Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The KSA Truck Aggregator market reached approximately USD ~ billion based on a recent historical assessment, driven by rapid expansion of digital freight platforms linking shippers with fragmented trucking fleets across the Kingdom. Strong demand from construction, industrial supply chains, and e-commerce logistics accelerated platform adoption, improving fleet utilization and reducing empty miles. Government-backed transport digitalization and logistics corridor development further strengthened aggregator penetration across domestic and cross-border freight operations.

Riyadh, Jeddah, and Dammam dominate the KSA Truck Aggregator market due to concentration of industrial production, port logistics, and consumption hubs requiring high freight mobility. Riyadh leads through central distribution networks and large construction activity, while Jeddah benefits from Red Sea port throughput and import logistics flows. Dammam’s petrochemical and manufacturing clusters sustain heavy haulage demand, encouraging aggregator deployment to optimize fleet coordination and regional freight connectivity across Eastern Province supply corridors.

Market Segmentation

By Service Type:

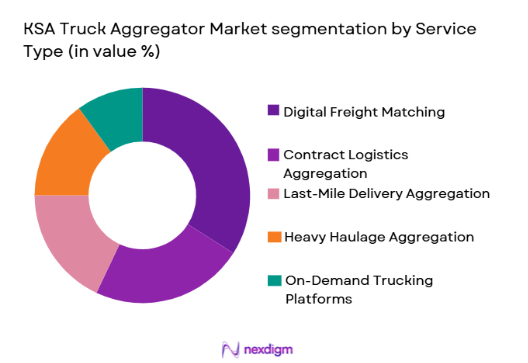

KSA Truck Aggregator market is segmented by service type into digital freight matching, contract logistics aggregation, last-mile delivery aggregation, heavy haulage aggregation, and on-demand trucking platforms. Recently, digital freight matching has a dominant market share due to factors such as strong SME shipper demand, widespread mobile platform accessibility, and need for real-time truck availability across fragmented fleets. Shippers increasingly prefer flexible spot-market bookings rather than long-term fleet ownership, while aggregators provide route optimization, pricing transparency, and faster dispatching that improve logistics efficiency across domestic and cross-border movements.

By End User:

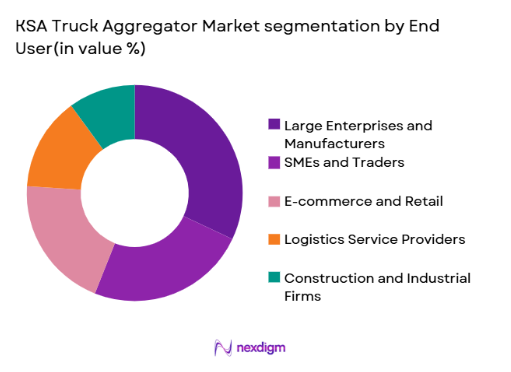

KSA Truck Aggregator market is segmented by end user into SMEs and traders, large enterprises and manufacturers, e-commerce and retail, logistics service providers, and construction and industrial firms. Recently, large enterprises and manufacturers have a dominant market share due to factors such as high freight volumes, integrated supply chain operations, and structured procurement requiring scalable logistics coordination. These firms adopt aggregators to optimize distribution between production sites, ports, and warehouses while ensuring visibility and compliance, generating sustained high-value contracts for digital trucking platforms across national freight corridors.

Competitive Landscape

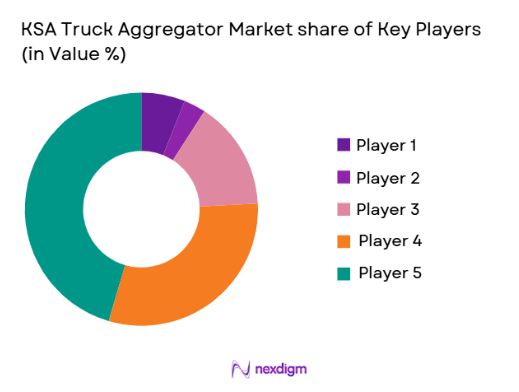

The KSA Truck Aggregator market shows moderate consolidation with regional digital freight platforms competing alongside logistics majors integrating aggregator capabilities into broader supply chain services. Leading players leverage large carrier networks, technology integration, and cross-border reach to secure enterprise contracts. Strategic partnerships with ports, industrial zones, and e-commerce distributors strengthen platform ecosystems, while smaller aggregators focus on niche freight categories or SME segments to maintain competitive relevance in a technology-driven logistics environment.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Network Scale |

| Trukker | 2016 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Trella | 2018 | Cairo | ~ | ~ | ~ | ~ | ~ |

| Naqel Express | 1993 | Riyadh | ~ | ~ | ~ | ~ | ~ |

| Aramex | 1982 | Dubai | ~ | ~ | ~ | ~ | ~ |

| Agility Logistics | 1979 | Kuwait | ~ | ~ | ~ | ~ | ~ |

KSA Truck Aggregator Market Analysis

Growth Drivers

National Logistics Digitalization Under Vision-Driven Infrastructure Programs:

explanation continues in the same sentence. The KSA Truck Aggregator market benefits significantly from nationwide logistics digitalization initiatives aimed at transforming transport efficiency and supply chain transparency across the Kingdom. Government infrastructure programs have expanded highways, logistics zones, and multimodal corridors, creating greater demand for coordinated trucking capacity and digital freight visibility. Aggregator platforms enable centralized booking, route optimization, and fleet monitoring that align with national goals of improving logistics performance and reducing transportation costs. Regulatory encouragement of digital documentation and electronic freight transactions further accelerates adoption among enterprises and carriers. Industrial diversification strategies promote manufacturing and mining sectors requiring scalable trucking coordination across regions. The shift toward integrated supply chain management encourages large shippers to outsource fleet management to aggregator platforms. Cross-border trade corridors with neighboring Gulf economies also require digital freight matching for efficiency. As logistics modernization advances, aggregators become essential intermediaries linking shippers, carriers, and infrastructure networks. These structural developments create sustained demand for platform-based trucking services across domestic and regional freight ecosystems.

E-commerce Expansion and Industrial Supply Chain Distribution Growth:

explanation continues in the same sentence. The KSA Truck Aggregator market experiences strong demand from expanding e-commerce fulfillment networks and industrial distribution systems requiring flexible freight capacity across urban and intercity routes. Rapid growth in online retail increases shipment frequency and last-mile requirements that aggregators efficiently coordinate through distributed trucking fleets. Warehousing expansion and fulfillment center development generate continuous regional cargo flows connecting ports, cities, and industrial clusters. Aggregators provide dynamic capacity allocation that supports seasonal demand spikes without permanent fleet investments by shippers. Manufacturing and construction supply chains also rely on reliable trucking availability for materials and equipment transport across the Kingdom. Platform-based freight procurement reduces idle capacity and improves load utilization, lowering logistics costs for enterprises. Integration with warehouse management and enterprise systems further embeds aggregators into supply chain operations. SME merchants increasingly adopt digital trucking services to access nationwide distribution networks. Combined growth of commerce and industrial logistics strengthens aggregator platform penetration across freight categories.

Market Challenges

Fragmented Trucking Fleet Structure and Carrier Digital Adoption Barriers:

The KSA Truck Aggregator market faces structural challenges due to highly fragmented trucking ownership dominated by small fleet operators with limited digital readiness. Many carriers lack advanced telematics, standardized processes, or technological integration needed for seamless participation in aggregator platforms. Resistance to digital booking and pricing transparency reduces network efficiency and limits real-time capacity visibility. Informal contracting practices persist across segments, complicating standardized aggregator transactions and compliance monitoring. Smaller operators often depend on traditional brokers, slowing transition toward digital freight matching ecosystems. Platform onboarding costs and training requirements further discourage adoption among independent drivers and micro-fleets. Inconsistent service quality and documentation from fragmented carriers affect aggregator reliability for enterprise customers. Geographic dispersion of carriers also creates coordination complexity in remote industrial regions. Without accelerated carrier digitization and consolidation, aggregator scalability and operational efficiency remain constrained across the national trucking landscape.

Pricing Pressure and Competitive Platform Economics in Freight Marketplaces:

The KSA Truck Aggregator market experiences margin challenges due to intense price competition among platforms and traditional logistics intermediaries competing for shipper contracts. Aggregators often prioritize network expansion and carrier acquisition, leading to discounted freight rates and reduced commission margins to attract users. Shippers benefit from pricing transparency and competitive bidding, limiting platform profitability despite rising transaction volumes. Volatile fuel costs and trucking operational expenses also pressure carrier pricing, reducing aggregator revenue potential. Entry of regional logistics firms with digital capabilities intensifies competition in enterprise freight segments. Platforms must continuously invest in technology, marketing, and network development, increasing operating costs. Lack of standardized pricing frameworks across routes and cargo types complicates sustainable rate management. Smaller aggregators struggle to achieve scale needed for profitable operations. Persistent pricing pressure challenges long-term economic sustainability of digital freight marketplaces in the Kingdom.

Opportunities

Integration with Multimodal Logistics Corridors and Regional Freight Networks:

The KSA Truck Aggregator market holds significant opportunity through integration with expanding multimodal transport corridors connecting ports, rail networks, and industrial logistics zones across the Kingdom. National logistics hub development increases intermodal freight flows requiring coordinated trucking for first-mile and last-mile connectivity. Aggregators can provide unified booking across transport modes, enhancing supply chain efficiency for exporters and importers. Regional Gulf trade integration further expands cross-border trucking demand accessible via digital platforms. Participation in bonded logistics zones and free trade corridors creates high-value freight opportunities for aggregators. Integration with port community systems and rail freight networks strengthens platform relevance across cargo movements. Enterprises seek seamless multimodal visibility, favoring aggregators offering end-to-end freight orchestration. Industrial cluster expansion in mining and manufacturing regions also generates corridor-based trucking demand. These developments position aggregators as central coordinators of multimodal logistics ecosystems across the Kingdom and GCC region.

Advanced AI-Driven Freight Optimization and Predictive Logistics Services:

The KSA Truck Aggregator market can expand through deployment of advanced artificial intelligence for predictive demand forecasting, route optimization, and dynamic pricing across trucking networks. AI enables accurate capacity planning based on historical freight flows, seasonal patterns, and industrial production cycles. Predictive analytics improves truck utilization by matching loads with available capacity across regions and time windows. Intelligent dispatching reduces empty miles and transit times, increasing carrier productivity and shipper cost efficiency. Aggregators offering analytics dashboards and supply chain insights gain strategic value for enterprise customers. Integration of IoT telematics and real-time tracking enhances data-driven decision-making across fleets. Predictive maintenance and driver performance analytics further improve network reliability. As logistics digital maturity increases, AI-enabled platforms differentiate through operational intelligence rather than basic brokerage functions. Adoption of advanced analytics services creates new revenue streams and competitive advantage for trucking aggregators in the Kingdom.

Future Outlook

The KSA Truck Aggregator market is expected to expand steadily over the next five years driven by logistics digitalization, e-commerce distribution growth, and industrial diversification. Technology adoption including AI routing and telematics integration will enhance efficiency and scalability of aggregator platforms. Regulatory support for digital freight documentation and transport modernization will further accelerate adoption. Increasing multimodal logistics integration and regional trade connectivity will strengthen demand for coordinated trucking services across domestic and cross-border supply chains.

Major Players

- Trukker

- Trella

- Naqel Express

- Aramex

- Agility Logistics

- SMSA Express

- Bahri Logistics

- Almajdouie Logistics

- Almarai Logistics

- Batic Logistics

- Wared Logistics

- GWC Logistics

- Fetchr Logistics

- LoadMe

- Salasa

Key Target Audience

- Logistics and transportation companies

- E-commerce retailers and marketplaces

- Manufacturing and industrial enterprises

- Construction and infrastructure firms

- Supply chain technology providers

- Government and regulatory bodies

- Investments and venture capitalist firms

- Freight forwarding and distribution companies

Research Methodology

Step 1: Identification of Key Variables

Primary variables including freight volumes, fleet availability, digital platform adoption, and logistics demand drivers were identified through sector mapping and transport ecosystem analysis across KSA trucking and logistics markets.

Step 2: Market Analysis and Construction

Market sizing and segmentation were constructed using freight demand modeling, platform transaction estimates, enterprise logistics adoption patterns, and supply chain activity indicators across industrial and commercial sectors.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions were validated through consultations with logistics operators, freight platforms, supply chain managers, and transport policy experts to ensure realistic representation of market dynamics and structural factors.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into structured analysis covering market size, segmentation, competition, and outlook, ensuring consistency with logistics sector trends and platform economy developments.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of e-commerce logistics demand

Vision 2030 transport digitalization initiatives

Rising cross-border GCC trade flows

Fleet utilization optimization needs

Growth in construction and industrial freight - Market Challenges

Fragmented trucking fleet ownership

Regulatory compliance complexities

Driver shortages and labor constraints

Limited digital adoption among SMEs

Price competition and margin pressure - Market Opportunities

Integration with multimodal logistics corridors

AI-enabled predictive freight optimization

Expansion into regional GCC aggregation networks - Trends

Shift toward real-time freight visibility platforms

Adoption of dynamic pricing logistics models

Integration with warehouse and fulfillment tech

Growth of contract-based digital freight

Increased use of telematics-driven dispatching - Government Regulations & Defense Policy

National transport digitalization frameworks

Cross-border freight compliance reforms

Logistics sector foreign investment policies - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Digital Freight Matching Platforms

Full-Service Logistics Aggregators

Last-Mile Delivery Aggregators

Heavy Haulage Aggregators

On-Demand Trucking Platforms - By Platform Type (In Value%)

Mobile App-Based Platforms

Web-Based Portals

API-Integrated Enterprise Platforms

Cloud Logistics Marketplaces

Telematics-Integrated Platforms - By Fitment Type (In Value%)

Standalone Aggregator Platforms

ERP-Integrated Solutions

Fleet Management Integrated Platforms

Marketplace Plug-in Modules

White-Label Aggregator Solutions - By EndUser Segment (In Value%)

SME Shippers

Large Enterprises and Manufacturers

E-commerce and Retail Companies

Logistics Service Providers

Construction and Industrial Firms - By Procurement Channel (In Value%)

Direct Platform Subscription

Enterprise Contracts

Government Logistics Tenders

Third-Party Logistics Partnerships

Digital Marketplace Enrollment - By Material / Technology (in Value %)

AI-Based Load Matching Algorithms

GPS and Telematics Integration

Cloud-Native Logistics Architecture

Blockchain Freight Documentation

IoT Fleet Monitoring Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Platform Capability, Fleet Network Size, Pricing Model Flexibility, Geographic Coverage, Integration Capability, Real-Time Tracking, Value-Added Services, Industry Focus, Technology Stack, Customer Segment Focus)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Trukker

Trella

TruckIt

Cargon

Blacklane Logistics

LoadMe

FretLink

Salasa

Fetchr Logistics

Aramex Freight Digital

GWC Logistics Digital

Agility Logistics Platforms

Bahri Logistics Digital

SMSA Express Freight

Naqel Digital Logistics

- SMEs increasingly adopt aggregators for cost-efficient freight access

- Large enterprises integrate aggregators into supply chain systems

- E-commerce firms rely on aggregators for last-mile scalability

- Industrial sectors use aggregators for project logistics flexibility

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now