipment category.

Emergence of Custom/Performance-oriented Products

In the KSA tennis equipment market, there is a discernible shift toward specialized and performance‑oriented products that cater to nuanced consumer demands beyond basic recreational gear. As participation deepens and players seek competitive or advanced recreational play, demand for premium rackets, high‑performance footwear, and customized strings/grips rises. Trends in consumer behavior indicate that buyers increasingly evaluate equipment based on technological features, weight profiles, ergonomics, and materials science innovations that enhance playability and durability. This demand trajectory is supported by broader retail dynamics, as digital and traditional retailers now stock expanded selections of performance brands and customization options in response to global consumer preferences. Given the relatively high internet and mobile penetration rates — where Saudi users rely on digital research and peer reviews for product decisions — brands can leverage e‑commerce data to tailor offerings and configuration options that meet specific play style preferences. The presence of youth academies and competitive coaching environments amplifies demand for these differentiated products, as players and coaches seek equipment that aligns with performance benchmarks established in regional and international competition frameworks.

Future Outlook

The KSA tennis equipment market is expected to show significant growth over the next decade, driven by government sports initiatives, increased sports participation, and technological innovations in equipment. The rising popularity of tennis, especially among youth, combined with the growing middle class and rising disposable incomes, is expected to fuel demand. Additionally, the ongoing expansion of tennis academies and clubs across the kingdom, along with professional events, will further boost the market’s growth trajectory. Innovations in smart tennis equipment and the integration of digital tools to track performance will continue to influence consumer preferences, offering more personalized experiences and helping to push the market forward.

Major Players

- Wilson Sporting Goods

- Head Sport GmbH

- Babolat

- Prince Global Sports

- Yonex Co. Ltd.

- Dunlop

- Tecnifibre

- Slazenger

- Nike, Inc.

- Adidas AG

- ASICS Corporation

- New Balance

- Li-Ning

- Puma

- Under Armour

Key Target Audience

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Tennis Clubs and Academies

- Distributors and Retailers of Sports Equipment

- E-commerce Platforms

- Fitness Centers and Wellness Clubs

- Sporting Goods Manufacturers

- Event Organizers and Sponsors

Research Methodology

Step 1: Identification of Key Variables

The first step involves mapping the ecosystem of all stakeholders within the KSA tennis equipment market. This includes identifying key market participants such as manufacturers, retailers, distributors, and consumers. Through a combination of secondary research and proprietary databases, we define and categorize critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

This phase compiles and analyzes historical data about market trends and demand patterns, such as the penetration rates of different product categories and regional distribution. Key performance indicators (KPIs) like unit sales, average prices, and consumer demand across segments are scrutinized to provide an accurate view of market size and growth.

Step 3: Hypothesis Validation and Expert Consultation

Once market hypotheses are developed, they are validated through interviews with industry experts and stakeholders. This step includes phone interviews, online surveys, and interactions with local distributors and manufacturers. Insights from these consultations help refine assumptions and ensure the credibility of the market data.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing data from the previous steps into a comprehensive market report. This involves direct engagement with key industry players to verify consumer preferences, purchasing behaviors, and market trends, ensuring that the report’s findings are accurate, reliable, and actionable for business stakeholders.

- Executive Summary

- Research Methodology (Market Definitions and Reporting Standards, Data Sources and Assumptions, Domestic vs Import Balance Methodology, Exchange Rate & Tariff Adjustment Approaches, Primary Field Intake: Retailers, Clubs, Distributors, E‑Commerce Panels, Supply‑Side, Limitations & Risk Controls)

- Scope and Market Definition

- Industry Genesis & Evolution

- Global vs KSA Demand Dynamics Comparison

- Tennis Participation & Grassroots Promotion

- Equipment Usage Patterns

- Supply Chain & Value Chain Analysis

- Growth Drivers (Growth in Tennis Participation Rate, Expansion of Tennis Academies & Coaching Infrastructure, Rising Disposable Income, Premium Sports Consumption Trends, Government Initiatives and Sports Tourism Promotion)

- Market Challenges (Supply Chain Disruptions & Import Dependency, Seasonal Demand Fluctuations, High Cost of Premium Equipment vs Price Sensitivity, Competitive Pricing Pressure from E-commerce)

- Market Opportunities (Growth in Digital Retail & Omni-channel Experiences, Emergence of Custom/Performance-oriented Products, Institutional Procurement (Schools, Sports Leagues, Federations), Partnerships Between Brands and Local Clubs)

- Market Trends (Smart Equipment & Sensor Integration, Sustainability in Materials & Packaging, Athlete-centric Product Differentiators, Localized Product Mix Adaptation)

- Regulatory and Trade Environment (Import Tariffs & Free Trade Agreements, Compliance Standards, Sports Federation Policy Impact, Intellectual Property and Branding Enforcement)

- SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats of the KSA tennis equipment market)

- Stakeholder Ecosystem (Relationships among manufacturers, distributors, retail chains, sports federations, tennis clubs, and coaches)

- Porter’s Five Forces (Competitive Rivalry, Supplier Power (e.g. material suppliers), Buyer Power, Threat of New Entrants (niche sports tech startups), Threat of Substitutes)

- By Market Value in KSA (2020-2025)

- By Market Volume (2020-2025)

- By Average Selling Price per Product Category (2020-2025)

- By Per Capita Equipment Consumption Estimates (2020-2025)

- By Domestic Production vs Import Trade Gap (2020-2025)

- By Product Type (In Value%)

Tennis Racquets

Tennis Balls

Footwear

Strings & Grips

Training Aids & Accessories - By End‑User Segment (In Value%)

Professional Players

Amateur & Recreational

Youth & Juniors

Women & Female Players

Schools & Institutional Procurement - By Distribution Channel (In Value%)

Specialty Sports Retailers

Departmental/Supermarkets

E‑Commerce Platforms

Pro Shops & Club‑Affiliated Retail

Direct OEM/Bulk Corporate Sales - By Price Tier (In Value%)

Economy / Mass‑Market

Mid‑Range Performance

Premium / Pro‑Level Equipment - By Region Within KSA (In Value%)

Riyadh & Central Region

Western Region

Eastern Province

Southern Region

- Market Share Analysis (Value, Volume, Channel Breakdown)

- Cross Comparison Parameters (Company Profile, Business Model, Product Portfolio Breadth, R&D Intensity, Price Positioning, Distribution Footprint, E‑Commerce Penetration, Brand Penetration Index, SKU Count, Warranty & After‑Sales, Supply Chain Stability, Local Partnerships, Marketing Spend, Sustainability Practices)

- Pricing Analysis (Average selling prices and SKU-level pricing for major brands, premium vs standard product lines)

- SWOT of Major Players (Strengths, Weaknesses, Opportunities, Threats for key companies)

- Competitive Intelligence & Benchmarking (Pricing and Promotional Index, Product Launches & Innovation Pipeline, Retailer and Consumer Sentiment Analysis, Omni-channel Performance Scorecards)

- Detailed Profiles of Major Companies

Wilson Sporting Goods Co.

Head Sport GmbH

Babolat VS SAS

Yonex Co., Ltd.

Prince Global Sports LLC

Dunlop Sports

Tecnifibre

Slazenger

Nike, Inc.

Adidas AG

ASICS Corporation

New Balance Athletics Inc.

Li‑Ning Company Limited

Puma SE

Under Armour, Inc.

- Demand and Utilization (Sales breakdown by end-user type: recreational players vs professional athletes, club/academy purchases)

- Consumer Demographics and Purchasing Behavior (Age, income, gender distribution, purchasing frequency, channel preferences)

- Budget and Price Sensitivity (Pricing tiers: premium vs mid-range vs value segment, consumer spending patterns on equipment and apparel)

- Needs, Desires and Pain Points (Comfort, performance, and durability requirements, desire for brand/image, issues like gear availability or fitting)

- Decision-Making Process (Influencers in purchase decisions: coaches’ recommendations, peer reviews, online research, role of professional endorsements and demo clinics)

- By Value (2026-2035)

- By Volume (2026-2035)

- By Average Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now