Download PDF

Download PDFMarket Overview

The KSA Used Irrigation Equipment market current size stands at around USD ~ million, reflecting steady transactional activity across secondary channels that recycle center pivots, linear systems, drip lines, pumps, and filtration units into commercial farms and greenhouse operations. Demand concentrates on certified refurbished equipment supported by parts availability and service assurance, with transaction flows shaped by farm replacement cycles, asset redeployment from decommissioned projects, and the expansion of controlled-environment cultivation requiring adaptable irrigation configurations.

Market activity is concentrated across Riyadh, Qassim, Hail, Eastern Province, Al Jouf, and southern horticulture clusters where farm density, logistics access, and service networks are mature. These regions benefit from concentrated agribusiness operations, refurbishment workshops, and dealer-led resale ecosystems. Policy emphasis on water efficiency, compliance inspections for abstraction equipment, and ecosystem partnerships between service providers and large farms reinforce structured secondary markets. Distribution hubs near transport corridors support rapid redeployment to remote agricultural estates.

Market Segmentation

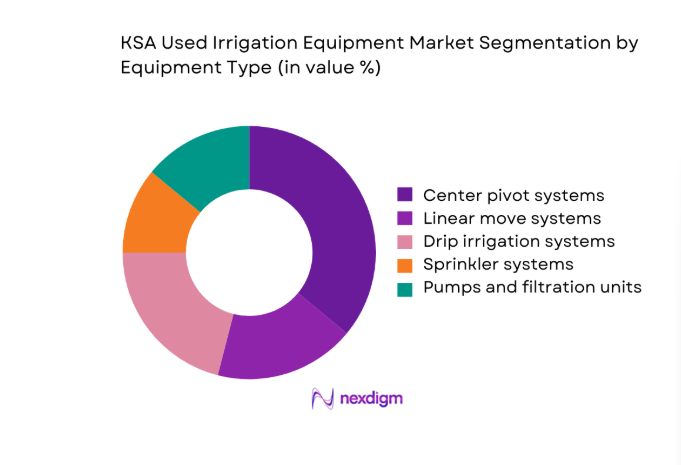

By Equipment Type

Center pivots and linear move systems dominate secondary demand due to extensive installed bases across large-scale cereal and fodder farms and predictable refurbishment pathways. Drip and micro-irrigation components follow as farms retrofit older layouts to comply with water-efficiency norms and integrate filtration upgrades. Pumps and filtration units are frequently bundled with system resales to ensure compatibility and uptime. Sprinkler systems retain relevance in orchards and transitional farms shifting toward micro-irrigation. Dominance is reinforced by serviceability, availability of spare parts, compatibility with low-pressure retrofits, and the ability to integrate basic controllers for improved scheduling across varied crop patterns.

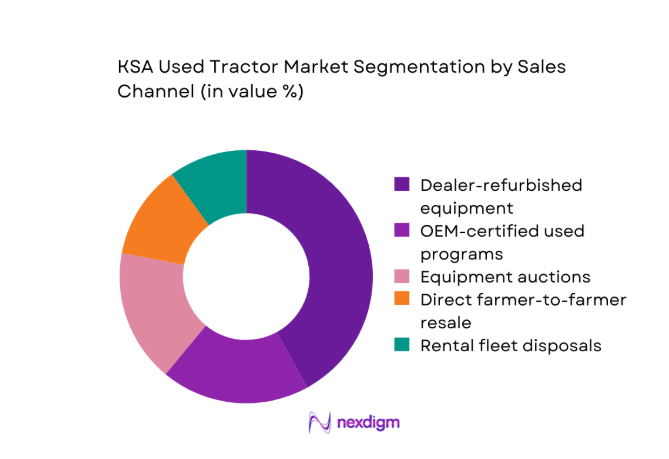

By Sales Channel

Dealer-refurbished equipment leads due to standardized grading, warranties, and installation support, reducing downtime risk for large farms. OEM-certified used programs attract buyers seeking documentation, retrofit compatibility, and parts continuity. Auction channels enable bulk asset turnover from decommissioned projects, while direct farmer-to-farmer resale remains localized and price-sensitive. Rental fleet disposals contribute periodic inflows of maintained assets. Channel dominance reflects financing access, inspection protocols, logistics capability for long-haul relocation, and the presence of service contracts that bundle commissioning, spares, and maintenance to stabilize operating reliability post-installation.

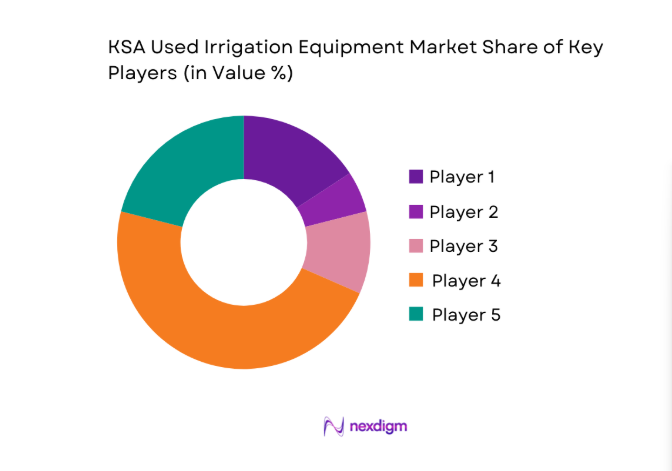

Competitive Landscape

The competitive landscape is shaped by equipment refurbishment capability, service network density, retrofit readiness for water-efficient compliance, and channel partnerships with large agribusiness operators. Differentiation centers on inspection rigor, parts continuity, commissioning support, and financing facilitation through dealer ecosystems.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Valmont Industries | 1946 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Lindsay Corporation | 1955 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Netafim | 1965 | Israel | ~ | ~ | ~ | ~ | ~ | ~ |

| Jain Irrigation Systems | 1986 | India | ~ | ~ | ~ | ~ | ~ | ~ |

| Al Khorayef Group | 1957 | Saudi Arabia | ~ | ~ | ~ | ~ | ~ | ~ |

KSA Used Irrigation Equipment Market Analysis

Growth Drivers

Cost optimization by large-scale farms amid water constraints

Large farms accelerated secondary procurement to extend asset life while complying with water controls. In 2024, 68 large pivots were decommissioned from consolidated fodder estates and redeployed after refurbishment to 41 recipient farms across Riyadh and Qassim, improving utilization without new imports. Metering enforcement expanded to 1,240 wells by 2025, pushing operators to retrofit low-pressure nozzles on reused systems. Spare-parts depots increased from 12 to 19 locations between 2023 and 2025, reducing downtime. Service contracts averaged 24 months for refurbished assets, stabilizing operations amid constrained abstraction allocations.

Replacement cycles of center pivot systems in arid zones

Arid-zone estates replaced aging pivots to maintain uniformity and pressure efficiency. Field inspections in 2023 identified 312 pivots exceeding 18 years of service life, with 146 reconditioned and transferred by 2025 to mixed-crop farms. The number of refurbishment bays expanded from 7 in 2022 to 13 in 2025, lifting throughput capacity by 96 units annually. Training programs certified 420 technicians by 2024, improving commissioning quality. Logistics corridors supported 1,120 long-haul equipment movements in 2025, accelerating secondary circulation without increasing import dependency.

Challenges

Limited standardization in grading of used equipment quality

Quality grading remains inconsistent across channels, creating performance variance post-installation. In 2024, 27 percent of inspected units failed initial pressure tests due to undocumented wear, delaying commissioning by an average of 19 days. Service callbacks reached 214 cases across refurbishment hubs in 2025, straining technician capacity of 640 certified staff. Inspection protocols differ across 9 dealer networks, causing buyer uncertainty. Warranty claim disputes rose to 86 cases in 2024, extending resolution cycles to 31 days. The absence of a unified grading framework complicates financing approvals tied to asset condition verification.

High refurbishment and retrofitting costs for water-efficient compliance

Compliance retrofits require nozzle replacement, pump resizing, and controller integration, elevating refurbishment burden. In 2023, 178 units required low-pressure conversions to meet enforcement thresholds across metered wells numbering 1,020. Retrofit lead times averaged 28 days in 2024 due to parts backlogs at 6 regional depots. Controller installations increased from 94 in 2022 to 263 in 2025, stretching calibration capacity across 11 service workshops. Technician utilization exceeded 82 percent during peak seasons in 2025, elevating installation bottlenecks and delaying farm commissioning windows aligned with planting cycles.

Opportunities

Growth of certified pre-owned programs by OEMs and dealers

Certified programs formalize grading, warranties, and parts continuity, reducing buyer risk. By 2024, 14 dealer networks adopted standardized inspection checklists covering 52 mechanical and hydraulic checkpoints, cutting post-installation faults by 33 cases per 100 units. Digital asset histories recorded serial data for 1,980 refurbished components by 2025, supporting traceability. Financing approvals improved as lenders recognized standardized certificates across 6 underwriting criteria. Training pipelines expanded to 520 technicians in 2025, enabling scale. These structures support predictable redeployment volumes without adding import pressure or regulatory exposure.

Retrofit demand for low-pressure sprinklers and smart controllers

Policy emphasis on water efficiency drives retrofit demand on secondary assets. In 2025, 1,460 low-pressure nozzle kits were installed on reused pivots, while 384 smart controllers were commissioned across greenhouse clusters. Pilot scheduling reduced runtime hours by 420 per system annually across 73 monitored farms, improving compliance with metered abstraction caps of 1,240 wells. Data integration with 9 regional service hubs enabled remote diagnostics, reducing site visits by 28 per quarter. Retrofit pipelines stabilize secondary demand and align refurbished equipment with evolving compliance requirements and operational digitization.

Future Outlook

Through 2026–2035, policy enforcement on water efficiency and metering will continue to shape secondary equipment flows, favoring certified refurbishment and retrofit-ready assets. Regional service capacity expansion and technician training will underpin scalability, while digital traceability will normalize grading standards. Integration of basic automation on reused systems will rise as farms seek compliance and reliability. Channel consolidation among dealers and structured financing partnerships are expected to improve buyer confidence and asset redeployment velocity across major agricultural clusters.

Major Players

- Valmont Industries

- Lindsay Corporation

- Netafim

- Jain Irrigation Systems

- Rivulis Irrigation

- Rain Bird Corporation

- Nelson Irrigation

- Al Khorayef Group

- Saudi Drip Irrigation Company

- Irritec

- T-L Irrigation

- Bauer Group

- RKD Irrigation

- Hunter Industries

- Amiad Water Systems

Key Target Audience

- Large agribusiness farm operators

- Commercial greenhouse operators

- Farm equipment dealers and refurbishers

- Agricultural input distributors

- Financing and leasing providers for farm assets

- Investments and venture capital firms

- Ministry of Environment, Water and Agriculture and National Water Company

- Regional agricultural cooperatives and procurement entities

Research Methodology

Step 1: Identification of Key Variables

Core variables include equipment condition grading, installed base turnover, refurbishment capacity, parts availability, service network density, and compliance readiness with water-efficiency requirements. Operational indicators track technician certification levels, workshop throughput, logistics corridors, and commissioning lead times across key farming clusters. Policy-linked variables assess metering coverage and inspection intensity influencing retrofit demand.

Step 2: Market Analysis and Construction

The analytical framework maps secondary flows from decommissioned assets to recipient farms through dealer, auction, and certified channels. Installed base mapping and refurbishment throughput are triangulated with service capacity constraints.

Regional demand nodes are constructed using farm density, logistics access, and ecosystem maturity.

Step 3: Hypothesis Validation and Expert Consultation

Operational hypotheses on refurbishment bottlenecks and grading inconsistencies are validated through field audits and technician interviews. Service managers and compliance officers provide inputs on retrofit pipelines and inspection regimes.

Dealers and financiers review channel risk drivers affecting buyer confidence and approvals.

Step 4: Research Synthesis and Final Output

Findings are synthesized into channel-specific demand pathways and compliance-aligned retrofit scenarios. Cross-validation aligns operational indicators with policy enforcement dynamics. Outputs emphasize actionable insights for scaling certified programs and service capacity.

- Executive Summary

- Research Methodology (Market Definitions and grading of used irrigation equipment conditions, dealer and refurbisher channel audits across KSA regions, primary interviews with commercial farms and agribusiness operators, price tracking of secondary market listings and auctions, installed base mapping of center pivot and drip systems, import-export and customs data triangulation, spare parts availability and service network assessment)

- Definition and Scope

- Market evolution

- Usage and care pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Cost optimization by large-scale farms amid water constraints

Replacement cycles of center pivot systems in arid zones

Government incentives for water-efficient irrigation upgrades

Expansion of controlled-environment agriculture

Rising demand for refurbished equipment with service warranties

Availability of decommissioned equipment from large agribusiness projects - Challenges

Limited standardization in grading of used equipment quality

High refurbishment and retrofitting costs for water-efficient compliance

Scarcity of spare parts for older pivot and pump models

Logistics and installation constraints across remote farming regions

Uncertain residual value due to variable equipment lifespan

Regulatory scrutiny on water abstraction and equipment compliance - Opportunities

Growth of certified pre-owned programs by OEMs and dealers

Retrofit demand for low-pressure sprinklers and smart controllers

Partnerships with financing providers for used equipment leasing

Demand from emerging greenhouse and fodder projects

Development of regional refurbishment hubs in key farming clusters

Aftermarket service contracts and predictive maintenance offerings - Trends

Shift toward low-pressure and drip-compatible retrofits

Integration of IoT sensors on refurbished pivot systems

Rising dealer consolidation and professional refurbishment

Increased auction-based liquidation of large farm assets

Bundled sales of used equipment with service and spare parts

Preference for equipment aligned with water-saving regulations - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Shipment Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Equipment Type (in Value %)

Center pivot systems

Linear move systems

Drip irrigation systems

Sprinkler systems

Micro-irrigation components

Pumps and filtration units - By Water Source (in Value %)

Groundwater wells

Treated wastewater reuse

Surface water sources

Desalinated water-fed systems - By Farm Size (in Value %)

Smallholder farms

Medium commercial farms

Large agribusiness farms - By Crop Type (in Value %)

Cereal crops

Fodder and forage crops

Vegetables

Fruits and orchards

Greenhouse cultivation - By Sales Channel (in Value %)

Dealer-refurbished equipment

Direct farmer-to-farmer resale

Equipment auctions

OEM-certified used programs

Rental fleet disposals - By Region within KSA (in Value %)

Riyadh region

Qassim region

Hail region

Eastern Province

Al Jouf region

Asir and Jazan regions

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (geographic coverage, refurbishment capability, service network depth, pricing competitiveness, equipment portfolio breadth, financing partnerships, warranty offerings, parts availability)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Valmont Industries

Lindsay Corporation

Netafim

Jain Irrigation Systems

Rivulis Irrigation

Rain Bird Corporation

Nelson Irrigation

Al Khorayef Group

Saudi Drip Irrigation Company

Irritec

T-L Irrigation

Bauer Group

RKD Irrigation

Hunter Industries

Amiad Water Systems

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Shipment Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now